Texas Service Sector Outlook Survey

Growth in Texas service sector activity continues

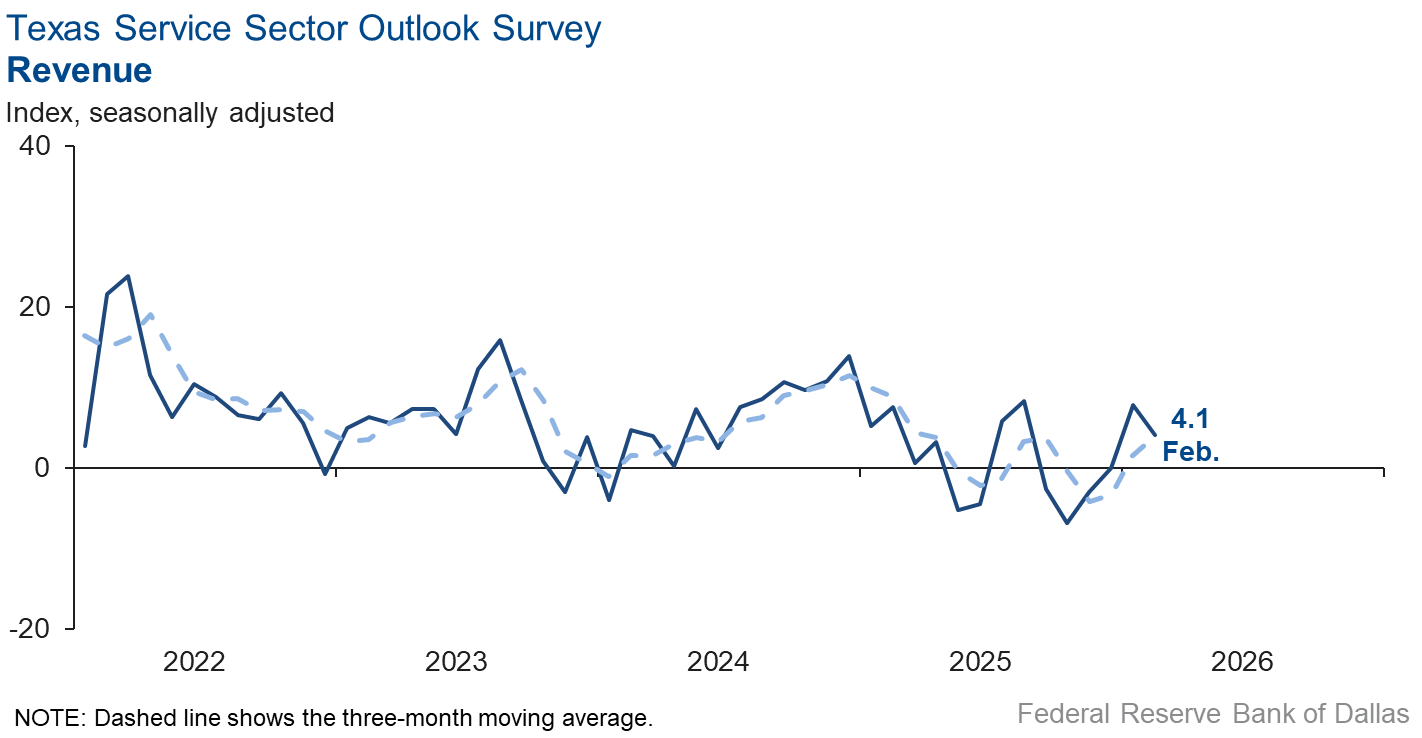

Texas service sector activity grew slightly in February, according to business executives responding to the Texas Service Sector Outlook Survey. The revenue index, a key measure of state service sector conditions, ticked down four points but remained in positive territory at 4.1.

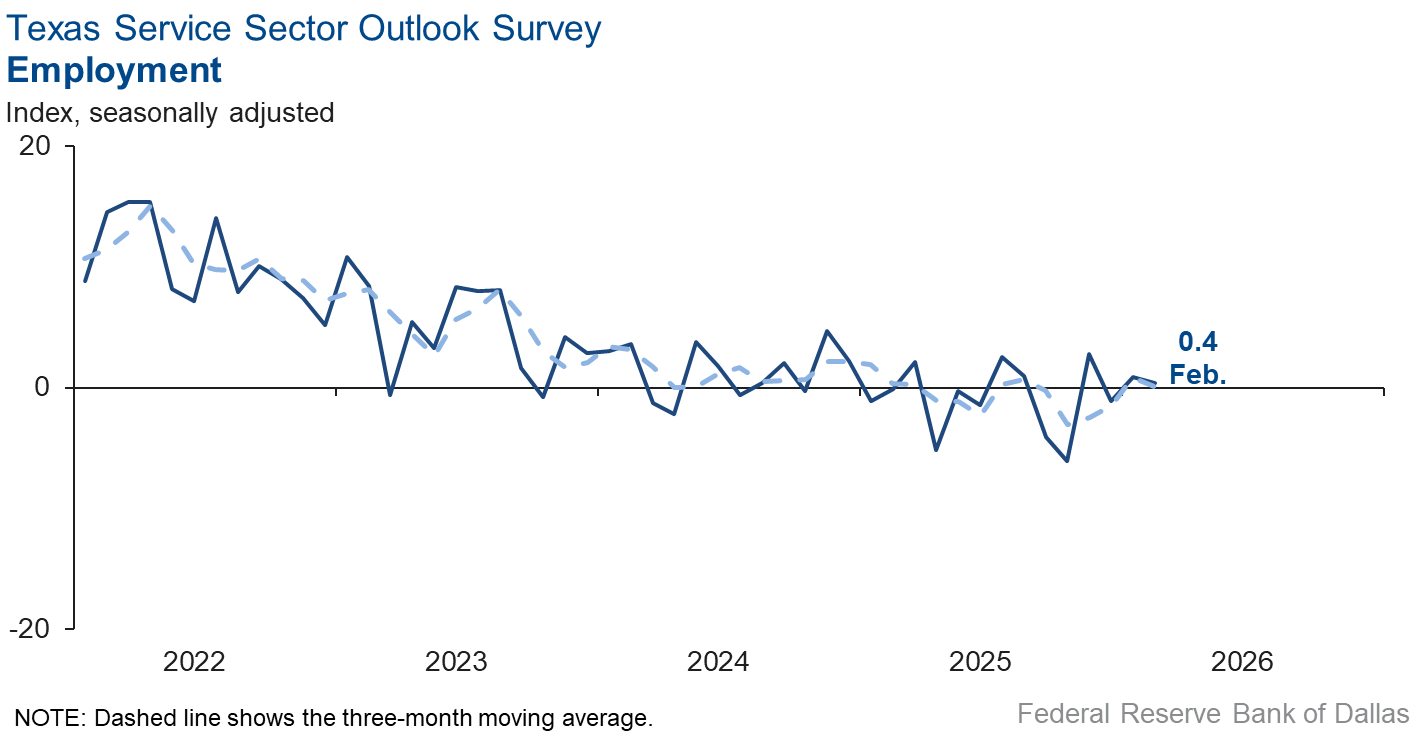

Labor market measures suggested little change in employment, though hours worked contracted slightly. Both the employment and part-time employment indexes registered near-zero readings, suggesting little change in February. The hours worked index declined four points to -2.7.

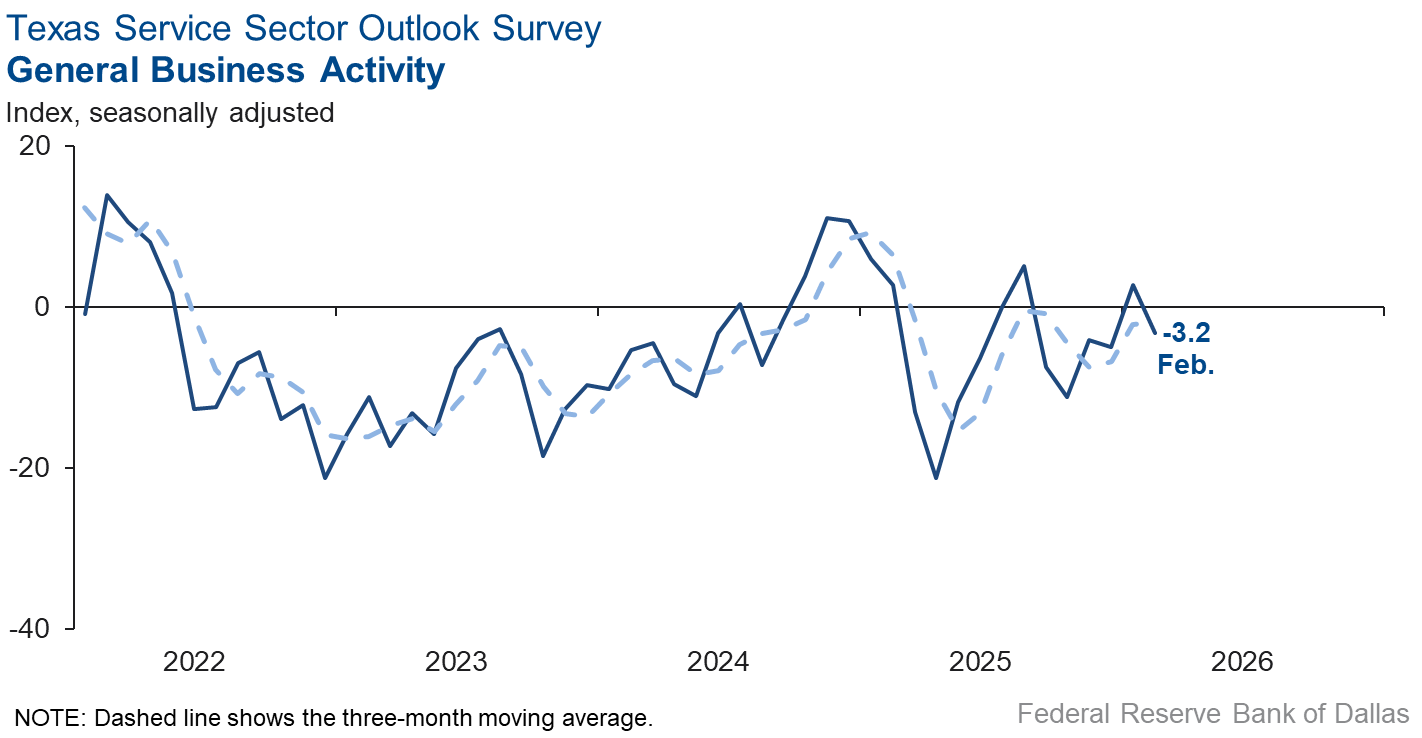

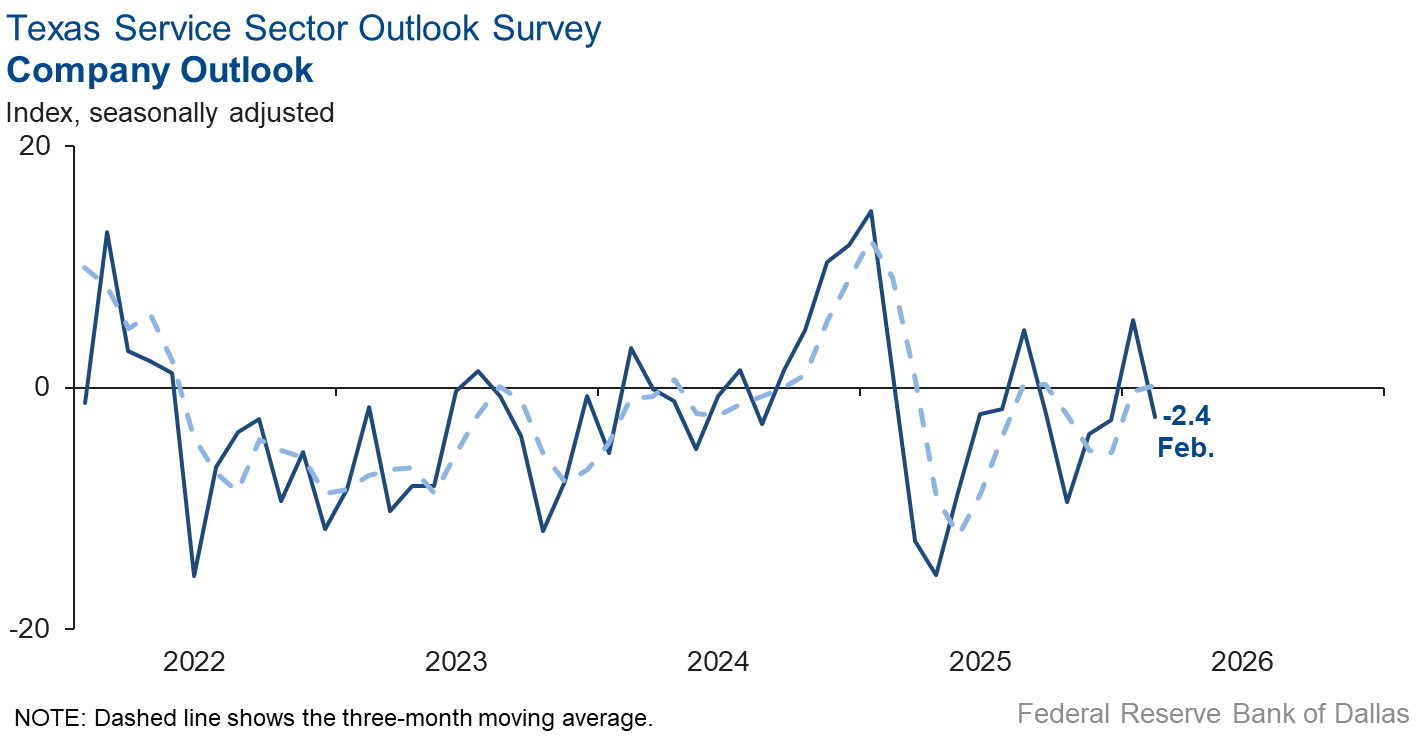

Perceptions of broader business conditions worsened slightly. The general business activity index fell to -3.2 from 2.7 in January. The company outlook index also declined, falling eight points to -2.4. Meanwhile, the outlook uncertainty index fell seven points to 9.3, its lowest reading since January 2025.

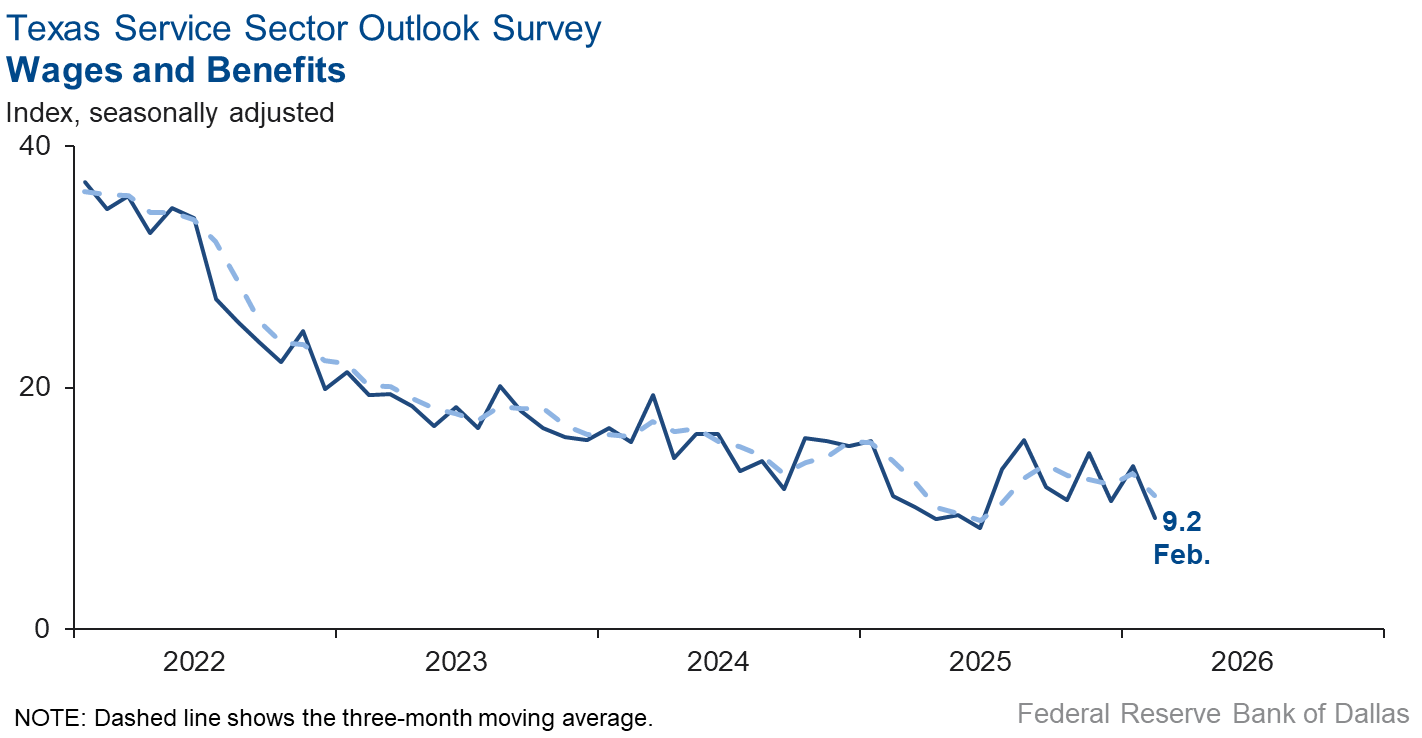

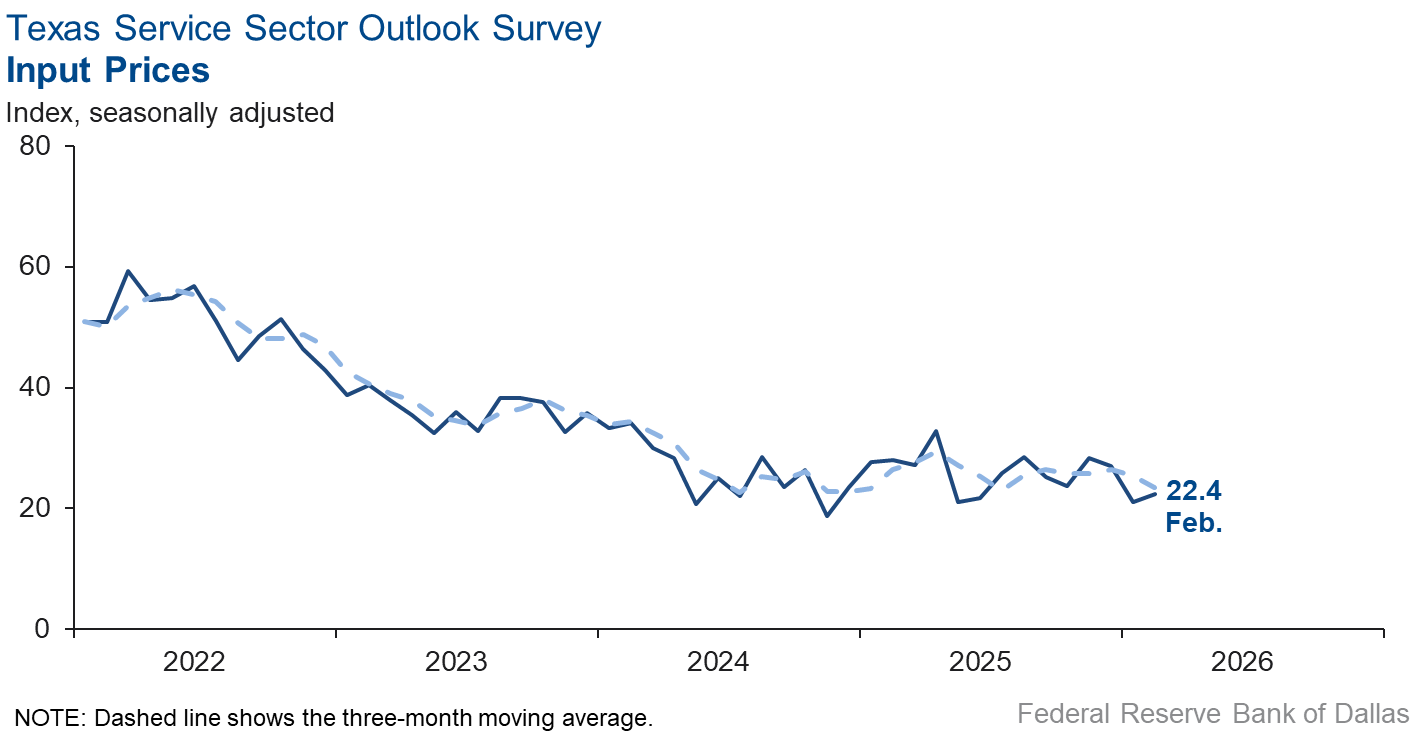

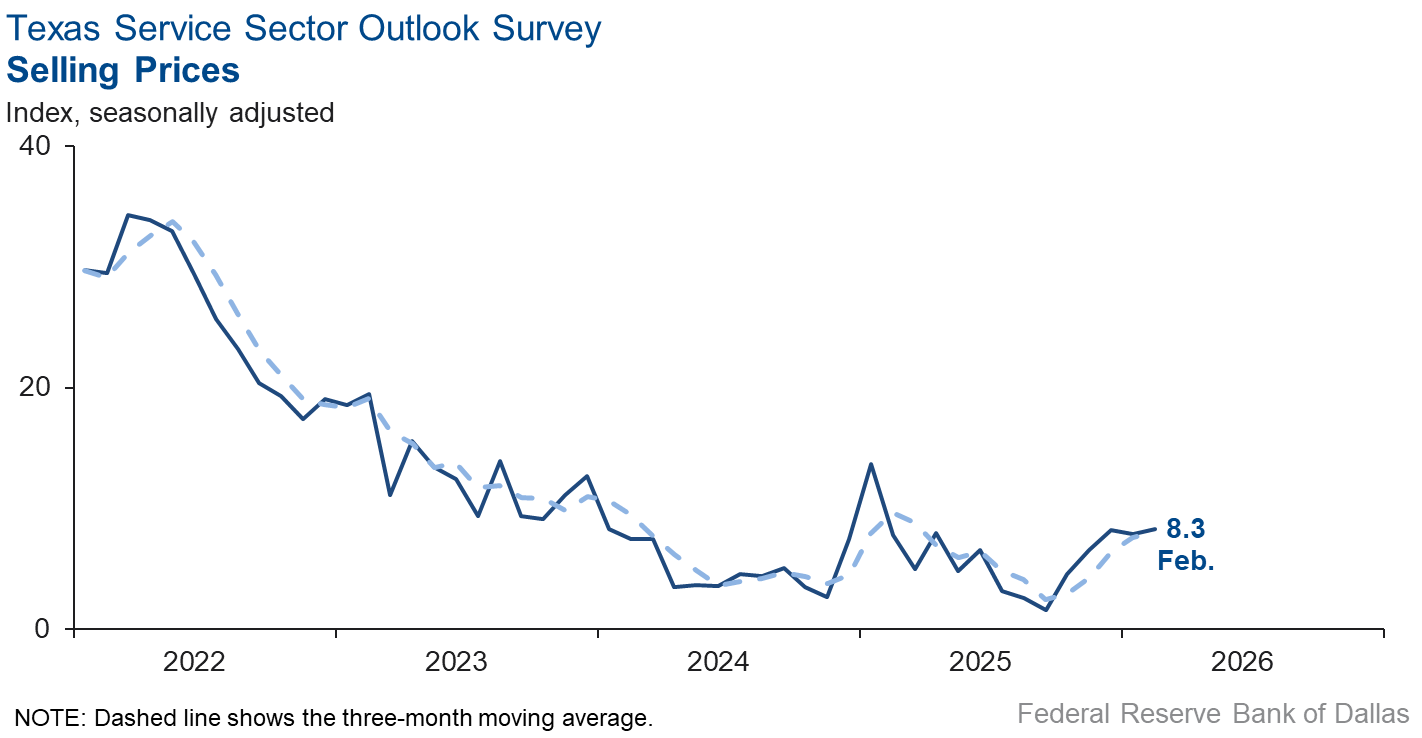

Input and selling prices rose at about the same pace as in January. The input and selling prices indexes were little changed, registering 22.4 and 8.3, respectively. The wages and benefits index fell four points to 9.2.

Respondents’ expectations regarding future service sector activity continued to improve. The future revenue index ticked down three points to 38.3, though it still remained in-line with the series average of 37.2. The future general business activity index was little changed at 15.0. Other future service sector activity indexes, such as employment and capital expenditures, remained in solidly positive territory.

Next release: March 31, 2026

Data were collected Feb. 10–18, and 240 of the 347 Texas service sector business executives surveyed submitted responses. The Dallas Fed conducts the Texas Service Sector Outlook Survey monthly to obtain a timely assessment of the state’s service sector activity. Firms are asked whether revenue, employment, prices, general business activity and other indicators increased, decreased or remained unchanged over the previous month.

Survey responses are used to calculate an index for each indicator. Each index is calculated by subtracting the percentage of respondents reporting a decrease from the percentage reporting an increase. When the share of firms reporting an increase exceeds the share reporting a decrease, the index will be greater than zero, suggesting the indicator has increased over the prior month. If the share of firms reporting a decrease exceeds the share reporting an increase, the index will be below zero, suggesting the indicator has decreased over the prior month. An index will be zero when the number of firms reporting an increase is equal to the number of firms reporting a decrease.

Data have been seasonally adjusted as necessary.

Historical data are available from January 2007 to the most current release month.

| Business Indicators Relating to Facilities and Products in Texas Current (versus previous month) | ||||||||

| Indicator | Feb Index | Jan Index | Change | Series Average | Trend* | % Reporting Increase | % Reporting No Change | % Reporting Decrease |

Revenue | 4.1 | 7.8 | –3.7 | 10.0 | 2(+) | 25.1 | 53.9 | 21.0 |

Employment | 0.4 | 0.9 | –0.5 | 5.8 | 2(+) | 9.4 | 81.6 | 9.0 |

Part–Time Employment | –0.2 | 5.5 | –5.7 | 1.2 | 1(–) | 5.3 | 89.2 | 5.5 |

Hours Worked | –2.7 | 1.1 | –3.8 | 2.4 | 1(–) | 4.2 | 88.9 | 6.9 |

Wages and Benefits | 9.2 | 13.5 | –4.3 | 15.5 | 69(+) | 15.4 | 78.4 | 6.2 |

Input Prices | 22.4 | 21.1 | +1.3 | 27.7 | 70(+) | 27.2 | 68.0 | 4.8 |

Selling Prices | 8.3 | 7.9 | +0.4 | 7.4 | 67(+) | 17.5 | 73.4 | 9.2 |

Capital Expenditures | 4.5 | 6.8 | –2.3 | 9.7 | 67(+) | 12.8 | 78.9 | 8.3 |

| General Business Conditions Current (versus previous month) | ||||||||

| Indicator | Feb Index | Jan Index | Change | Series Average | Trend** | % Reporting Improved | % Reporting No Change | % Reporting Worsened |

Company Outlook | –2.4 | 5.6 | –8.0 | 3.9 | 1(–) | 14.0 | 69.6 | 16.4 |

General Business Activity | –3.2 | 2.7 | –5.9 | 1.9 | 1(–) | 14.0 | 68.8 | 17.2 |

| Indicator | Feb Index | Jan Index | Change | Series Average | Trend* | % Reporting Increase | % Reporting No Change | % Reporting Decrease |

Outlook Uncertainty | 9.3 | 16.5 | –7.2 | 13.8 | 57(+) | 20.0 | 69.2 | 10.7 |

| Business Indicators Relating to Facilities and Products in Texas Future (six months ahead) | ||||||||

| Indicator | Feb Index | Jan Index | Change | Series Average | Trend* | % Reporting Increase | % Reporting No Change | % Reporting Decrease |

Revenue | 38.3 | 41.0 | –2.7 | 37.2 | 70(+) | 50.9 | 36.5 | 12.6 |

Employment | 21.2 | 22.0 | –0.8 | 22.9 | 70(+) | 29.7 | 61.8 | 8.5 |

Part–Time Employment | 3.3 | 7.1 | –3.8 | 6.4 | 8(+) | 10.3 | 82.7 | 7.0 |

Hours Worked | 6.1 | 9.1 | –3.0 | 5.9 | 8(+) | 11.0 | 84.1 | 4.9 |

Wages and Benefits | 37.2 | 40.1 | –2.9 | 37.5 | 70(+) | 40.9 | 55.5 | 3.7 |

Input Prices | 37.5 | 37.5 | 0.0 | 44.2 | 230(+) | 43.6 | 50.3 | 6.1 |

Selling Prices | 16.6 | 27.0 | –10.4 | 24.4 | 70(+) | 27.6 | 61.4 | 11.0 |

Capital Expenditures | 17.2 | 18.4 | –1.2 | 22.4 | 69(+) | 25.6 | 66.1 | 8.4 |

| General Business Conditions Future (six months ahead) | ||||||||

| Indicator | Feb Index | Jan Index | Change | Series Average | Trend** | % Reporting Improved | % Reporting No Change | % Reporting Worsened |

Company Outlook | 13.8 | 18.7 | –4.9 | 15.3 | 10(+) | 28.5 | 56.8 | 14.7 |

General Business Activity | 15.0 | 14.7 | +0.3 | 11.9 | 9(+) | 28.1 | 58.8 | 13.1 |

*Shown is the number of consecutive months of expansion or contraction in the underlying indicator. Expansion is indicated by a positive index reading and denoted by a (+) in the table. Contraction is indicated by a negative index reading and denoted by a (–) in the table.

**Shown is the number of consecutive months of improvement or worsening in the underlying indicator. Improvement is indicated by a positive index reading and denoted by a (+) in the table. Worsening is indicated by a negative index reading and denoted by a (–) in the table.

Data have been seasonally adjusted as necessary.

Comments from survey respondents

Survey participants are given the opportunity to submit comments on current issues that may be affecting their businesses. Some comments have been edited for grammar and clarity.

- High interest rates (on a relative basis) and low energy prices make for a difficult market in Houston. Heightened uncertainty regarding federal and state economic policies makes business planning more difficult.

- Interest rates are hurting our client companies. We can't wait for them to be reduced.

- We are subcontractors to a large firm that has been awarded a contract with the Department of Defense.

- Job market for professional, white-collar roles is only getting worse. I am scared and worried for my business and my employees. Small businesses are suffering.

- Health care utilization has decreased, due in part to warmer winter temperatures (i.e., less seasonal flu and winter colds), coupled with the severe cold weather that led to facility closures. Additionally, the doubt that has been cast on the medical profession by the current administration's policies on things such as vaccines has also hampered business. Higher layoffs—particularly white-collar layoffs, which often lead to loss of health insurance—have also been a drag on patient volume. Finally, significantly higher input costs, particularly for supplies and services, have created financial strain on our business.

- Mounting government debt will drag the U.S. economy down if fiscal spending is not reduced.

- The changes in the regulatory environment could change the future outlook for banks. The number of mergers and acquisitions has increased. FinTech activity has ramped up, and banks are looking to partner with FinTech [companies] to diversify their lending bases and enter the AI market indirectly.

- Decreased inflationary pressures and rising employment is good.

- Store visits were off 30 percent in January; sales were down 11.5 percent.

- The Permian Basin is unique in that even though energy prices are falling, residents seem not to be aware of signs in the community that things aren't as they appear. Oil companies continue to lay off workers or reduce overtime, houses on the market continue to rise, community services [needs] continue to rise; water rates, electric rates and community debt are also rising.

- Insurance premiums in Texas for many lines are holding or falling, yet our expenses and payrolls are increasing. So we have pressure to find new customers and hope our current customers grow their businesses to offset the revenue reduction that comes from falling insurance premiums. Just part of the normal insurance cycle, but the insurance cycle is not always timed with or dependent on the economic performance of our region or country.

- We are cautiously optimistic about 2026. We are expanding into the Austin market, which is the cause for our increase in the number of employees and capital expenditures both in February and six months from now.

- President Trump's haphazard approach to applying and then rescinding tariffs is spreading chaos in the food supplier and export markets. To date, we have not seen any meaningful impact to our exports, but our customers are being very cautious when placing their next orders.

- Although we continue to see sales increases year over year, the magnitude of the increases has diminished greatly in the past 30 days. December and January saw 12 percent increases year over year, while February so far has seen a 7 percent increase.

- We see continued softening in the lower-income segment of car buyers.

- This area has been hit by the amount of construction workers that were not legal and are no longer working or have left the country. The construction industry has been severely hit, and it is affecting the expenditures of people in south Texas, creating a down effect in retail sales.

- There doesn't seem to be any retail pattern or playbook these days. I used to be able to compare this year and last year. My rule of thumb is go back to customer relationships, [hosting] fun events that people want to come to and continuing to find unique items for the customer walking in the doors or shopping online.

- Hiring is very difficult right now. It appears that there are a few more qualified drivers who have solid work histories but finding a qualified person for a clerical-type job has been difficult. It seems like almost all of the job applicants on Indeed have a history of changing jobs every year. It is extraordinary. I don't know who will be able to do the work in the economy when my generation retires.

- We implemented a price increase in February to offset increased operating expenses. This has added to general business uncertainty. We have also had to increase employee wages.

- Because our business is regulated by the state, our only way to increase revenue is with more activity, which is challenging in real estate these days. Things are going well overall, but costs are definitely still increasing. We continue to raise wages to retain our team, but outside talent is also getting more expensive.

- There is hardly any government spending by local institutions. School districts are struggling. There are no more bonds. Bonds that did go out and projects that were awarded went to large, out-of-town firms.

- I think what you see from the economy today is what you're going to get over the next 12 to 18 months. So if you are waiting for a "rising tide" to lift your company's fortunes, you are in for a long wait.

- The general level of business activity has picked up, and with the banks and lenders seeming more interested in making real estate loans, our outlook for 2026 has improved. We will know more once the first quarter is over and hopefully this trend will continue.

- AI is amazing. Our company cut labor and improved the scope of what we deliver for our clients.

- It is hard to tell how things will be six months from now. We chose "no change" because we don't know!

- Workers, workers, workers. We're in the architecture, engineering and construction industry. We need qualified and experienced workers. No one is knocking at the door for jobs. We are unable to grow to meet demand.

- Much of our work and backlog is sector-focused. We definitely see the K-shaped economy at play in Texas, with commercial activity not yet recovered to 2019 levels and with oil, gas, industrial, and power infrastructure contributing to 90 percent of our growth.

- We expect a strong 2026 financial year. However, our biggest customer of 2025 is not renewing their support contract for 2026 and later years, making us [try to recoup] the revenue we got last year from this customer from existing or new customers. The U.S. and global economies looks strong to us for 2026, and our software products are needed to securely connect systems even as AI arrives and makes some other software solutions less needed. So we expect demand for our software products to increase in 2026 and 2027. The U.S. is at a tipping point for AI productivity gains, and small companies like us will benefit more than big companies as we can adjust how we operate must faster to leverage AI benefits.

- Our company provides engineering consulting services, primarily to public sector infrastructure clients. Tight budgets are affecting capital expenditures on the part of our clients.

- There has been an uptick in the number of approved projects. Projects that had been hung up pending management approval suddenly have moved forward. That said, there is still a lot of unease visible within our current customers and prospects.

- Our recruiting is getting better. We have much more stable and reliable staff. We are concentrating on growing our market share for the next six months. We are also working on getting more efficient.

- We sell computer infrastructure products and services. We have just learned in the last two weeks that supply-chain constraints related to memory chips are bad and about to be really, really tight. There is talk of pandemic-like supply constraints, and prices have already jumped more than 50 percent in all memory-related products (servers, etc.) in just the last two weeks. This will affect our revenue and our cash flow, as well as our profitability. I don't know how long this will last, but am guessing it could last six months.

- The world and its politicians seem to have figured out that oil and gas are and will remain critical commodities in the 21st century.

- The market for our design services and construction appears to be steady to slightly increasing.

- Real estate developers remain on the sidelines.

- There is no change in the level of uncertainty; it still remains high. We just don't know what is happening next. There is no defined path to the direction the administration is taking on anything (except maybe deportations).

- We are facing a rate decrease for title premiums starting March 1. The decrease is 6.2 percent. We are also required to report FinCEN [Financial Crimes Enforcement Network] starting in March, which is an additional cost to the title industry. The expense will be passed on to the consumer.

- As a government-centric software business, uncertainty remains the biggest issue to manage the business.

- The macro forces that have compounded over the last year—inflation, high interest rates, tariffs, reduced government spending and general government volatility—are now significantly impacting our business negatively. The on-the-ground reality among midmarket businesses we are seeing seems radically disconnected from Fortune 500 public equity performance, which is supported by job elimination, which will have a deleterious economic impact at some point.

- The market seems to be excited with movement, just need to see if the movement will pay off in sales.

- It is very tough to see where the economy is headed. It seems to be treading water. Most clients seem to be very conservative in their outlook and spending.

- Due to being in the leisure industry, we continue to expect sales to drop. Some level of uncertainty still lingers for some of our clients.

- We must stabilize the economy and eliminate chaos in D.C, and as well rekindle good will among Western nations. As worsens, the economic impact here will follow. Further, we are losing the employment base at the immigrant level, so there must be a policy and laws passed to permit inmigration in a logical procedure to allow that employment base to return safely with free guidelines defined, which include expulsion for any criminal act.

- Our economic outlook continues to darken. Transaction volume has slowed, and any momentum that was in place a few months ago has played itself out. 2026 is not looking to be an expansion year, or even a stable one.

- Across all of the multifamily industry's 2026 forecasts and prognostications we've been to lately, consensus seems to be that renters are squeezed, prospects are muted, uncertainty abounds and challenged debtholders have run out of options. No one is singing the administration's praises. We're expecting recession and another tough year. We plan to make do with what we have, focus on the basics and skip investments in new systems.

- As a financial services firm, we are impacted by economic and market conditions. Recent gains in investment markets moved first quarter 2026 revenues higher.

- We are seeing a reduction in spending.

- The recent increase in regulatory enforcement in the trucking industry is beginning to produce a long-needed correction in both rates and available freight assignments. As noncompliant and unsafe carriers exit, we are seeing new business opportunities emerge. For four years, most shippers and intermediaries were paying rates below sustainable market levels. That dynamic is now shifting, and carriers are regaining some negotiating leverage. We are increasingly able to require rates that support profitable operations. That said, margins have not yet fully recovered to levels necessary to restore balance sheets across the sector. Continued normalization will be important to ensure long-term capacity stability.

- I feel that the economy is doing well, and there is optimism.

- Overall outlook is stable, with continued price inflation pressures.

Special questions

For this month’s survey, Texas business executives were asked supplemental questions on demand, regulation and hiring. Results below include responses from participants from both the Texas Manufacturing Outlook Survey and Texas Service Sector Outlook Survey. View individual survey results.

Historical Data

Historical data can be downloaded dating back to January 2007.

Indexes

Download indexes for all indicators. For the definitions of all variables, see data definitions.

| Unadjusted |

| Seasonally adjusted |

All Data

Download indexes and components of the indexes (percentage of respondents reporting increase, decrease, or no change). For the definitions of all variables, see data definitions.

| Unadjusted |

| Seasonally adjusted |

Questions regarding the Texas Service Sector Outlook Survey can be addressed to Isabel Brizuela.

Sign up for our email alert to be automatically notified as soon as the latest Texas Service Sector Outlook Survey is released on the web.