COVID-19’s fiscal ills: busted Texas budgets, critical local choices

Texas tax revenue on a year-over-year basis plunged by an alarming 49 percent in April, the first month to fully reflect the economic impact of COVID-19. While tax collections have since partially recovered, the state comptroller forecasts a $4.6 billion shortfall for the 2020–21 budget cycle. Many localities, also dependent on the sales tax, project significant belt-tightening.

The budgetary woes pose potentially dire implications for individuals seeking government services and for firms whose survival depends not only on consumers’ current health, but also on who bears the tax burden.

Texas’ Tax Structure

The Texas budget had anticipated expenditures of about $125 billion, with about half of the money expected to come from state taxes and the rest from other sources such as license fees, lottery proceeds and federal transfers.

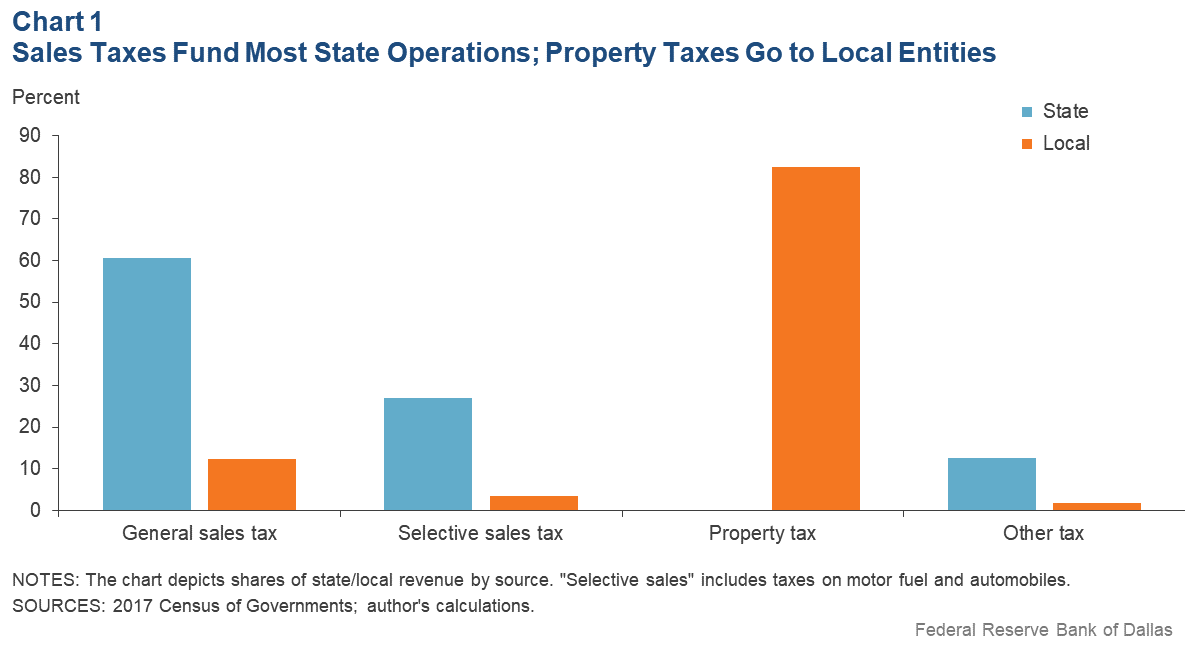

The state raises its revenue primarily by taxing consumption (Chart 1). Roughly three-fifths of tax dollars come from a single source: the general sales tax of 6.25 percent that is assessed on most retail transactions.[1] Another quarter comes from selective sales taxes on goods such as motor fuel and automobile purchases, and most of the remainder (one-eighth) from business taxes such as the franchise tax.

The sales tax is less important to local governments. Cities, counties and other taxing authorities raise more than 80 percent of their revenue from the property tax and most of the rest (12.3 percent) from the general sales tax.[2]

The remainder (5.2 percent) comes from a variety of sources, including hotel taxes and utility taxes, which are important for certain jurisdictions though they constitute only a small part of total revenue.

While there are differences in how state and local governments raise revenue in Texas, one area in common is the lack of an income tax. Such a tax provides about a quarter of state and local revenue in other states but is subject to greater revenue volatility in tough economic times, potentially leading to larger fiscal adjustments than would be expected in Texas.[3] Yet, no tax system can fully guard against recession.

Great Recession Lessons

When an economy enters recession, two things simultaneously happen. Demand for government services rises as people find themselves with less income because they are working fewer hours or no hours at all. At the same time, the revenue available to fund those services falls because those reduced personal earnings translate directly to a reduction in taxes paid.

Countries typically handle these kinds of shortfalls by running deficits during difficult times. However, this avenue is not available to U.S. states because (with the exception of Vermont) they are required to balance their budgets. Similarly, cities are generally required either by state law or their own charters to run balanced budgets on a yearly basis.[4]

Thus, lawmakers must make fiscal adjustments to close the gap between expected revenues and necessary expenditures, often with distinct consequences for those dependent on local government services and for the taxpayers who fund the services.

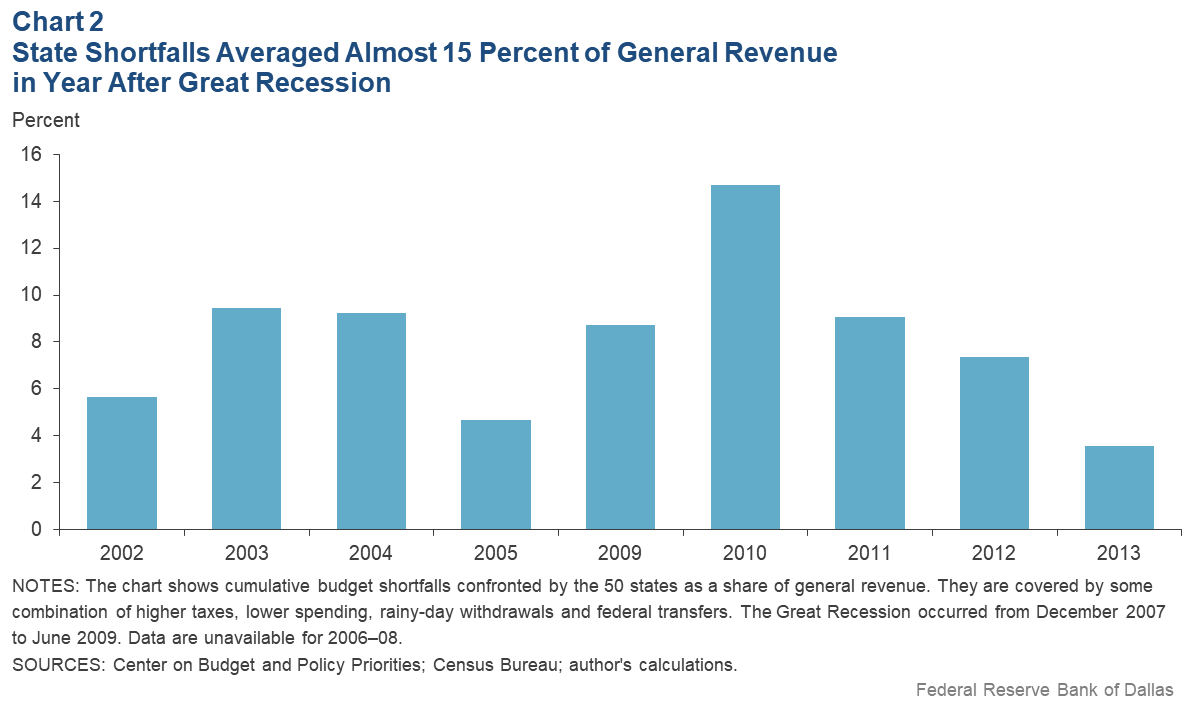

While it’s unclear what that adjustment will look like in the COVID-19 era, a look at the Great Recession reveals what can happen. State lawmakers across the U.S. were required to close an 8.5 percent budget shortfall in 2009 through a combination of spending cuts and tax increases (Chart 2).

Officials initially hoped they could reverse those cuts in the next fiscal year. Instead, they faced an additional 14.5 percent shortfall in 2010 and a 9 percent gap in 2011, leading to deep cuts in areas such as education.[5] Such reductions can hurt struggling families in the short run and likely reduce economic growth over the long run.[6]

How did U.S. tax revenue change as the Great Recession took hold? Between 2008 and 2009, state sales and gross receipts taxes on all products fell 3.9 percent, to $345 billion. State individual income tax revenue fell much more, down 11.9 percent to $245 billion, and corporate income tax revenue declined 22.6 percent to $38 billion.

By comparison, local property taxes rose 3.8 percent over the period, though home price declines would later take a fiscal toll on localities.

Overall, state income tax revenue fell about four times faster than sales tax revenue, prompting fiscal crises in states such as California and New York that rely heavily on income taxes. This is consistent with economic research documenting the relative volatility of such tax revenue and suggests income-tax-reliant states might have a tougher time dealing with the economic impact of COVID-19 despite federal income support programs to mitigate income declines.[7]

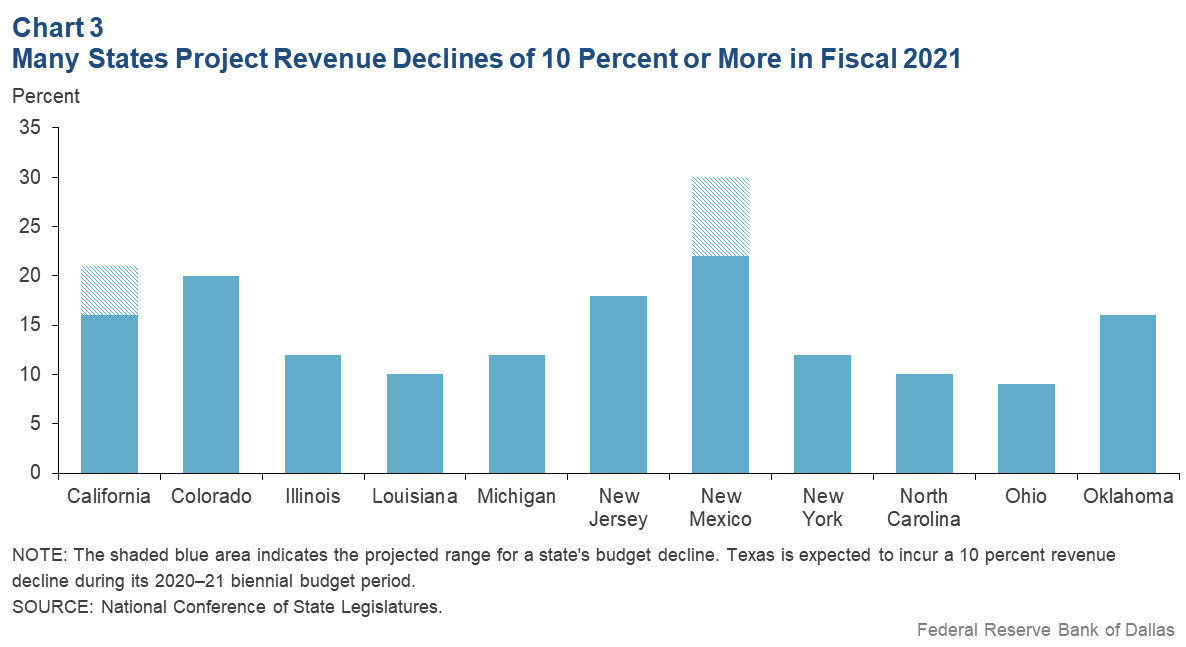

While all states are facing revenue shortfalls, those with a high dependence on income taxes are projecting truly prodigious revenue shortfalls (Chart 3).[8] California’s legislative analyst office projects a deficit of 16 to 21 percent in the new fiscal year, which began July 1. New Jersey’s treasury department says the state will run 18 percent below budgeted levels, while New York anticipates a 12 percent gap.

Separate estimates from the Center on Budget and Policy Priorities reinforce these general conclusions. The nonprofit research institute finds that, nationwide, real state budget shortfalls for fiscal 2020–21 will be about 10 percent larger than during the Great Recession years of 2009–10, a sobering prospect for many.[9]

Texas Tax Receipt Slump

Texas started its current fiscal year on an upbeat note. Halfway through fiscal 2020—at the end of February—tax revenue was 5.6 percent ahead over the same period in the year prior.

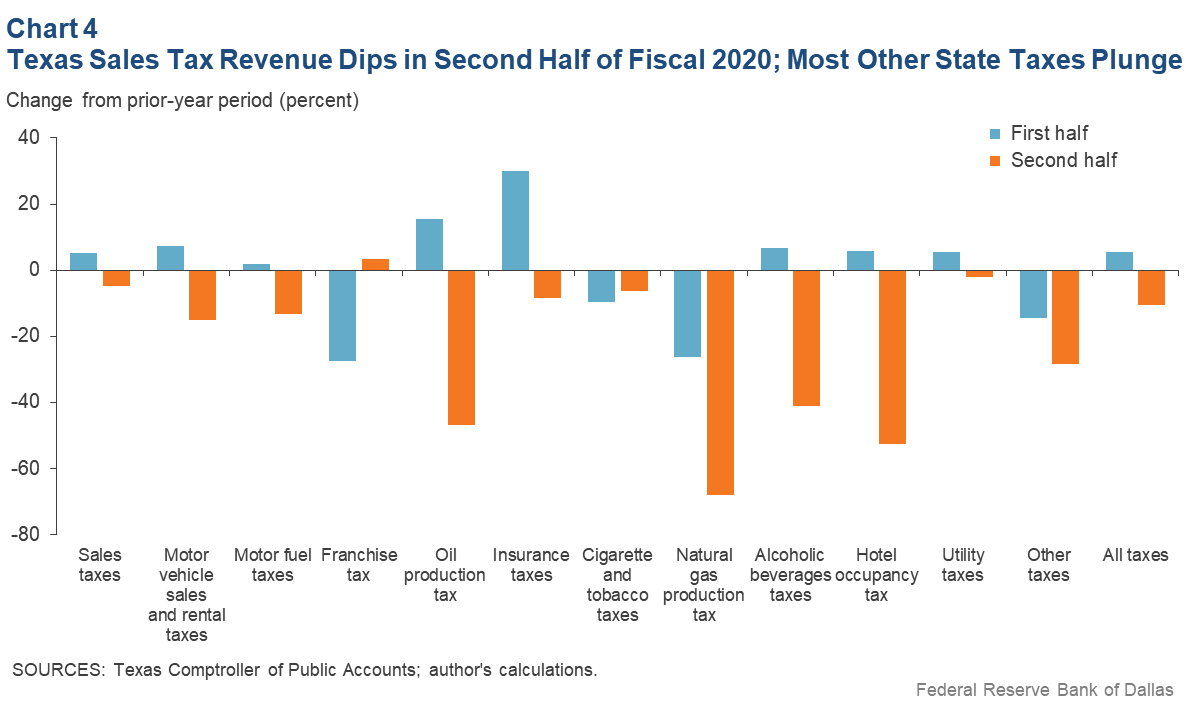

However, revenue declined 10.6 percent in the second half of the fiscal year compared with the same period in 2019 as COVID-19’s economic impact emerged. Sales tax collections alone fell 4.7 percent ($816 million) during the period.

Consumption often falls during recessions as people find themselves with less disposable income, putting at risk the three-fifths of state tax revenue that the sales tax provides.

If anything, social-distancing policies aimed at limiting COVID-19 spread may have exacerbated sales tax losses because the additional obstacles to conducting in-person transactions have been only partially offset by online or internet alternatives.

While diminished sales tax receipts are certainly part of the story, total state tax revenue slipped just over $3 billion in the second half of the fiscal year. That disappearing $800 million, while significant, represents only one-quarter of the state’s total tax revenue loss. That means other, smaller taxes have declined far more than the sales tax (Chart 4).

Levies on gasoline (down 13.3 percent), alcohol (off 41.0 percent) and hotels (down 52.6 percent) have been a key contributor to the shortfall. These taxes all correspond to the leisure and hospitality activities that have been dramatically curtailed because of social-distancing behavior, lockdown regulations and consumer health concerns.

Generating revenue from these taxes depends on how quickly individuals resume normal activities and policymakers permit businesses—which are themselves dependent on the level of COVID-19 cases—to fully reopen.

Another important contributor is the tax on oil production and extraction, a sector that was just beginning to recover from the late-2018 price slump and uneven recovery in 2019 when the pandemic struck.[10] Oil-tax revenue fell slightly last fall and rose 33 percent in the winter before abruptly plummeting by half during the ensuing months.

This can be contrasted with the less-meaningful tax on natural gas, where COVID-19 exacerbated difficulties in an already soft market.

One of the few taxes moving in the other direction is the franchise tax—Texas’ main tax on business revenue—which actually rose 3.4 percent in the second half of fiscal 2020. However, firms’ 2020 franchise-tax payments reflect revenue earned in 2019, in much the same way individuals pay income taxes on what they earned the previous year. As a result, the 3.4 percent increase is not reflective of current economic conditions, though it helps mitigate the revenue declines.

Unequal Metro Performance

While available local government data are mostly dated—largely collected before COVID-19—the recent Texas tax revenue developments shed light on what is happening in the state’s larger metropolitan areas.

The Dallas Fed publication At the Heart of Texas examines major metros in the Federal Reserve’s Eleventh District and highlights their key industries, several of which correspond directly to soft spots in the tax data.[11]

For example, the large decline in social/travel tax revenue at the state level can be expected to disproportionately affect San Antonio, whose economy is substantially based on tourism. Declines in the retail sector can be expected to disproportionately impact cities such as McAllen that are regional retail hubs and destinations of significant (but now much diminished) traffic from Mexico. And the ongoing decline in severance-tax revenue stems from energy sector woes that would disproportionately touch Houston and especially Midland/Odessa, whose economy is less diversified than Houston’s and, thus, even more vulnerable to energy slowdowns.

More generally, year-to-date sales tax revenue by city provides insight into the impact on metros of social-distancing behavior and related regulations. Very few other comprehensive local-government data sources are available on a timely basis.

In the COVID-19 era, one might reasonably suspect that consumption in smaller towns would hold up better than in larger cities because the virus would spread more rapidly in densely populated areas and people residing in rural or suburban areas would be less prone to travel to nearby large cities for social outings.

This is borne out in the data, with 73 percent of the state’s municipalities showing sales-tax growth for fiscal 2020, which began Sept. 1, 2019. However, the five largest cities are all down for the year. Whether this might lead to a longer-term shift toward less-densely-populated living or simply a brief social-distancing blip remains unclear, but it will be critically important to localities in the years to come.

Federal Government Aid

Overall, the decline in Texas tax revenue illustrates the many and varied ways in which COVID-19 has directly or indirectly affected the state government’s fiscal situation. Many local governments are struggling as well, especially in the hardest-hit larger cities.

Because both the state and its major municipalities are bound by balanced-budget requirements, they can resolve their current fiscal disparities—assuming the jurisdictions are left to their own devices—with a combination of tax increases and spending cuts.

That means Texas and its constituent parts face the unpalatable choice of either raising taxes during soft economic times or reducing services in areas such as health and education whose provision is, arguably, particularly important during the crisis. The state at least has access to its $8.5 billion rainy-day fund, which could soften the fiscal blow, but localities don’t typically have similar fund balances and, in many cases, were fiscally stretched even before COVID-19 began.[12], [13]

To mitigate those developments, Congress has provided some fiscal support to state and local governments, such as the $150 billion Coronavirus Relief Fund, which was created as part of the Coronavirus Aid, Relief, and Economic Security Act enacted in March to defray unplanned expenditures made necessary by the impact of COVID-19.[14]

Additionally, the Federal Reserve’s Municipal Liquidity Facility is providing credit to some cash-strapped state and local governments around the country. However, the Fed backing is in the form of loan guarantees, not gifts, so it is best viewed as adding fiscal leeway rather than actually bailing out affected localities.

While these measures provide a degree of respite for state and local officials, they can only go so far to relieve the stress of COVID-19. A safe return to more-normal business operations is a necessary prerequisite to generate the robust state and local tax revenue on which social services ultimately depend.

Notes

- Local jurisdictions can add 2 percentage points, bringing the total rate assessed on many transactions to 8.25 percent.

- For more on property taxes in Texas, see “Texas Property Taxes Soar as Homeowners Confront Rising Values,” by Jason Saving, Federal Reserve Bank of Dallas Southwest Economy, Third Quarter, 2018.

- These taxes also differ in their regressiveness. For more information, see “Texas Taxes: Who Bears the Burden?” by Jason Saving, Federal Reserve Bank of Dallas Southwest Economy, Third Quarter, 2017.

- “Public Budgets,” National League of Cities, www.nlc.org/public-budgets, accessed Aug. 5, 2020.

- For more on the lasting legacy of these cuts, see “A Punishing Decade for School Funding,” by Michael Leachman, Kathleen Masterson and Eric Figueroa, Center on Budget and Policy Priorities, November 2017.

- For an overview of how funding affects outcomes, see “Does Money Matter in Education?” by Bruce D. Baker, Albert Shanker Institute, April 2019.

- Much of the federal support provided during the pandemic, such as the $1,200 stimulus checks, are not taxable income and, thus, don’t directly contribute to state income tax revenue.

- Fiscal years typically extend from July 1 to June 30. However, Texas' fiscal year runs from Sept. 1 to Aug. 31.

- See “States Continue to Face Large Shortfalls Due to COVID-19 Effects,” by Elizabeth McNichol and Michael Leachman, Center on Budget and Policy Priorities, July 2020.

- For more on the relationship between energy prices and the state budget, see “Lingering Energy Bust Depresses, Doesn’t Sink State Budget,” by Jason Saving, Federal Reserve Bank of Dallas Southwest Economy, Fourth Quarter, 2016.

- For more information, see At the Heart of Texas: Cities’ Industry Clusters Drive Growth, Federal Reserve Bank of Dallas, December 2018.

- For more on Texas’ relative lack of health coverage pre-COVID-19, see “Texas Health Coverage Lags as Medicaid Expands in U.S.,” by Jason Saving and Sarah Greer, Federal Reserve Bank of Dallas Southwest Economy, Fourth Quarter, 2015.

- During the 2011 downturn, budget cuts particularly fell on K-12 education. For an analysis of their impact, see “2011 Budget Cuts Still Hampering Schools,” by Kiah Colliar, Texas Tribune, Aug. 31, 2015.

- Among the Texas jurisdictions receiving Coronavirus Relief Fund proceeds are Austin, Dallas, El Paso, Fort Worth, Houston and San Antonio and Bexar, Collin, Dallas, Denton, El Paso, Fort Bend, Harris, Hidalgo, Montgomery, Tarrant, Travis and Williamson counties.

About the Author

Jason Saving

Saving is a senior economist in the Communications and Outreach Department at the Federal Reserve Bank of Dallas.

Southwest Economy is published quarterly by the Federal Reserve Bank of Dallas. The views expressed are those of the authors and should not be attributed to the Federal Reserve Bank of Dallas or the Federal Reserve System.

Articles may be reprinted on the condition that the source is credited to the Federal Reserve Bank of Dallas.

Full publication is available online: www.dallasfed.org/research/swe/2020/swe2003.