Dirty air from wildfires casts a cloud over household finances

California’s Camp Fire, which began in November 2018, is among the most damaging U.S. wildfires to date. Residents of Butte County, about 85 miles north of Sacramento, were left to pick up the pieces after the fire ravaged 153,335 acres, destroying 18,800 structures. Roughly 30,000 people lost their homes and 86 people died.

Since 2018, wildfires have become more frequent and intense. Using the Camp Fire as a natural laboratory, a new working paper examines the effects of both fire and smoke-related air pollution on household credit card spending and repayment.

The paper finds increased spending, indebtedness and loan delinquencies among households distant from the Camp Fire but exposed to high levels of wildfire-linked air pollution. Further analysis points to health-related spending associated with the adverse financial impacts.

The estimated effects of wildfire smoke and pollution are salient to substantial, geographically dispersed populations and add appreciably to estimates of household financial distress arising from extreme climatic events.

Credit effects of air pollution differ

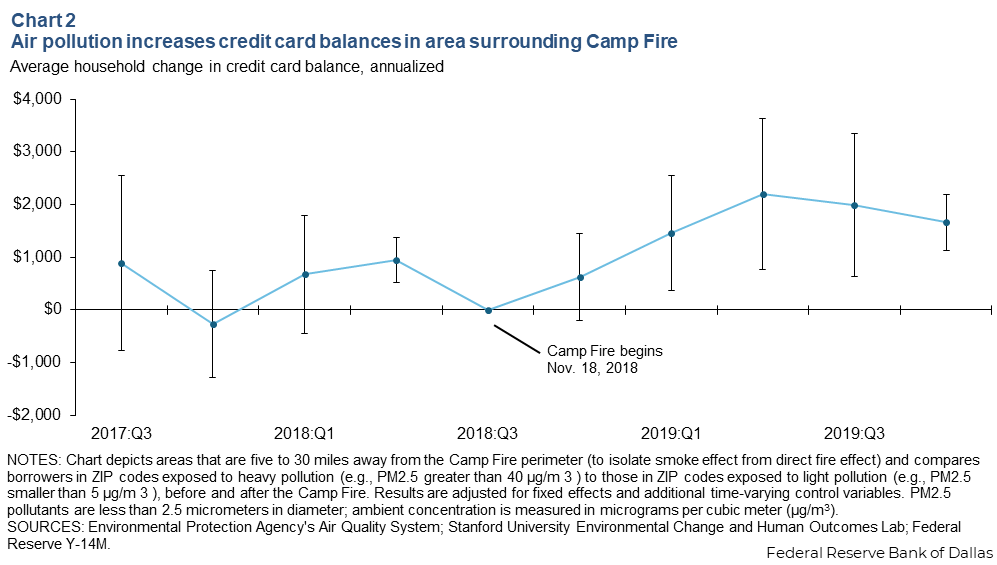

Due to differing geography and weather, the area surrounding a wildfire’s burn zone experiences varying levels of air pollution. We take advantage of this fact to examine air pollution’s effect on household credit, considering areas within a 5- to 30-mile ring surrounding the burn zone. Differences in credit use emerge within this ring—areas of heavy pollution compared with areas of light pollution.

Both credit card spending and balances increased in areas exposed to higher levels of pollution (Chart 1).

In fact, borrowers exposed to higher levels of wildfire-related air pollution, on average, increased spending by $730 each on an annual basis relative to those exposed to lower levels of air pollution. Repayment of credit card debt among the more highly exposed households was $521 less per household on an annual basis, leaving individual members of this group with roughly $1,400 more in annualized credit card balances.

The effect of wildfire-related air pollution on credit card spending and repayment could be explained by an increase of health care costs, loss of income and lack of homeowner’s insurance payouts among those experiencing heavy wildfire-related air pollution (Chart 2).

Increased air pollution often leads to higher health care costs, as individuals spend on both preventative and non-preventative expenses. Costs associated with medication, ER visits and accessories such as air purifiers all tend to contribute to increased credit card spending following a wildfire. Amplifying an increase in spending, loss of income can affect an individual’s ability to repay credit card balances as businesses often choose to remain closed in times of hazardous air pollution.

These individuals are unable to resolve financial strains with insurance money. Instead, they must rely on savings or government assistance to mitigate difficult financial situations.

Reliance on savings and assistance is evident within the data. For those experiencing heavy pollution, increases in credit card spending are found largely among super-prime borrowers and borrowers with high credit limits—likely members of high-income households who are more likely than members of low-income households to have the resources to repay increased credit card debt.

Reductions in credit card repayments are found primarily among lower credit score borrowers, who are unable to access as many resources as those with high credit scores.

Insurance a likely important factor in recovery for burn zone households

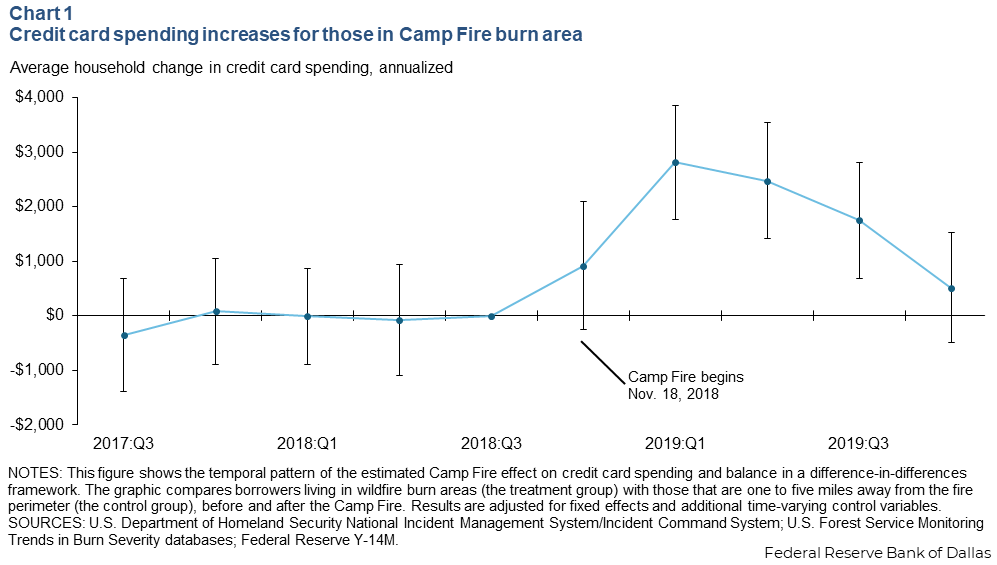

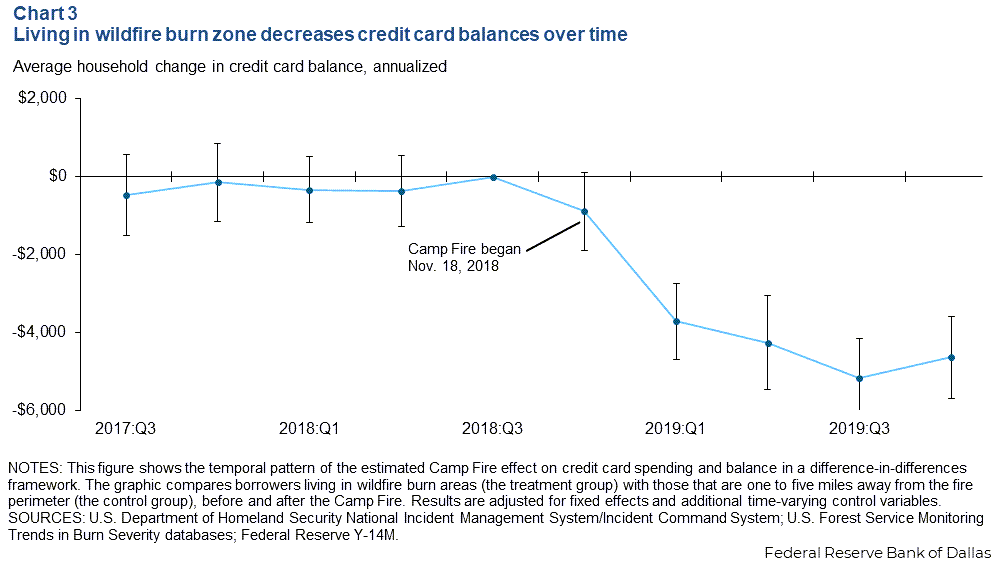

To look at the effect of the Camp Fire, we compare data from its burn zone to that of the surrounding one- to five-mile area.

While credit card spending increased, credit card balances decreased significantly following the wildfire. Those living in the burn zone of Camp Fire each spent roughly $1,670 annualized more than those in the surrounding area in the 14 months following the fire. Burn area households also engaged in about $2,350 each in additional annual repayment. This resulted in an average reduction in the credit card balance of $2,370 per household annually (Chart 3).

A decline in credit card balances may seem counterintuitive given the increased credit card spending. Insurance payments to homeowners experiencing fire damage likely explain what occurred.

While homeowners receiving insurance payouts could pay down balances, most renters lacked insurance funds and did not undertake significant cash repayments. Consequently, the renters experienced higher rates of credit card delinquency.

Air pollution’s effects widespread, cumulatively large

Fire has a greater effect than air pollution on individual household credit card spending and balances. However, wildfire related emissions affect a larger and more dispersed group than the fire itself. Such economic impacts, though smaller at the household level, can add up over time.

The Canadian wildfires of June 2023 provide an example of the far-reaching effects. In the wake of the fires, heavy smoke and particulate emissions blanketed an area with 122 million residents across major parts of the Northeast and north-central United States, resulting in some of the region’s most polluted days on record.

If we conservatively impute estimated pollution effects of the Camp Fire to the 19 million people in the New York metro area who were exposed to similarly elevated levels of smoke and pollution from the Canadian wildfires, a back-of-the-envelope calculation suggests affected households incurred an incremental $6 billion in credit card spending and an added $10 billion to credit card debt.

In this instance, like many others, wildfire related air pollution caused significant financial stress. Recognizing and quantifying this stress allows for more pointed recovery spending for all victims, not just those in the immediate burn zone.

About the authors

Xudong An is a vice president at the Federal Reserve Bank of Philadelphia.

Stuart A. Gabriel is a professor of finance at the UCLA Anderson School of Management.

Nitzan Tzur-Ilan is a senior research economist in the Research Department at the Federal Reserve Bank of Dallas.