Texas Service Sector Outlook Survey

Growth resumes in Texas service sector

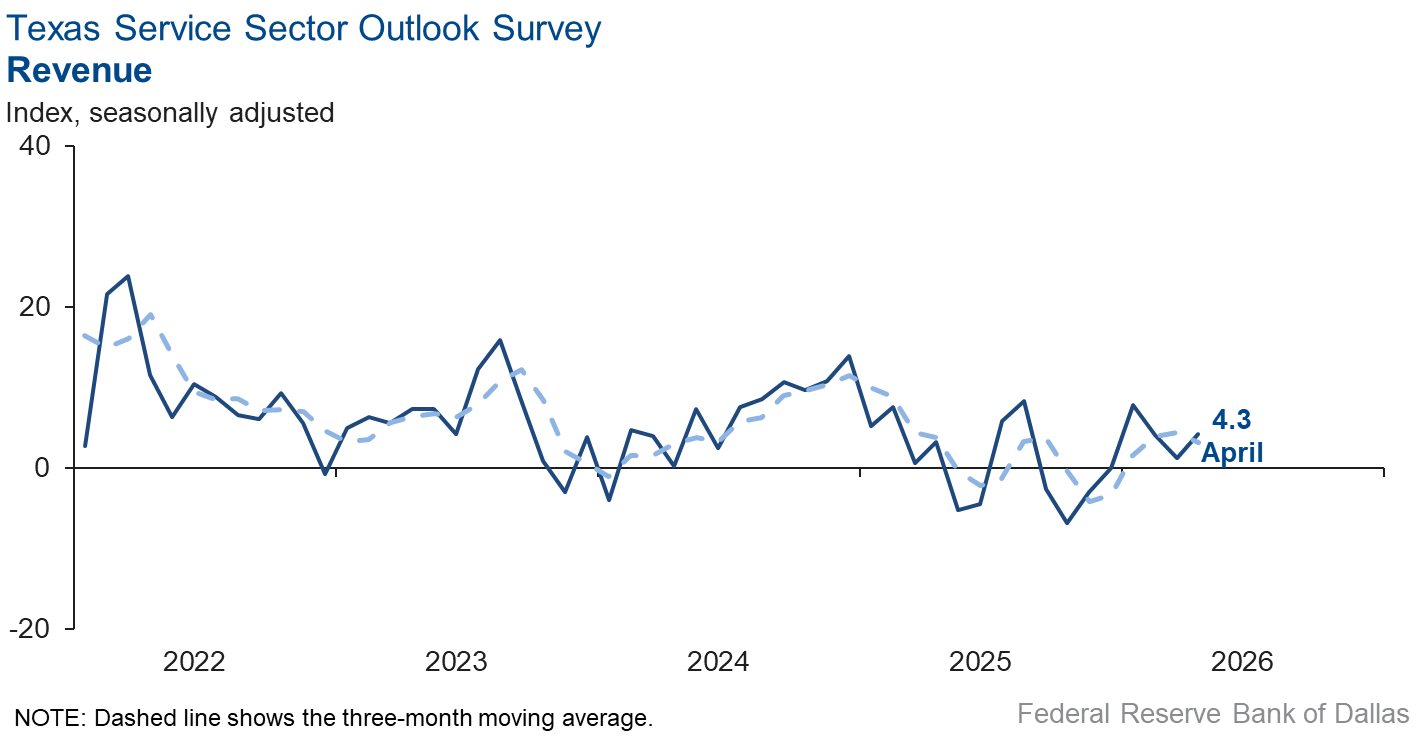

Texas service sector activity increased in April, according to business executives responding to the Texas Service Sector Outlook Survey. The revenue index, a key measure of state service sector conditions, edged up three points to 4.3, suggesting revenue increased slightly.

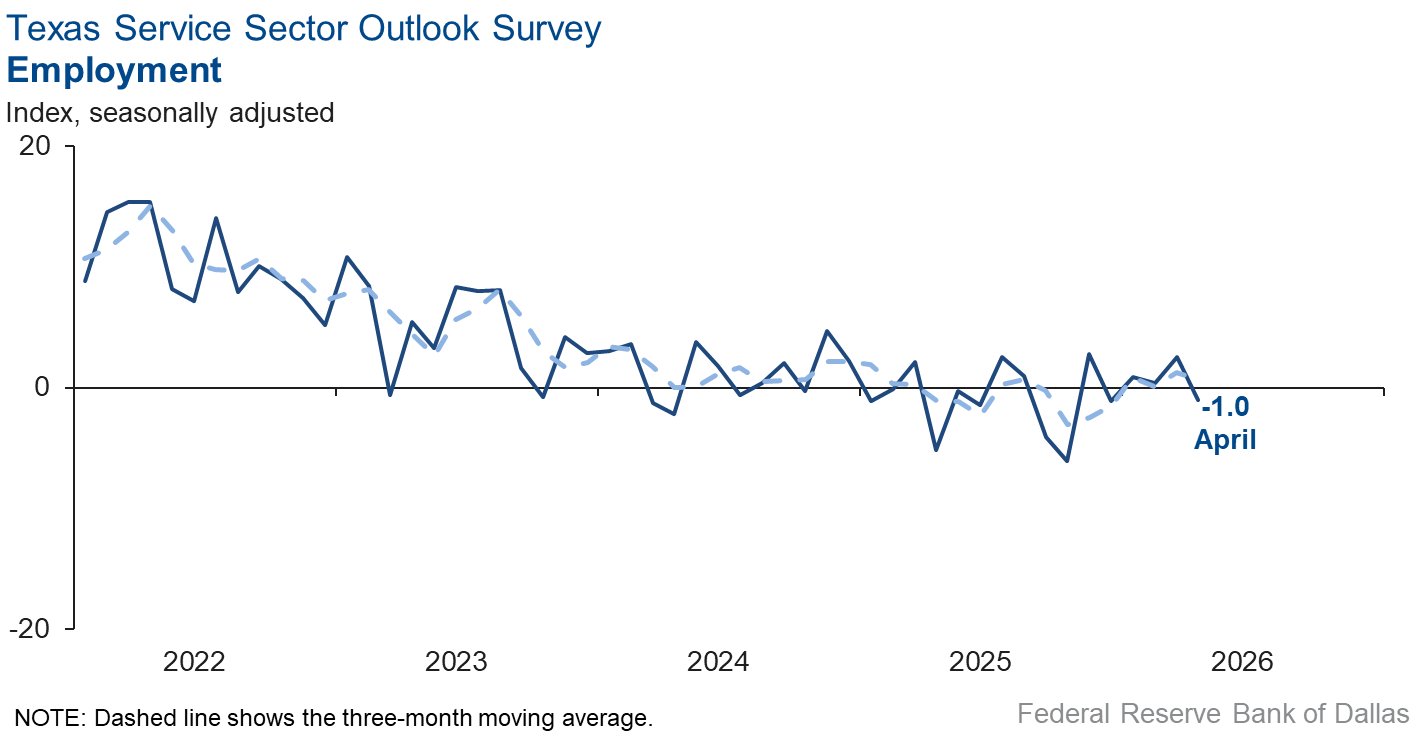

Labor market measures suggested both employment and workweeks were unchanged in April. The employment, part-time employment and hours worked indexes all registered near-zero readings, indicating little change from March.

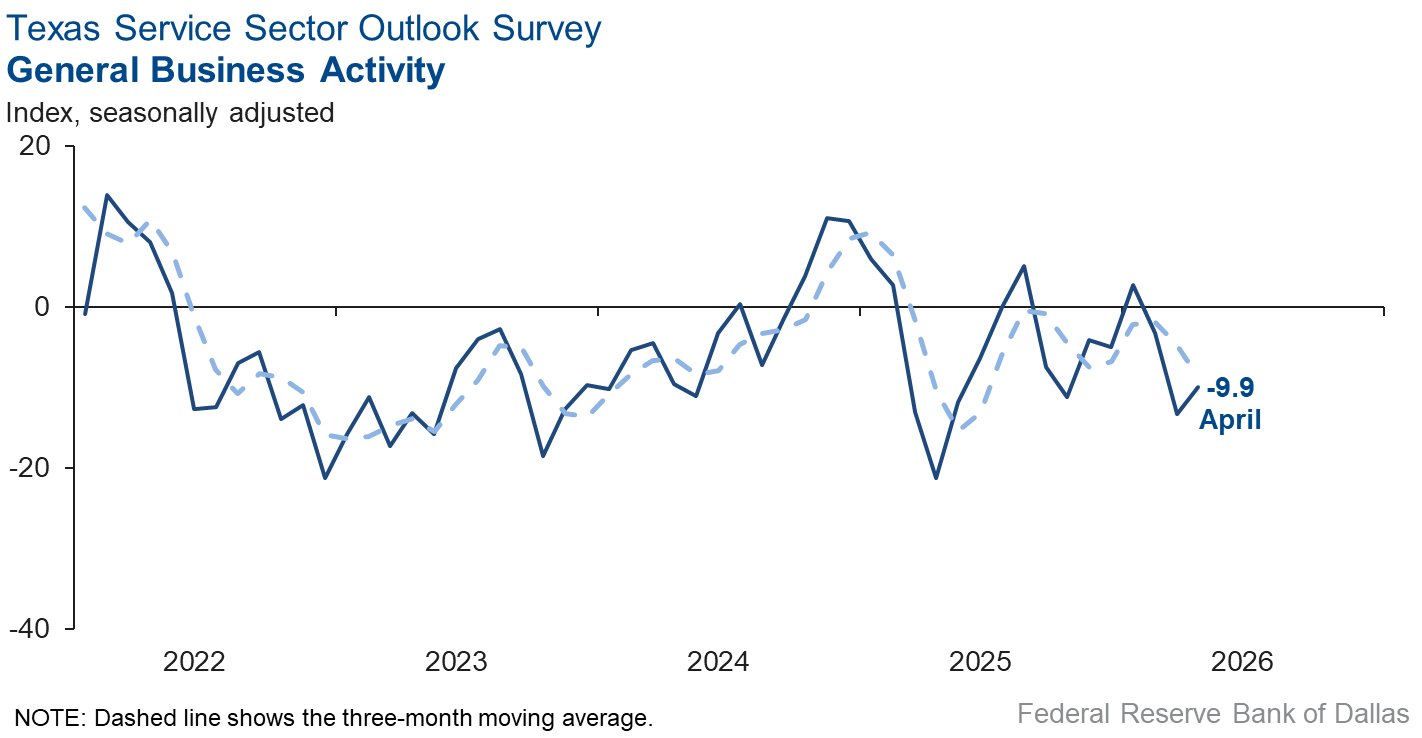

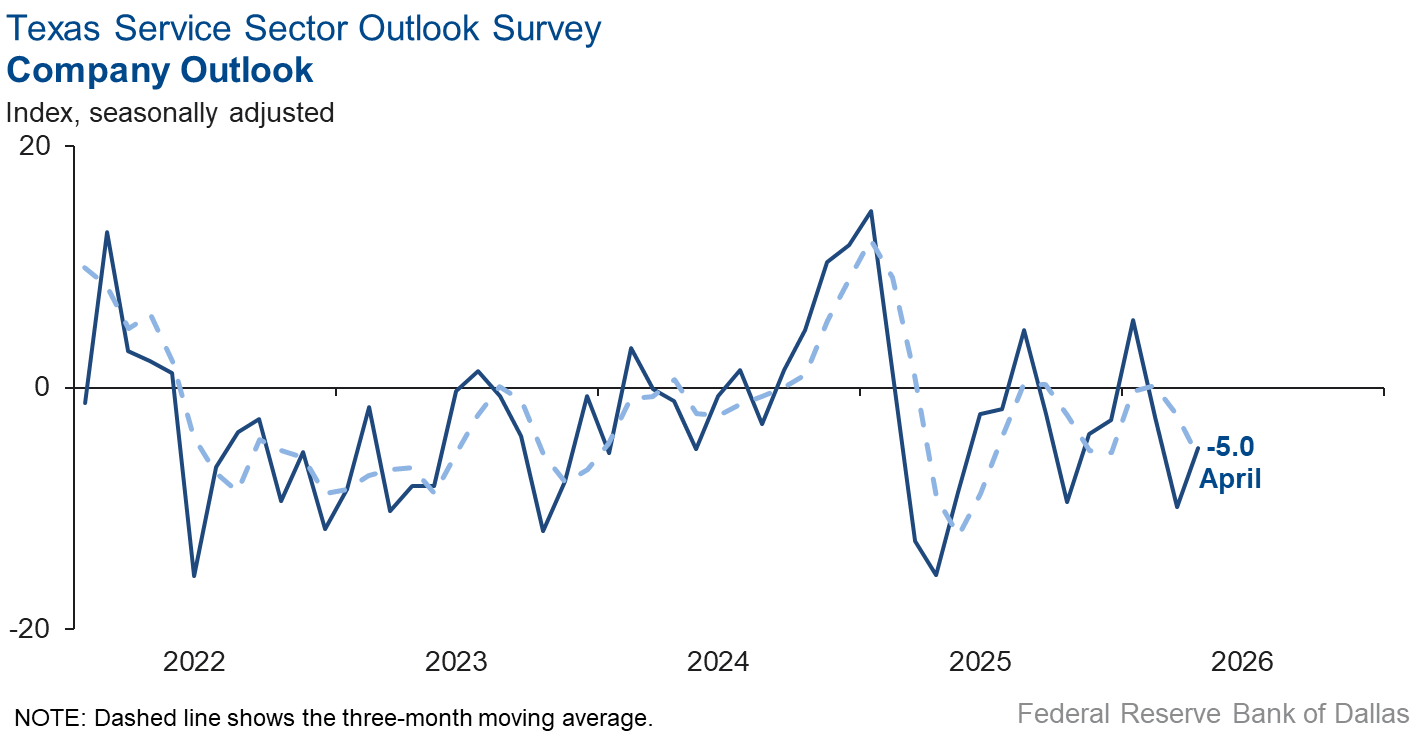

Perceptions of broader business conditions continued to worsen in April, though the indexes were less negative than the prior month. The general business activity index ticked up three points to -9.9, and the company outlook index rose five points to -5.0. Meanwhile, the outlook uncertainty index dipped two points to 24.8 but was still well above the series average of 14.1.

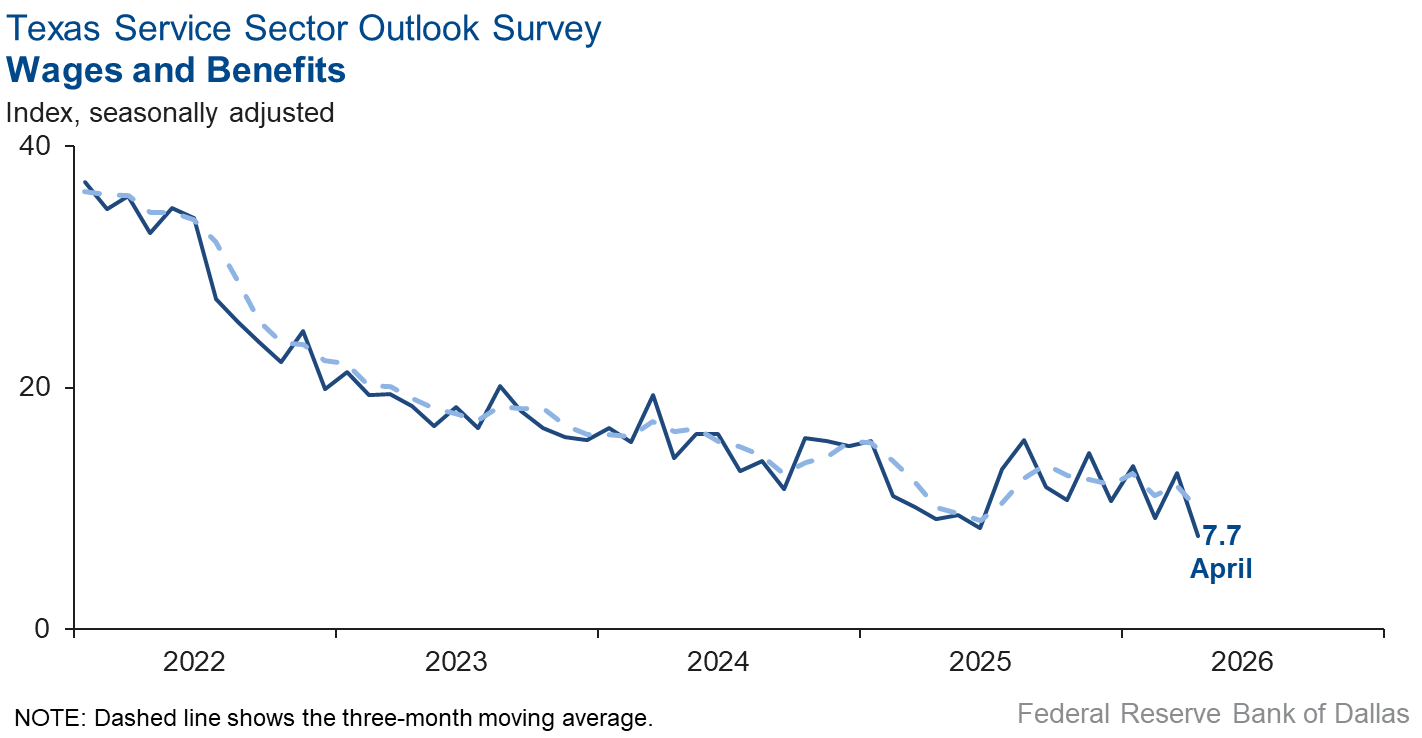

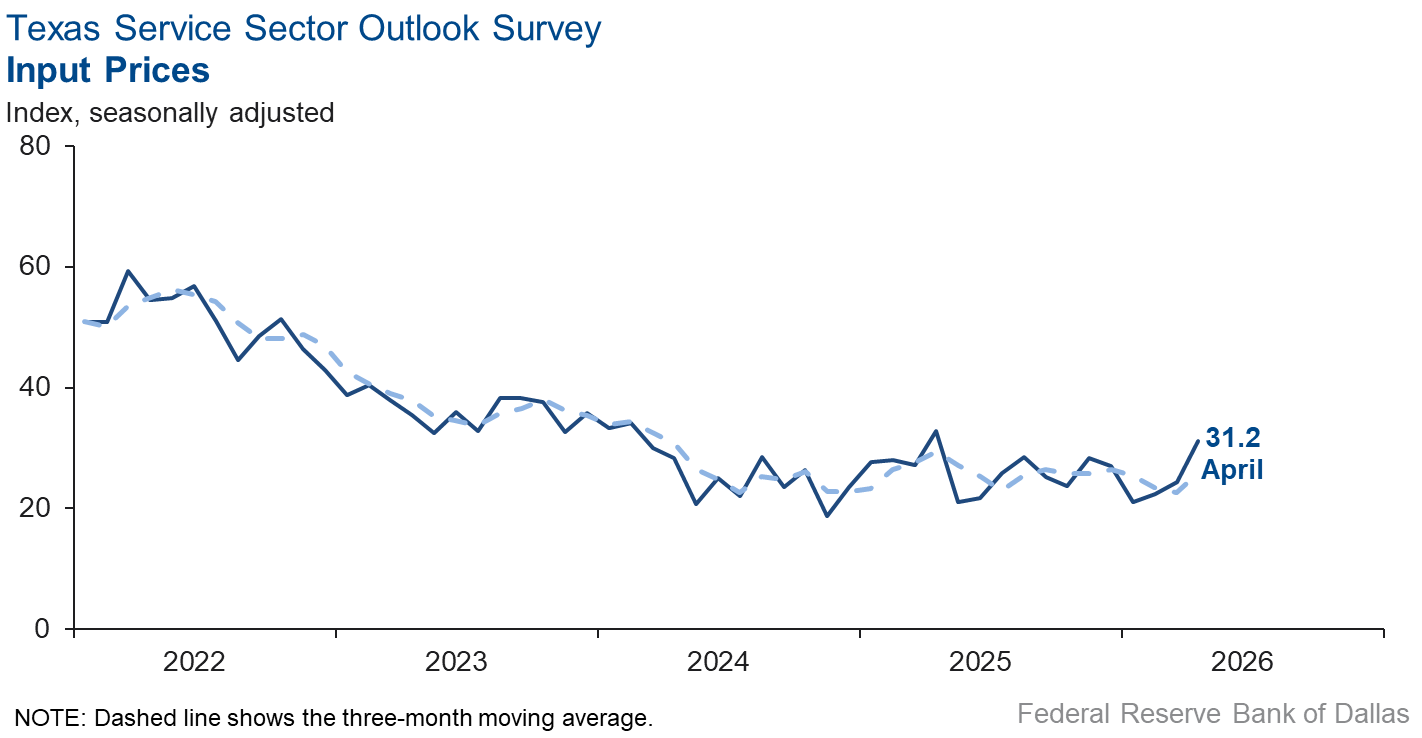

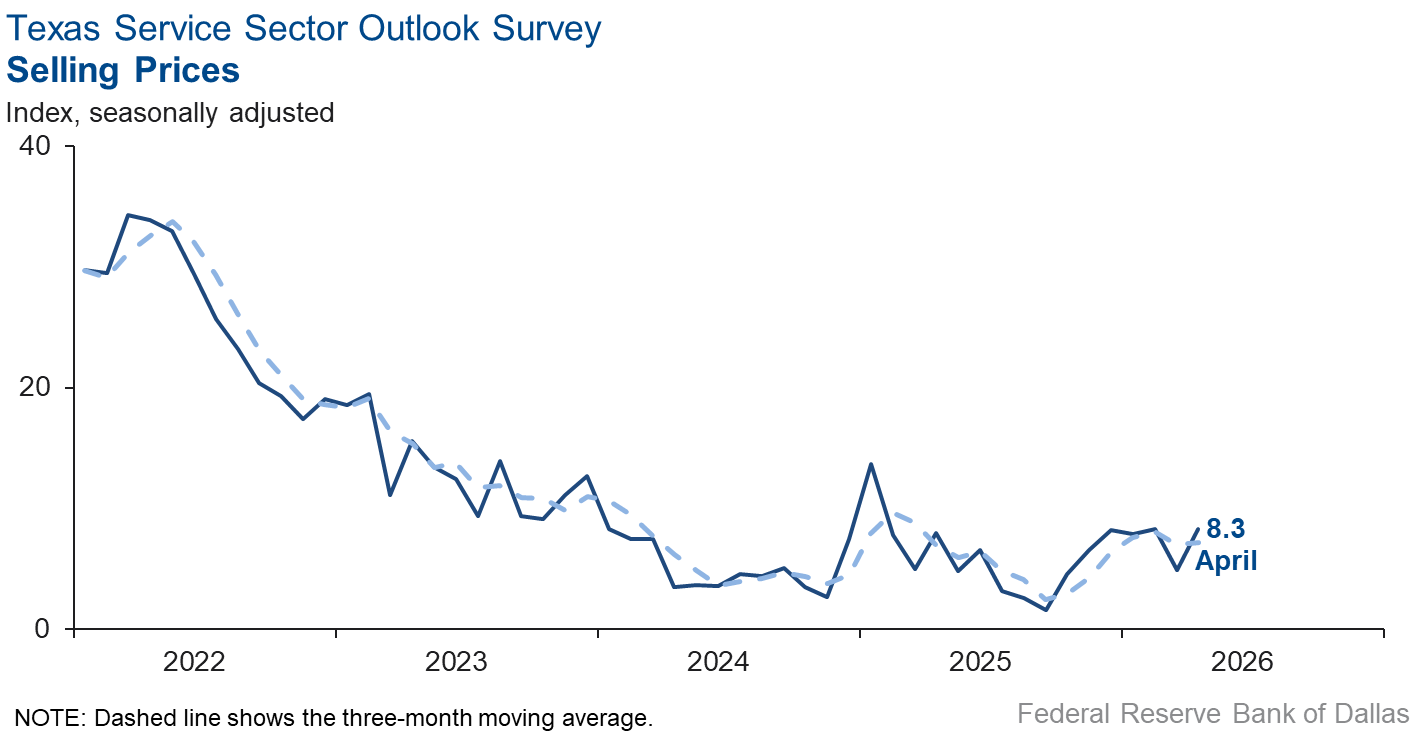

Selling and input price pressures increased while wage pressures eased. The selling prices index increased slightly to 8.3 from 4.9 in March. The input prices index rose seven points to 31.2, surpassing the series average of 27.7. Meanwhile, the wages and benefits index fell five points to 7.7.

Respondents’ expectations regarding future service sector activity improved. The future revenue index was little changed from March at 31.5. The future general business activity index edged up two points to 4.7. Other future service sector activity indexes, such as employment and capital expenditures, remained in positive territory.

Next release: May 27, 2026

Data were collected April 14–22, and 244 of the 349 Texas service sector business executives surveyed submitted responses. The Dallas Fed conducts the Texas Service Sector Outlook Survey monthly to obtain a timely assessment of the state’s service sector activity. Firms are asked whether revenue, employment, prices, general business activity and other indicators increased, decreased or remained unchanged over the previous month.

Survey responses are used to calculate an index for each indicator. Each index is calculated by subtracting the percentage of respondents reporting a decrease from the percentage reporting an increase. When the share of firms reporting an increase exceeds the share reporting a decrease, the index will be greater than zero, suggesting the indicator has increased over the prior month. If the share of firms reporting a decrease exceeds the share reporting an increase, the index will be below zero, suggesting the indicator has decreased over the prior month. An index will be zero when the number of firms reporting an increase is equal to the number of firms reporting a decrease.

Data have been seasonally adjusted as necessary.

Historical data are available from January 2007 to the most current release month.

| Business Indicators Relating to Facilities and Products in Texas Current (versus previous month) | ||||||||

| Indicator | Apr Index | Mar Index | Change | Series Average | Trend* | % Reporting Increase | % Reporting No Change | % Reporting Decrease |

Revenue | 4.3 | 1.3 | +3.0 | 10.0 | 4(+) | 26.1 | 52.1 | 21.8 |

Employment | –1.0 | 2.5 | –3.5 | 5.7 | 1(–) | 11.8 | 75.4 | 12.8 |

Part–Time Employment | 0.7 | 0.5 | +0.2 | 1.2 | 2(+) | 6.3 | 88.1 | 5.6 |

Hours Worked | –1.3 | –0.1 | –1.2 | 2.4 | 3(–) | 6.6 | 85.5 | 7.9 |

Wages and Benefits | 7.7 | 12.9 | –5.2 | 15.4 | 71(+) | 13.3 | 81.1 | 5.6 |

Input Prices | 31.2 | 24.4 | +6.8 | 27.7 | 72(+) | 34.9 | 61.4 | 3.7 |

Selling Prices | 8.3 | 4.9 | +3.4 | 7.4 | 69(+) | 16.1 | 76.1 | 7.8 |

Capital Expenditures | 6.2 | 6.4 | –0.2 | 9.7 | 69(+) | 12.4 | 81.4 | 6.2 |

| General Business Conditions Current (versus previous month) | ||||||||

| Indicator | Apr Index | Mar Index | Change | Series Average | Trend** | % Reporting Improved | % Reporting No Change | % Reporting Worsened |

Company Outlook | –5.0 | –9.9 | +4.9 | 3.8 | 3(–) | 13.7 | 67.6 | 18.7 |

General Business Activity | –9.9 | –13.3 | +3.4 | 1.8 | 3(–) | 11.1 | 67.9 | 21.0 |

| Indicator | Apr Index | Mar Index | Change | Series Average | Trend* | % Reporting Increase | % Reporting No Change | % Reporting Decrease |

Outlook Uncertainty | 24.8 | 27.0 | –2.2 | 14.1 | 59(+) | 35.5 | 53.7 | 10.7 |

| Business Indicators Relating to Facilities and Products in Texas Future (six months ahead) | ||||||||

| Indicator | Apr Index | Mar Index | Change | Series Average | Trend* | % Reporting Increase | % Reporting No Change | % Reporting Decrease |

Revenue | 31.5 | 32.8 | –1.3 | 37.2 | 72(+) | 49.8 | 32.0 | 18.3 |

Employment | 18.0 | 21.1 | –3.1 | 22.9 | 72(+) | 30.9 | 56.2 | 12.9 |

Part–Time Employment | 5.1 | 9.7 | –4.6 | 6.4 | 10(+) | 12.7 | 79.7 | 7.6 |

Hours Worked | 2.5 | 7.2 | –4.7 | 5.9 | 10(+) | 8.9 | 84.7 | 6.4 |

Wages and Benefits | 35.2 | 37.3 | –2.1 | 37.5 | 72(+) | 38.9 | 57.4 | 3.7 |

Input Prices | 46.9 | 45.1 | +1.8 | 44.2 | 232(+) | 52.1 | 42.6 | 5.2 |

Selling Prices | 29.8 | 22.4 | +7.4 | 24.5 | 72(+) | 36.6 | 56.6 | 6.8 |

Capital Expenditures | 16.5 | 15.1 | +1.4 | 22.4 | 71(+) | 24.7 | 67.1 | 8.2 |

| General Business Conditions Future (six months ahead) | ||||||||

| Indicator | Apr Index | Mar Index | Change | Series Average | Trend** | % Reporting Improved | % Reporting No Change | % Reporting Worsened |

Company Outlook | 6.8 | 9.2 | –2.4 | 15.3 | 12(+) | 25.4 | 56.0 | 18.6 |

General Business Activity | 4.7 | 2.3 | +2.4 | 11.8 | 11(+) | 23.2 | 58.3 | 18.5 |

*Shown is the number of consecutive months of expansion or contraction in the underlying indicator. Expansion is indicated by a positive index reading and denoted by a (+) in the table. Contraction is indicated by a negative index reading and denoted by a (–) in the table.

**Shown is the number of consecutive months of improvement or worsening in the underlying indicator. Improvement is indicated by a positive index reading and denoted by a (+) in the table. Worsening is indicated by a negative index reading and denoted by a (–) in the table.

Data have been seasonally adjusted as necessary.

Comments from survey respondents

Survey participants are given the opportunity to submit comments on current issues that may be affecting their businesses. Some comments have been edited for grammar and clarity.

- The consumer shock from higher gas prices and rising airfares is negatively impacting both meetings and individual booking volumes for future months.

- The current news cycle is not good for travel sales. Current world conditions are not good for travel sales. People must feel comfortable about their world before committing to leaving home and spending sizable amounts for luxury travel.

- The longer the conflict with Iran continues, the less business will be done—even here in Texas.

- While we have experienced an uptick in demand for talent-searching—particularly for white-collar, professional positions in shared-services functions—finding experienced candidates remains the central challenge. Educated professionals are reluctant to change jobs in this environment, and without candidates to fill open roles, staffing firms cannot generate revenue, prolonging financial stress and uncertainty. Compounding this, for the first time in 15 years, two clients have failed to pay within a reasonable timeframe—one due to insolvency proceedings, the other a nonprofit facing significant delays in grant funding. Increased demand for our services paired with uncollectable receivables creates an unsustainable operating environment. We remain committed to navigating these conditions and are cautiously optimistic that improved employer confidence and a loosening of candidate risk aversion will signal the turn we are watching for. Let's hope the light appears at the end of this tunnel soon.

- The labor market continues to be uneven, there is some employer relief in terms of asking-pay rates of candidates. Supply costs and vendor costs are expected to increase between 20 and 30 percent over the coming 3 to 6 months. In the healthcare industry, demand has slowed with a low respiratory infection season (i.e., flu season), and patients are being much more economically sensitive to seeking care. This has led to much sicker patients due to delayed urgent care matters. Additionally, the current administration's stances on global health policies such as vaccinations have caused some overall wariness of the healthcare industry as a whole, which has also led to lower patient volumes seeking care.

- Concerns about Iran and the economic environment have caused uncertainty in the market.

- There is economic uncertainty with all of the geopolitical factors whipsawing consumer and business sentiment. AI is beginning to filter into the equation, and the loan volume of OFIs [Other Financial Intermediaries]/private lending has created concerns about debt service.

- The Iran war should be coming to an end, and hopefully we will see oil prices move lower.

- The poor man is getting poorer. The environment is not good.

- The administration sends mixed messages that make me rethink future building modeling, big equipment purchases and increasing salaries. I worry about customer pushback on price increases that will affect meeting our budget goals.

- Our business continues to enjoy the benefits of pricing power and increases in revenue, but we are beginning to see moderation and even slowing in same-store, same-period traffic numbers over 2025. This is a new phenomenon for our business and is the first we've seen in the company's 16-year history. Specialty coffee is a bit of an affordable luxury, so this indicates to our thinking that the upper-middle-class American consumer may actually be running out of steam. We also have become increasingly concerned about the looming possibility of a depression-level economic event in 2029-2030 that could last for a decade. This is premised upon the forecasts of a consulting firm and the irrefutable stressors of ballooning national debt, continuing outsized annual deficits, the aging, and now dying, baby boomer demographic, declines in work force, increases in entitlement spending, etc., all of which are what they are. We are left with no supportable scenario or theory for avoidance of an economic collapse absent "things will just work out." So, we are going to suspend new cafe contracts and complete only the five additional cafes that are in our development timeline through the first quarter of 2027. We are in a wait-and-see and debt-reduction mode for the time being. It is important to note that this is a newly established stance. Current economic and demographic metrics are simply, inarguably unsustainable. Maybe a new Federal Reserve Chair will bolster resistance to politically accommodative policy. I sure hope so. It still may be too little, too late, if my concerns are valid.

- The war in Iran’s impact on fuel prices and a general decrease in customer discretionary income [are an issue impacting our business].

- There has been a minor increase in uncertainty due to Middle East unrest, increasing fuel costs to the transportation sector and increased food and beverage costs to our restaurant policyholders, which are squeezing profit margins significantly.

- Public companies’ stock prices are falling from the threat of AI, which has changed the value of privately held companies.

- The U.S.-Iran conflict has created an increase in product and transportation costs as well as issues with supply. These items increase the uncertainty for businesses, which could have an impact on the level of business activity.

- Regarding the general business conditions, business has been strong this year. We have added several accounts in Costa Rica, Guatemala and El Salvador. My assumptions are based on a prolonged conflict with Iran that keeps pressure on the Strait of Hormuz and upward pressure on oil (above $90 per barrel). Starting April 12, we are getting hit with fuel surcharges across all forms of transportation (trucking, ocean, cold storage) because of higher diesel prices. If oil drops in the next 60 days, we should see a lot of these surcharges fall off, so the impact to pricing is relatively short-lived and will not result in higher energy costs being baked into commodities prices.

- The current decrease in sales revenue is caused by low new and used inventory. Selling price decreases are being caused by discounts on new vehicles in an effort to increase turnover and earn additional allocations.

- General business activity at the retail level has been affected by the uncertainty of the war, but more importantly the dramatic increase in gas prices at the pump. One big difference versus previous gasoline price spikes is that consumers aren’t trading large vehicles for more fuel-efficient vehicles. In previous fuel price hikes, there was an irrational move to fuel-efficient vehicles. This tells me consumers are being more rational in navigating the economy.

- Section 232 tariffs are going to put some dealers out of business.

- Customer traffic has slowed significantly in April.

- We sell propane, gasoline and diesel. We are experiencing price volatility, but I feel like it will be short term. I am feeling more uncertain about the period between now and the end of the year, but I anticipate the business environment will become more normal after that.

- The City of Dallas, which is an important partner, is under extreme budget stress as a result of both revenue and expense constraints that were imposed on it. This is unsustainable and will impact any organization that does work with the city or relies on city services.

- The continued increase in fuel costs has impacted our consumers as well as the uncertainty.

- My concern is the rise in oil prices and its impact on consumers. I am worried about a slowdown in the economy and discretionary spending declines due to higher energy prices.

- Midstream revenue is tied to producer activity. With the Iran war and de-stocking of global inventory, oil prices are strong, and producer activity is steady but dependent on the forward curve.

- Small businesses like us will benefit more from AI than large companies. We are using AI to solve problems faster at a cheaper cost, keeping customers happy and generating more sales with current staff or few hirings. Our revenue and profit will both increase in 2026 and 2027 without much new hiring cost due to AI productivity gains.

- High fuel prices are affecting the cost of operating our vehicle fleet. We cannot increase prices on ongoing negotiated contracts. We are concerned about continued fuel price increases and the resulting inflationary impacts to the cost of delivering our services.

- There is some uncertainty as to how potential inflation will impact margins on GSA [General Services Administration] Schedule and IDIQ [Indefinite Delivery, Indefinite Quantity] contracts which have established rates.

- Global conflicts and material supply costs are making projections difficult and creating a need to defer or delay projects due to higher costs for construction.

- Potential clients, primarily foreign investors, are increasingly redirecting their investments to other countries, most notably Canada, due to ongoing policy changes and heightened uncertainty. As a result, we have experienced a decline in our client base, with approximately 12 percent of clients lost under the current conditions.

- Uncertainty has continued due to the ongoing war with Iran and no clear way out for the U.S.

- The chaos resulting from rapid policy and funding reversals by the administration continues to have undesirable impacts on government business opportunities. This has also resulted in a softening commercial marketplace. The Iran war has added even more uncertainty and threatens to undermine the many applied-research and development markets that are served by our organization. My feedback is based on assumptions that include a quick and noncatastrophic end to the Iran war and the belief that Congress will take unified action regarding the most recent PBR (President’s budget request).

- Uncertainty is now the status quo.

- Uncertainty in policy decisions affects our ability to plan effectively. Professional services pursuits have declined due to scarcity in public funding of infrastructure projects.

- The conflict in the Middle East has increased the uncertainty for us all.

- Over 80 percent of new hires do not have a background in our industry, so we will have to train in-house. That is a change from five years ago, when more than half could be found from a related industry. Finding qualified field staff remains a challenge.

- We focus on energy, so higher oil prices are probably good for us. Utility clients are our largest area of business. But we also serve other energy people, like pipelines. We try to focus on the parts that are immune to changes in oil price.

- The residential real estate market remains sluggish, but the commercial real estate market is showing signs of life. Hopefully, we will get out of the Iran war, and things will pick up in the second half of the year.

- Uncertainty is the name of the game. The only certain thing is that the defense contractors will do well. The companies making parts and pieces for missiles and bombs should prosper.

- I think that a lot of people in the business community believe that there will be a resolution to the situation in the Middle East, and when that happens, the economy will explode.

- The U.S. Economy is showing signs of strength. After the Iran war ends, our assessment from [the perspective of] a small business with global customers in over five countries is that the U.S. and global economies will grow very substantially with lower oil prices, and the AI productivity boom will kick in.

- We are seeing cost increases in construction materials and delivery charges.

- We are seeing the same number of inquiries but at much lower investment amounts. We lost an employee in April that I managed out, partly because of culture fit, but also because I didn't want to eat into our company's reserves, given the revenue isn't coming in at the pace and levels we had last year. Mileage reimbursement for our work in the valley has tripled, and we are starting to see other program costs, related to training and education, rise.

- I put on here that our outlook is better this month than last, but just slightly. I'm only a little bit more optimistic than I have been.

- In addition to tariffs and inflation, geopolitical uncertainty is now impacting our ability to expand and invest, as well as creating general uncertainty and hesitancy among customers, leading to longer sales cycles. However, given we are in a fixed-cost-intensive industry, it is difficult for us to adjust down expenses to match general business activity.

- Uncertainty in the Gulf remains a major concern, even in Houston, Texas.

- There is potential for petroleum prices to ripple through to the cost of construction commodities.

- It is very tough to see where the economy is going. I think it is worse than reported or than we feel. I feel like the whole thing could collapse at any time. We need to get fuel prices down quickly.

- We're doing okay, but things are getting tougher every day.

- Continued tariff chaos impacts our manufacturing members negatively and increases their input costs. The recent Iran war is spiking oil prices, which impacts refined chemicals and the cost of plastic resin, which are input costs for many manufacturing companies.

- We had to increase our trip charges on all our jobs to account for high fuel prices.

- Obviously, the war adds a significant unknown to everyone’s business. It’s just one more reason to hold onto your cash and not take on new debt, which is very bad for capital goods dealerships like ours.

- The prospect for lower interest rates has decreased due to the uncertainty and the high cost of goods due to the higher cost of energy from the war in Iran and the higher federal deficits caused by the increased spending on the war. As a company engaged in commercial real estate, the higher uncertainty caused by the war coming on the heels of the uncertainty from tariffs, leading to delayed decisions by companies looking to lease or expand their commercial real estate space. Higher transportation costs are also feeding into increased costs for materials needed for new commercial real estate development.

- Discretionary spending is way down in the middle class. I’m seeing roughly a 10 percent drop year over year in some recreational businesses even after discounts and special offers. I expect there will be ongoing contraction this year due to the war and general fear.

- We are not seeing bidding opportunities and facilities spending is down.

- Global instability and uncertainty will affect business and investment decisions. Tariffs remain part of these decisions.

- Due to the war, people are more concerned about their finances, which is inhibiting spending a little.

- The longer the war persists, the more uncertainty we continue to face on multiple fronts. We do expect resolution at some point, at which time we expect shipments and revenues to decrease from the record high levels we're at currently.

Special questions

For this month’s survey, Texas business executives were asked supplemental questions on the Iran war. Results below include responses from participants from both the Texas Manufacturing Outlook Survey and Texas Service Sector Outlook Survey. View individual survey results.

Historical Data

Historical data can be downloaded dating back to January 2007.

Indexes

Download indexes for all indicators. For the definitions of all variables, see data definitions.

| Unadjusted |

| Seasonally adjusted |

All Data

Download indexes and components of the indexes (percentage of respondents reporting increase, decrease, or no change). For the definitions of all variables, see data definitions.

| Unadjusted |

| Seasonally adjusted |

Questions regarding the Texas Service Sector Outlook Survey can be addressed to Isabel Brizuela.

Sign up for our email alert to be automatically notified as soon as the latest Texas Service Sector Outlook Survey is released on the web.