Capacity constraints drive the OPEC+ supply gap

The growing gap between OPEC+ production quotas and actual oil production has drawn increased attention in recent months because of its implications for crude oil prices. Production capacity constraints in several OPEC+ countries are driving much of this gap. These constraints will only become more binding through the year.

OPEC+ slowly unwinding supply cuts

OPEC+, a group of 23 oil-producing countries, enacted a massive supply cut in April 2020 to accommodate the drop in global oil demand associated with the coronavirus pandemic. The move effectively ended a price war in global oil markets. Since mid-2021, the group has been unwinding these cuts, typically raising production quotas each month by a combined 400,000 barrels per day (b/d).

Every OPEC+ member’s individual quota increases by an amount related to how much it contributed to the total cut in 2020. For example, the group’s quota in January 2022 was 400,000 b/d higher than in the prior month. Saudi Arabia, which made up 26 percent of the initial cut, saw its January quota increase by 104,000 b/d. Eventually, each country’s quota will return to its “baseline” production level, which in most cases corresponds to what the country produced in October 2018.

Importantly, if a country cannot meet its individual quota for a given month, there is no written agreement for other members to make up for that shortfall.

This has certain advantages. For example, each country is given a fair chance to increase its production every month using an agreed-upon formula; at the same time, there is no need to undertake potentially thorny discussions surrounding which member may increase production should another member fail to meet its monthly quota. Additionally, OPEC+ has a compensation mechanism in which countries are given time to adjust when their compliance falls below 100 percent.

The downside of this arrangement is that it becomes challenging for the group to target a specific production level because no country can step in if another falls short of its target.

How to measure OPEC+ production

Measuring OPEC+ production is a necessary first step when quantifying the supply gap. While this task may seem straightforward, there are at least six different sources for production data that do not always align with one other. Here we rely on International Energy Agency (IEA) data from its monthly Oil Market Report released in March 2022. Supply gaps calculated using other sources may vary from those we report.

It is important to note that three OPEC members—Iran, Venezuela and Libya—are currently excluded from the production quotas. Additionally, while some observers include Mexico among the larger group of OPEC+ countries, it is not bound by any official quota. We therefore exclude these four countries from our supply-gap calculations and focus on the remaining 19 members of OPEC+ that have official quotas.

This distinction can be important in some months. For example, in January 2022, the 19 countries we consider increased their production collectively by 370,000 b/d, which was about 92.5 percent of the 400,000 b/d quota increase for that month.

The production increase after including Iran, Venezuela, Libya and Mexico was 230,000 b/d, or just 57.5 percent of the quota increase. This makes the shortfall look larger in January. However, since none of these four countries have official targets, it seems more appropriate to focus on the 19 that do.

Growing supply gap garners attention

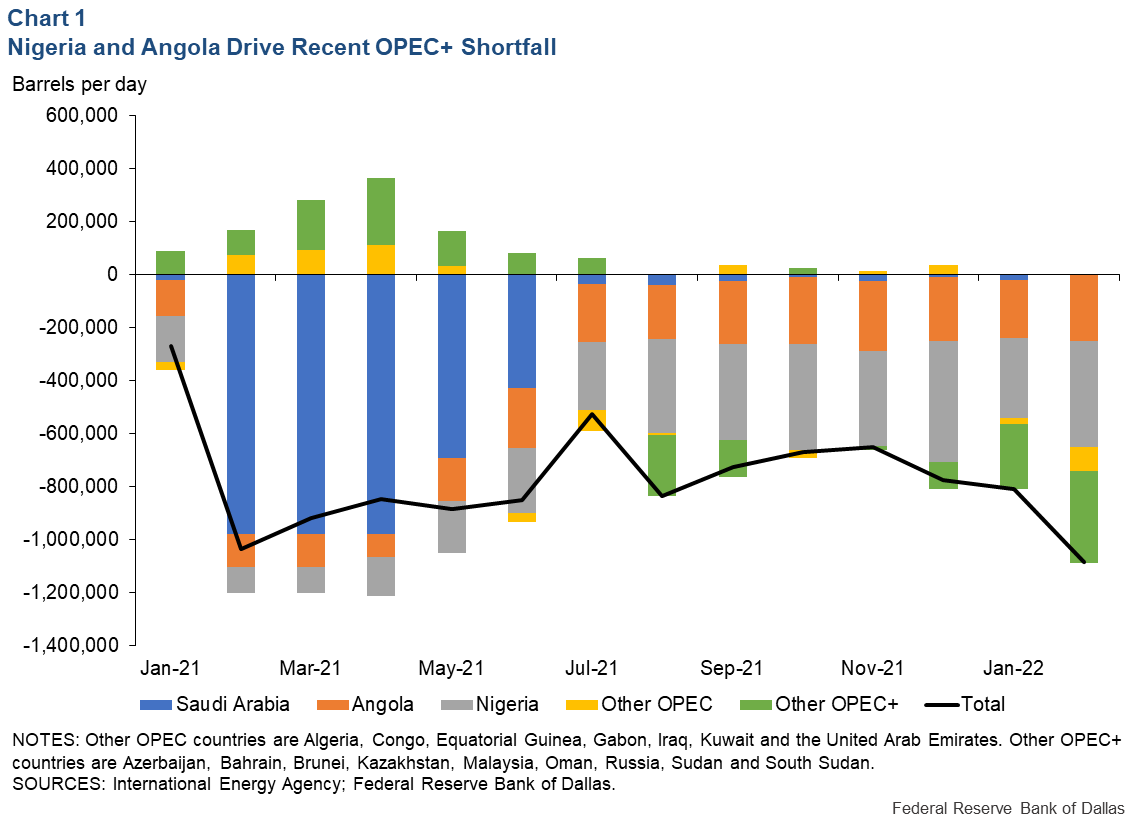

Various commentators have noted a gap between OPEC+ quotas and actual production levels. There are several ways of presenting this gap. Some report a monthly gap between the total quota and total production, considering only those countries participating in the agreement. This gap stood at almost 1.1 million barrels per day (mb/d) in February, the most recent month for which there are official production data (Chart 1).

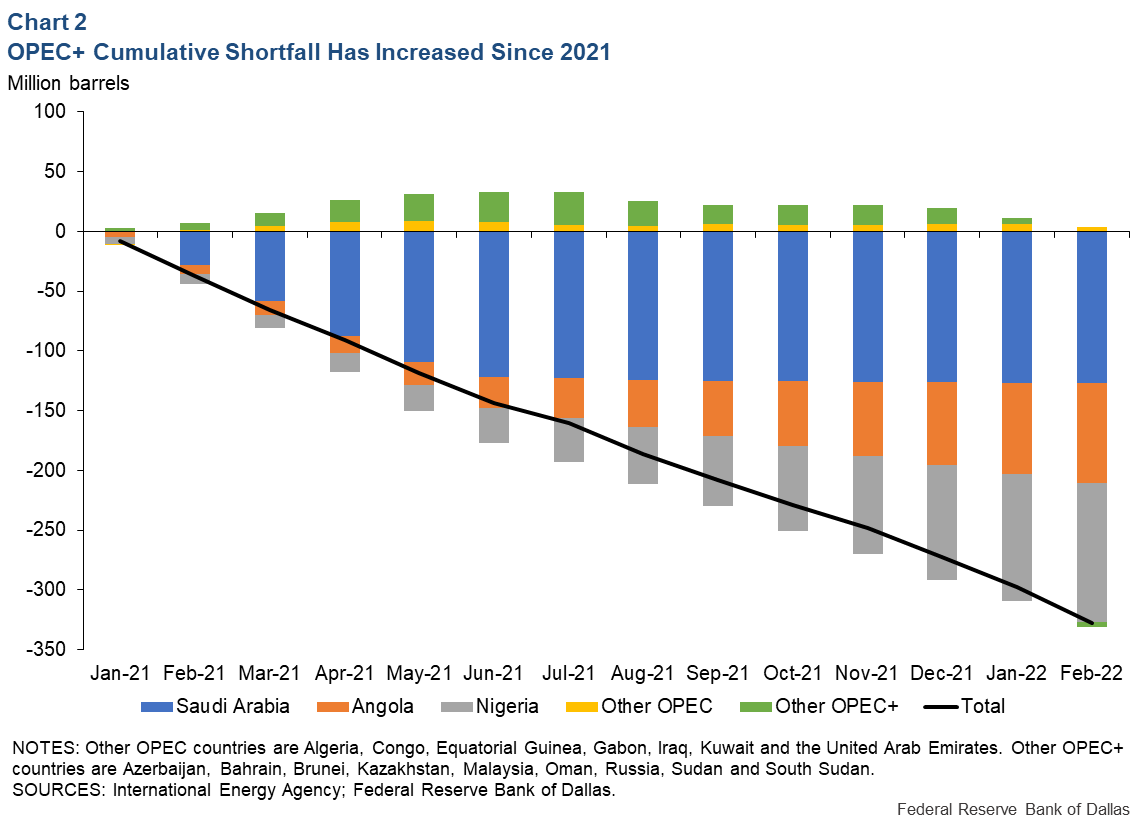

Others report the cumulative losses in supply over some period. By this measure, there was a large and growing production shortfall in the group, with the total reaching more than 300 million barrels by the end of 2021 and increasing into 2022 (Chart 2). A closer look shows that this shortfall is largely attributable to three countries: Angola, Nigeria and Saudi Arabia.

Capacity constraints drive supply gap

There are a number of reasons this supply gap has emerged. One important explanation—and one that continues to play a role in 2022—is the inability of some OPEC+ members to increase production to take advantage of their growing quotas. These countries are bumping into capacity constraints for several reasons, including infrastructure issues and the difficulty of attracting sufficient investment to offset production declines at existing wells.

Angola is an example. Its quota in February 2022 was 1.42 mb/d. However, Angola’s maximum capacity is 1.19 mb/d, according to IEA estimates. This supply gap will only worsen in coming months, as Angola’s quota will eventually reach 1.53 mb/d, the country’s October 2018 output according to OPEC.

Capacity constraints also affect Nigeria, whose February target was 1.70 mb/d but whose sustainable capacity was 1.54 mb/d, according to the IEA. Even reaching the sustainable capacity level has been difficult for the country—it has not produced at that level since mid-2020.

Saudi Arabia’s shortfall in the first half of 2021 was unrelated to capacity constraints, on the other hand. The country enacted a voluntary production cut from February 2021 to June 2021, with the goal of bringing down global inventory levels.

Increasing attention on OPEC+ supply role

Dwindling OPEC+ spare capacity looms large, given expectations of continued strong global demand in 2022 and 2023—concerns that have been elevated by Russia’s invasion of Ukraine.

Assuming that the group increases production at the same pace it has in recent months, only a handful of countries in OPEC+ will have spare capacity left by the start of the summer, a number that will dwindle as year-end approaches. Thus, the supply gap is expected to continue growing this year with many OPEC+ countries unable to take advantage of the higher production quotas they will receive under the group’s agreement.

About the Authors

Kilian is a senior economic policy adviser in the Research Department at the Federal Reserve Bank of Dallas.

Plante is a senior research economist and adviser in the Research Department at the Federal Reserve Bank of Dallas.

Patel is a senior business economist in the Research Department at the Federal Reserve Bank of Dallas.

The views expressed are those of the authors and should not be attributed to the Federal Reserve Bank of Dallas or the Federal Reserve System.