Dallas Fed Energy Survey Q1 2026 update

|

In response to recent developments in the global oil market, we conducted a follow-up to the first quarter survey that published March 25. | See the original first quarter survey results. |

Special questions

Data were collected April 15–20; 120 oil and gas firms responded. Of the respondents, 78 were exploration and production firms, and 42 were oilfield services firms.

All firms

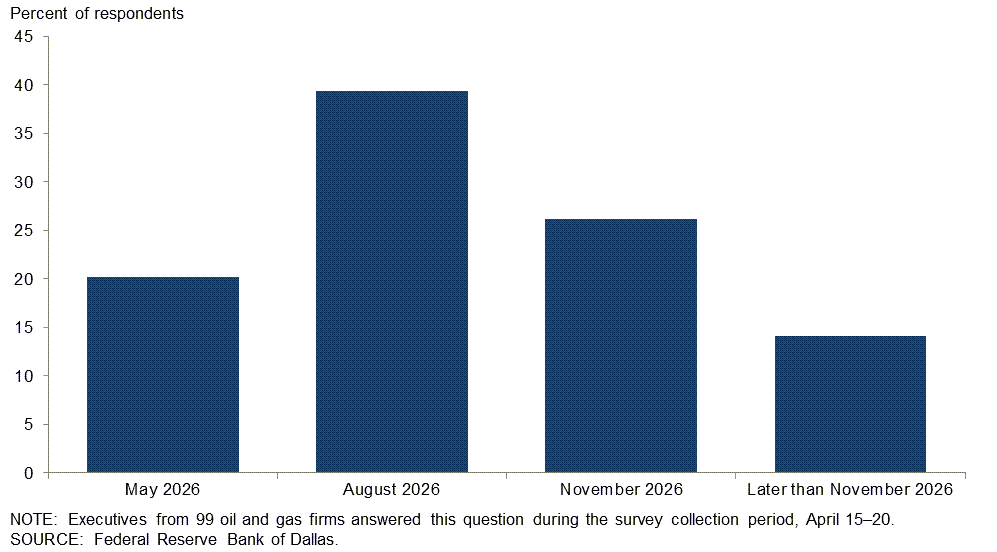

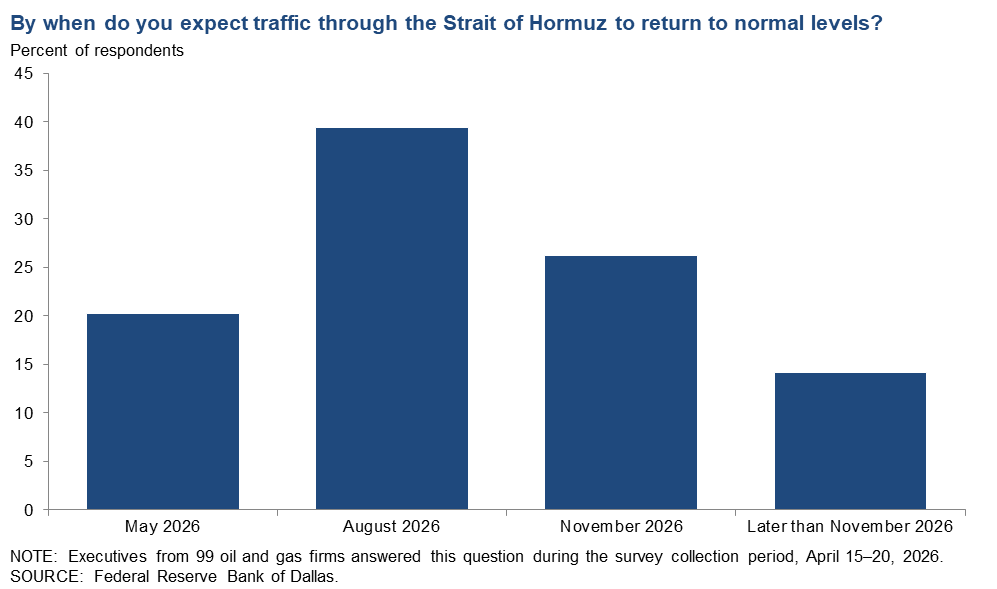

By when do you expect traffic through the Strait of Hormuz to return to normal levels?

Executives expect traffic through the Strait of Hormuz to eventually normalize, although most believe it will take time. Of the executives surveyed, 20 percent expect traffic through the Strait of Hormuz to return to normal levels by May 2026, 39 percent expect recovery by August 2026, 26 percent by November 2026, and 14 percent later than that.

{kind=link}

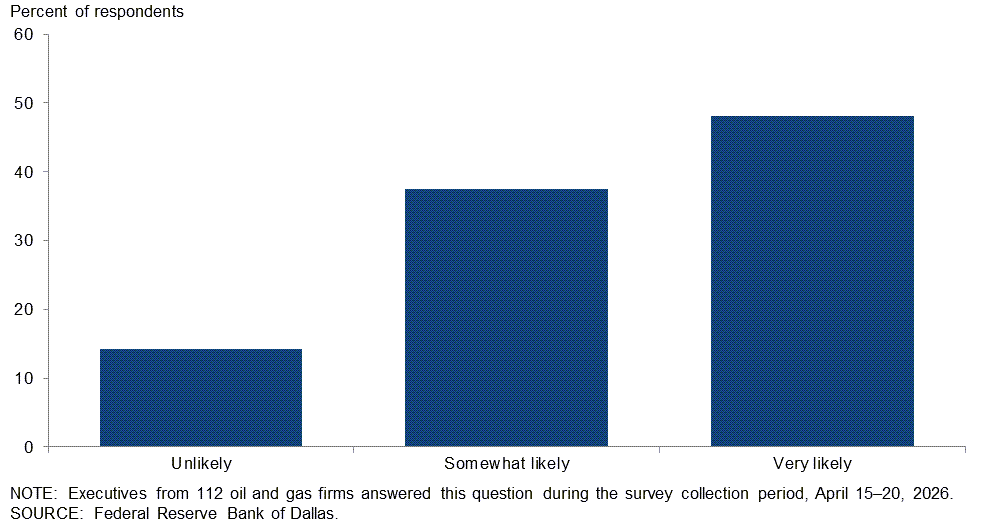

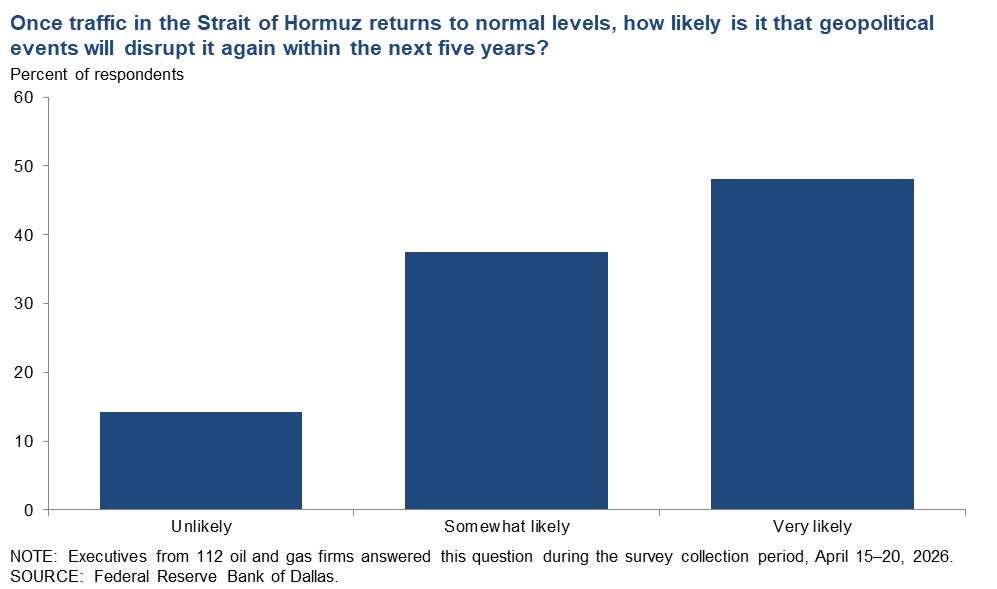

Once traffic in the Strait of Hormuz returns to normal levels, how likely is it that geopolitical events will disrupt it again within the next five years?

A majority of executives say future disruptions to the Strait of Hormuz are likely. Of respondents, 48 percent say it is “very likely” that geopolitical events will disrupt traffic again within the next five years, while 38 percent view it as “somewhat likely.” Only 14 percent of executives consider future disruptions “unlikely.”

{kind=link}

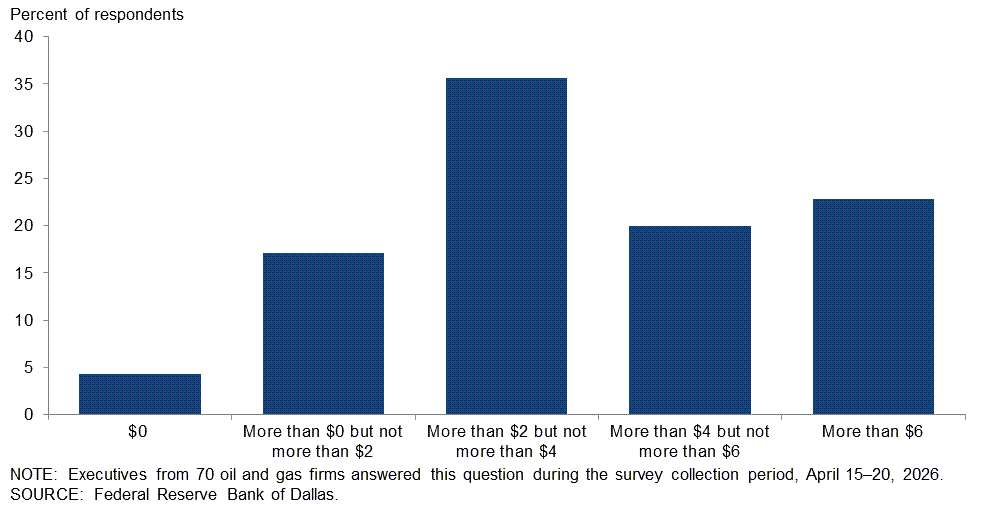

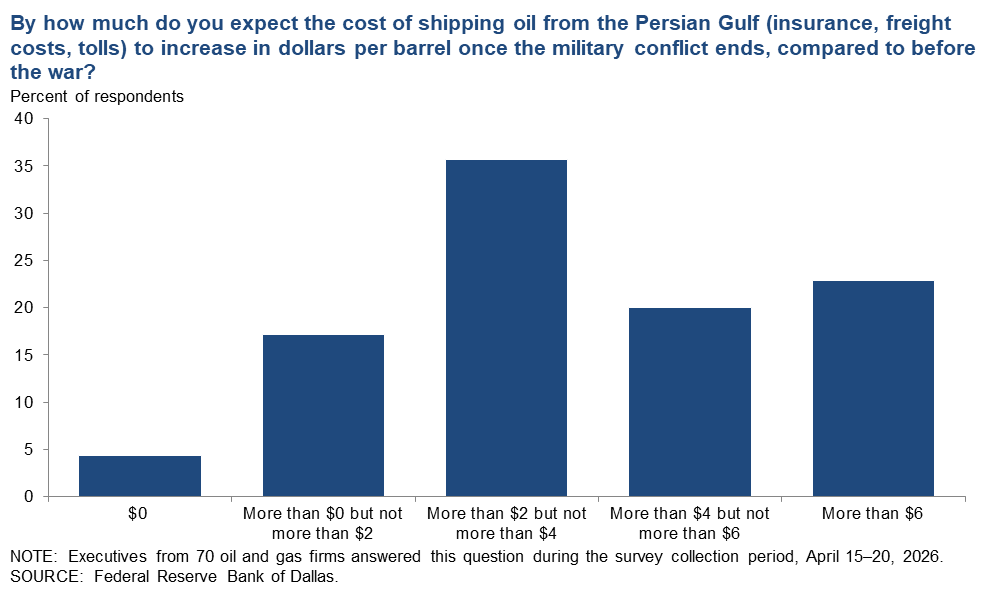

By how much do you expect the cost of shipping oil from the Persian Gulf (insurance, freight costs, tolls) to increase in dollars per barrel once the military conflict ends, compared to before the war?

Most executives expect shipping costs from the Persian Gulf to increase after the military conflict ends. The most selected response in dollars per barrel was “more than $2 but not more than $4” (36 percent of respondents).

{kind=link}

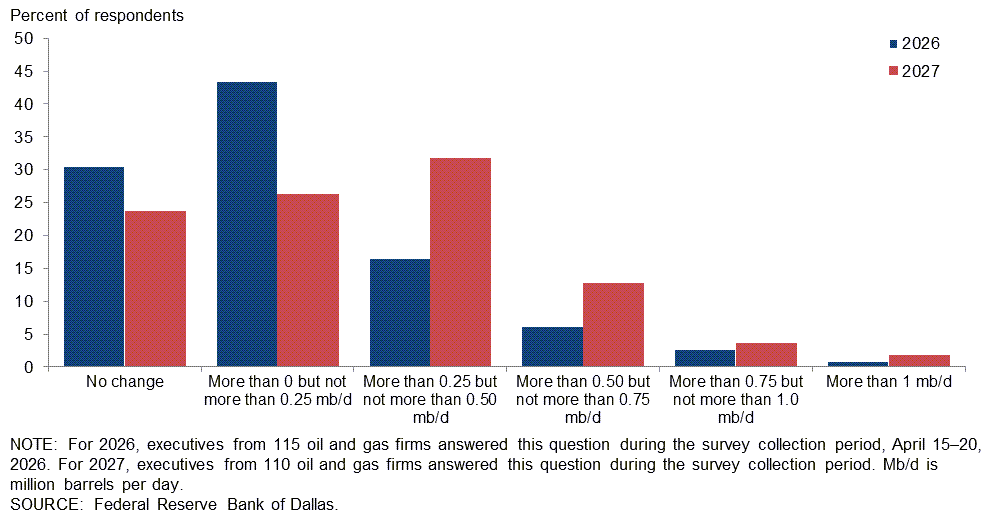

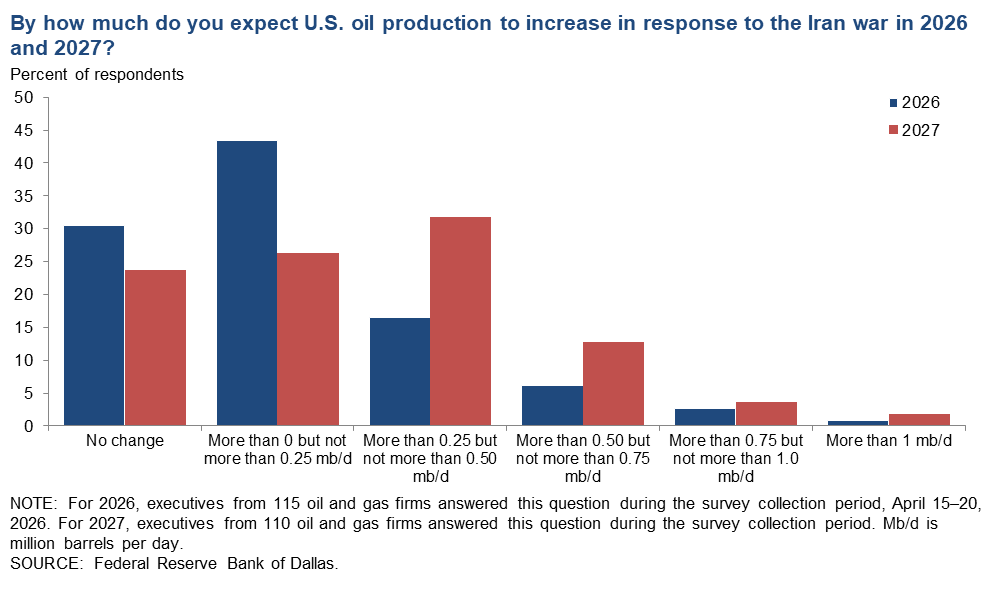

By how much do you expect U.S. oil production to increase in response to the Iran war in 2026 and 2027?

Most executives expect U.S. oil production to increase in response to the Iran war. The most selected response for 2026 was “more than 0 but not more than 0.25 mb/d,” selected by 43 percent of the respondents. The most selected response for 2027 was “more than 0.25 but not more than 0.50 mb/d,” selected by 32 percent of the respondents.

{kind=link}

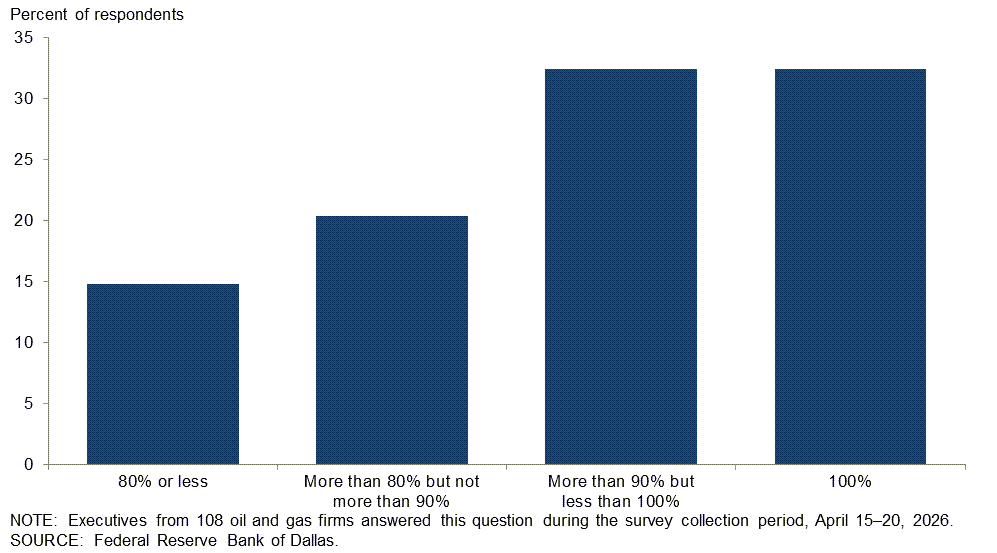

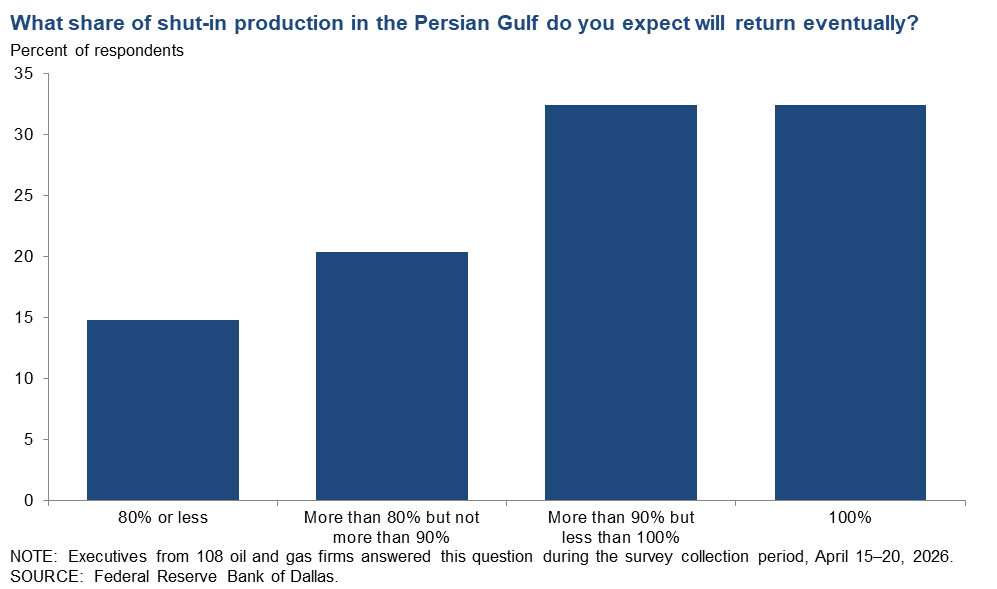

What share of shut-in production in the Persian Gulf do you expect will return eventually?

About two-thirds of respondents think at least 90 percent of shut-in production in the Persian Gulf will return to market eventually.

{kind=link}

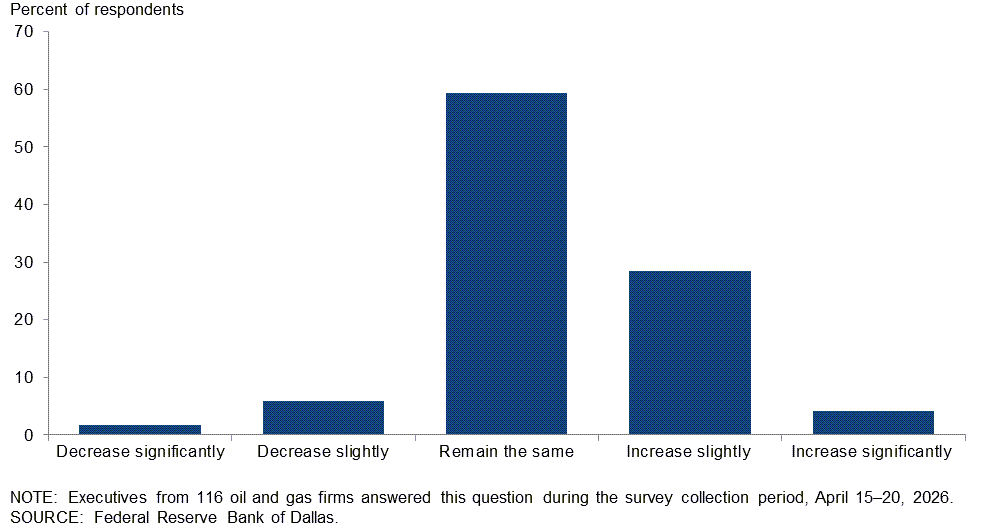

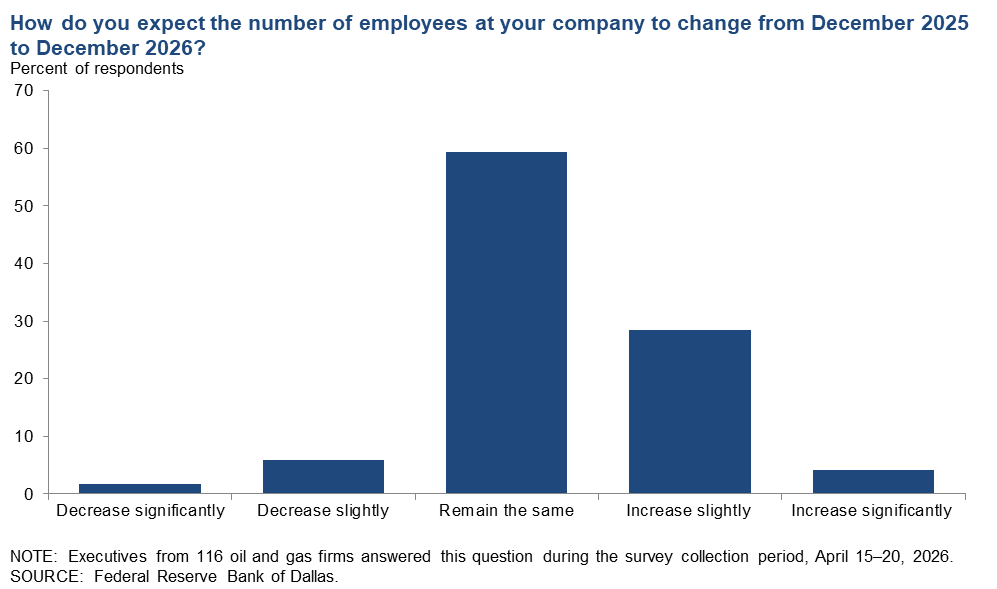

How do you expect the number of employees at your company to change from December 2025 to December 2026?

The largest group, 59 percent of executives, expect employment at their firms to remain the same from December 2025 to December 2026. About a third of respondents expect employment to increase to some degree and only 8 percent expect a decline.

Whereas the most-selected response among E&P firms was for employment to “remain the same” in 2026, the most-selected response of support service firms was for employment to “increase slightly” in 2026.

{kind=link}

| Response | Percent of respondents | ||

| All firms | E&P | Services | |

| Increase significantly | 4 | 1 | 10 |

| Increase slightly | 28 | 17 | 49 |

| Remain the same | 59 | 73 | 34 |

| Decrease slightly | 6 | 5 | 7 |

| Decrease significantly | 2 | 3 | 0 |

| NOTE: Executives from 75 exploration and production firms and 41 oil and gas support services firms answered this question during the survey collection period, April 15–20. The “all” column reports the percentage out of the total 116 responses. Percentages may not sum to 100 due to rounding. SOURCE: Federal Reserve Bank of Dallas. |

|||

Comments »

Comments from survey update respondents

Survey participants are given the opportunity to submit comments on any special questions or on any current issues that may be affecting their businesses. Some comments have been edited for grammar and clarity.

Exploration and production (E&P) firms

- Extreme oil price volatility is leaving both small and large E&Ps unsure of whether to increase capital spending and activity. Even after nearly a month of oil above $90 per barrel, rig counts declined, signaling little confidence that prices will hold. Closing the supply gap from the Iran conflict will require greater certainty and higher 2027 future prices to incentivize additional rig and frack deployments. This is also keeping supply chain inflation in the industry under check.

- With all of the chaos, predicting anything in the energy sector is very difficult.

- There are way too many variables for these predictions to have real value.

- The Iranian conflict has become too much about energy. This is a knock-off effect. If the administration feels that we need to prolong the conflict, it needs to better articulate the long-term strategic goal and the risk of inaction. This cannot be solely about barrels.

- The difference between the gyration of paper market oil prices versus what seems to be substantially higher physical prices sends conflicting signals to operators who cannot plan rigs and capital budgets when prices swing wildly based on tweets. Our hypothesis is [that] the paper market is being manipulated. This will likely lead to an even worse supply and demand imbalance and higher prices in the medium term (next 12 months).

- As we know, there is no way to predict the outcome of the war with Iran. The effect it will have on domestic oil production depends on how long the strait remains closed, and that is how long Iran can control the movement through the strait.

- Shut-in production in the Persian Gulf will eventually rise above pre-war levels, but it will take time. This is not a quick return to production.

- The price of oil will fall back to the $65-per-barrel level very quickly once this conflict settles down.

- It’s too early to tell for most things. The administration’s comment about an “Iran terror premium” existing for decades with crude oil pricing is laughable. But now the administration has created one where it did not exist before.

- The geopolitical events are too chaotic to provide any degree of certainty to commodity pricing or unimpeded transportation through the Strait of Hormuz at this time. I am of the opinion that the costs related to shipping oil from the Persian Gulf will increase, but by how much I am not sure. I am not optimistic that the Iran conflict will cease in the near future. Locating or removing (or rendering unusable) the uranium materials and processing facilities will continue to be a top priority of this administration.

- All answers depend on how the conflict ends. Does it end with Iran hard-liners in control, or will there be a move toward democracy? I’m betting the new regime will be a repeat of the old one, unless things change drastically in where we are headed at present.

- My career has had me visiting Tehran and working in Qatar, Kuwait, Iraq and Syria over the years. The political issues between cultures are entrenched and solutions to the current disruptions will not occur overnight. These are interesting times. Answering these questions is not easy.

- Disruption of the oil markets due to the Iran war? The reality of those markets being unbalanced due to disruptions of oil deliveries was an overreaction. At same time, the uncertainty of the Gulf states and Iran is a reality. I believe the fear of oil disruptions will persist for some time.

- We do not hedge our oil production. There are domestic basins (like Magellan East Houston on the Texas Gulf Coast) that are seeing premiums relative to prewar, and that is also affecting our revenue.

- Supply and demand per market are ultimately dependent on every market's secure deliverability assessment for pricing and preference. That will, in every market that is dependent on export by sea now, put a highly variable pricing and preference component in each of such market's supply and demand pricing components, and that variable will logically even add additional pricing components that have not been of material or obvious influence or consideration until recently.

- The recent events are temporary.

- Some of the questions are open-ended as to time factor. A Republican president elected in 2028 with control of both houses of Congress is a big difference in foreign affairs verses a Democrat president and one of the houses of Congress being held by Democrats.

Oil and gas support services firms

- Middle East oil contribution as a percentage will decrease and will be offset by U.S./Latin America/Africa, as the risk premium to operate in Middle East will increase, hence capital should flow to other geographies

- Uncertainty is problematic in the oil and gas business, and this administration is the definition of uncertainty. I expect to see material demand destruction come over the longer term as many societies will come to see hydrocarbons as no longer a certainty in a future of increased energy requirement.

- The long-term consequences of this war were not fully considered. The disruption this will cause to energy markets and other macroeconomic measures will be significant. The unpredictable nature of the current administration makes business modeling near impossible.

- In response to the roughly 45 days of West Texas Intermediate over $75 per barrel, we are hearing increased talk of smaller operators adding rigs. We are also seeing larger independent operators move up drilling schedules. We don't have a clear idea of what Persian Gulf production levels will look like when the strait re-opens, but we don't expect an immediate ramp-up to previous (to closure) levels on account of the infrastructure damage during the bombing campaign. We are roughly estimating that when the strait reopens, we'll be working with a $70-$80 per barrel floor for WTI in the near future.

- Within the oilfield services sector, the low-cost environment is starting to put companies out. We are having founders approach us to take them over. The balance sheet is drained, and the pathway to make money for immature firms with low capital reserves is difficult. Manpower and machinery are depleting within the industry. Realized prices will have to rise significantly with longer-term positive prospects for widespread investment to pick up.

- The disconnect between spot prices and midstream feasibility is widening. Extended lead times for pipeline products and significantly increased transportation costs, both exacerbated by the shipping crisis in Hormuz, have turned our 12-month projections into logistical jigsaw puzzles. The extended shipping blocks are effectively an unlegislated tariff on our infrastructure, forcing us to choose between paying a premium for domestic supply or waiting indefinitely for increasingly expensive global shipments.

Questions regarding the Dallas Fed Energy Survey can be addressed to Michael Plante at Michael.Plante@dal.frb.org or Kunal Patel at Kunal.Patel@dal.frb.org.

Sign up for our email alert to be automatically notified as soon as the latest Dallas Fed Energy Survey is released on the web. For additional energy-related academic research and market analysis, please visit the Dallas Fed’s Center for Energy and the Economy.