Groundwater markets slowly evolve in ever-thirstier Texas

The year after one of the worst droughts in Texas history, the 2012 State Water Plan was developed, combining plans from 16 regions across the state. It called for conservation, reuse, redistribution, new reservoirs and the development of water markets that could significantly increase water-usage efficiency.

Although those drought conditions eased, water scarcity remains. The state’s projected growth over the next 50 years highlights the need for officials to ensure water availability. Development of water markets remains a key dimension of water planning.

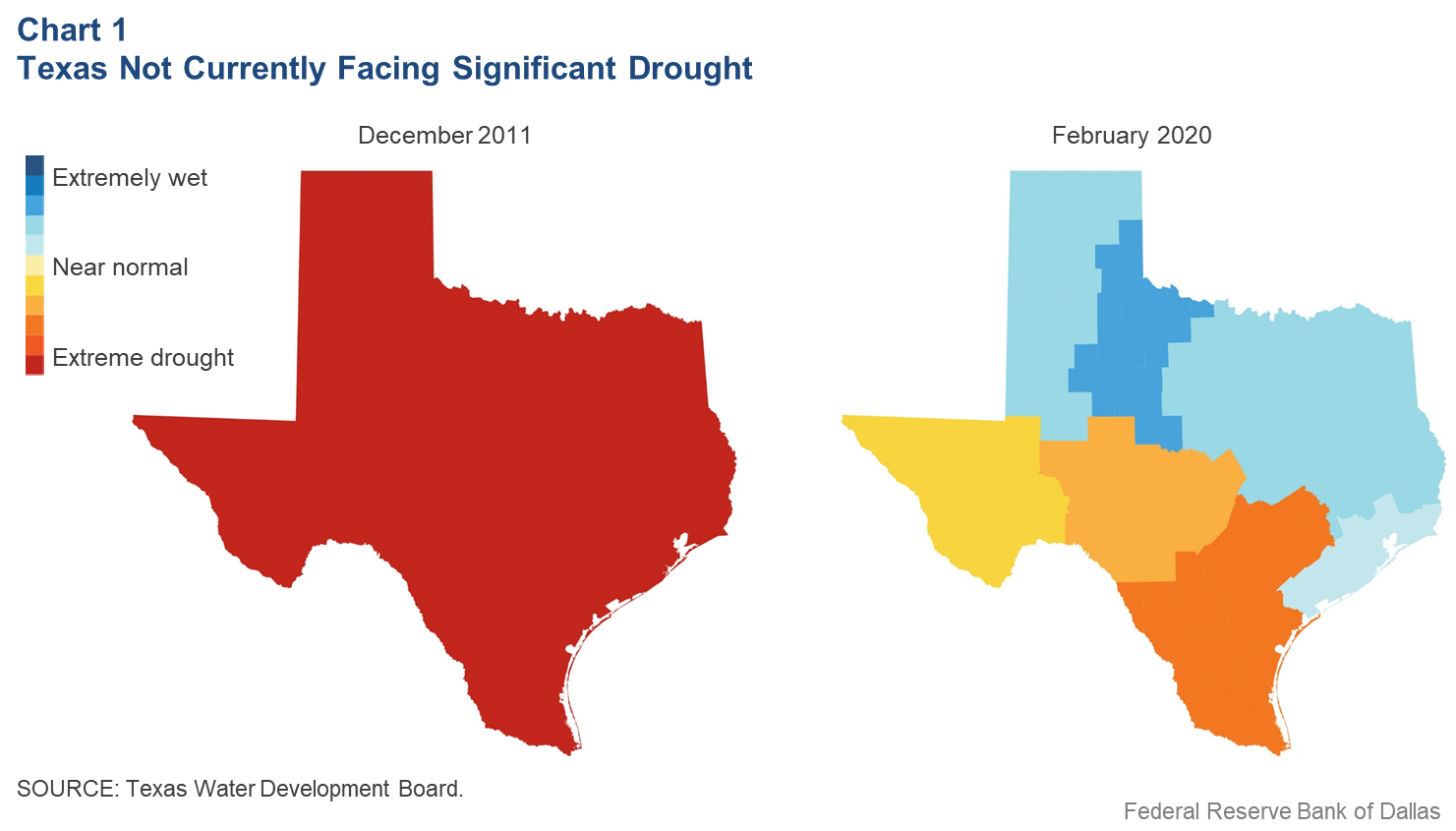

Drought Conditions in Texas

Texas has a long history of regular and severe droughts. The Edwards Plateau and South Central climate divisions were two of 10 in Texas experiencing moderate drought as of February 2020, based on the long-running Palmer Drought Index (Chart 1). This contrasts greatly with 2011, when water rationing and limits were ordered in many communities as Texas suffered the worst year of drought since records began in 1895.

A notable example of drought-induced rationing occurred along the Coastal Bend, where water availability for agriculture was significantly reduced in 2012 and 2013.[1] Because of the drought’s severity, the Lower Colorado River Authority decreased most of the flow to rice farmers to limit water curtailment in Austin.

This action lowered the authority’s allotted share of water for agriculture to 21 percent in 2012 from 60 percent in 2011. The reduction lasted four years, resulting in significant financial losses to farmers and the community businesses that served them.[2]

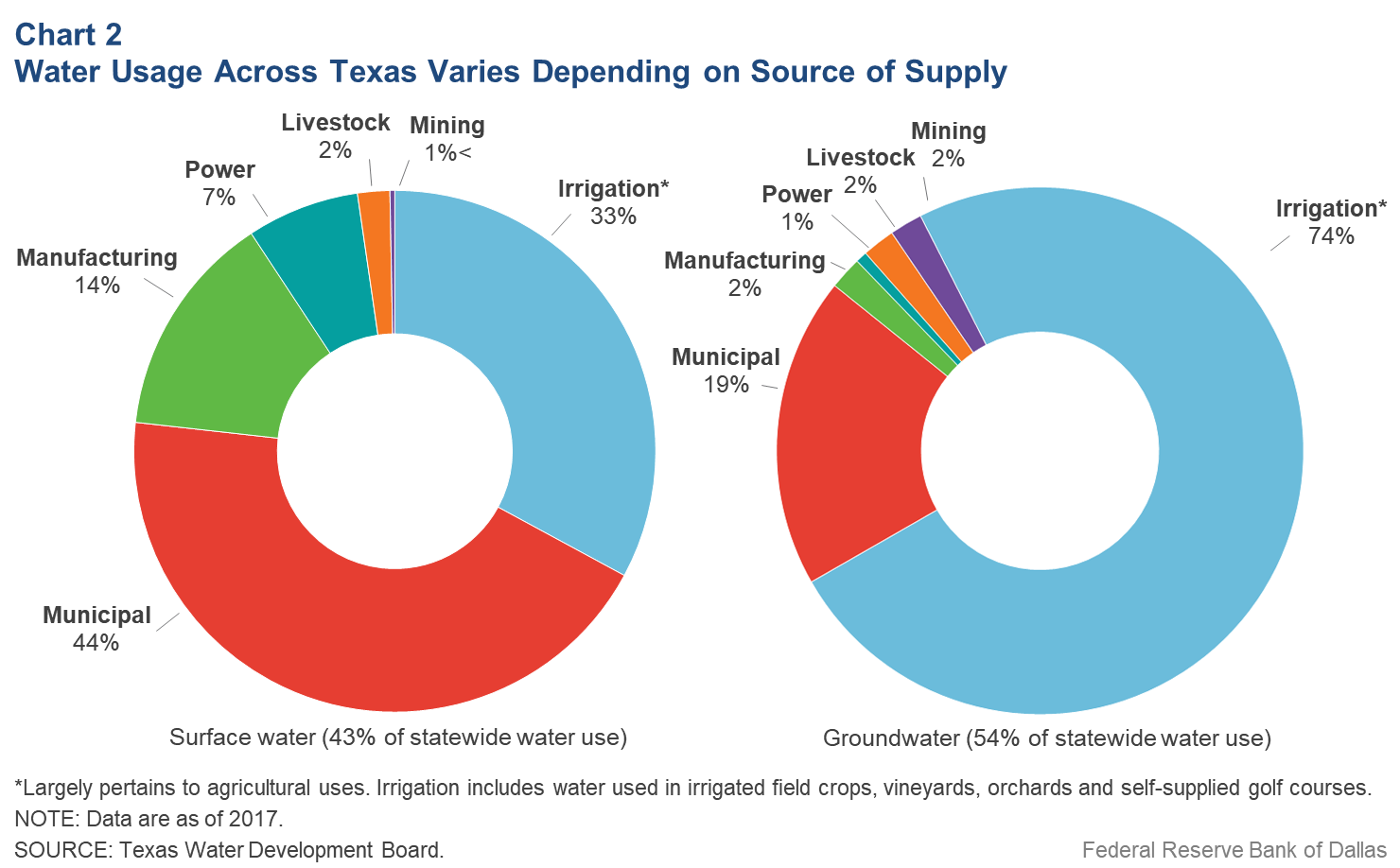

Water Use Based on Source

Texas water comes from groundwater (aquifers) and surface water (rivers, lakes and reservoirs), with water usage differing greatly depending on its source (Chart 2).

The Ogallala and Gulf Coast aquifers are among the largest in Texas and this year will provide more than 50 percent of the 12.3 million acre-feet of available groundwater in Texas. (An acre-foot is the amount of water needed to cover an acre of land to a depth of one foot.)

The Ogallala Aquifer is one of the world’s largest, covering eight U.S. states. It serves approximately 95 percent of the agricultural needs of a region that includes West Texas and most of the Panhandle.

The portion of the Ogallala under Texas has a slow water recharge rate, and excessive pumping is leading to depletion. Water levels in some areas have fallen several feet annually in recent years as the annual average recharge rate has held at a mere half-inch.

State water authorities estimate that groundwater availability will drop 20 percent from 2020 to 2070, largely due to declines in the Ogallala and Gulf Coast aquifers.[3] Water levels in the other seven major aquifers in Texas vary from stable to declining.

Rising population levels will primarily drive future water scarcity. Indeed, more people will require more water in municipalities for sanitation, industrial use, landscaping and individual consumption. Texas’ population is expected to grow more than 70 percent, from 29.5 million in 2020 to 51 million in 2070. The Texas Water Development Board forecasts that water demand will rise 17 percent.[4]

One reason water use likely won’t increase more is that nonresidential irrigation (primarily agricultural), which accounts for the largest share of state water usage, is anticipated to decline 18 percent by 2070.[5] The transfer of water rights from agriculture to municipalities, where the population growth will occur, is responsible for part of the sector’s decline.

Surface, Groundwater Allocation

Water laws in the U.S. fall into two general categories: prior appropriation and riparian rule. Many western states, such as California and Colorado, follow the law of prior appropriation, which holds that water rights are obtained through fulfillment of specific statutory requirements. Other states follow riparian rule, which means that the rights to a body of water are determined by property ownership.

In Texas, surface water rights are subject to both prior appropriation and riparian rule, and the state is largely responsible for issuing water permits. Close to 70 percent of surface water rights are owned by 23 river authorities that typically manage reservoirs and regulate the flow of water to rivers.

When river authorities sell water to farmers or cities, the price is dictated by policies and is usually based on purification and transportation costs. In times of scarcity, the authorities often restrict supply to certain groups—just as the Lower Colorado River Authority did in 2012—rather than rely on market pricing and allocation.

Groundwater rights are based on riparian rule and historically governed by the rule of capture, allowing landowners to pump as much water as they choose even when the water source extends to adjacent properties. Because water becomes private property only after it is drawn, there is a strong incentive to pump as much water as desired.

Overpumping groundwater can cause land subsidence and saltwater intrusion. Yet the rule-of-capture doctrine creates an incentive to pump water faster as it becomes scarcer. This results in overconsumption and resource depletion.

Water Market Efficiency

A water market, which is essentially a voluntary sale or lease of legal rights to water from one entity to another, is a useful way to allocate water. In general, markets are efficient because the price moves with changes in supply and demand so that shortages or excesses are avoided.

In a drought, for example, the price of water is driven higher, which encourages conservation and the movement of water from lower-value uses to higher-value ones. Faced with a high price, suburban homeowners may reduce lawn watering and farmers may plant fewer water-intensive crops and convert from flood irrigation to more efficient watering systems. Without markets and market prices, there may be little incentive to conserve even as scarcity increases. In some cases, the incentives can be the opposite—use as much as you can before it’s gone.

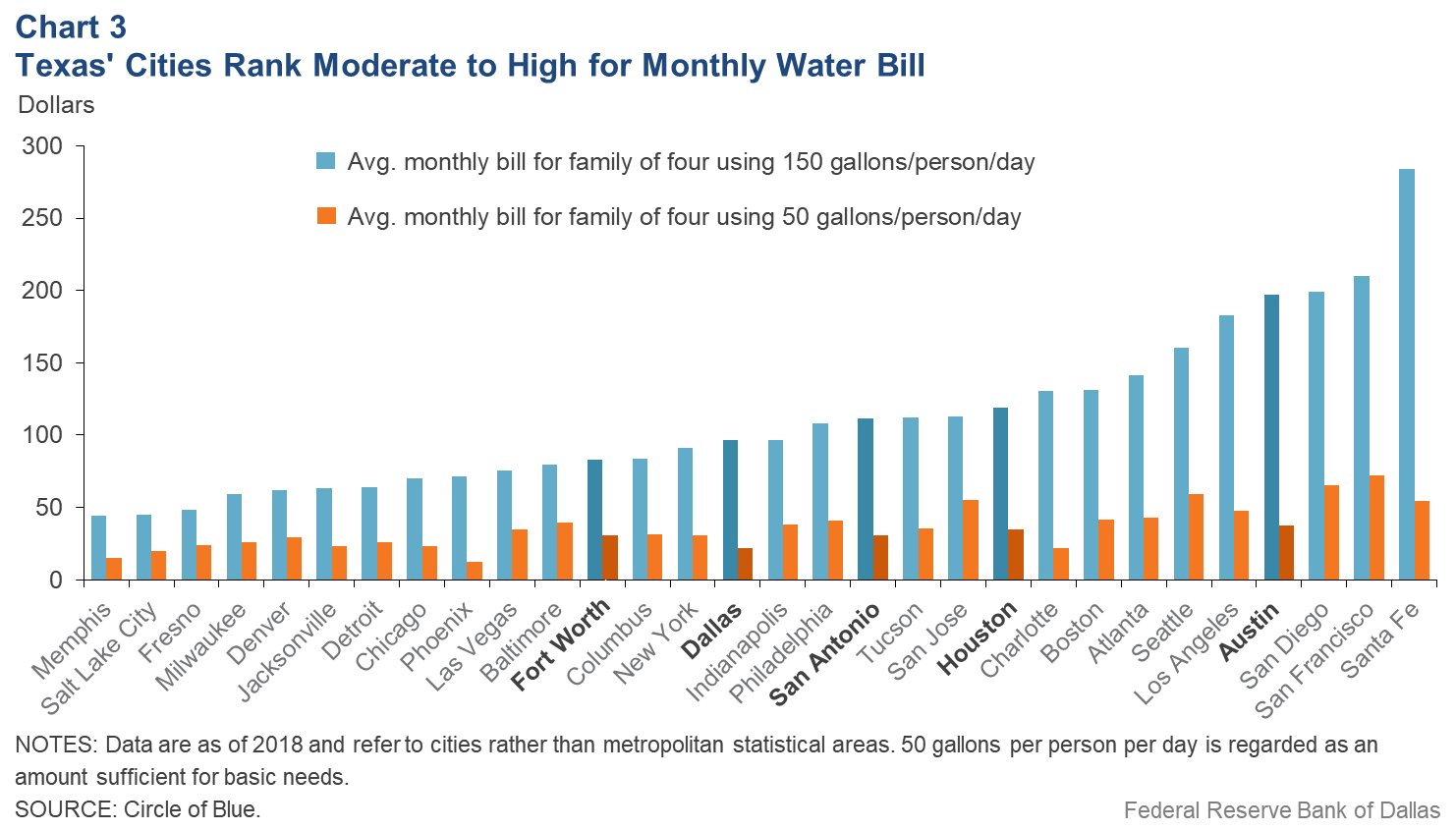

Among the nation’s 30 major cities, those in Texas rank moderate to high in terms of the average monthly water bill for a family of four using 150 gallons per person per day (Chart 3).

Many water agencies are concerned about the impact of high water prices on low-income families and, thus, offer prices at consumption levels generally sufficient for basic needs. There is less variation across cities in the cost of the lower consumption level. Tiered pricing is often used to discourage high water consumption, which typically results from landscape watering.

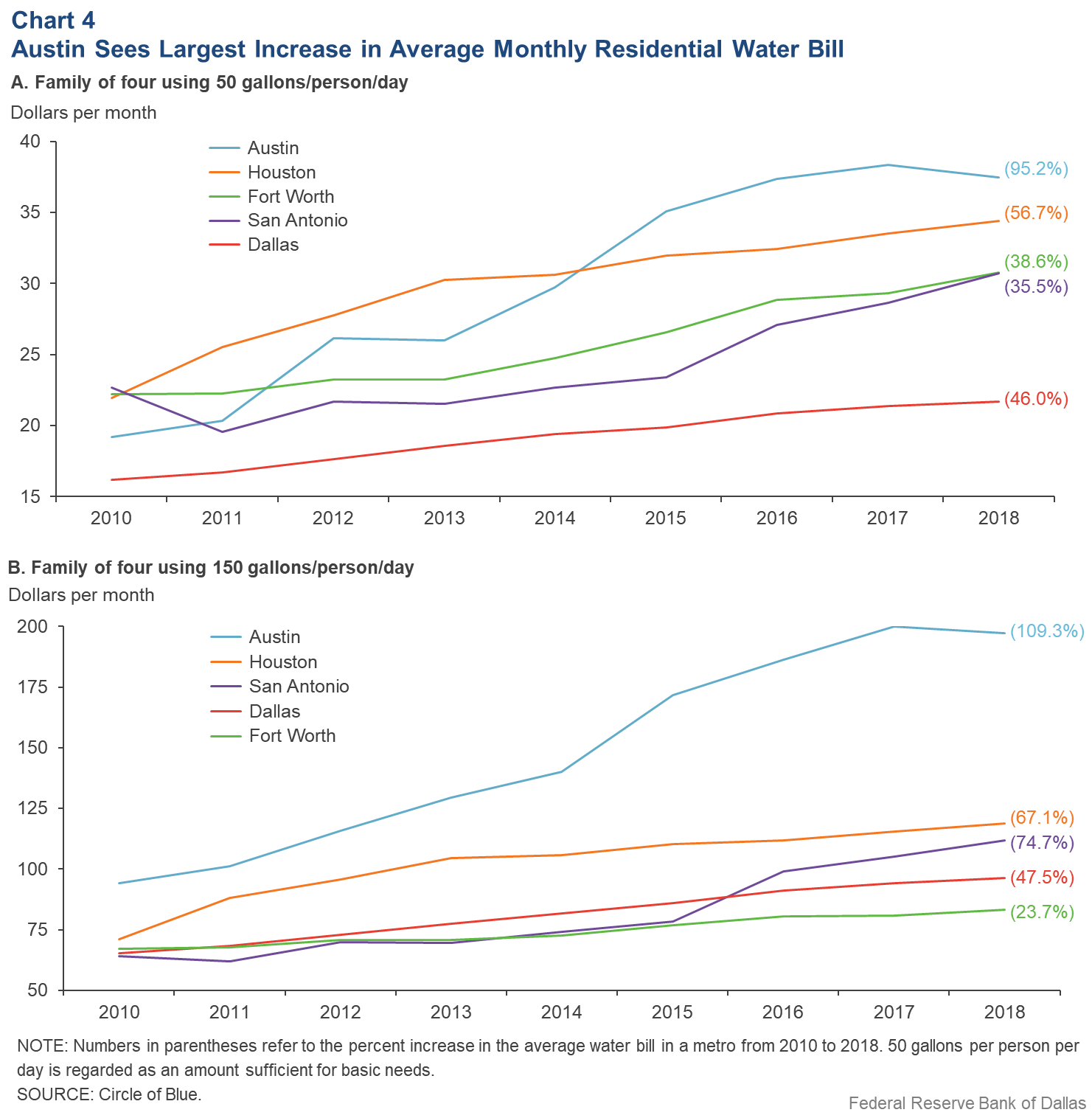

Municipal water rates in Texas increased sharply in the eight years ended in 2018, rising faster than the Texas consumer price index (Chart 4). The water price increase, particularly for high consumption levels, is likely the result of water agencies paying more for water and seeking to curtail consumption and generate revenue for alternative sources.

Dallas is one of the many cities that rely on surface water. With the area’s population increasing, the number of lakes from which it draws water rose from three in 1970 to six today. The city is building infrastructure to buy water from Lake Palestine, 90 miles to the southeast.

By comparison, San Antonio relies solely on groundwater from the Edwards Aquifer. The Edwards Aquifer Authority has spent money on recharge dams to enhance supply and has developed markets to encourage the sale and lease of water rights.

Meanwhile, the San Antonio Water System has sought alternative supplies. In 2017, it purchased water rights of up to 50,000 acre-feet from a separate aquifer 142 miles away. A pipeline to the source is scheduled to be completed this year, at a total project cost of nearly $3.4 billion.

State Groundwater Markets

The rule of capture applies to the more than 50 percent of Texas water coming from groundwater and limits the ability of water markets to allot it.[6] Senate Bill 1, enacted in 1997, gave groundwater conservation districts the ability to create markets for groundwater by establishing private property rights to the water. The law provided the conservation districts with the power to issue pumping permits and manage withdrawals. Once individuals and business entities had ownership of a specified amount of water, markets could form.

Still, few water markets exist in the state. The major exception is the Edwards Aquifer Authority, which got its authority before the Texas law took effect as a result of an Endangered Species Act claim brought by the Sierra Club in 1993.[7]

The court ruled in the case that excessive pumping from the aquifer threatened several endangered species and that the state was obligated to create a pumping cap, setting the stage for creation of the Edwards Aquifer Authority and its ability to allocate pumping rights and create markets.

To cap pumping at 572,000 acre-feet per year, the authority established permits based on past usage. It allowed new users to receive a permit after all historical permits had been issued—if any water remained under the cap. Permits were subject to temporary reduction if the aquifer dropped below predetermined levels that might threaten stream flows.

The cap is now fully subscribed, and no new permits are likely to be issued. In order for users such as the San Antonio Water System to increase their draw amount, they must buy or lease water from the existing permit owners.

Market Developments

Permit values have increased consistently since the authority was established. Sales and transfers that were initially free or of little value as of 2016 are now valued at between $5,000 and $10,000 per acre-foot. The Edwards Aquifer Authority does not manage or track sales, although it facilitates sales through a website that connects sellers and buyers.

Website transactions are usually short-term leases for small amounts of water and generally take place during droughts when water is restricted. Large water purchases occur outside the authority’s marketplace. Buyers approach potential sellers with offers that are then transacted via a warranty deed that provides a clear claim to the water.

A recent innovation has been an option program involving voluntary irrigation suspension. Participating irrigators annually receive a guaranteed payment of $54 per acre-foot of water made available for the program. If the aquifer falls below 635 feet at a designated measurement location on Oct. 1, delivery of the enrolled water is suspended the following year. Participants also receive $160 per acre-foot for the year of suspension. Prices can be adjusted year to year to reach an enrollment goal of 40,000 acre-feet.

Implementation Limitations

While these developments are encouraging, the Edwards Aquifer marketplace faces constraints. Water can’t be transported outside of the aquifer, and irrigators can only sell or lease up to half of their permitted volume. Domestic and livestock wells that pump up to 25,000 gallons a day need not be permitted and, thus, their usage can reduce permitted irrigators’ available supply.

Furthermore, legal tension exists between the rule of capture, which remains in place, and the legislative authority given to the Edwards Aquifer Authority and groundwater conservation districts. The Texas Supreme Court in 2015 declined appeals by the authority of a case brought by Glenn and JoLynn Bragg, who had invested $2 million to grow pecans on 100 acres of land over the Edwards Aquifer in Hondo, Texas.[8]

The Braggs applied for 625 acre-feet per year but received a permit for only 120 acre-feet and sued for damages, claiming ownership of the water under the rule of capture. A jury awarded the Bragg family $4 million in compensation and interest based on the estimated value of the land with full water rights and the value with the water rights as permitted by the Edwards Aquifer Authority.

The potential for a growing number of such lawsuits challenges the financial viability of the Edwards Aquifer Authority and groundwater authorities in general.

Developing Water Markets

Water markets are evolving in Texas. Well-defined property rights governing surface water have served as the basis for marketplaces for a long time. A handful of large river authorities can hamper the formation of markets, but in places such as El Paso, Dallas and the Rio Grande Valley, cities are buying surface water primarily from irrigators.

The Legislature has encouraged water markets, setting a framework for them. Bulletin board markets, derivative markets, and environmental leasing and purchasing programs have been active since the 1990s. The Texas Water Bank, a bulletin board market, serves as a platform for buyers and sellers to post requests and offers.[9]

There are also market-based mechanisms seeking to secure water for environmental and wildlife purposes. The Texas Water Trust purchases or leases water from irrigators for purposes such as increasing instream flows in lakes for fish and other wildlife.

Developing groundwater markets remains a challenge. The rule of capture continues to threaten the legal rights of groundwater authorities to cap withdrawals and issue permits. Complicating the process are groundwater control districts, which generally follow county lines, sometimes leading to multiple districts with oversight of the same aquifer.[10]

Markets can’t properly function unless all such groundwater control districts work together to coordinate a permitting process and establish a cap that ensures the viability of the water supply. While the 2012 State Water Plan established groundwater management areas that encompass the boundaries of entire aquifers or subdivisions, each district has the legal authority to permit as it sees fit. This has limited the use of the cap-and-trade system outside the Edwards Aquifer.

As Texas’ population grows, markets will need to develop. In the future, water is likely to move from agriculture to burgeoning cities. Agriculture accounts for 54 percent of all water consumption in the state but produces less than 2 percent of state gross domestic product.

Texas households have experienced sharply higher water prices over the past 10 years. While the increase has been necessary to discourage consumption and develop alternative sources of supply, the further development of water markets would likely allow for smaller price increases as water freely moves from lower- to higher-value uses.

Notes

- See “Water Scarcity a Potential Drain on the Texas Economy,” by Keith Phillips, Edward Rodrigue and Mine Yücel, Federal Reserve Bank of Dallas Southwest Economy, Fourth Quarter, 2013.

- See “During Drought, Once-Mighty Texas Rice Belt Fades Away,” by Dylan Baddour, StateImpact, a reporting project of National Public Radio member stations, Aug. 12, 2014.

- See the 2017 State Water Plan, Texas Water Development Board.

- See note 3.

- Nonresidential irrigation includes field crops, vineyards, orchards and golf courses.

- Much of the information is summarized from “Texas Groundwater Markets and the Edwards Aquifer,” by Amy Hardberger, The Rockefeller Foundation, 2016.

- See note 6.

- Edwards Aquifer Authority v. Bragg, Court of Appeals of Texas, Nov. 13, 2013.

- See “A Place for Water Markets: Performance and Challenges,” by Ereney Hadjigeorgalis, Review of Agricultural Economics, vol. 31, no. 1, 2009.

- See note 6.

About the Author

The views expressed are those of the authors and should not be attributed to the Federal Reserve Bank of Dallas or the Federal Reserve System.

Southwest Economy is published quarterly by the Federal Reserve Bank of Dallas. The views expressed are those of the authors and should not be attributed to the Federal Reserve Bank of Dallas or the Federal Reserve System.

Articles may be reprinted on the condition that the source is credited to the Federal Reserve Bank of Dallas.

Full publication is available online: www.dallasfed.org/research/swe/2020/swe2001