Texas Service Sector Growth Rebounds in September

Texas Service Sector Outlook Survey

September 29, 2020

Texas Service Sector Growth Rebounds in September

What’s New This Month

For this month’s survey, Texas business executives were asked supplemental questions on the impacts of COVID-19. Results for these questions from the Texas Manufacturing Outlook Survey, Texas Service Sector Outlook Survey and Texas Retail Outlook Survey have been released together. Read the special questions results.

NOTE: We have discontinued the report PDF, but the page is formatted for your printer and will look similar to the PDF previously provided. You can either print the report or save it as a PDF via the print function of your browser.

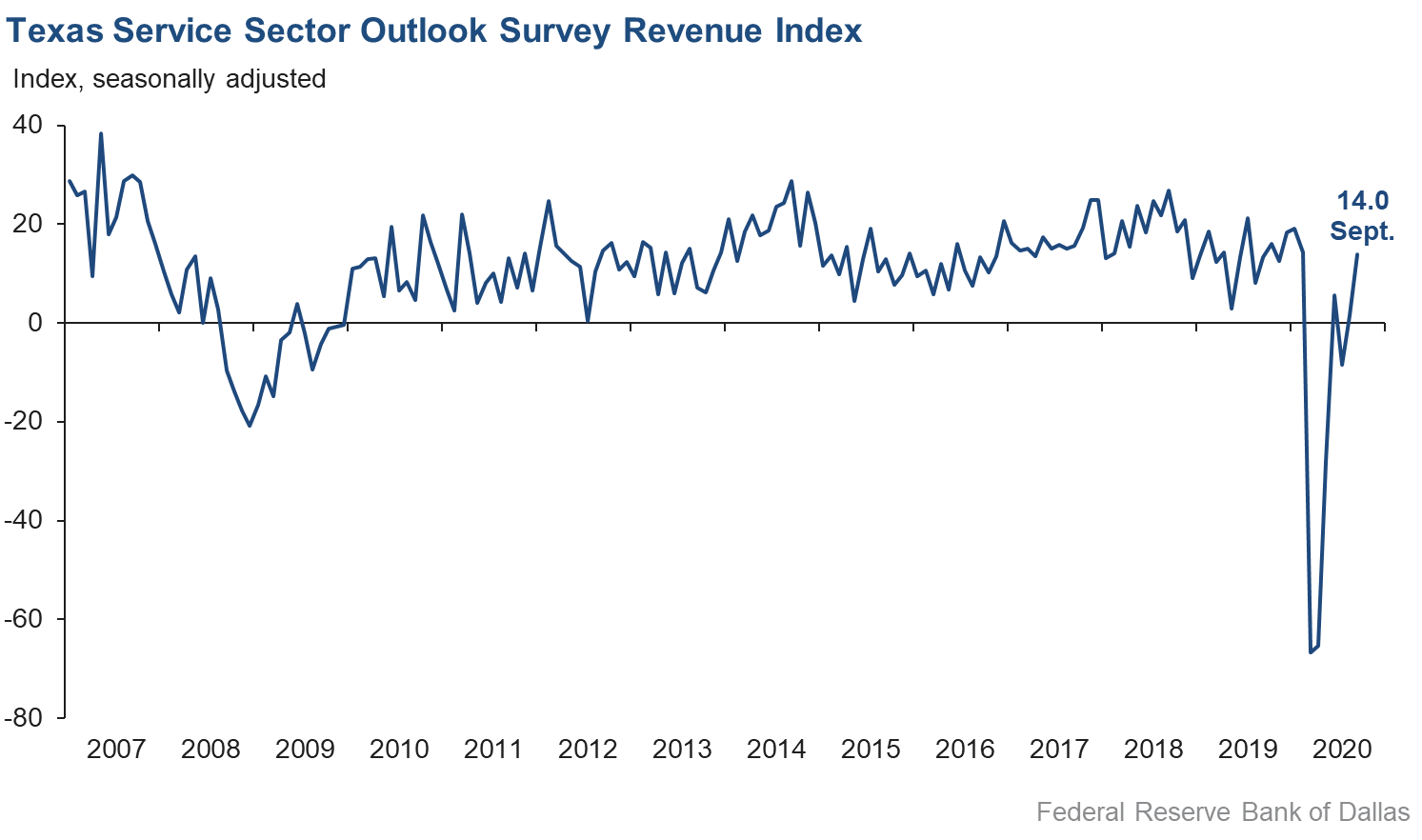

Activity in the Texas service sector grew at its fastest pace since February, according to business executives responding to the Texas Service Sector Outlook Survey. The revenue index, a key measure of state service sector conditions, jumped from 1.5 in August to 14.0 in September, with one-third of respondents indicating an increase in revenues.

Labor market indicators reflected growth in employment and workweek length in September. The employment index rose three points to 2.7, its first positive reading since February. The hours worked index surged nearly eight points to 6.6, its best reading since mid-2019.

Perceptions of broader business conditions continued to improve compared with August. The general business activity index advanced about seven points to 11.5, while the company outlook index rose from 5.6 to 9.7. The outlook uncertainty index fell to 0.0, suggesting that the same share of respondents believed outlooks were less uncertain as believed outlooks were more uncertain.

Wages pressures rose in September, while price pressures eased. The wages and benefits index rose from 4.9 to 7.1, pointing to a faster pace of growth in worker compensation. The selling prices index slipped about two points to 2.2, while the input prices index fell from 22.2 to 19.4.

Respondents’ expectations regarding future business activity remained optimistic in September but weakened slightly compared with August. The future general business activity index was unchanged at 18.9, while the future revenue index slipped from 35.5 to 31.9, though over half of respondents still expect their revenues to be higher in six months. Other indexes of future service sector activity such as employment fell but remain near pre-COVID-19 levels, suggesting expectations of significant expansion in activity by early 2021.

Texas Retail Outlook Survey

September 29, 2020

Texas Retail Sales Rise Sharply

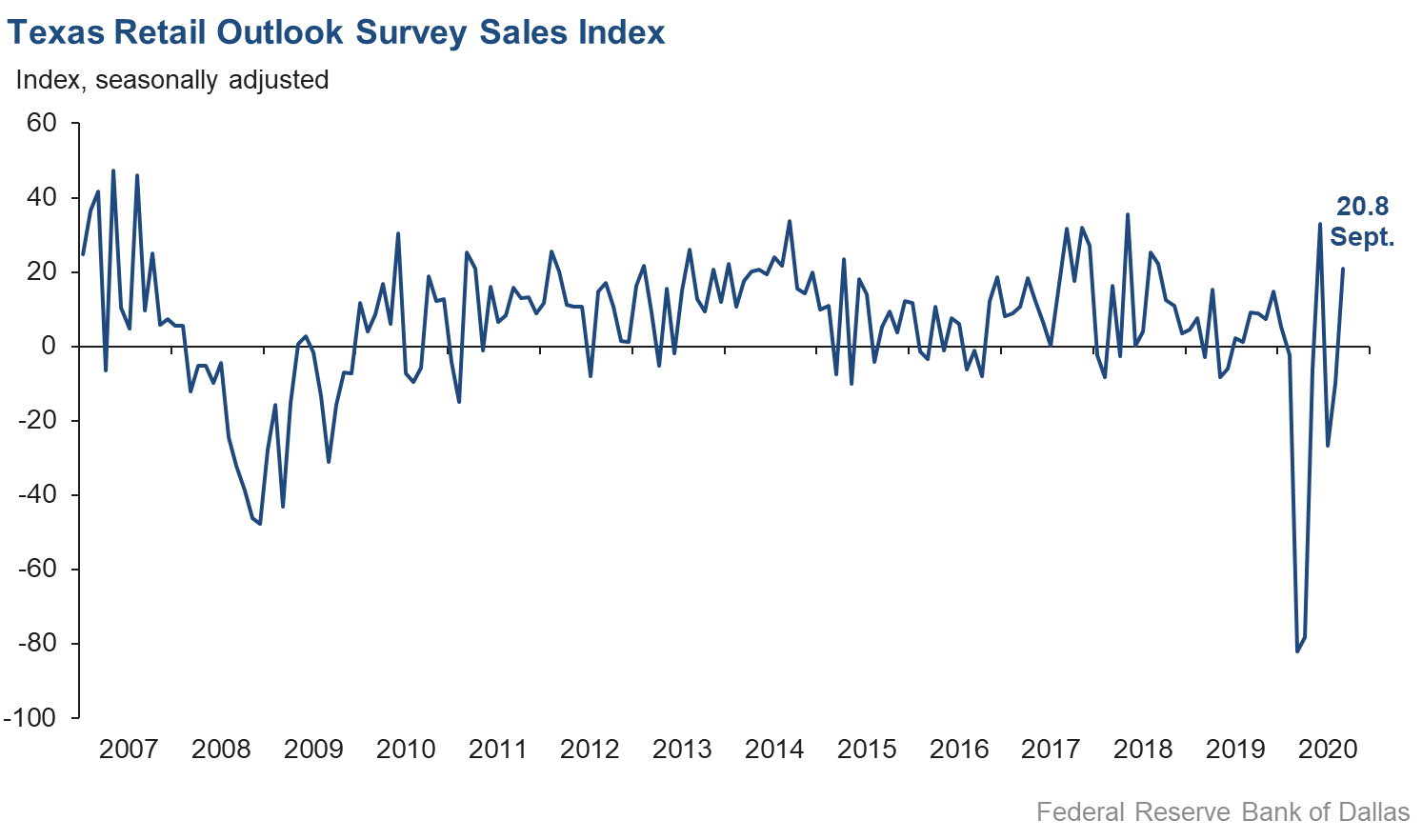

Retail sales activity soared in September after two months of declines, according to business executives responding to the Texas Retail Outlook Survey. The sales index, a key measure of state retail activity, advanced from -9.9 to 20.8. Over 35 percent of respondents reported increased sales compared with August, while just 16 percent reported decreases—the lowest share since November 2019. The decline in inventories continued to ease, with the inventories index increasing from -8.7 to -4.1.

Retail labor market indicators were positive in September, with net increases in employment and average workweek length. The employment index was roughly unchanged at 2.3, while the hours worked index surged 17 points to 3.1—its first positive reading since January.

Retailers’ perceptions of broader business conditions remained positive in September. The general business activity index rose six points to 10.3, while the company outlook index was mostly unchanged at 8.9. The outlook uncertainty index fell further from 7.2 to 0.0, with nearly 80 percent of respondents noting no change in uncertainty compared with August.

Retail wage and price pressures climbed sharply in September. The wages and benefits index increased from 0.9 to 7.3, while the input prices index surged from 16.0 to 26.3. The selling prices index advanced over eight points to 22.6—its highest reading since February.

Retailers’ perceptions of future activity continued to reflect optimism in September. The future general business activity index slipped three points but remained positive at 24.8, while the future sales index rose nearly eight points to 42.7—a two-year high. Other indexes of future retail activity such as employment were at or above pre-COVID-19 levels, pointing to expectations of significantly stronger activity in six months.

The Texas Retail Outlook Survey is a component of the Texas Service Sector Outlook Survey that uses information only from respondents in the retail and wholesale sectors.

Next release: October 27, 2020

|

Data were collected September 15–23, and 231 Texas service sector and 57 retail sector business executives responded to the survey. The Dallas Fed conducts the Texas Service Sector Outlook Survey monthly to obtain a timely assessment of the state’s service sector activity. Firms are asked whether revenue, employment, prices, general business activity and other indicators increased, decreased or remained unchanged over the previous month. Survey responses are used to calculate an index for each indicator. Each index is calculated by subtracting the percentage of respondents reporting a decrease from the percentage reporting an increase. When the share of firms reporting an increase exceeds the share reporting a decrease, the index will be greater than zero, suggesting the indicator has increased over the prior month. If the share of firms reporting a decrease exceeds the share reporting an increase, the index will be below zero, suggesting the indicator has decreased over the prior month. An index will be zero when the number of firms reporting an increase is equal to the number of firms reporting a decrease. Data have been seasonally adjusted as necessary. |

Texas Service Sector Outlook Survey

September 29, 2020

Historical data are available from January 2007 to the most current release month.

| Business Indicators Relating to Facilities and Products in Texas Current (versus previous month) | ||||||||

| Indicator | Sep Index | Aug Index | Change | Series Average | Trend* | % Reporting Increase | % Reporting No Change | % Reporting Decrease |

Revenue | 14.0 | 1.5 | +12.5 | 10.8 | 2(+) | 33.4 | 47.2 | 19.4 |

Employment | 2.7 | –0.3 | +3.0 | 6.0 | 1(+) | 12.0 | 78.7 | 9.3 |

Part–Time Employment | 3.7 | 0.1 | +3.6 | 1.2 | 2(+) | 7.8 | 88.1 | 4.1 |

Hours Worked | 6.6 | –1.0 | +7.6 | 2.2 | 1(+) | 11.9 | 82.8 | 5.3 |

Wages and Benefits | 7.1 | 4.9 | +2.2 | 13.9 | 4(+) | 12.5 | 82.1 | 5.4 |

Input Prices | 19.4 | 22.2 | –2.8 | 24.9 | 5(+) | 24.4 | 70.5 | 5.0 |

Selling Prices | 2.2 | 4.4 | –2.2 | 5.0 | 2(+) | 10.4 | 81.4 | 8.2 |

Capital Expenditures | 4.9 | –0.5 | +5.4 | 9.7 | 1(+) | 14.3 | 76.3 | 9.4 |

| General Business Conditions Current (versus previous month) | ||||||||

| Indicator | Sep Index | Aug Index | Change | Series Average | Trend** | % Reporting Improved | % Reporting No Change | % Reporting Worsened |

Company Outlook | 9.7 | 5.6 | +4.1 | 4.8 | 2(+) | 21.1 | 67.5 | 11.4 |

General Business Activity | 11.5 | 4.7 | +6.8 | 2.6 | 2(+) | 26.6 | 58.3 | 15.1 |

| Indicator | Sep Index | Aug Index | Change | Series Average | Trend* | % Reporting Increase | % Reporting No Change | % Reporting Decrease |

Outlook Uncertainty† | 0.0 | 5.7 | –5.7 | 13.1 | 1() | 16.3 | 67.4 | 16.3 |

| Business Indicators Relating to Facilities and Products in Texas Future (six months ahead) | ||||||||

| Indicator | Sep Index | Aug Index | Change | Series Average | Trend* | % Reporting Increase | % Reporting No Change | % Reporting Decrease |

Revenue | 31.9 | 35.5 | –3.6 | 36.6 | 5(+) | 50.7 | 30.5 | 18.8 |

Employment | 19.5 | 21.9 | –2.4 | 21.5 | 5(+) | 32.5 | 54.5 | 13.0 |

Part–Time Employment | 4.8 | 1.8 | +3.0 | 6.3 | 2(+) | 14.1 | 76.6 | 9.3 |

Hours Worked | 9.0 | 7.2 | +1.8 | 5.4 | 5(+) | 15.4 | 78.2 | 6.4 |

Wages and Benefits | 27.2 | 23.8 | +3.4 | 35.6 | 5(+) | 33.3 | 60.7 | 6.1 |

Input Prices | 30.2 | 32.0 | –1.8 | 43.5 | 165(+) | 35.3 | 59.6 | 5.1 |

Selling Prices | 14.5 | 13.8 | +0.7 | 22.6 | 5(+) | 24.3 | 65.9 | 9.8 |

Capital Expenditures | 11.5 | 17.3 | –5.8 | 23.0 | 4(+) | 23.6 | 64.3 | 12.1 |

| General Business Conditions Future (six months ahead) | ||||||||

| Indicator | Sep Index | Aug Index | Change | Series Average | Trend** | % Reporting Improved | % Reporting No Change | % Reporting Worsened |

Company Outlook | 20.8 | 21.9 | –1.1 | 15.9 | 2(+) | 34.3 | 52.2 | 13.5 |

General Business Activity | 18.9 | 19.2 | –0.3 | 12.6 | 2(+) | 35.2 | 48.4 | 16.3 |

Texas Retail Outlook Survey

September 29, 2020

Historical data are available from January 2007 to the most current release month.

| Business Indicators Relating to Facilities and Products in Texas Retail (versus previous month) | ||||||||

| Indicator | Sep Index | Aug Index | Change | Series Average | Trend* | % Reporting Increase | % Reporting No Change | % Reporting Decrease |

Retail Activity in Texas | ||||||||

Sales | 20.8 | –9.9 | +30.7 | 5.7 | 1(+) | 36.4 | 47.9 | 15.6 |

Employment | 2.3 | 1.4 | +0.9 | 1.7 | 2(+) | 8.1 | 86.1 | 5.8 |

Part–Time Employment | 1.7 | –1.9 | +3.6 | –2.2 | 1(+) | 7.1 | 87.5 | 5.4 |

Hours Worked | 3.1 | –13.9 | +17.0 | –2.1 | 1(+) | 7.5 | 88.1 | 4.4 |

Wages and Benefits | 7.3 | 0.9 | +6.4 | 9.1 | 2(+) | 11.9 | 83.5 | 4.6 |

Input Prices | 26.3 | 16.0 | +10.3 | 18.7 | 5(+) | 30.4 | 65.5 | 4.1 |

Selling Prices | 22.6 | 14.3 | +8.3 | 9.9 | 4(+) | 27.7 | 67.2 | 5.1 |

Capital Expenditures | –2.8 | –2.8 | 0.0 | 7.5 | 7(–) | 6.4 | 84.4 | 9.2 |

Inventories | –4.1 | –8.7 | +4.6 | 2.4 | 8(–) | 20.0 | 55.9 | 24.1 |

Companywide Retail Activity | ||||||||

Companywide Sales | 6.6 | –4.5 | +11.1 | 7.0 | 1(+) | 30.6 | 45.5 | 24.0 |

Companywide Internet Sales | 6.3 | 0.4 | +5.9 | 6.2 | 2(+) | 18.4 | 69.5 | 12.1 |

| General Business Conditions, Retail Current (versus previous month) | ||||||||

| Indicator | Sep Index | Aug Index | Change | Series Average | Trend** | % Reporting Improved | % Reporting No Change | % Reporting Worsened |

Company Outlook | 8.9 | 9.6 | –0.7 | 3.2 | 2(+) | 21.3 | 66.3 | 12.4 |

General Business Activity | 10.3 | 4.2 | +6.1 | –1.1 | 2(+) | 23.9 | 62.5 | 13.6 |

| Outlook Uncertainty Current (versus previous month) | ||||||||

| Indicator | Sep Index | Aug Index | Change | Series Average | Trend* | % Reporting Increase | % Reporting No Change | % Reporting Decrease |

Outlook Uncertainty† | 0.0 | 7.2 | –7.2 | 10.5 | 1() | 10.5 | 78.9 | 10.5 |

| Business Indicators Relating to Facilities and Products in Texas, Retail Future (six months ahead) | ||||||||

| Indicator | Sep Index | Aug Index | Change | Series Average | Trend* | % Reporting Increase | % Reporting No Change | % Reporting Decrease |

Retail Activity in Texas | ||||||||

Sales | 42.7 | 34.9 | +7.8 | 31.9 | 5(+) | 57.4 | 27.9 | 14.7 |

Employment | 18.6 | 19.5 | –0.9 | 11.8 | 5(+) | 26.5 | 65.6 | 7.9 |

Part–Time Employment | 5.0 | –0.4 | +5.4 | 0.5 | 1(+) | 13.2 | 78.6 | 8.2 |

Hours Worked | 7.3 | 1.9 | +5.4 | 2.6 | 5(+) | 12.2 | 82.9 | 4.9 |

Wages and Benefits | 24.8 | 18.3 | +6.5 | 26.8 | 5(+) | 28.7 | 67.4 | 3.9 |

Input Prices | 32.7 | 20.7 | +12.0 | 32.4 | 5(+) | 38.2 | 56.4 | 5.5 |

Selling Prices | 34.0 | 21.2 | +12.8 | 28.5 | 5(+) | 42.9 | 48.2 | 8.9 |

Capital Expenditures | 21.8 | 13.4 | +8.4 | 16.9 | 4(+) | 29.1 | 63.6 | 7.3 |

Inventories | 33.5 | 26.3 | +7.2 | 8.2 | 5(+) | 47.5 | 38.5 | 14.0 |

Companywide Retail Activity | ||||||||

Companywide Sales | 38.0 | 38.9 | –0.9 | 30.4 | 5(+) | 51.9 | 34.2 | 13.9 |

Companywide Internet Sales | 36.4 | 25.0 | +11.4 | 21.7 | 6(+) | 43.2 | 50.0 | 6.8 |

| General Business Conditions, Retail Future (six months ahead) | ||||||||

| Indicator | Sep Index | Aug Index | Change | Series Average | Trend** | % Reporting Improved | % Reporting No Change | % Reporting Worsened |

Company Outlook | 27.3 | 28.6 | –1.3 | 16.7 | 5(+) | 41.3 | 44.7 | 14.0 |

General Business Activity | 24.8 | 28.1 | –3.3 | 12.4 | 2(+) | 37.5 | 49.7 | 12.7 |

*Shown is the number of consecutive months of expansion or contraction in the underlying indicator. Expansion is indicated by a positive index reading and denoted by a (+) in the table. Contraction is indicated by a negative index reading and denoted by a (–) in the table.

**Shown is the number of consecutive months of improvement or worsening in the underlying indicator. Improvement is indicated by a positive index reading and denoted by a (+) in the table. Worsening is indicated by a negative index reading and denoted by a (–) in the table.

†Added to survey in January 2018.

Data have been seasonally adjusted as necessary, with the exception of the outlook uncertainty index which does not yet have a sufficiently long time series to test for seasonality.

Texas Service Sector Outlook Survey

September 29, 2020

Texas Retail Outlook Survey

September 29, 2020

Texas Service Sector Outlook Survey

September 29, 2020

Comments from Survey Respondents

These comments are from respondents’ completed surveys and have been edited for publication.

Utilities

- Uncertainty around COVID-19 remains high. It looks like this fall and winter could be very difficult periods due to COVID-19.

- There is more uncertainty in the marketplace, along with more bad debt, which is becoming an issue.

Truck Transportation

- [There are issues due to] COVID-19 closures in transportation and regulations.

- We are having trouble finding qualified diesel mechanics.

Pipeline Transportation

- Our level of uncertainty has not changed from last month; it remains high.

- There is the uncertainty of global factors impacting demand and the U.S. election outcome.

Warehousing and Storage

- The past six weeks have shown increased activity in crude exports but also in refined products. We are cautiously optimistic that this is a trend that is going to continue, albeit at a slow pace.

Publishing Industries (Except Internet)

- More indications are emerging and developing that near-term interest and the probability of larger software and platform orders for AR/VR [augmented reality/virtual reality] advanced tech interfaces and apps for training and virtual trade/business events using eye-retina and no-touch finger/hands user interface motion will improve and be funded. Both DoD [Department of Defense]/government and enterprise seem to be improving as prospects bubble up more and more.

Data Processing, Hosting and Related Services

- We are optimistic that purchasing decision-makers will try to make up ground lost during COVID-19 in the fourth quarter.

Credit Intermediation and Related Activities

- The election and politics have captivated the attention of most people and substantially elevated the anxiety level. The markets are reacting very nervously. With the velocity of money slowing to a crawl, there are fewer opportunities to expand the volume of portfolios. Yields are low, and margins continue to tighten.

- We have eight different entities. Delays in getting some financing finalized have resulted in much less working capital. When paired with a lack of grant funding for the nonprofit, cash is getting tight, and we are getting ready to lay off some people.

- There are some signs of new stabilization and operating expectations for our clients.

- We still believe that after government stimulus programs fade, businesses will begin to falter. Demand for goods and services will fall. We will see additional business failures in first quarter 2021.

Securities, Commodity Contracts, and Other Financial Investments and Related Activities

- There appears to be some stability developing with regard to a "new normal" for the time being.

- It's a tough market for oil and gas and metal fabrication. The prospects are not good now, and the present market for other products doesn't seem to move much.

Insurance Carriers and Related Activities

- We are still seeing higher sales prices as weather causes increases in the property insurance policies we sell. There are increases in management liability due to COVID-19 and business conditions, etc., lately as well.

Real Estate

- There appears to be a little more optimism regarding COVID-19 and, thus, things seem to be improving slightly. Tenants are still struggling with closures and restrictions on capacity, and the fear factor is still very prevalent with a good segment of the population. If we can’t find ways to enable people to celebrate the upcoming holidays, retailers that normally make all of their profit each year in the holiday season will probably fail or finally give up. We need to find a path to get people to be able to celebrate the holidays and we need to get kids back in school just to have the business sector survive. Everything from retailers to haircutters are at grave risk of failing due to the massive closures, and if we don't help them survive, we will have a huge recession and unemployment problem next year.

- People are wanting to spend money and eat out. Hopefully, news will continue to be positive about a vaccine. There is such mistrust with reporting; no one believes most of what the media puts out.

Rental and Leasing Services

- I think the uncertainty of the coronavirus, the Oil-Patch Bust and the self-induced economic disaster are somewhat accepted as business as usual for now. The extreme uncertainty that increases daily both personally and professionally is the national election and the possibility of electing an extreme anti-business administration that will significantly raise taxes and deter business and personal investment in America.

Professional, Scientific and Technical Services

- The global business climate has improved significantly from the COVID-19 slowdown. U.S. business orders and climate were already doing better and continue to improve.

- After a decrease in both design and construction activity in May, June and July, the backlog has increased on the design side in August and appears to be increasing in September. Construction projects put on hold in May are back or reported to begin at the end of September.

- Poor broadband access for highly skilled workers working from home is an issue.

- Although we are seeing a slight increase in our business activity (two new contracts: one is capacity building, the other is politically related), we attribute the larger [contract] to the upcoming election as it is focused on building out a website to get local citizens to vote and to provide resources. It is a demanding project because of the time constraints but one that we hated to pass up because of the uncertainty of the future. The second one is a bit smaller in scale but will take us into 2021, which helps us instill confidence in what we might be able to bring in next year.

- The general expectation for legal professional services for the remainder of the year is optimistic, with a caveat being what the U.S. election might do to the business cycle. There is still concern over the long-term impact the pandemic will have on legal services globally. Our outlook for 2021 is very cautious.

- Uncertainty is high due to the upcoming election, mail-in ballots, the ability to determine a winner after election day and the misleading media.

- The uncertainty of COVID-19 affects everything, and the complications of the pending election make things more polarized.

- We are worried about a second wave of COVID-19 infections and new business closures.

Management of Companies and Enterprises

- I feel more optimistic and ready to invest more into the economy. Uncertainty in the economy and markets is giving us opportunities.

Administrative and Support Services

- Six months from now is a long time given what is taking place politically. My answers could be very different depending on the outcome of the election.

- Overall, things have increased. We are seeing more RFQs [requests for quotations] from the industrial manufacturing side than in August.

- We continue to have challenges hiring workers.

- We have been surprised by the lack of interest in applying for open positions. We have seen this with our own organization and have heard similar comments from other employers. Despite much higher unemployment rates, employers are still struggling to find suitable employees.

- The stimulus and low interest rates are still key drivers. There is a question of how sustainable they are.

- Our government customers are more active. August was the best month we had since the pandemic started. There is a lot of activity regarding RFIs [requests for information] and RFPs [requests for proposal] for new government contracts. Leisure travel has not been active at all, and for what we know, it will not be active until late next year. Corporate accounts are having their meetings via Zoom, and we have not seen any activity; we only have one account that is active. Obviously, we have decided to concentrate 100 percent on government contracts. The PPP [Paycheck Protection Program] loan is exhausted, and we need more income now to stay in business.

Educational Services

- Our business (higher education) is highly seasonal. Uncertainty decreased and outlook improved in the current month as more students enrolled than anticipated. However, we are concerned this will not persist to spring; uncertainty is high.

Ambulatory Health Care Services

- Dentistry, particularly the regular preventative exams/cleanings, tend to go in six-month cycles for patients. Beginning Sept. 22 and for six weeks thereafter, we begin the overlap of our forced closure starting in late March, during which we saw no patients and couldn't set their next appointment for six months later. Naturally, prebookings are way down for about a third of our business during this upcoming period. This is being discussed by dentists across the country as we're all about to get hit with a second round of reduced revenue due to COVID-19. So, expect dentists across the region to report lower month-over-month revenue in October.

- Health care is uniquely impacted with increased workload, increased compliance and increased challenges for health care workers, while reimbursement [issues], including CMS [Centers for Medicare & Medicaid Services] pushing to control cost, are lowering income vs. increasing operational cost. This is leading to increasing consolidation in the industry (which may be the unstated interest of CMS), resulting in significant business-margin impact for independent and small business enterprises in the health care sector.

- There are so many issues that make us all fret. The central issue is the coronavirus threat. And who will ever pay down the debt? The dramatic increase in safety and screening and PPE [personal protective equipment] costs in health care, when combined with pending lower reimbursement, have and will result in growing numbers of retirements and closures and accelerate a worsening in the social determinants of health.

Social Assistance

- Our outlook improved with decreased uncertainty, as the need for our core services (workforce development) increased due to continued impact during the pandemic. Delivery of virtual services continue, which increased costs in delivery, but funding increased through the CARES [Coronavirus Aid, Relief and Economic Security] Act and subcontracting from local government.

Performing Arts, Spectator Sports and Related Industries

- The election and who wins is of concern—two totally different outlooks on capitalism.

Museums, Historical Sites and Similar Institutions

- We are working hard to bring the public back into the facility. If current growth continues, and we keep all our expenses cut, and no further setbacks occur, we may break even for 2020.

Amusement, Gambling and Recreation Industries

- The prospects for clubs/restaurants are still questionable. Until the limits are lifted and until the circumstances change to allow large gatherings for weddings, political fund raisers, meetings, etc., and even more importantly, until more people feel safe again, there is not a positive future. I am afraid many will start questioning whether it is worth all the expense and hard work to keep going. [It is] certainly a sentiment that we are hearing over and over again. On top of it, there is no relief on property taxes or rent. Some will survive, but many will not.

- Attendance was 30 percent below the average in the previous three years. The mask and uncertainty of CDC [Centers for Disease Control] protocols kept people away. School starting also cut into operating days.

Accommodation

- Uncertainty is the only constant. In the lodging and restaurant space, nothing will change until governments relax restrictions, and people regain confidence in air travel and public gatherings.

- Business is poor, and the outlook remains poor. We are a suburban location, next to a convention center. Without group business at this center, we will see no discernable change in our outlook. Additionally, when businesses feel it is appropriate to meet, we will see some benefit.

Food Services and Drinking Places

- Finding people that want to work [is a problem]; we cannot get people who want to work.

Religious, Grantmaking, Civic, Professional, and Similar Organizations

- We are adapting, but the idea of things getting to normal no longer applies.

Merchant Wholesalers, Durable Goods

- The slow oil and gas market continues to have a significant impact on spending in DFW.

- We continue to see small increases in revenue month after month (May was the bottom of the trough). Additionally, we are selling products so that restoration contractors can respond to the devastation from Hurricane Laura in southeast Texas/southwest Louisiana.

- [We are] out of business.

Merchant Wholesalers, Nondurable Goods

- Our existing business continues to drag as a result of dining room closures (or partial reopenings). We have started shipping a new market in Costa Rica, so that has accounted for a large increase in August sales (and going forward). I'm still concerned that the hourly wage earners that have been laid off or have taken a pay cut will not return to pre-COVID-19 levels of dining out. Ultimately, the dining segment will shrink, and restaurants will close, but the demand will remain.

Motor Vehicle and Parts Dealers

- Generally, we still believe there is a great deal of uncertainty as the election approaches. Business failures in airlines, hotels, restaurants, retail and other affected industries are concerning.

- Vehicle inventory is gradually increasing as [assembly plants] are operating at 100 percent in order to replenish production lost during the COVID-19 shutdown.

- We are seeing supply-chain delays.

- Inventories continue to be a challenge, both in parts and vehicle day supplies

Building Material and Garden Equipment and Supplies Dealers

- Our sales are down about 8 percent from last year, but we're making adjustments that should help us grow next year even though we feel that the economy may not be doing as well because of all the small businesses that will not reopen. We're gambling that being aggressive during this down period will pay off, and we're able to do this based on our balance sheet with no debt and good cash flow.

Historical Data

Historical data can be downloaded dating back to January 2007.

Indexes

Download indexes for all indicators. For the definitions of all variables, see Data Definitions.

Texas Service Sector Outlook Survey |

Texas Retail Outlook Survey |

| Unadjusted | Unadjusted |

| Seasonally adjusted | Seasonally adjusted |

All Data

Download indexes and components of the indexes (percentage of respondents reporting increase, decrease, or no change). For the definitions of all variables, see Data Definitions.

Texas Service Sector Outlook Survey |

Texas Retail Outlook Survey |

| Unadjusted | Unadjusted |

| Seasonally adjusted | Seasonally adjusted |

Questions regarding the Texas Service Sector Outlook Survey can be addressed to Christopher Slijk at christopher.slijk@dal.frb.org.

Sign up for our email alert to be automatically notified as soon as the latest Texas Service Sector Outlook Survey is released on the web.