Energy financing trends consistent with renewables’ growth

Banks and financial markets have long provided credit intermediation in the financing of U.S. energy firms’ capital expenditures. Thus, it is notable that oil and gas (O&G) was the second-largest sector for U.S. corporate bankruptcies attributable to cyclical and structural strains in 2020.

Energy is experiencing a significant transition stemming from efforts to address climate change and reduce carbon emissions. Solar, wind and other renewable-energy technologies are maturing and their costs are declining rapidly.

Equity markets appear to favor renewable-energy producers relative to their hydrocarbon counterparts. The corporate bond market shows notable differences between O&G and renewables in issuance volumes and secondary market spreads relative to Treasuries. However, the relatively smaller size of many renewables projects complicates direct comparisons of bank lending to hydrocarbon and renewable entities.

Stark differences visible in U.S. equity markets

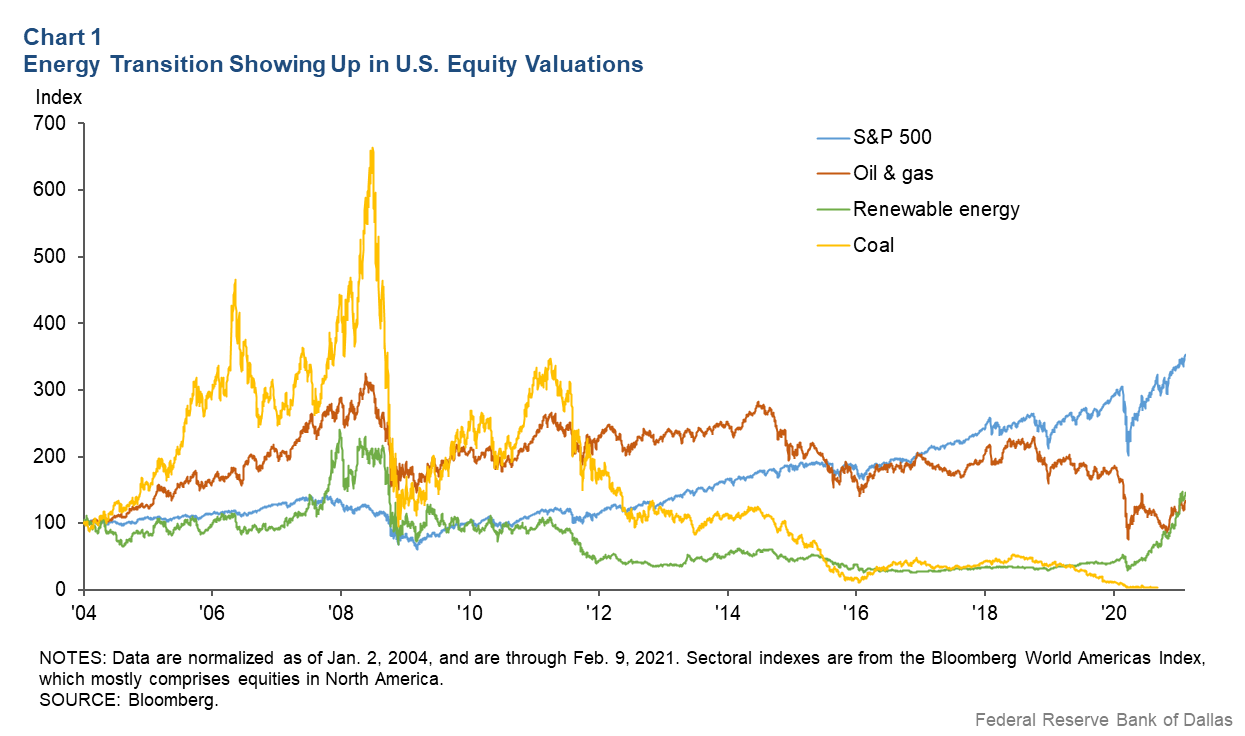

O&G stocks underperformed the overall U.S. equity market in the past decade, a period in which valuations boomed (Chart 1). O&G was the second-worst performing sector and a significant drag on market returns.

O&G firms, which accounted for 16 percent of the Standard & Poor’s 500 index in third quarter 1990, make up just 2 percent of the index today. The U.S. coal sector’s equity performance has struggled even more, losing 97 percent of its market capitalization since 2004. Conversely, the renewable-energy sector is up 47 percent during this period, notably propelled by recent market gains.

While O&G shares have risen this year, mirroring recent increases in oil and natural gas prices, firms’ highly leveraged balance sheets and the need to self-fund significant capital expenditures may constrain future equity valuations. Additionally, according to a recent Deutsche Bank survey, the influence of environmental, social and governance investing is a fast growing theme, with two-thirds of 460 surveyed portfolio managers globally reporting these considerations influenced more than 10 percent of their investments as of February 2021.

O&G, renewables bonds differ markedly in issuance and spread

O&G companies have sold $707 billion in new corporate bonds since 2011, while coal companies accounted for $25 billion in new issuance. Renewable-energy firms—largely involved in power generation—have placed just $4.2 billion cumulatively in net new corporate bonds during the period, amounting to about 30 percent of a broader “renewables” category. It includes companies in a range of industrial activities, including battery and electric vehicle manufacturing.

However, market contacts note that low levels of renewable-energy corporate bond issuance mostly reflect a preponderance of smaller renewable-energy transactions, most of which are funded through project finance and not corporate bonds. They describe much of this financing market as coming from investors seeking tax credits, private equity firms and banks active in project finance. Among the investments are U.S. wind projects totaling $143 billion during the past 10 years, according to American Wind Energy Association estimates.

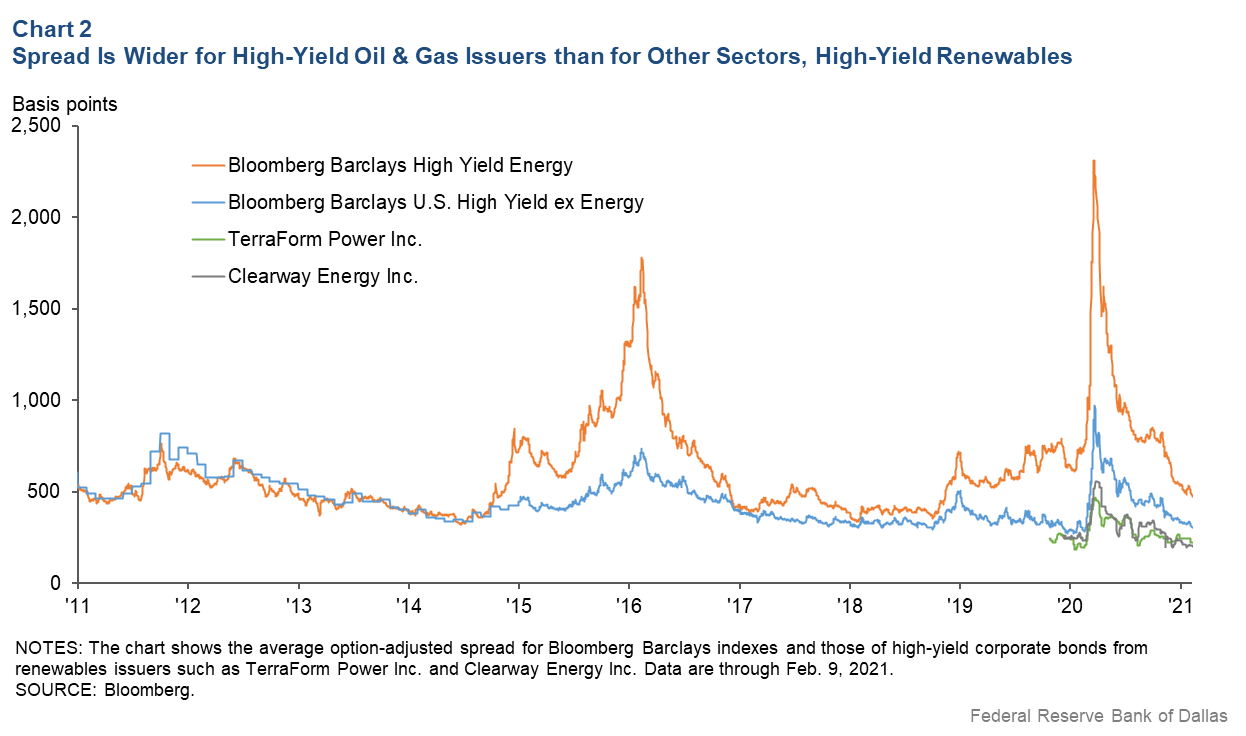

Meanwhile, high-yield O&G issuers’ corporate bonds have, since 2014, consistently traded at spreads over Treasuries that exceed those of high-yield bonds of all other issuers (Chart 2).

Just before the COVID-19 outbreak began last year, option-adjusted spreads on high-yield bonds of O&G issuers rose to levels exceeding 2,000 basis points. A basis point is 0.01 percentage points and is the common unit of measure used in bond and other fixed-income securities trading.

While overall spreads have since declined, those of high-yield O&G issuers remain nearly double those of other high-yield issuers. Option-adjusted spreads are tighter on bonds of high-yield corporate renewable-energy issuers Terraform Power Inc. and Clearway Energy Inc. These renewables firms’ bonds have comparable duration to the corporate bond indexes shown in Chart 2.

In February 2021, Standard & Poor’s increased the industry risk scores for exploration and production and midstream O&G firms due to structural headwinds from the transition to renewables. As a result, 12 investment-grade exploration and production issuers were put on CreditWatch, which sometimes precedes a credit rating reduction.

Bank lending for renewable-energy projects difficult to measure

There were $467 billion of outstanding commitments in syndicated loans to the O&G sector and $59 billion to the renewable-energy sector as of third quarter 2020. These data reflect much of the U.S. bank lending activity related to the hydrocarbon sector, while the renewables portion is likely not fully captured.

Renewable-energy lending is more difficult to measure because the loan data are limited to commitments exceeding $100 million syndicated to three or more unaffiliated federally supervised banking firms. Generally, these deals are much larger than the average renewable-power project. Sources such as kWh Analytics' Lendscape suggest that banks are active in financing for renewable solar projects.

Lender risks differ between O&G, renewables firms

Financing is challenging for many O&G producers even as the sector has the largest near-term financing need among U.S. corporates under a range of scenarios, according to a recent International Monetary Fund working paper. Reduced availability of equity capital to O&G firms—which can leave these firms overextended and more prone to default—negatively affects the desirability of bank lending and bond investment. An energy transition from hydrocarbons could saddle credit providers to that sector with assets that have diminished value at a time when there exists a limited market to offload them.

At the same time, interest is growing in providing credit to renewable energy. Here, imprudent lending is a possible hazard. Some examples of risks include wind failing to meet projections (resource availability risk) and falling cost structures due to technological change rendering some renewable-energy projects uneconomic. There is also the possibility of power offtake agreements—which traditionally have governed the sale of output from generating facilities—shifting pricing risk to renewable-energy producers from utilities.

Key data gaps complicate analysis

An energy transition is clearly underway, with renewable energy now providing more power than coal in the U.S. at a time of historically high O&G bankruptcies.

While some data provide insight on financing conditions among renewable-energy firms, assembling more complete data on bank and nonbank lending for renewable energy is a key shortcoming given the smaller size of these energy projects.

Such data are important to monitoring the structural changes occurring in this key sector of the U.S. economy given efforts to reduce carbon intensity. The energy sector will be an area that merits ongoing monitoring and oversight.

About the Authors

Sung Je Byun

Byun is a research economist in the Supervisory Risk and Surveillance Department at the Federal Reserve Bank of Dallas.

Jill Cetina

Cetina is a vice president in the Supervisory Risk and Surveillance Department at the Federal Reserve Bank of Dallas.

Joe Kneip

Kneip is a bank examiner in the Supervisory Risk and Surveillance Department at the Federal Reserve Bank of Dallas.

The views expressed are those of the authors and should not be attributed to the Federal Reserve Bank of Dallas or the Federal Reserve System.