Banks face new challenges as Texas rebounds from COVID-19 shock

Like much of the rest of the U.S. economy, the banking industry is finding its way after dealing with COVID-19 challenges in 2020. These included declining profitability—largely a product of lower net interest margins and greater loan loss provision expense.

Since the pandemic became widespread in March 2020, asset quality has deteriorated only slightly, holding up mostly because of loan forbearance. However, this support may simply push some credit-quality issues into the second half of 2021. While banks increased their allowance for loan and lease losses, credit quality remains a risk this year, particularly as exceptional government support ends.

For much of 2020, banks benefited from unprecedented public sector support—including historical levels of fiscal stimulus and the Paycheck Protection Program (PPP), which helped businesses maintain payrolls during the downturn. Regulators also encouraged banks to work with affected customers and offer loan forbearance.

Though many of these measures bolstered the economy, aggregate loan growth stalled in 2020 after excluding lending through PPP, in which most banks participated.

The Federal Reserve also played a significant role with its purchases of government securities to stimulate the economy and ensure smooth functioning of financial markets. These purchases increased bank balances at the Federal Reserve. When the Federal Reserve purchases government securities (Fed asset purchases) to support the economy, it credits the account of a bank or a bank customer with the cash. This activity has implications for banking system liquidity and capital.

In the case of banking system liquidity, Fed asset purchases can create deposits at banks, thus increasing their liquidity. When it comes to bank capital, Fed asset purchases can boost the size of the overall banking system’s balance sheet, reducing capital adequacy. Thus, in addition to facing possible strains from loan losses and pressured capital adequacy in 2021, banks will likely continue to confront headwinds to profitability from low interest rates and excess liquidity.

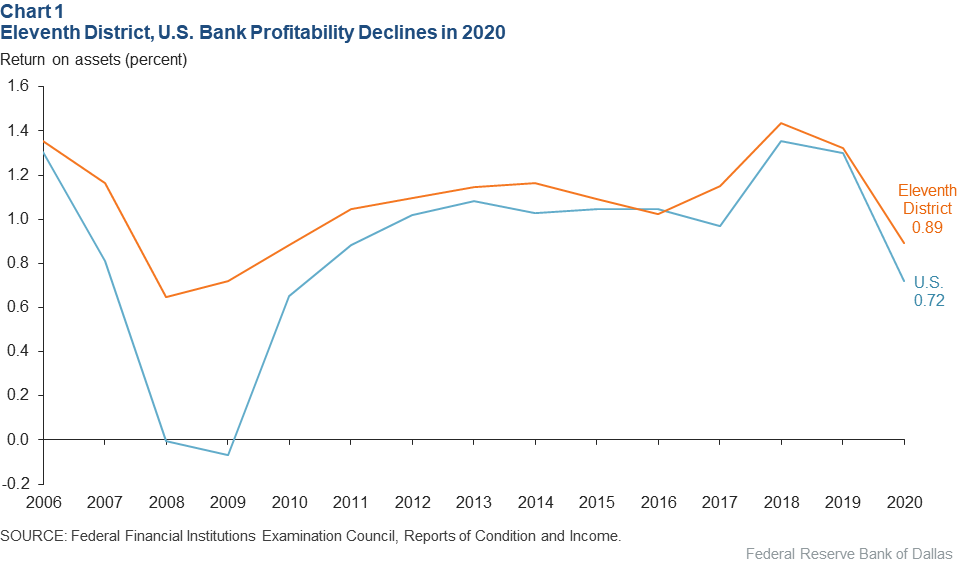

Sharply Lower Profits

The return on average assets for Eleventh District banks fell from 1.32 percent in 2019 to 0.89 percent in 2020—the lowest return since 2009 (Chart 1).[1] U.S. banks experienced an even steeper decline, from 1.30 percent to 0.72 percent—the lowest since 2010.

The decline in profitability was primarily driven by higher provision expense—which more than doubled from 2019 to 2020 for both district and U.S. banks—and by lower net interest margins.[2] Provision expense is the amount banks set aside to cover loan losses; provision expense gets added to a bank’s allowance for loan and lease losses, or loan loss reserves.[3] While the loan loss reserve is a buffer against expected losses, additions to it reduce profitability.

Net interest margins can fluctuate based on changes in interest rates—both rates paid on deposits and rates charged on loans. It can also vary with changes in the volumes of deposits and earning assets, such as loans and securities.

Interest rate changes were mainly responsible for the decline in net interest margins in 2020. They declined as the economic outlook weakened, as evidenced by cuts to the federal funds rate in early 2020 and a flattening of the Treasury curve—a reduction in the difference in interest rates investors demand for short- and long-term Treasury obligations.

This affected the rates banks charged borrowers on their loans as well as the deposit rates banks paid to customers. Rates charged on loans fell faster than those paid on deposits. The drop in net interest margins was also due, to a lesser extent, to a surge in the quantity of deposits, causing banks to pay out more in interest to customers despite falling interest rates.

Deposits at commercial banks nationally totaled $17.7 trillion at year-end 2020—23 percent higher than at year-end 2019 (Table 1). The annual growth in deposits was significantly greater than any year since 1973, when data collection began. The surge in deposits added to banks’ liquidity and can be attributed to the pandemic support measures, with significantly higher U.S. household savings and Fed asset purchases both contributing.

Table 1: PPP, Fed Balances and Securities Fuel Banking System Balance-Sheet Growth

| Change, Dec. 31, 2019–Dec. 31, 2020 | ||||

| Eleventh District banks | U.S. banks | |||

| Dollars (billions) | Percent | Dollars (billions) | Percent | |

| Total assets | 105 | 19 | 3,223 | 17 |

| PPP | 23 | – | 406 | – |

| Loans (excl PPP) | -$2 | -0.5 | -62 | -0.6 |

| Investment securities | 40 | 31 | 1,127 | 28 |

| Balances due from Federal Reserve Banks | 67 | 152 | 1,594 | 103 |

| Other | -23 | -63 | 158 | 6 |

| Total liabilities | 100 | 21 | 3,109 | 19 |

| Deposits | 97 | 21 | 3,273 | 23 |

| Wholesale funding | -0.1 | -0.6 | -343 | -32 |

| Other | 3 | 29 | 179 | 19 |

| Equity capital | 5 | 8 | 114 | 5 |

| NOTE: PPP refers to the Paycheck Protection Program. SOURCES: Federal Financial Institutions Examination Council, Reports of Condition and Income; Federal Reserve H.4.1 Release. |

||||

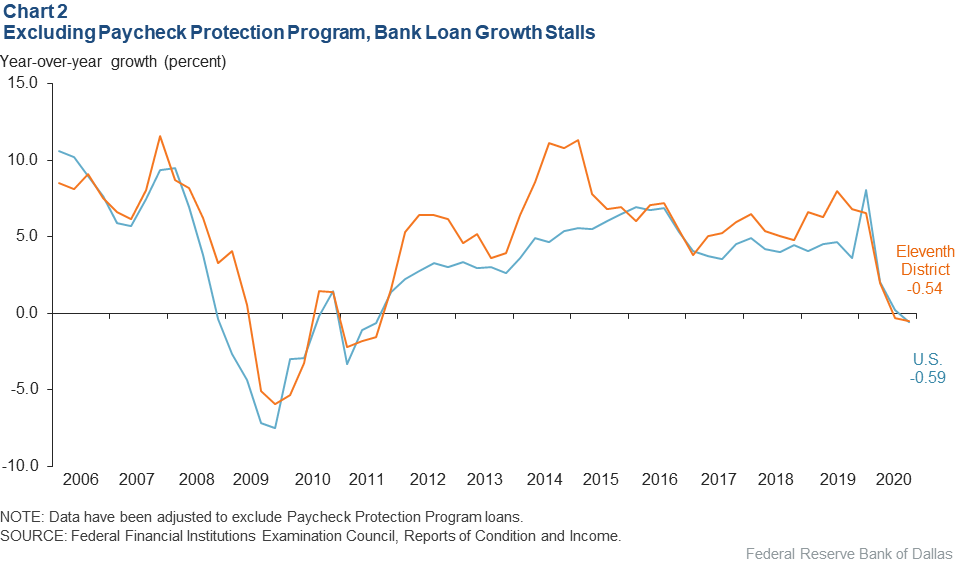

Loan Volume Declines

A decline in interest income caused by lower loan volume further pressured net interest margins. Loan growth—outside of PPP loans—stalled nationally and in the district in 2020. Excluding PPP loans, total loans contracted year over year in fourth quarter 2020—the first such decline since 2011—falling 0.54 percent for district banks and 0.59 percent for U.S. banks (Chart 2).

Aggregate loan growth, inclusive of PPP loans, was positive in 2020. Now that the PPP has ended, many of those loans will be forgiven under terms of the law creating the federal assistance effort or, in some cases, they will be repaid. Should loan demand remain sluggish as the economy improves, banks could feel pressure to search for other opportunities to deploy their excess liquidity, such as buying securities.

Bigger Balance Sheets

Banks’ total assets grew despite soft loan conditions because of public sector intervention. Among Eleventh District banks in 2020, assets increased $105 billion, or 19 percent, compared with 17 percent for all U.S. banks, as seen in Table 1.

Bank balance-sheet growth in 2020 can be attributed to PPP loans, growth in reserve balances at the Federal Reserve due to Fed asset purchases, and increased holdings of investment securities. District banks experienced larger balance-sheet growth than their national counterparts. Increases in the size of bank balance sheets act to weaken banks’ leverage ratios—a measure of a bank’s core capital relative to its total assets.[4]

Bank reserves at the Federal Reserve are likely to continue to increase in 2021 as a result of additional Fed asset purchases—part of the Federal Reserve’s ongoing response to the pandemic— and stimulus funds moving from the Treasury to taxpayers, who, in turn, increase deposit balances at banks.

Assessing Asset Quality

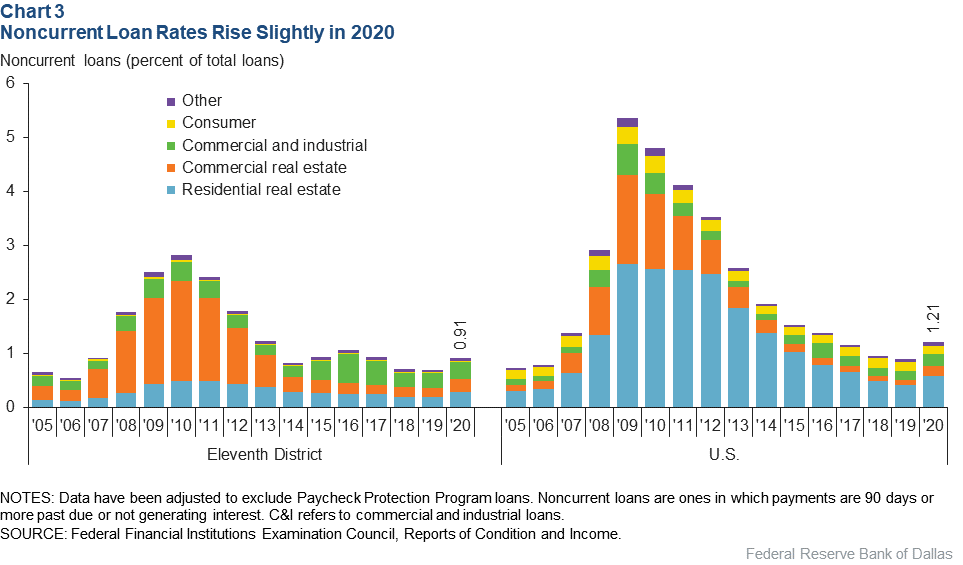

Credit quality largely held up in 2020, despite a sharp recession and historical levels of unemployment that would normally be consistent with a sharp deterioration in asset quality. Personal bankruptcies actually fell during the pandemic, while corporate bankruptcies rose but have remained well below 2008–09 levels.

The noncurrent loan rate—the percentage of loans past-due 90 days or more or on nonaccrual status (not generating interest)—ticked up to 1.21 percent nationally and 0.91 percent in the district in 2020, still well below financial-crisis levels. The increase in the noncurrent loan rate was primarily due to increases in noncurrent residential real estate loans, followed by increases in noncurrent commercial real estate (CRE) loans, both nationally and in the district (Chart 3).

During prior downturns, high CRE-related losses contributed to bank failures and constrained bank lending. Banks with less than $100 billion in total assets may be particularly vulnerable to such losses because they are more concentrated in CRE relative to larger banks. Within CRE, the retail and hotel segments have been stressed the most during the pandemic. However, risk of future deterioration in office and even multifamily segments, combined with sizable bank exposures to these sectors, could lead to credit losses.

While bank CRE losses have risen only marginally during the pandemic, they tend to lag the deterioration of commercial mortgage-backed securities (CMBS)—packages of commercial mortgage loans sold to investors and not backed by a U.S. government-sponsored enterprise such as Fannie Mae or Freddie Mac.[5]

Credit deterioration within the CMBS market has been more evident during the pandemic. The delinquency rate on loans in CMBS securitizations—30 days or more past due—rose from just 2 percent prepandemic (March 2020) to a peak of 10.3 percent in June and stood at 6.5 percent in April 2021, according to Trepp, a provider of mortgage data.

Other measures of risk for loans in CMBS securitizations, including watch lists and special servicing for troubled loans, are also elevated. The share of CMBS loans on watch lists, indicating possible credit concerns, stood at 25.7 percent in April 2021, up significantly from 8.5 percent in March 2020. The share transferred into special servicing, designed to help resolve troubled loans, was 9.0 percent in April 2021, also up notably from 2.7 percent in March 2020. CMBS credit deterioration could signal trouble ahead for banks’ CRE credit quality.

The limited deterioration in banks’ asset quality is largely a result of extensive government and Federal Reserve support to households and businesses in response to the pandemic. Additionally, the Coronavirus Aid, Relief, and Economic Security (CARES) Act gave banks greater latitude to work with affected customers, offering forbearance—including payment deferrals, fee waivers and extension of payment terms—on outstanding loans.

Banks’ loan balances in forbearance under the CARES Act totaled 2.8 percent of all loans (excluding PPP) nationally as of fourth quarter 2020. This share was down from 5.8 percent in second quarter 2020, an improvement that banks largely attributed to customers resuming normal payments once their deferral period ended.

Loan balances remaining in forbearance could negatively affect banks’ asset quality if they become noncurrent.

Potential Loan Losses

While the economy is set to grow quickly this year, concern remains that once pandemic relief measures end, delinquent loans and loan losses might increase. This could occur if businesses and consumers in forbearance are unable to resume loan payments or because of structural changes in the economy permanently affecting certain industries, such as retail, hospitality and office construction.[6]

While the banking sector was generally well-capitalized before the pandemic, scenario analysis can provide insight about the potential impact of higher loan losses on bank capital levels.

The Federal Reserve Bank of Dallas has developed an internal capital calculation tool that translates a set of loan loss rates into an estimate of banks’ risk-based and leverage capital ratios.[7] The resulting capital ratios under a given loan loss scenario can help determine if an institution could become undercapitalized—at least one capital ratio falling below regulatory minimums.

Using this tool, one can consider the impact of two potential scenarios of loan loss (loans that default) over a one-year horizon. One is a baseline scenario that stresses all loan categories using a loss rate—loans that default as a share of total loans—of 1.5 percent. The other is a downside scenario using loss rates derived from regulators’ 2020 large-bank stress tests.[8]

Table 2 shows the one-year loss rates—the share of total loans that default in one year—for each scenario. For reference, the peak one-year loss rates from the financial crisis and the average of bank regulators’ 2013–19 large-bank stress test loss rates by major loan type are also shown.

Table 2: Loan Loss Rates May Rise with Added Stress

Scenario Analysis, One-Year Loan Loss Rates (Pct.)

| First-lien residential | Jr. lien/HELOC | C&I | CRE | Credit card | Other consumer | Other loans | |

| Baseline scenario | |||||||

| Downside scenario | 0.95 | 1.40 | 3.35 | 5.60 | 9.90 | 2.85 | 1.80 |

| Financial crisis peak | 2.01 | 4.25 | 2.94 | 2.92 | 12.89 | 3.73 | 0.82 |

| Large-bank stress tests average (2013–19) | 1.61 | 3.00 | 2.79 | 3.41 | 6.55 | 2.52 | 1.40 |

| NOTES: The large-bank stress tests’ average one-year loan loss rates are from bank regulators’ 2013–19 Dodd-Frank Act Stress Tests. HELOC refers to home equity line of credit; C&I refers to commercial and industrial loans; CRE refers to commercial real estate loans. SOURCES: Federal Reserve Bank of Dallas; Dodd-Frank Act Stress Tests; Federal Financial Institutions Examination Council, Reports of Condition and Income. |

|||||||

Nationally, only 3 percent of banks are estimated to become undercapitalized in the baseline scenario. Banks becoming undercapitalized may face restrictions on their growth, capital distributions and merger transactions. The share of all U.S. banks estimated to become undercapitalized increases to 10 percent in the downside scenario.

Within the Eleventh District, 2 percent of banks could become undercapitalized in the baseline scenario, increasing to 8 percent in the downside scenario. Given continued economic improvement this year, it is unlikely loan loss rates for all loan categories will be as high as those in the downside scenario. However, it is possible that some loan categories could experience stress once public sector support expires.

Looking Ahead

While strong economic growth is anticipated in the second half of 2021 as the economy reopens, some credit deterioration and losses are possible as fiscal support and forbearance programs end.

There is significant uncertainty about potential loan losses at banks, but scenario estimates indicate moderate possible impacts on bank capital in 2021. Banks also face continued pressure on net interest margins absent a rebound in loan demand and a sustained, steeper Treasury curve.

Notes

- Data for Eleventh District institutions have been adjusted for structure changes such as mergers, acquisitions and relocations. The district comprises Texas, northern Louisiana and southern New Mexico.

- Net interest margin is the difference between a bank’s interest income (loan and securities yields) and interest expense (deposit and other borrowing costs) weighted by average earning assets.

- Allowance for loan and lease losses (ALLL) increased, partly due to the adoption of the current expected credit loss (CECL) model by some institutions in early 2020, but not many Eleventh District banks adopted CECL in 2020. Other increases in ALLL were due to normal provisioning for loan losses.

- A bank’s core capital includes assets that can be easily liquidated if the bank needs capital in the event of a large unexpected loss or financial crisis. PPP loans were excluded from bank leverage ratios if they were funded with Payment Protection Program Liquidity Facility borrowings from a Reserve Bank.

- Due to their structure, CMBS loans can be more difficult to modify or defer than bank loans.

- "COVID-19 Slammed into Texas, Leaving Long-Lasting Impacts,” by Emily Kerr, Judy Teng and Keith Phillips, Federal Reserve Bank of Dallas Southwest Economy, First Quarter 2021.

- Capital estimates are equal to beginning capital plus cumulative pre-provision net revenue (PPNR) minus cumulative loan losses, taxes and dividends. PPNR is based on current-quarter net interest income, the average of the most recent four quarters for noninterest expense and the average of the four quarters prior to PPP for noninterest income. A tax rate of 21 percent is applied to institutions with PPNR greater than loan losses. Dividends are equal to the sum of the most recent four quarters.

- The downside scenario uses loan loss rates based on the Dodd-Frank Act Stress Test (DFAST) December 2020 Severely Adverse scenario. For purposes of this article, published nine-quarter DFAST loan loss rates are converted to four-quarter loss rates. See federalreserve.gov/publications/files/2020-dec-stress-test-results-20201218.pdf.

About the Authors

Amy Chapel

Chapel is a macrosurveillance manager in the Banking Supervision Department at the Federal Reserve Bank of Dallas.

Kory Killgo

Kilgo is a financial industry analyst in the Banking Supervision Department at the Federal Reserve Bank of Dallas.

Kelly Klemme

Klemme is a data scientist in the Banking Supervision Department at the Federal Reserve Bank of Dallas.

Southwest Economy is published quarterly by the Federal Reserve Bank of Dallas. The views expressed are those of the authors and should not be attributed to the Federal Reserve Bank of Dallas or the Federal Reserve System.

Articles may be reprinted on the condition that the source is credited to the Federal Reserve Bank of Dallas.

Full publication is available online: www.dallasfed.org/research/swe/2021/swe2102.