Texas Service Sector Outlook Survey

Texas service sector activity holds steady

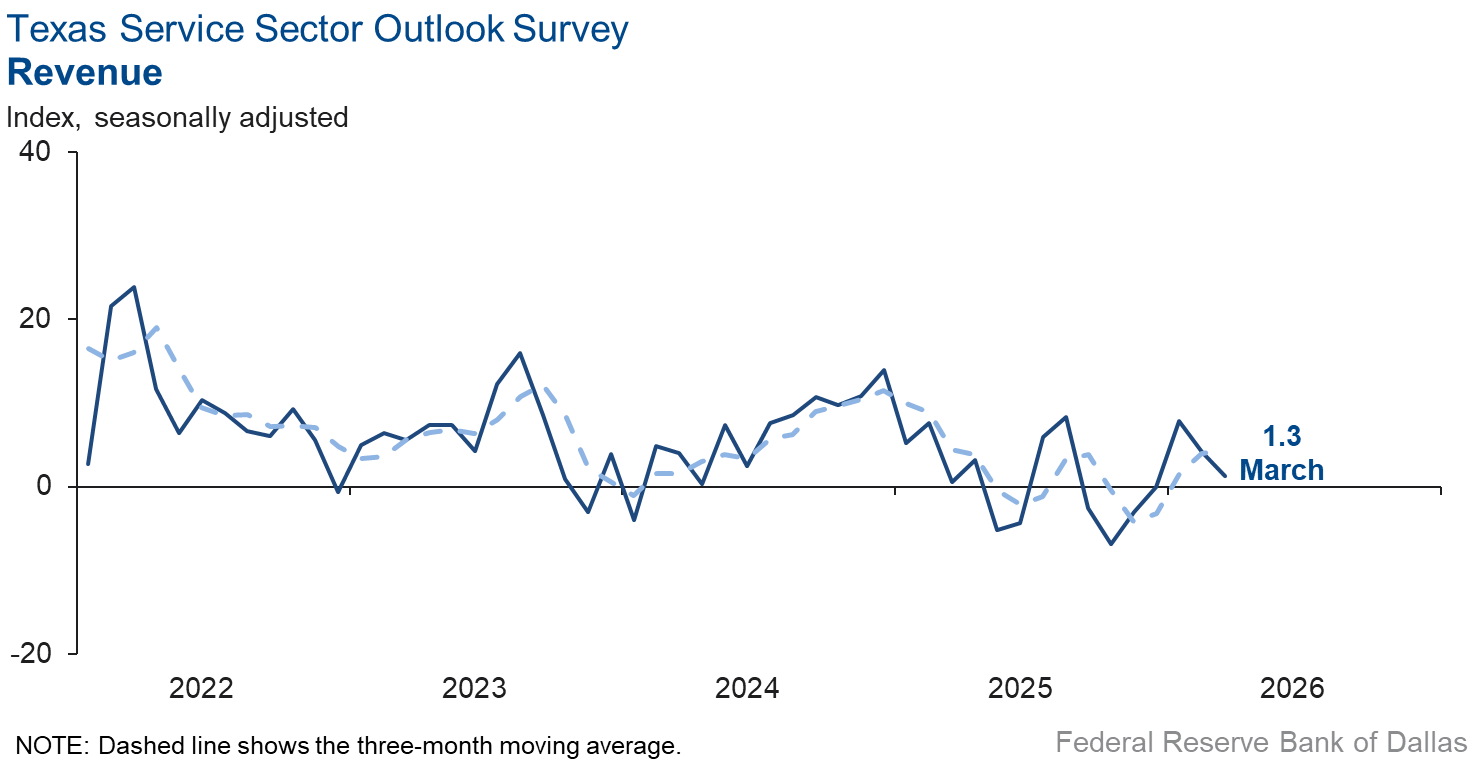

Texas service sector activity was little changed in March, according to business executives responding to the Texas Service Sector Outlook Survey. The revenue index, a key measure of state service sector conditions, fell three points to 1.3, with the near-zero reading indicating flat revenue.

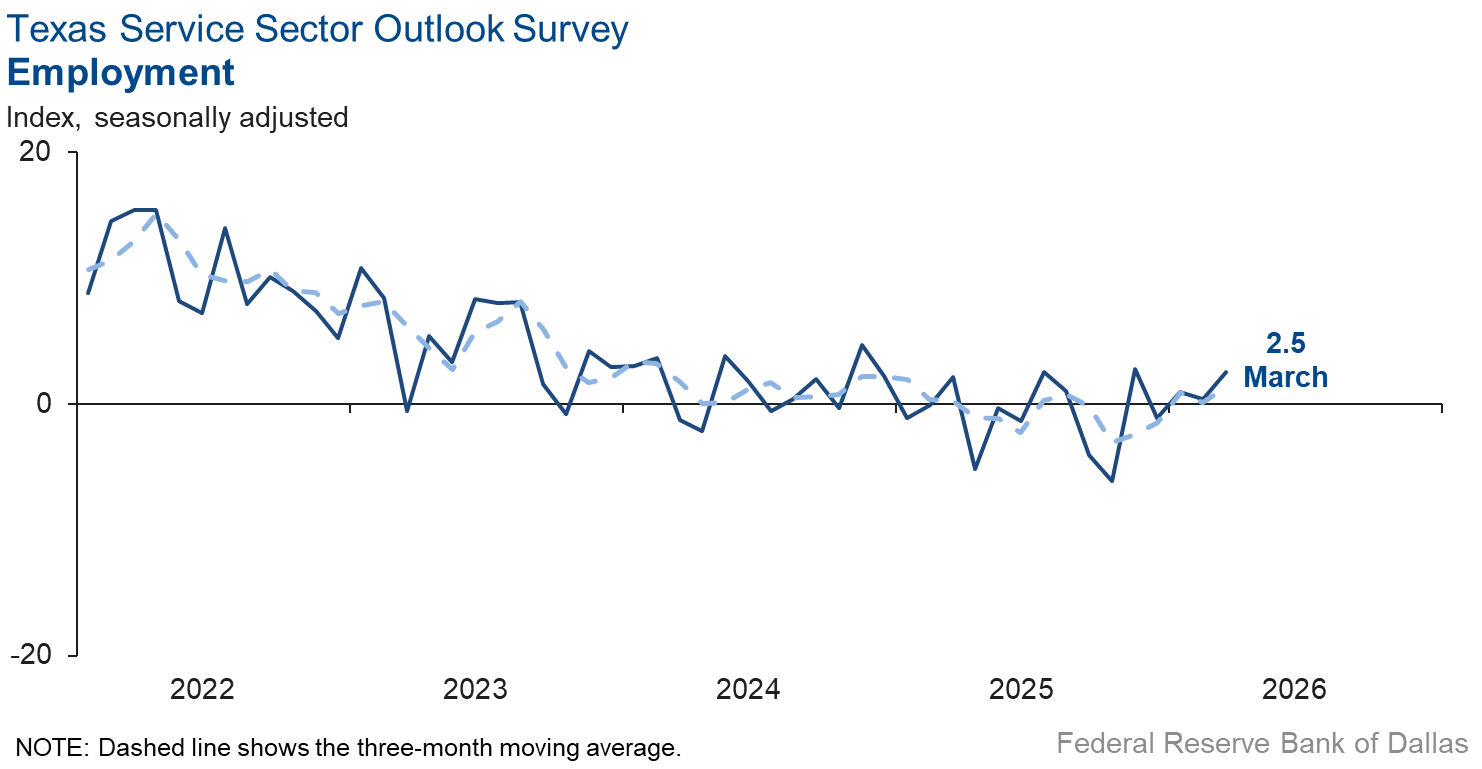

Labor market measures suggested employment increased slightly in March, though hours worked were unchanged. The employment index edged up two points to 2.5. Both the part-time employment and hours worked indexes registered near-zero readings, suggesting little change from February.

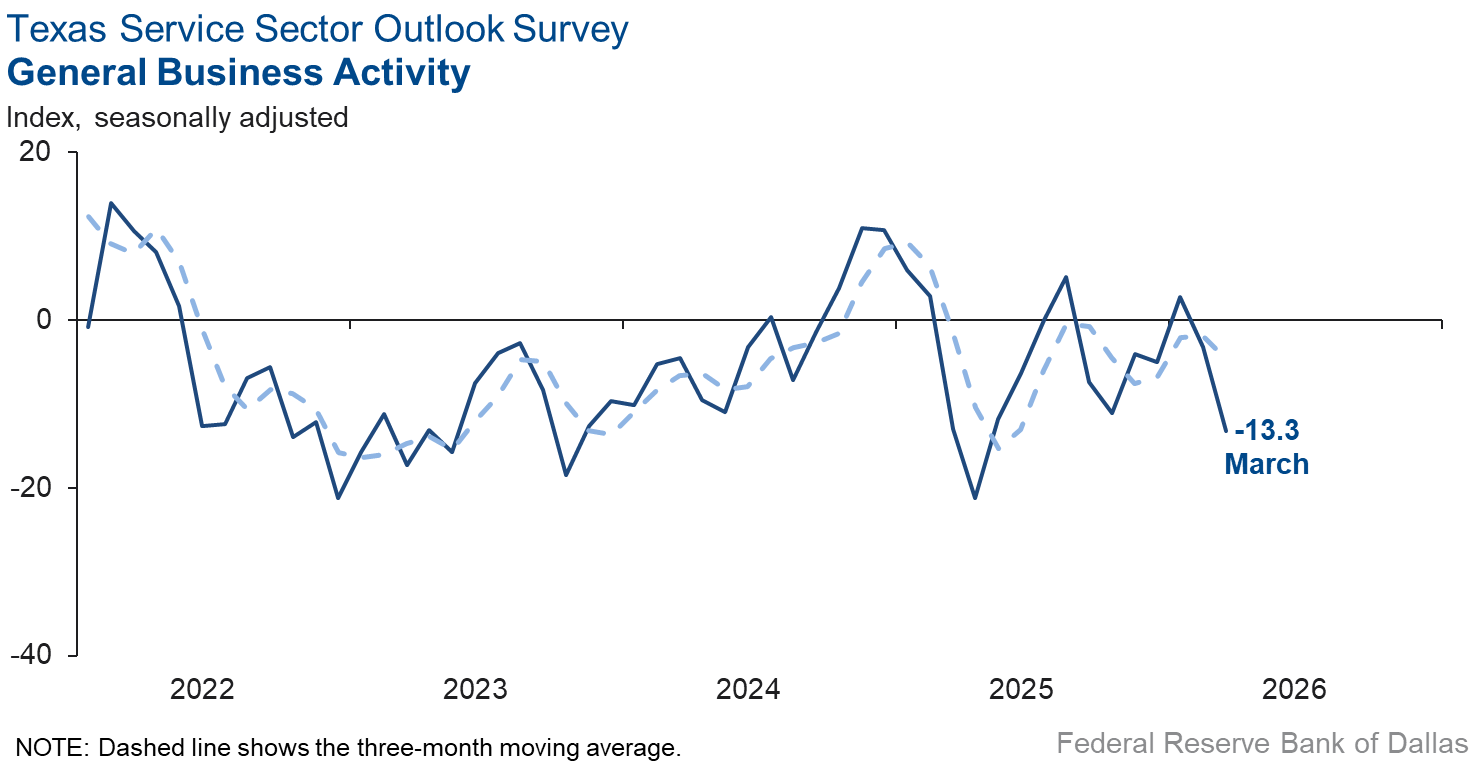

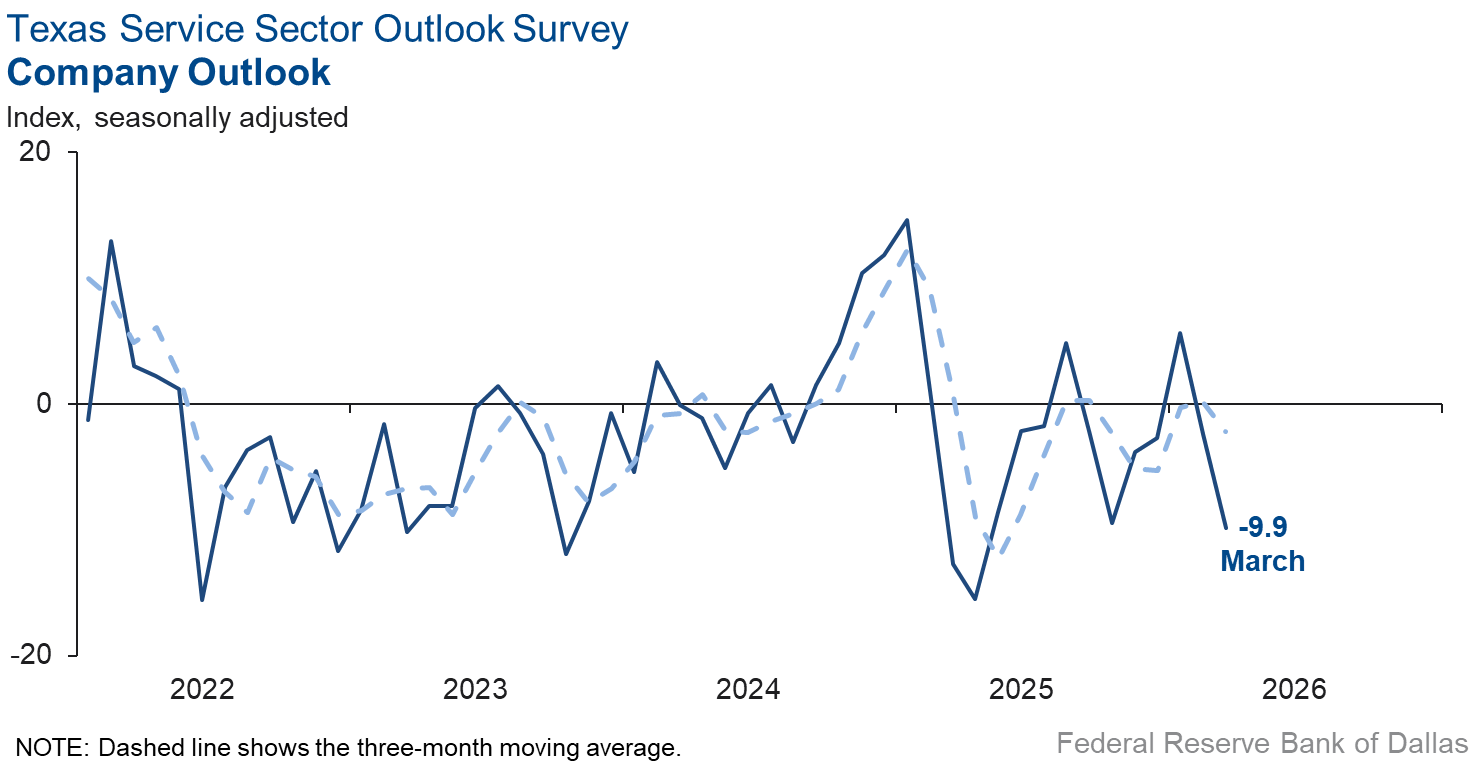

Perceptions of broader business conditions worsened substantially in March. The general business activity index fell 10 points to -13.3. The company outlook index also declined, falling eight points to -9.9. Meanwhile, the outlook uncertainty index jumped up 18 points to 27.0.

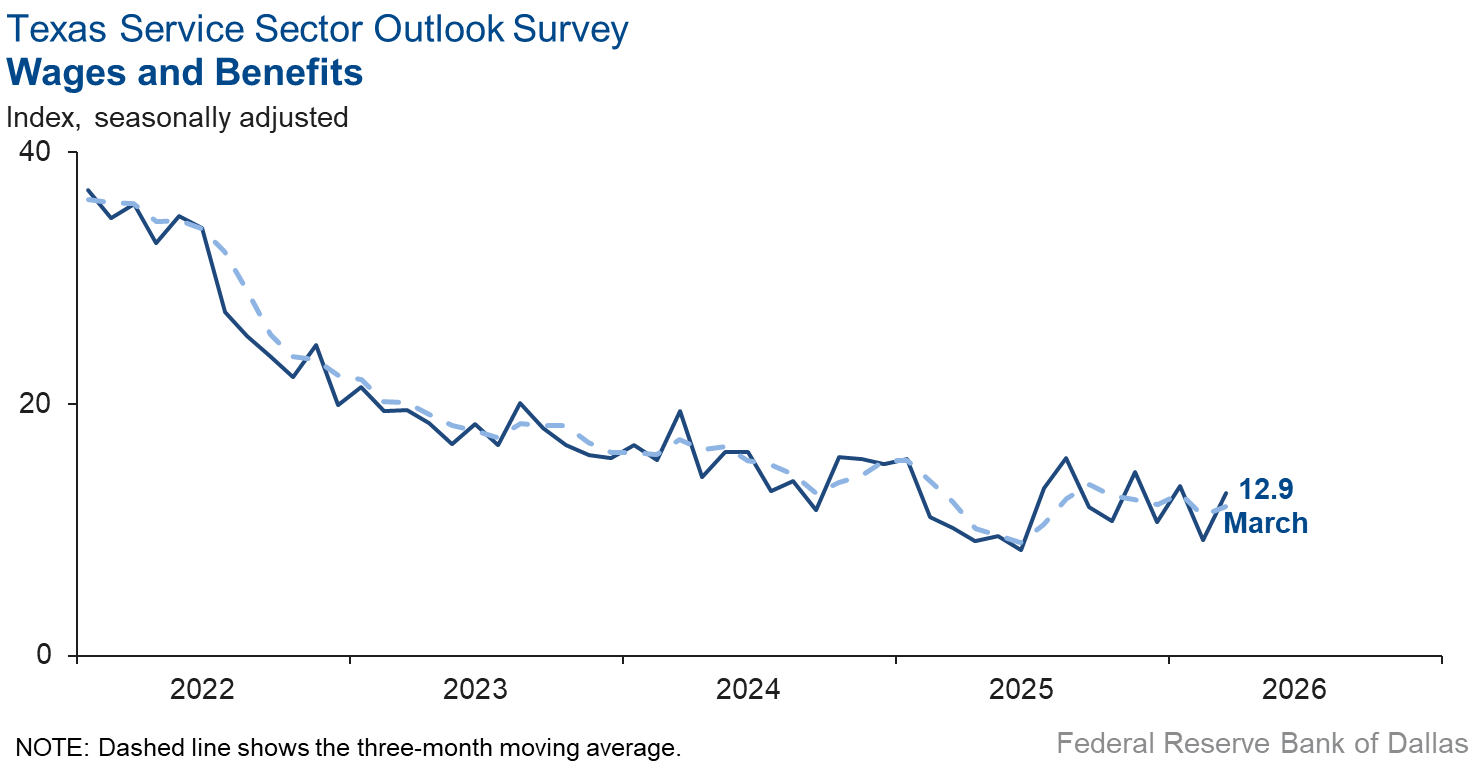

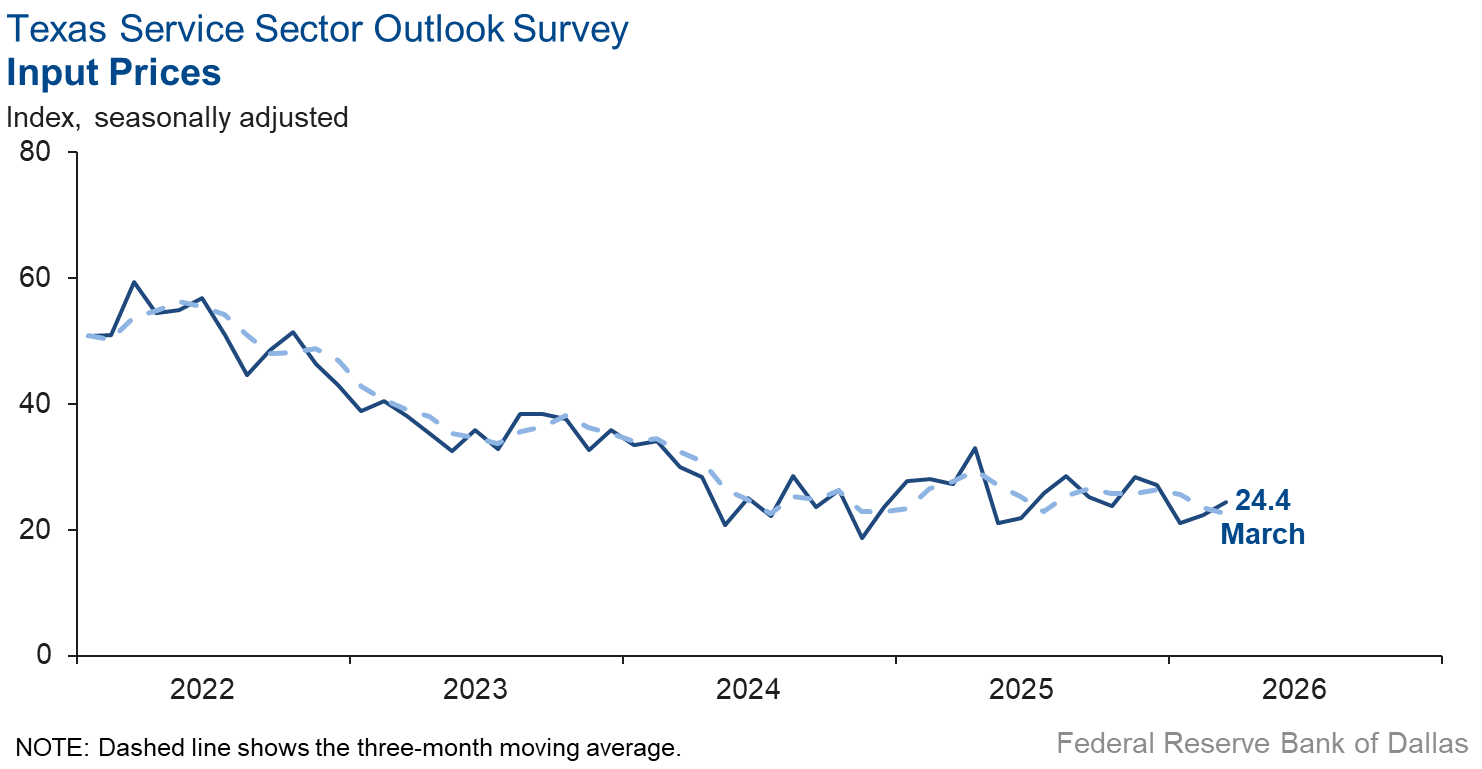

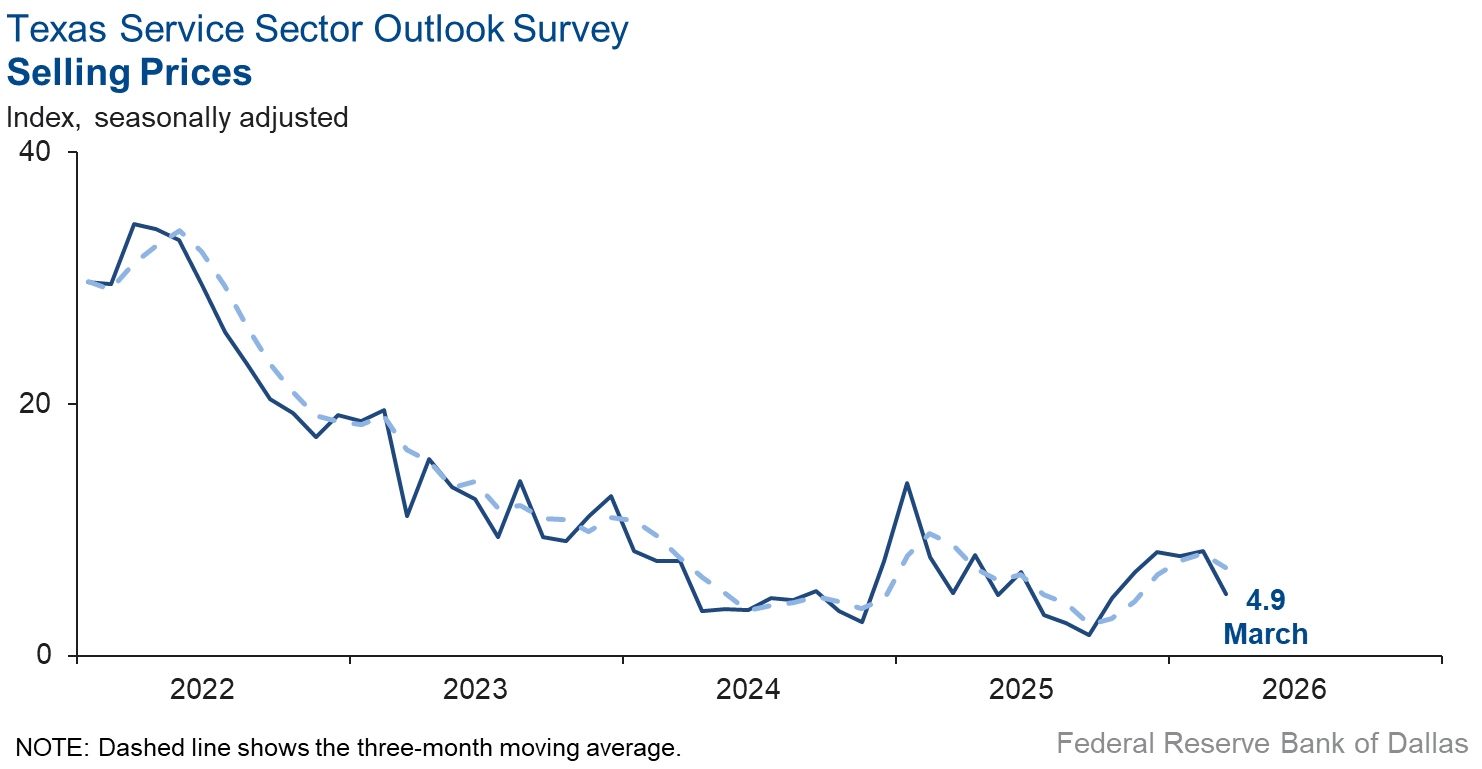

Selling price pressures eased while input price and wage pressures increased slightly. The selling prices index dipped to 4.9 from 8.3 in February. The input prices index edged up to 24.4 from 22.4 but remained below the series average of 27.7. Meanwhile, the wages and benefits index rose four points to 12.9.

Respondents’ expectations regarding future service sector activity remained positive but eased in March. The future revenue index ticked down six points to 32.8. The future general business activity index plunged 13 points to 2.3. Other future service sector activity indexes, such as employment and capital expenditures, remained in solidly positive territory.

Next release: April 28, 2026

Data were collected March 17–25, and 247 of the 352 Texas service sector business executives surveyed submitted responses. The Dallas Fed conducts the Texas Service Sector Outlook Survey monthly to obtain a timely assessment of the state’s service sector activity. Firms are asked whether revenue, employment, prices, general business activity and other indicators increased, decreased or remained unchanged over the previous month.

Survey responses are used to calculate an index for each indicator. Each index is calculated by subtracting the percentage of respondents reporting a decrease from the percentage reporting an increase. When the share of firms reporting an increase exceeds the share reporting a decrease, the index will be greater than zero, suggesting the indicator has increased over the prior month. If the share of firms reporting a decrease exceeds the share reporting an increase, the index will be below zero, suggesting the indicator has decreased over the prior month. An index will be zero when the number of firms reporting an increase is equal to the number of firms reporting a decrease.

Data have been seasonally adjusted as necessary.

Historical data are available from January 2007 to the most current release month.

| Business Indicators Relating to Facilities and Products in Texas Current (versus previous month) | ||||||||

| Indicator | Mar Index | Feb Index | Change | Series Average | Trend* | % Reporting Increase | % Reporting No Change | % Reporting Decrease |

Revenue | 1.3 | 4.1 | –2.8 | 10.0 | 3(+) | 23.6 | 54.1 | 22.3 |

Employment | 2.5 | 0.4 | +2.1 | 5.8 | 3(+) | 11.3 | 79.9 | 8.8 |

Part–Time Employment | 0.5 | –0.2 | +0.7 | 1.2 | 1(+) | 6.0 | 88.5 | 5.5 |

Hours Worked | –0.1 | –2.7 | +2.6 | 2.4 | 2(–) | 7.1 | 85.7 | 7.2 |

Wages and Benefits | 12.9 | 9.2 | +3.7 | 15.5 | 70(+) | 17.0 | 78.9 | 4.1 |

Input Prices | 24.4 | 22.4 | +2.0 | 27.7 | 71(+) | 28.3 | 67.8 | 3.9 |

Selling Prices | 4.9 | 8.3 | –3.4 | 7.4 | 68(+) | 15.6 | 73.8 | 10.7 |

Capital Expenditures | 6.4 | 4.5 | +1.9 | 9.7 | 68(+) | 12.2 | 82.0 | 5.8 |

| General Business Conditions Current (versus previous month) | ||||||||

| Indicator | Mar Index | Feb Index | Change | Series Average | Trend** | % Reporting Improved | % Reporting No Change | % Reporting Worsened |

Company Outlook | –9.9 | –2.4 | –7.5 | 3.9 | 2(–) | 13.5 | 63.1 | 23.4 |

General Business Activity | –13.3 | –3.2 | –10.1 | 1.8 | 2(–) | 14.1 | 58.5 | 27.4 |

| Indicator | Mar Index | Feb Index | Change | Series Average | Trend* | % Reporting Increase | % Reporting No Change | % Reporting Decrease |

Outlook Uncertainty | 27.0 | 9.3 | +17.7 | 14.0 | 58(+) | 38.8 | 49.3 | 11.8 |

| Business Indicators Relating to Facilities and Products in Texas Future (six months ahead) | ||||||||

| Indicator | Mar Index | Feb Index | Change | Series Average | Trend* | % Reporting Increase | % Reporting No Change | % Reporting Decrease |

Revenue | 32.8 | 38.3 | –5.5 | 37.2 | 71(+) | 46.5 | 39.9 | 13.7 |

Employment | 21.1 | 21.2 | –0.1 | 22.9 | 71(+) | 29.9 | 61.3 | 8.8 |

Part–Time Employment | 9.7 | 3.3 | +6.4 | 6.4 | 9(+) | 15.5 | 78.7 | 5.8 |

Hours Worked | 7.2 | 6.1 | +1.1 | 5.9 | 9(+) | 11.6 | 84.0 | 4.4 |

Wages and Benefits | 37.3 | 37.2 | +0.1 | 37.5 | 71(+) | 42.0 | 53.3 | 4.7 |

Input Prices | 45.1 | 37.5 | +7.6 | 44.2 | 231(+) | 49.9 | 45.2 | 4.8 |

Selling Prices | 22.4 | 16.6 | +5.8 | 24.4 | 71(+) | 32.4 | 57.6 | 10.0 |

Capital Expenditures | 15.1 | 17.2 | –2.1 | 22.4 | 70(+) | 23.1 | 68.9 | 8.0 |

| General Business Conditions Future (six months ahead) | ||||||||

| Indicator | Mar Index | Feb Index | Change | Series Average | Trend** | % Reporting Improved | % Reporting No Change | % Reporting Worsened |

Company Outlook | 9.2 | 13.8 | –4.6 | 15.3 | 11(+) | 26.4 | 56.4 | 17.2 |

General Business Activity | 2.3 | 15.0 | –12.7 | 11.9 | 10(+) | 23.3 | 55.7 | 21.0 |

*Shown is the number of consecutive months of expansion or contraction in the underlying indicator. Expansion is indicated by a positive index reading and denoted by a (+) in the table. Contraction is indicated by a negative index reading and denoted by a (–) in the table.

**Shown is the number of consecutive months of improvement or worsening in the underlying indicator. Improvement is indicated by a positive index reading and denoted by a (+) in the table. Worsening is indicated by a negative index reading and denoted by a (–) in the table.

Data have been seasonally adjusted as necessary.

Comments from survey respondents

Survey participants are given the opportunity to submit comments on current issues that may be affecting their businesses. Some comments have been edited for grammar and clarity.

- Global conflict, increasing energy costs and a government shutdown that is affecting TSA all represent increasing headwinds to an already sluggish economy. The self-inflicted uncertainty we are dealing with is hurting group and convention business and the average family's vacation plans.

- Wars and disruptions will always increase uncertainty. High oil prices are net good for Texas, but we cannot carry the load for the whole country.

- Interest rates are stifling any opportunity for improvement.

- The number of possible reasons for economic uncertainty has increased even more in the past month. As if tariffs, government deficits and AI were not enough, now add war and a likely energy price shock.

- The Dallas-Fort Worth professional employment market remains marked by significant uncertainty. Companies that are hiring are doing so reluctantly, deliberately and slowly. Decision-making timelines have stretched considerably, leading to prolonged hiring processes and real productivity losses for organizations. On the candidate side, economic uncertainty is keeping people in place; fewer professionals are willing to make a move right now. The result is a market that hasn't stopped but has largely stalled—fewer employers hiring, fewer candidates looking and very little momentum on either side.

- Geopolitical issues and heightened operating risk profile, including higher energy prices as well as a likely increase in interest rates and the incremental impact of tariffs and immigration enforcement [are issues impacting our business].

- Military issues generate secondary concerns and angst. The effect are likely shorter term and will correct by end of the year.

- The reduction in interest rates has improved the lead, application and contract numbers greater than what we would expect.

- There are many unique variables causing concerns in forecasting the future business activity. The volatility of fuel prices will cause inflation to be a factor for the economy.

- Consolidation of current clients and prospects is shrinking the market and affecting purchasing decision-making. Uncertainty presented by AI is putting purchasing decisions for software on hold. The hype versus reality is confusing buyers who don't want to make a wrong decision. Lastly, current monetary policies are hurting small businesses. The difficult borrowing climate over the past two years for small businesses has favored very large businesses that have cash and capital, to the point of squeezing smaller, innovative companies. This is even giving very large companies an edge over our small yet highly innovative business during contract renewals with longstanding customers. Due to this, rising bankruptcy rates for small businesses are not a surprise.

- Political uncertainty affects everything we do.

- Input costs are rising. We will have to go up in price and do less sales.

- The Iran war is causing fuel prices to keep going higher, stocks are going up and down every day, and people are afraid of the future.

- The onset of military action in Iran combined with an increasingly volatile legislative environment has heightened longer-term concerns about economic stability. But we remain bullish that favorable business conditions will persist in our Texas market. Margin and overall profitability have both been heavily impacted by the imposition of tariffs on green coffee. This is generally misunderstood, as conventional wisdom tends to limit the expected negative impacts to coffees originating in Brazil, but this ignores the impact that limiting this supply had on other coffee markets, namely Colombian, Central American and African coffees. Demand that would otherwise have been filled by the Brazilian coffees was transferred to coffees from other origins, creating severe upward pricing pressure. Overall, our three primary green-coffee-category costs have increased between 41 and 114 percent since late 2024. For many roasters, this may prove to be the end of their business model. Fortunately, our retail cafe business provides a buffer to this supply chain shock, and we are forecasting that our average coffee costs will come somewhat back to normal by mid-summer. But this has proven to be a tremendously costly experiment for those of us in the retail and wholesale coffee business.

- War with Iran has upset the cart, and nothing feels safe. The chaos in Washington is stressful. Rising gas price and rising inflation will be eating away at Americans' security when deciding what to cut from their monthly budgets. I hear a lot of complaining about the prices of groceries, eating out and travel.

- Geopolitical uncertainty is changing the economic outlook of our customers. Oil and fuel costs are changing spending habits.

- The threat of AI lowered the stock prices of public companies in our industry. This made the value a company would acquire ours for go down.

- Geopolitical uncertainty and gas prices, along with TSA uncertainty, cause people to question spending, travel, etc. Specific to our insurance business, some people worry about terrorism, vandalism, etc. but only superficially so far, until something really happens, which I feel will occur this calendar year.

- The year started off strong, but the geopolitical issues in the Middle East are causing some concerns. Higher oil prices will drive up product costs as well as freight and delivery costs. Any increase in costs could cause a slowdown in business activity.

- Bombing Iran has brought significant disruption to the oil market, which has driven oil and diesel prices higher. Over the very short term (less than 30 days), we will absorb some of this cost. But next month, we will need to raise prices because diesel is a direct cost in shipping and significantly impacts our margins.

- Consumer confidence is currently weak for discretionary spending.

- Uncertainty remains a problem. Business conditions are subject to change based on the many uncertainties. January and February were both disappointing months, and March is not pacing at its usual level. Affordability is a major concern. Beyond tax refunds for some, there is nothing to suggest relief soon. Net sales don't suggest improved profitability. Margins are eroding.

- Elevated fuel prices are always concerning in the automobile business. Strained affordability continues to be an issue, but not as much at our luxury-brand dealerships. If we see continued increases in fuel prices, it will ultimately affect our business and our employees.

- I felt a little better, but now with gas pricing, it seems our shipping will go up, and that is really hard to pass onto the customer or add into the pricing.

- I am concerned about the impact of the war to the pocketbooks of Americans.

- Consumer confidence is key to our ability to maintain margins and/or grow total sales. Uncertainty in the economy has a significant impact on our sales and average price. We operate on a largely fixed price model, so yield optimization is critical. We are pessimistic about the coming months.

- Inflation and rising costs [are issues impacting our business]. Customers are uncertain.

- I have some concerns about the Iran war and increasing oil prices causing inflation.

- The self-inflicted damage to our economy from the attacks on Iran and its retaliation to its Gulf neighbors could become disastrous. Time will tell.

- Iran war has made things in the energy world a nightmare. Ending of the war would open opportunity for engineering and construction in rebuilding Middle East LNG and oil processing facilities in countries that have been attacked by Iran.

- Market uncertainty has restricted client interest in renewing contracts at this time.

- Uncertainty is at best a real downer for normal business activities.

- The uncertainty over the war with Iran and its ripple effects throughout the country and the world are obviously affecting economic activity and spending.

- Global uncertainty, higher oil prices, higher wages and employees demanding more benefits and paid time off are all price pressures to pass on to our customers.

- Things look much better in terms of activity, but I am not sure what is causing this. I also remain concerned about sustaining the level of activity.

- We're all on pause. We expect greater clarity in six to eight weeks.

- Until the war has ended, I am not certain how to make projections. Best-case scenario is no change [in business activity]. There are signs that the job market is softening, but it is not certain.

- The year started out with a lot of companies wanting to hire but it seems to be slowing a bit. The positions that we are asked to fill the most often are accounting, finance and experienced sales professionals.

- General economic conditions are softening. Talent is becoming more available with some companies reducing workforce and government spending for professional services decreasing.

- Our clients are feeling the strain of increases in the cost of business. Continued increases to operating costs (gas, supplies), with no matches in increased revenue has them reviewing expenditures and cutting costs. It is a fine linethat they are dancing, making expense-cutting necessary when rising prices are not able to be absorbed over continued periods of time.

- We rely on the H-2B visa program for seasonal staffing. The delays at the Department of Labor due to the partial shutdown will have a significant negative impact on our business for March and April.

- Recent geopolitical developments, particularly the conflict involving Iran, have contributed to a noticeable slowdown in real estate market activity. Market participants appear to be taking a cautious approach as they assess the potential impact on inflation and interest rates. While there had been early indications of the beginning of a new real estate cycle, ongoing uncertainty, especially if the conflict becomes prolonged, could delay or disrupt that momentum. We will continue to monitor economic indicators closely as conditions evolve.

- The Iran war, increases in materials costs and lots of instability [are issues impacting our business].

- Our business is regulated by [the State of] Texas, and it dropped the amount we can collect. So, even though our costs are still increasing, the amount we can charge is decreasing.

- More of our work depends on U.S. government contracting. Political volatility disrupts payments and cash flow.

- We are seeing some pressure to lower our prices. It seems like our market is contracting a little. Luckily, we have invested in becoming more efficient. I think we can lower our prices slightly and still maintain our profitability.

- I am feeling the stress of increased gas prices, the increase in the 2026 IRS mileage reimbursement rate and our company policy of reimbursing at that rate. This is coupled with the decreasing volume of "big ticket" work. We are still receiving inquiry calls, but at a lesser rate, and the work is smaller projects. Nonprofits are figuring out ways to minimize the need for our type of capacity-building work, and we are starting to feel it.

- I think most businesses and industries are in a holding pattern due to an iffy economy and the Middle East war. I think if the war is resolved relatively soon and the Strait of Hormuz secured, the economy will react in a very positive manner.

- No impact to date from increased fuel prices, but we are anticipating it later this year.

- Rising oil and gas prices will once again make public infrastructure project costs exponentially increase. We had just started to stabilize.

- Our company has a large fleet of vehicles used to deliver our services. Increasing fuel prices are raising our costs and affecting our profitability.

- AI is helping us reduce our costs to provide our services in addition to accelerating our ability to deliver our services.

- There are signs of a pull-up in demand outside of a normal business cycle. Industrial and land development sectors are extremely busy, and activity is brisk. However, we see early warning signs of economic weakness in the second half of 2026.

- Our company outlook remains the same. The influencing factors for second quarter 2026 are the delayed 2026 federal budget approval, a slower pace of contract activity in February and March, some backlog spillover from 2025 disruptions and, in some cases, a shrinking or constrained federal acquisition staff.

- The war [is an issue impacting our business].

- We've seen a flurry of requests for quotations from the private and public sectors, but selection decisions and awards are slow to actualize.

- There has been more uncertainty with government projects. It is harder to predict funding approvals.

- When there is uncertainty, people get nervous and hold on to their money. Travel is difficult, and the Iran war is unsettling.

- Overall, the business of owning and operating workforce apartments is stagnant. Few people are moving by choice. A majority of those who are moving have issues, are unqualified or are presenting fake documents. The leverage that fueled the run-up continues to haunt those who are burdened with it. There are plenty of willing buyers for multifamily assets, but sellers are only letting go if they have to. Valuations on the books remain significantly higher than rational market prices.

- We are actively working toward liquidating a real estate investment trust and spinning off a small self-storage company.

- We are a heavy construction machinery dealership with 27 stores in Texas, Oklahoma and New Mexico. We have 750 employees. We have just finished maybe the two slowest months we have ever had. We finished February down 10.4 percent after being down 5 percent at the end of January. I think people are out of money. Even if we provide 0 percent, 60 month financing for new equipment, they are not taking on new debt. On the other side of the ledger, my employee health coverage jumped 39 percent this year for no reason. I provide it for our people, but they have to pay for coverage for their dependents, and they cannot afford a 39 percent increase. Their wages have probably increased 24.5 percent in the last 3 years but not 39 percent in the last year.

- The war, decline in stock markets and increased fuel prices are adding to uncertainty in the broader economy. Uncertainty always negatively impacts hiring decisions.

- The lack of moisture is hurting all agriculture. Higher oil prices will increase royalty incomes, and data center construction will tighten the job market.

- All of my clients, friends and family that own businesses are reporting a rough February into March, with sales down. Inflation will also be up significantly. Oil and gas, along with nondurable goods, are up quite a bit. I would not be surprised to see an inflation figure north of 3 percent.

- The war against Iran has caused my inflation outlook to worsen and likelihood of Fed decreasing interest rates to decline or be eliminated. I now fear stagflation. Success of my business is linked to job growth and low interest rates, both of which seem unlikely to occur.

- Given the quickly changing policies from the current administration, we have found it very difficult to predict and meet the needs of our community. The policies I am referring to are the impact of tariffs, immigration, and the dissolution of the Department of Education.

- I am optimistic that the remainder of the year will see improved market conditions for trucking, based on continued [regulatory] enforcement and increased activity in the manufacturing sector.

- The Iran war has increased uncertainty.

- The Iran war is increasing short-term revenues from oil shipments, but I would expect to see a corresponding dip once the conflict is resolved as stranded oil around the Strait of Hormuz begins to move again. Shipments of crude oil, which is 60 percent of our business usually, are up roughly 25 percent in the past 5 weeks.

Special questions

For this month’s survey, Texas business executives were asked supplemental questions on wages, prices and outlook concerns. Results below include responses from participants from both the Texas Manufacturing Outlook Survey and Texas Service Sector Outlook Survey. View individual survey results.

Historical Data

Historical data can be downloaded dating back to January 2007.

Indexes

Download indexes for all indicators. For the definitions of all variables, see data definitions.

| Unadjusted |

| Seasonally adjusted |

All Data

Download indexes and components of the indexes (percentage of respondents reporting increase, decrease, or no change). For the definitions of all variables, see data definitions.

| Unadjusted |

| Seasonally adjusted |

Questions regarding the Texas Service Sector Outlook Survey can be addressed to Isabel Brizuela.

Sign up for our email alert to be automatically notified as soon as the latest Texas Service Sector Outlook Survey is released on the web.