Agricultural Survey

Third Quarter 2019

Survey Highlights

Bankers responding to the third-quarter survey reported overall weaker conditions across most regions of the Eleventh District. They noted that poor rainfall in the quarter contributed to extremely dry conditions, affecting crop yields, particularly corn, cotton and wheat. Prices continued to be weak.

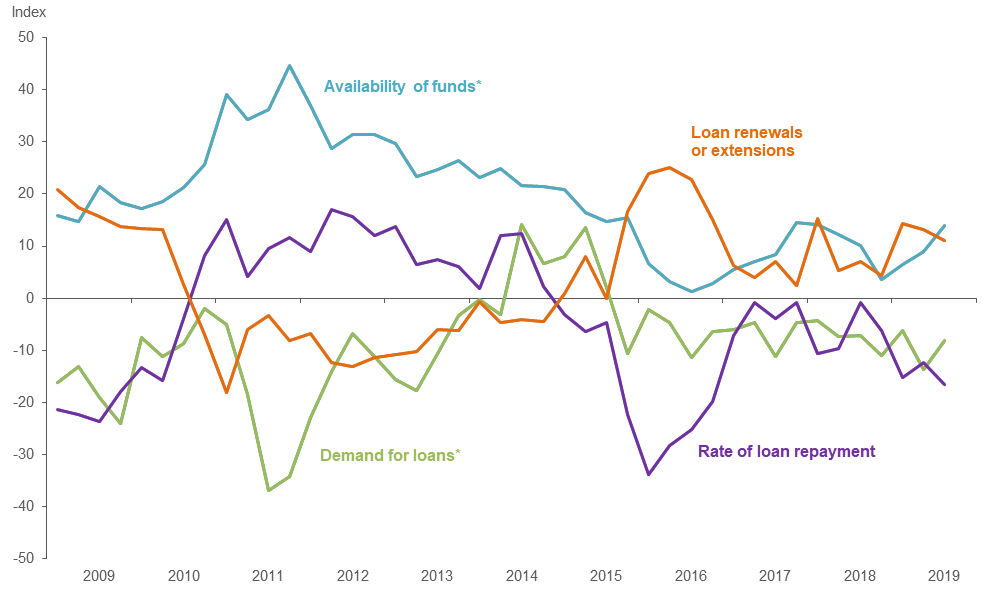

Demand for agricultural loans continued to decline, with the loan demand index registering its 16th consecutive quarter in negative territory. Loan renewals and extensions continued to increase, and the rate of loan repayment declined to its lowest level since the end of 2016. With the exception of operating loans, which were mostly flat, loan volume fell across all major categories compared with a year ago (Figure 1).

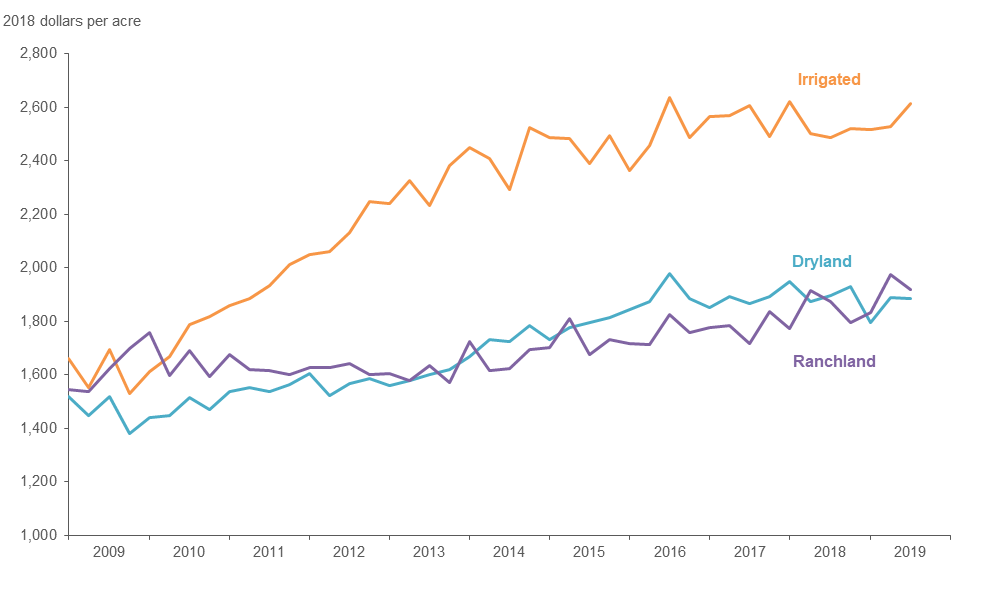

District irrigated cropland values picked up notably this quarter, while dryland values were stable and ranchland values declined moderately (Figure 2). According to bankers who responded in both this quarter and third quarter 2018, nominal cropland and ranchland values increased year over year in Texas, northern Louisiana and southern New Mexico (Table 1).

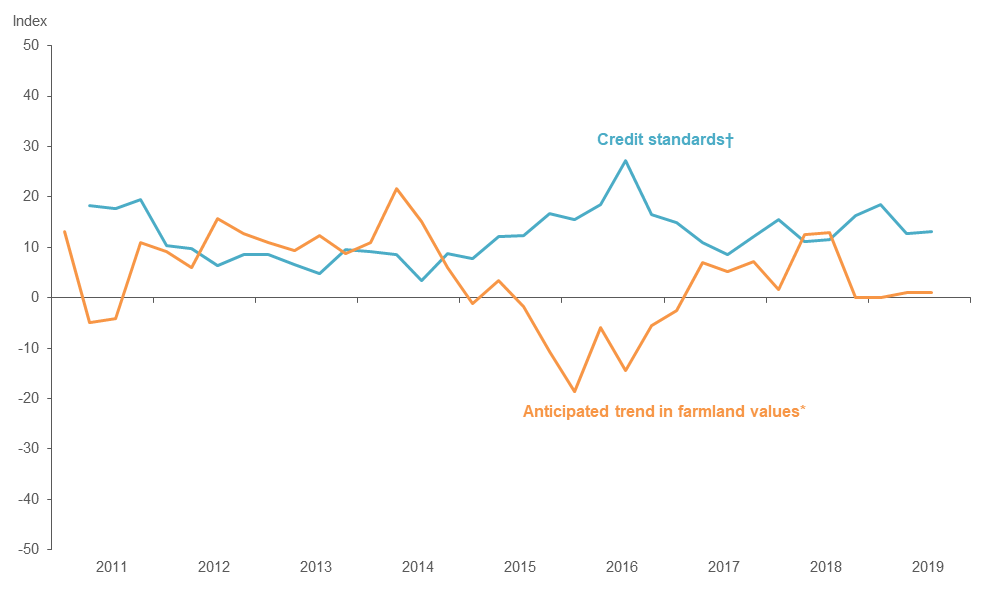

The anticipated trend in farmland values index was flat for a fourth consecutive quarter, suggesting respondents expect farmland values to hold steady. The credit standards index held steady at an elevated level, indicating further tightening of standards on net (Figure 4).

Quarterly Comments

District bankers were asked for additional comments concerning agricultural land values and credit conditions. These comments have been edited for publication.

Region 1—Northern High Plains

- Commodity prices are low, and it has been very dry. Some of the farmers did not contract early, so this could affect their ability to repay their loans in full.

- After struggling with getting fall crops planted due to cool, wet conditions, it has now turned hot and dry, resulting in difficult farming conditions for this current crop. Yields will be down, and costs will be up. Commodity price slides in corn, wheat, cotton and cattle will negatively affect equities and cash flow in late 2019 and early 2020. As a result, agricultural producers are suffering in our area. Capital expenditures for equipment will remain down.

- Commodity prices on cattle, corn, wheat and cotton have been extremely volatile. However, we believe some farmers will have an above-average year because of the recently announced Market Facilitation Program (MFP) payments by the United States Department of Agriculture (USDA). On the other hand, cattlemen will be hit much harder, probably resulting in a considerable erosion of equity showing up during renewals this fall and winter.

Region 2—Southern High Plains

- We only had about three sales in the last three quarters.

- All commodities are struggling at this time. Trade uncertainty has greatly weighed on commodity markets. Input costs remain high; drought conditions are going to affect yields. Many borrowers would not be able to repay operating loans without the MFP. It will be extremely difficult to project profit for next year if the markets do not rebound.

- Extreme heat and drought since mid-June have taken their toll on Southern Plains crops. Irrigated cotton is pretty good, having benefited from a good subsoil moisture profile, but the dryland crop will be very disappointing. Prices for all crops have tanked. On a brighter note, the 2019 MFP will benefit producers, especially dryland cotton growers.

Region 3—Northern Low Plains

- Politics continue to compound the agriculture market’s problems; prospects for the future look very dismal.

Region 4—Southern Low Plains

- We believe most farmers are still supportive of the current administration and bringing trade into balance. How long will that last? That is the question. Extreme weather conditions have also played a huge role in decreasing profitability as costs continue to rise.

- Flash drought has hurt crops, and yields are expected to be poor. Pasture conditions are fair to poor. Tank water is low, and cattle prices are unstable. However, MFP will cover most of the cash flow shortfall, but for next year, the cash flow looks dreadful. Average yields have dropped so low that multiple-peril crop insurance (MPCI) guarantees are below production cost.

Region 5—Cross Timbers

- Early spring rains gave way to hot, dry conditions in July, August and into September. We need some rain to finish up most crops before harvest. Cattle markets have taken a dive after a fire at the [Kansas] processing plant.

Region 6—North Central Texas

- Low commodity prices and poor rainfall in the summer continue to stress local farmers.

- Crop prices are too low! Pastures are burning up.

- The overall agricultural environment in Hunt County remains stressed due to continued adverse weather conditions and overall weak agricultural market conditions.

Region 7—East Texas

- In the past three months, the area went from wet conditions to virtual drought. Corn harvest is complete, with production from 45 bushels to 150 bushels on dryland. The cotton crop looks good but is in various stages of growth. The southern area of Brazos River farmland cotton is being defoliated and harvested, while only 50 miles to the north, it is still being irrigated. Pastures are extremely dry, but most still have adequate grass. We are in dire need of cool, wet weather.

- Values of ranchland in the area have increased, possibly due to the migration of urban buyers.

Region 8—Central Texas

- We still have good demand and pricing on small rural land tracts, less than 50 acres, with larger land purchases being less prevalent at this time. A drop in interest rates has caused some banks to offer lower-than-normal loan rates to keep current borrowers from going to other banks. Land loan rates have become especially competitive between community banks and larger banking operations. Dry conditions continue to hamper cattle people, with farmers finishing up the corn harvest and the harvesting of cotton to begin in several areas. Initial pecan crop estimates are pretty bleak at this time, with most trees showing no signs of having pecans. There are no winter crops going in at this time, as ranchers are waiting on moisture to plant winter grasses.

- After a cool and wet spring and early summer, the rains have vanished, and the temperature has risen. Conditions are very dry at present with only spotty rainfall. Cattle prices are off, and hay prices are rising.

Region 11—Trans-Pecos and Edwards Plateau

- What started out as a wetter-than-usual summer turned to normal—hot and dry. Cattle prices have fallen a bit during the summer but are still in good shape. Sheep, goats, wool and mohair remain strong, even as the predator problem continues to trouble most producers in the area. Overall, nothing would be better for this area than two or three good, soaking rains in the next month.

- The cattle market continues its downward trend.

- Livestock losses in the area due to anthrax will have an impact on area producers’ livestock sales revenues, as well as potentially lower revenues from future hunting leases due to a significant loss of deer. Pastures generally have good stands of old, dry grass, with a severe need for widespread rain. Livestock is generally in good condition, with the sheep and goat markets being moderate though somewhat erratic, with the cattle markets having seen a significant negative pullback due to the Kansas cattle processing-plant fire. Hunting income remains a significant revenue source for most of our area producers. Our main land sales are for recreational purposes, though there have been some larger ranch sales due to heirs of longtime ranching families not being interested in continuing to own the land.

Region 12—Southern New Mexico

- Recent dry weather has damaged ensilage corn significantly in some of our trade area. It has been too dry to plant wheat on dryland farms. Depressed livestock prices look like they may continue their downward trend, with feedlot losses and dry weather being the major contributing factors. There is limited interest in the country calf crop to date. Fall auction barn runs look like they are ramping up in volume coming to town.

Eleventh District Agricultural Data

Figures

|

Figure 1 Farm Lending Trends |

|||||

|---|---|---|---|---|---|

| What changes occurred in non-real-estate farm loans at your bank in the past three months compared with a year earlier? | |||||

| Index | Percent reporting, Q3 | ||||

| 2019:Q2 | 2019:Q3 | Greater | Same | Less | |

| Demand for loans* | -13.6 | -8.1 | 8.4 | 75.1 | 16.5 |

| Availability of funds* | 9.0 | 13.9 | 16.9 | 80.1 | 3.0 |

| Rate of loan repayment | -12.3 | -16.7 | 2.8 | 77.8 | 19.4 |

| Loan renewals or extensions | 13.2 | 11.1 | 14.8 | 81.5 | 3.7 |

| What changes occurred in the volume of farm loans made by your bank in the past three months compared with a year earlier? | |||||

| Index | Percent reporting, Q3 | ||||

| 2019:Q2 | 2019:Q3 | Greater | Same | Less | |

| Non-real-estate farm loans | -8.9 | -10.4 | 8.5 | 72.6 | 18.9 |

| Feeder cattle loans* | -11.0 | -23.7 | 3.5 | 69.3 | 27.2 |

| Dairy loans* | -5.9 | -21.0 | 1.9 | 75.2 | 22.9 |

| Crop storage loans* | -5.7 | -15.9 | 4.4 | 75.3 | 20.3 |

| Operating loans | 2.7 | 1.0 | 15.5 | 69.9 | 14.6 |

| Farm machinery loans* | -10.8 | -22.4 | 4.8 | 68.0 | 27.2 |

| Farm real estate loans* | -5.1 | -10.5 | 8.4 | 72.7 | 18.9 |

| *Seasonally adjusted. NOTES: Survey responses are used to calculate an index for each item by subtracting the percentage of bankers reporting less from the percentage reporting greater. Positive index readings generally indicate an increase, while negative index readings generally indicate a decrease. |

|||||

| Figure 2 Real Land Values |

|---|

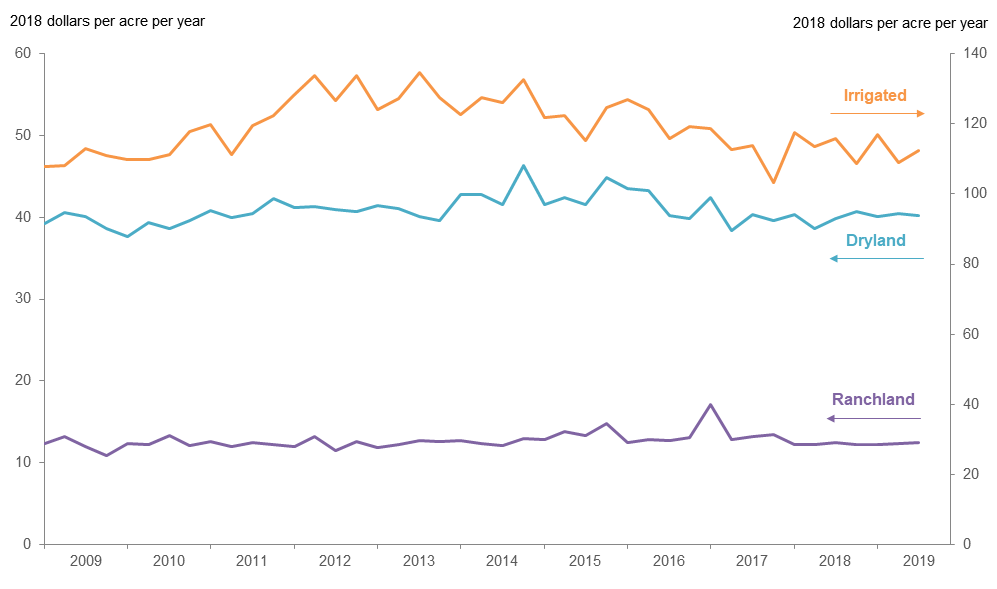

| Figure 3 Real Cash Rents |

|---|

NOTES: All values have been seasonally adjusted. Real values are created by deflating the nominal values using the implicit price deflator for U.S. gross domestic product.

|

Figure 4 Anticipated Farmland Values and Credit Standards |

|||||

|---|---|---|---|---|---|

| What trend in farmland values do you expect in your area in the next three months? | |||||

| Index | Percent reporting, Q3 | ||||

| Anticipated trend in farmland values* | 2019:Q2 | 2019:Q3 | Up | Stable | Down |

| 1.1 | 1.0 | 7.5 | 86.0 | 6.5 | |

| What change occurred in credit standards for agricultural loans at your bank in the past three months compared with a year earlier?† | |||||

| Credit standards | 2019:Q2 | 2019:Q3 | Tightened | Same | Loosened |

| 12.7 | 13.1 | 14.0 | 85.1 | 0.9 | |

†Added to survey in second quarter 2011.

NOTES: Survey responses are used to calculate an index for each item by subtracting the percentage of bankers reporting less from the percentage reporting greater. Positive index readings generally indicate an increase, while negative index readings generally indicate a decrease.

Tables

Tables | ||||

| Table 1 Rural Real Estate Values—Third Quarter 2019 |

||||

|---|---|---|---|---|

| Banks1 | Average value2 | Percent change in value from previous year3 | ||

| Cropland—Dryland | ||||

| District* | 88 | 1,923 | 1.9 | |

| Texas* | 78 | 1,926 | 1.0 | |

| 1 | Northern High Plains | 9 | 947 | 3.7 |

| 2 | Southern High Plains | 10 | 875 | 18.1 |

| 3 | Northern Low Plains* | 4 | 797 | 1.5 |

| 4 | Southern Low Plains* | 8 | 1,106 | -3.9 |

| 5 | Cross Timbers | 7 | 1,964 | 12.7 |

| 6 | North Central Texas | 14 | 3,129 | 7.3 |

| 7 | East Texas* | 6 | 2,923 | 6.5 |

| 8 | Central Texas | 9 | 3,911 | 3.1 |

| 9 | Coastal Texas | n.a. | n.a. | n.a. |

| 10 | South Texas | n.a. | n.a. | n.a. |

| 11 | Trans-Pecos and Edwards Plateau | 7 | 2,471 | 5.1 |

| 12 | Southern New Mexico | 4 | 581 | 54.9 |

| 13 | Northern Louisiana | 6 | 3,042 | 10.9 |

| Cropland—Irrigated | ||||

| District* | 65 | 2,667 | 7.7 | |

| Texas* | 53 | 2,333 | 9.6 | |

| 1 | Northern High Plains | 9 | 2,247 | 10.0 |

| 2 | Southern High Plains | 10 | 1,690 | 16.4 |

| 3 | Northern Low Plains* | n.a. | n.a. | n.a. |

| 4 | Southern Low Plains | 4 | 1,500 | 8.1 |

| 5 | Cross Timbers | 5 | 2,640 | 3.7 |

| 6 | North Central Texas | 6 | 3,592 | 15.1 |

| 7 | East Texas | 4 | 3,100 | 6.4 |

| 8 | Central Texas | 5 | 4,240 | 4.4 |

| 9 | Coastal Texas | n.a. | n.a. | n.a. |

| 10 | South Texas | n.a. | n.a. | n.a. |

| 11 | Trans-Pecos and Edwards Plateau | 5 | 3,870 | 6.0 |

| 12 | Southern New Mexico | 6 | 4,333 | 1.8 |

| 13 | Northern Louisiana | 6 | 4,275 | 4.5 |

| Ranchland | ||||

| District* | 94 | 1,957 | 3.0 | |

| Texas* | 84 | 2,329 | 2.7 | |

| 1 | Northern High Plains | 9 | 706 | 8.8 |

| 2 | Southern High Plains | 8 | 888 | 6.1 |

| 3 | Northern Low Plains | 4 | 750 | 0.0 |

| 4 | Southern Low Plains* | 7 | 1,182 | 0.0 |

| 5 | Cross Timbers | 9 | 2,189 | 13.9 |

| 6 | North Central Texas | 14 | 3,214 | 11.9 |

| 7 | East Texas | 8 | 3,000 | 9.8 |

| 8 | Central Texas | 10 | 6,330 | -2.3 |

| 9 | Coastal Texas | n.a. | n.a. | n.a. |

| 10 | South Texas | n.a. | n.a. | n.a. |

| 11 | Trans-Pecos and Edwards Plateau | 11 | 2,277 | 2.4 |

| 12 | Southern New Mexico | 5 | 350 | 12.9 |

| 13 | Northern Louisiana | 5 | 2,130 | 4.9 |

| *Seasonally adjusted. 1 Number of banks reporting land values. 2 Prices are dollars per acre, not adjusted for inflation. 3 Not adjusted for inflation and calculated using responses only from those banks reporting in both the past and current quarter. |

||||

| Table 2 Interest Rates by Loan Type |

|||||

|---|---|---|---|---|---|

| Feeder cattle | Other farm operating | Intermediate term | Long-term farm real estate | ||

| Fixed (average rate, percent) | |||||

| 2018:Q3 | 6.74 | 6.84 | 6.64 | 6.36 | |

| Q4 | 6.88 | 6.95 | 6.78 | 6.58 | |

| 2019:Q1 | 7.01 | 7.11 | 6.88 | 6.58 | |

| Q2 | 7.02 | 7.11 | 6.83 | 6.40 | |

| Q3 | 6.90 | 6.89 | 6.71 | 6.42 | |

| Variable (average rate, percent) | |||||

| 2018:Q3 | 6.48 | 6.48 | 6.43 | 6.02 | |

| Q4 | 6.70 | 6.69 | 6.66 | 6.26 | |

| 2019:Q1 | 6.81 | 6.83 | 6.75 | 6.44 | |

| Q2 | 6.84 | 6.85 | 6.80 | 6.42 | |

| Q3 | 6.58 | 6.59 | 6.50 | 6.21 | |

Back issues of Agricultural Survey »

For More Information

Questions regarding the Agricultural Survey can be addressed to Christopher Slijk at christopher.slijk@dal.frb.org.