Home insurance premiums influence mortgage delinquencies, relocations

Rising homeowners insurance premiums are compounding the financial burden of households across the country that are struggling with mounting housing costs.

When insurance premiums rise, homeowners have limited ways to respond. They can shop for cheaper coverage by switching insurers. Some people relocate to areas where insurance is less expensive. However, income-constrained households may be less likely to shop for lower-cost insurance and may find moving out of reach.

Instead, higher premiums can lead to greater reliance on credit cards, delayed mortgage payments and potential home loss. Because mortgages constitute a substantial share of household debt and bank assets, rising delinquencies can threaten broader financial stability.

On one hand, rapidly rising insurance premiums can lead to geographic sorting. Those who can afford to relocate do so to safer areas less prone to catastrophic claims. On the other hand, higher insurance costs may also increase delinquencies among homeowners, creating mortgage losses for those holding the notes.

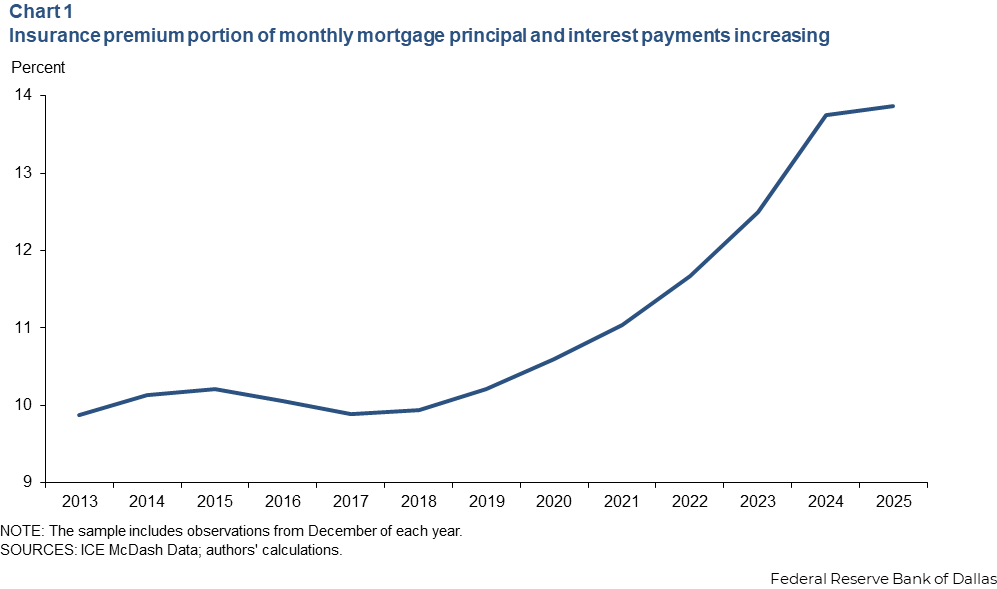

Insurance share of monthly payments grows

Insurance premiums nationally rose about 70 percent from 2019 to 2025, reflecting greater climate disaster risk and higher construction costs. We explore the insurance share of monthly mortgage payments, using recently available data from ICE McDash, a source of mortgage performance information. ICE McDash captures actual homeowner insurance payments for mortgagees, covering roughly two-thirds of the U.S. mortgage market.

For the average homeowner, the insurance premium represented 14 percent of the monthly payment that includes mortgage principal and interest in 2025 (Chart 1). That share compares with 10 percent in 2013, indicating that for many households over time, insurance has become a more substantial component of the monthly mortgage payment.

Higher insurance can trigger relocation, financial distress

In recent research, using detailed mortgage-level ICE McDash data covering 2015 to 2023, we study how rising homeowners insurance premiums affect household credit outcomes and relocation decisions. After linking insurance records with mortgage performance, credit reports and relocation data, three key findings emerge.

First, households facing larger premium increases are more likely than other households to relocate to areas with lower insurance premiums. When premiums rise sharply, moving becomes part of a broader adaptation strategy. We find that a $1,000 increase in insurance premium rates corresponds to a 0.54-percentage-point increase in relocation probability. The present value of the movers’ premium savings amounts to around $14,274 over 30 years (assuming a 6 percent discount rate).

Second, for households that cannot adjust by moving or switching insurers, higher premiums lead to meaningful financial distress. Increases in annual insurance premiums raise the likelihood of falling behind and becoming delinquent on mortgage payments. We estimate that premium increases pushed roughly 31,000 mortgages into delinquency in 2022.

Looking ahead, our projections suggest that continued increases in premiums could lead to an additional 203,000 mortgages per year falling into delinquency between 2025 and 2055. The calculation is based on an insurance premium projection by First Street Foundation, which specializes in modeling climate risk. The analysis estimates premiums will rise 29.4 percent by 2055 on average in the U.S.

The effects of the increase in homeowners insurance extend beyond mortgages, leading to higher credit card utilization and larger balances, indicative of greater reliance on credit cards to manage expenses.

Third, these effects are unequally distributed. Financially constrained households—those with lower credit scores—are much more likely to experience mortgage delinquency following premium increases, while financially secure households are more likely to respond by switching insurers or relocating. Over time, this dynamic may reshape communities, concentrating lower-income households in areas with higher climate risk and rising insurance costs, while more affluent households move away.

Implications of broad-based risk appear

Taken together, these findings highlight a new channel through which climate change affects both households and the financial system. The rise in mortgage delinquencies driven by higher insurance premiums has consequences extending beyond individual households to the broader economy. We find that the effect of rising insurance premiums is widespread across the mortgage market with delinquencies present among both government-sponsored and nongovernment-sponsored mortgages.

When delinquencies increase, they can strain mortgage markets and raise losses for lenders and government-backed or private entities that insure or guarantee home loans.

As policymakers debate how to address insurance affordability through regulatory reform, this research underscores the importance of affordability. The rise in insurance premiums is not just a pricing issue; it is a growing source of financial stress, inequality and geographic sorting. The increase may quietly reshape who can afford to leave, who is forced to stay, and who ultimately owns homes in communities with high climate risk.

Research analyst Rachel A. Jones assisted with this article.

About the authors

Shan Ge is an assistant professor of finance at New York University Stern School of Business.

Stephanie Johnson is an assistant professor of finance at the Jones School of Business, Rice University.

Nitzan Tzur-Ilan is a senior research economist in the Research Department at the Federal Reserve Bank of Dallas.