Texas Service Sector Growth Strengthens in June

Texas Service Sector Outlook Survey

Texas Service Sector Growth Strengthens in June

For this month’s survey, Texas business executives were asked supplemental questions on wages, prices and revenue restraints. Results for these questions from the Texas Manufacturing Outlook Survey, Texas Service Sector Outlook Survey and Texas Retail Outlook Survey have been released together. Read the special questions results.

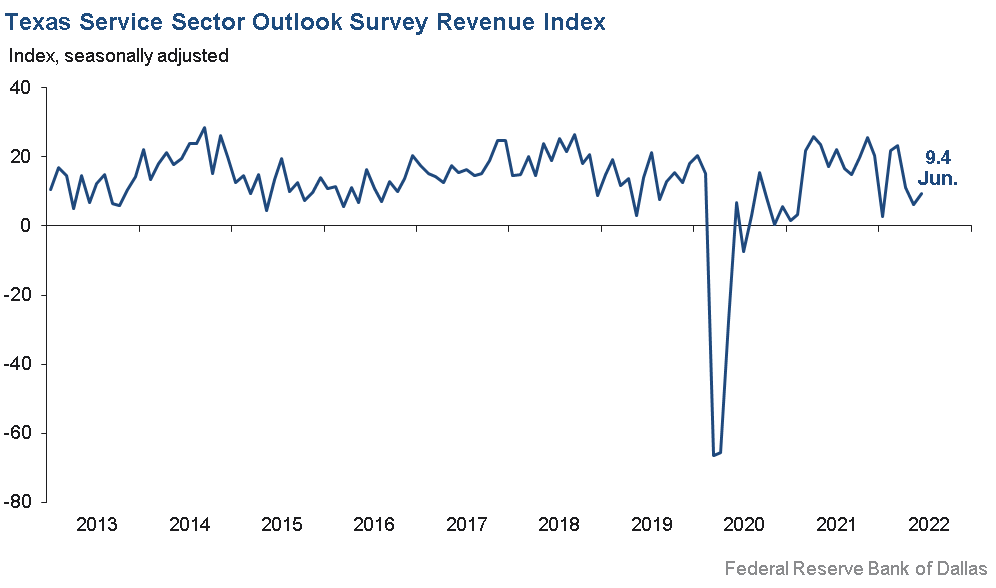

Activity in the Texas service sector picked up modestly in June, according to business executives responding to the Texas Service Sector Outlook Survey. The revenue index, a key measure of state service sector conditions, rose from 6.3 in May to 9.4 in June, as the share of firms reporting increasing revenues grew to 31 percent.

Labor market indicators continued to suggest steady growth in employment and hours worked compared with May. The employment index was roughly unchanged at 7.6, although the part-time employment index dipped one point to 1.9—its lowest reading since early 2021. The hours worked index was flat at 4.9, with about 10 percent of firms increasing employee hours compared with 5 percent cutting hours.

Perceptions of broader business conditions plunged in June, as firms noted a surge in outlook uncertainty. The general business activity index plunged from 1.5 to -12.4, as the share of firms noting a worsening of activity rose from 20 percent to 27 percent. The company outlook index similarly dropped into negative territory at -14.7—its worst reading since July 2020. The outlook uncertainty index surged 16 points to 41.2, nearing its record-high level during the initial onset of COVID in April 2020.

Price and wage pressures remained near record highs in June. The selling prices index moderated three points to 29.4, while the input prices index increased by two points to 55.8. The wages and benefits index was roughly flat at 34.6, though nearly 40 percent of firms noted higher wages compared with May.

Respondents’ expectations regarding future business activity weakened further in June. The future general business activity index dropped deeply into negative territory at -24.0, while the future revenue index declined nearly 17 points to 19.0. Other future service sector activity indexes such as employment and capital expenditures declined, suggesting expectations for weaker growth over the second half of the year.

Texas Retail Outlook Survey

Texas Retail Sales Deteriorate in June

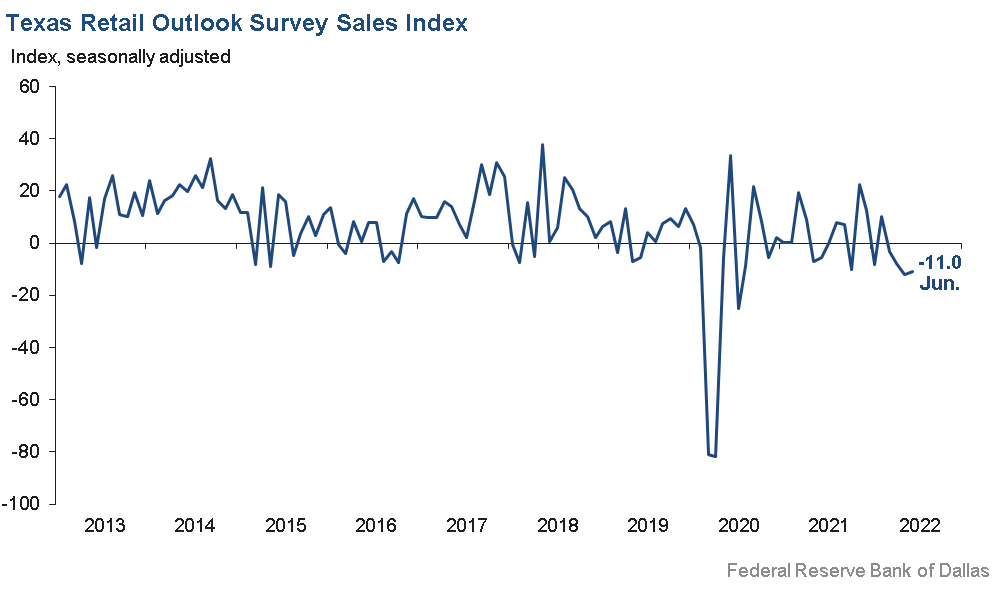

June retail sales activity continued to decline, according to business executives responding to the Texas Retail Outlook Survey. The sales index, a key measure of state retail activity, was roughly unchanged at -11.0 in June. Retailers’ inventories held mostly flat for a third consecutive month, with the inventories index reporting a near-zero reading.

Retail labor market indicators weakened in June. The employment index dipped into negative territory for the first time since July 2021, falling four points to -3.3, while the part-time employment index plunged eight points to -8.1. The hours worked index similarly declined eight points to -6.1, its weakest reading in a year.

Retailers’ perceptions of broader business conditions turned sharply pessimistic this month compared with May. The general business activity index shed 22 points to -25.2, while the company outlook index fell from -4.1 to -22.2; just 12 percent of retailers noted improved outlooks compared with 35 percent expecting worsening conditions. The outlook uncertainty index surged to 42.3, its highest reading since March 2020.

Retail price and wage pressures remained highly elevated in June. The selling prices index fell five points to 37.1, although a majority of firms continued to note they increased their selling prices over the past month. The input prices index held steady at 49.9, while the wages and benefits index was also stable at 30.4.

Expectations for future retail growth deteriorated significantly in June. The future general business activity index fell 23 points to -26.8, while the future sales index declined 17 points to 0.9. Other indexes of future retail activity also declined, suggesting lowered expectations for growth for the rest of 2022.

The Texas Retail Outlook Survey is a component of the Texas Service Sector Outlook Survey that uses information only from respondents in the retail and wholesale sectors.

Next release: July 26, 2022

Data were collected June 14–22, and 284 Texas service sector business executives, of which 55 were retailers, responded to the survey. The Dallas Fed conducts the Texas Service Sector Outlook Survey monthly to obtain a timely assessment of the state’s service sector activity. Firms are asked whether revenue, employment, prices, general business activity and other indicators increased, decreased or remained unchanged over the previous month.

Survey responses are used to calculate an index for each indicator. Each index is calculated by subtracting the percentage of respondents reporting a decrease from the percentage reporting an increase. When the share of firms reporting an increase exceeds the share reporting a decrease, the index will be greater than zero, suggesting the indicator has increased over the prior month. If the share of firms reporting a decrease exceeds the share reporting an increase, the index will be below zero, suggesting the indicator has decreased over the prior month. An index will be zero when the number of firms reporting an increase is equal to the number of firms reporting a decrease. Data have been seasonally adjusted as necessary.

Texas Service Sector Outlook Survey

Historical data are available from January 2007 to the most current release month.

| Business Indicators Relating to Facilities and Products in Texas Current (versus previous month) | ||||||||

| Indicator | Jun Index | May Index | Change | Series Average | Trend* | % Reporting Increase | % Reporting No Change | % Reporting Decrease |

Revenue | 9.4 | 6.3 | +3.1 | 11.3 | 23(+) | 30.6 | 48.2 | 21.2 |

Employment | 7.6 | 8.1 | –0.5 | 6.5 | 23(+) | 19.2 | 69.2 | 11.6 |

Part–Time Employment | 1.9 | 3.0 | –1.1 | 1.6 | 19(+) | 5.8 | 90.3 | 3.9 |

Hours Worked | 4.9 | 5.6 | –0.7 | 2.9 | 22(+) | 10.4 | 84.1 | 5.5 |

Wages and Benefits | 34.6 | 35.0 | –0.4 | 15.4 | 25(+) | 37.4 | 59.8 | 2.8 |

Input Prices | 55.8 | 53.5 | +2.3 | 26.8 | 26(+) | 58.0 | 39.8 | 2.2 |

Selling Prices | 29.4 | 32.6 | –3.2 | 6.9 | 23(+) | 34.1 | 61.2 | 4.7 |

Capital Expenditures | 12.1 | 14.7 | –2.6 | 10.0 | 22(+) | 19.4 | 73.3 | 7.3 |

| General Business Conditions Current (versus previous month) | ||||||||

| Indicator | Jun Index | May Index | Change | Series Average | Trend** | % Reporting Improved | % Reporting No Change | % Reporting Worsened |

Company Outlook | –14.7 | 0.9 | –15.6 | 5.5 | 1(–) | 12.6 | 60.1 | 27.3 |

General Business Activity | –12.4 | 1.5 | –13.9 | 4.0 | 1(–) | 14.9 | 57.8 | 27.3 |

| Indicator | Jun Index | May Index | Change | Series Average | Trend* | % Reporting Increase | % Reporting No Change | % Reporting Decrease |

Outlook Uncertainty† | 41.2 | 25.2 | +16.0 | 12.3 | 13(+) | 49.6 | 42.0 | 8.4 |

| Business Indicators Relating to Facilities and Products in Texas Future (six months ahead) | ||||||||

| Indicator | Jun Index | May Index | Change | Series Average | Trend* | % Reporting Increase | % Reporting No Change | % Reporting Decrease |

Revenue | 19.0 | 35.5 | –16.5 | 37.9 | 26(+) | 41.2 | 36.5 | 22.2 |

Employment | 23.4 | 32.9 | –9.5 | 23.0 | 26(+) | 33.3 | 56.8 | 9.9 |

Part–Time Employment | –0.3 | 8.6 | –8.9 | 7.0 | 1(–) | 7.2 | 85.3 | 7.5 |

Hours Worked | 2.8 | 8.8 | –6.0 | 6.0 | 26(+) | 9.3 | 84.2 | 6.5 |

Wages and Benefits | 50.5 | 50.5 | 0.0 | 37.0 | 26(+) | 53.5 | 43.5 | 3.0 |

Input Prices | 66.4 | 61.9 | +4.5 | 44.3 | 186(+) | 68.3 | 29.9 | 1.9 |

Selling Prices | 36.6 | 40.4 | –3.8 | 24.1 | 26(+) | 44.3 | 48.0 | 7.7 |

Capital Expenditures | 20.8 | 28.5 | –7.7 | 23.6 | 25(+) | 31.6 | 57.6 | 10.8 |

| General Business Conditions Future (six months ahead) | ||||||||

| Indicator | Jun Index | May Index | Change | Series Average | Trend** | % Reporting Improved | % Reporting No Change | % Reporting Worsened |

Company Outlook | –18.4 | 0.2 | –18.6 | 16.8 | 1(–) | 16.2 | 49.1 | 34.6 |

General Business Activity | –24.0 | –3.9 | –20.1 | 13.9 | 2(–) | 15.0 | 45.9 | 39.0 |

Historical data are available from January 2007 to the most current release month.

| Business Indicators Relating to Facilities and Products in Texas Retail (versus previous month) | ||||||||

| Indicator | Jun Index | May Index | Change | Series Average | Trend* | % Reporting Increase | % Reporting No Change | % Reporting Decrease |

| Retail Activity in Texas | ||||||||

Sales | –11.0 | –11.9 | +0.9 | 5.2 | 4(–) | 24.7 | 39.5 | 35.7 |

Employment | –3.3 | 0.8 | –4.1 | 1.9 | 1(–) | 11.3 | 74.1 | 14.6 |

Part–Time Employment | –8.1 | 0.2 | –8.3 | –1.6 | 1(–) | 2.6 | 86.7 | 10.7 |

Hours Worked | –6.1 | 1.4 | –7.5 | –1.7 | 1(–) | 6.5 | 80.9 | 12.6 |

Wages and Benefits | 30.4 | 31.1 | –0.7 | 10.8 | 23(+) | 37.9 | 54.6 | 7.5 |

Input Prices | 49.9 | 50.1 | –0.2 | 21.7 | 26(+) | 58.0 | 33.9 | 8.1 |

Selling Prices | 37.1 | 42.5 | –5.4 | 13.5 | 1(+) | 50.2 | 36.7 | 13.1 |

Capital Expenditures | 10.4 | 12.6 | –2.2 | 8.1 | 17(+) | 20.2 | 70.0 | 9.8 |

Inventories | –0.2 | –1.3 | +1.1 | 1.9 | 6(–) | 24.5 | 50.8 | 24.7 |

| Companywide Retail Activity | ||||||||

Companywide Sales | –7.8 | –12.9 | +5.1 | 6.7 | 2(–) | 26.2 | 39.8 | 34.0 |

Companywide Internet Sales | –10.4 | –18.2 | +7.8 | 5.5 | 2(–) | 10.8 | 68.0 | 21.2 |

| General Business Conditions, Retail Current (versus previous month) | ||||||||

| Indicator | Jun Index | May Index | Change | Series Average | Trend** | % Reporting Improved | % Reporting No Change | % Reporting Worsened |

Company Outlook | –22.2 | –4.1 | –18.1 | 3.3 | 4(–) | 12.3 | 53.2 | 34.5 |

General Business Activity | –25.2 | –3.2 | –22.0 | –0.2 | 2(–) | 16.1 | 42.6 | 41.3 |

| Outlook Uncertainty Current (versus previous month) | ||||||||

| Indicator | Jun Index | May Index | Change | Series Average | Trend* | % Reporting Increase | % Reporting No Change | % Reporting Decrease |

Outlook Uncertainty† | 42.3 | 18.2 | +24.1 | 10.1 | 13(+) | 53.8 | 34.6 | 11.5 |

| Business Indicators Relating to Facilities and Products in Texas, Retail Future (six months ahead) | ||||||||

| Indicator | Jun Index | May Index | Change | Series Average | Trend* | % Reporting Increase | % Reporting No Change | % Reporting Decrease |

| Retail Activity in Texas | ||||||||

Sales | 0.9 | 18.3 | –17.4 | 32.5 | 1(+) | 28.3 | 44.3 | 27.4 |

Employment | 10.3 | 22.0 | –11.7 | 13.3 | 26(+) | 28.9 | 52.5 | 18.6 |

Part–Time Employment | –0.8 | 0.5 | –1.3 | 1.7 | 1(–) | 10.7 | 77.8 | 11.5 |

Hours Worked | –7.4 | 4.0 | –11.4 | 3.1 | 1(–) | 6.4 | 79.8 | 13.8 |

Wages and Benefits | 43.6 | 50.1 | –6.5 | 29.0 | 26(+) | 49.5 | 44.6 | 5.9 |

Input Prices | 58.5 | 50.0 | +8.5 | 34.3 | 26(+) | 64.2 | 30.2 | 5.7 |

Selling Prices | 41.5 | 47.6 | –6.1 | 30.2 | 26(+) | 58.5 | 24.5 | 17.0 |

Capital Expenditures | 21.2 | 30.9 | –9.7 | 18.1 | 25(+) | 32.7 | 55.8 | 11.5 |

Inventories | 23.4 | 3.1 | +20.3 | 10.6 | 26(+) | 42.3 | 38.8 | 18.9 |

| Companywide Retail Activity | ||||||||

Companywide Sales | 4.0 | 14.6 | –10.6 | 31.3 | 26(+) | 32.3 | 39.3 | 28.3 |

Companywide Internet Sales | 5.1 | 17.2 | –12.1 | 22.8 | 27(+) | 20.5 | 64.1 | 15.4 |

| General Business Conditions, Retail Future (six months ahead) | ||||||||

| Indicator | Jun Index | May Index | Change | Series Average | Trend** | % Reporting Improved | % Reporting No Change | % Reporting Worsened |

Company Outlook | –13.8 | –3.5 | –10.3 | 17.3 | 2(–) | 21.4 | 43.3 | 35.2 |

General Business Activity | –26.8 | –3.5 | –23.3 | 12.8 | 4(–) | 17.7 | 37.7 | 44.5 |

*Shown is the number of consecutive months of expansion or contraction in the underlying indicator. Expansion is indicated by a positive index reading and denoted by a (+) in the table. Contraction is indicated by a negative index reading and denoted by a (–) in the table.

**Shown is the number of consecutive months of improvement or worsening in the underlying indicator. Improvement is indicated by a positive index reading and denoted by a (+) in the table. Worsening is indicated by a negative index reading and denoted by a (–) in the table.

†Added to survey in January 2018.

Data have been seasonally adjusted as necessary, with the exception of the outlook uncertainty index which does not yet have a sufficiently long time series to test for seasonality.

Texas Service Sector Outlook Survey

Texas Retail Outlook Survey

Texas Service Sector Outlook Survey

Comments from Survey Respondents

These comments are from respondents’ completed surveys and have been edited for publication.

- The twin issues of potential recession and high inflation are becoming more real in the industry. Finding associates who want to work is a huge issue (despite paying above-market rates).

- Inflation is increasing uncertainty.

- Recession talk is scaring people.

- As a company whose operations rely on the global supply-chain inventory for containers and domestic supply chain for chassis, we have been hamstrung in our ability to generate revenue by the shortage of containers for export loads, and especially, chassis for both import and export loads. Equipment is in short supply in the Dallas market, and we are not able to generate revenue without equipment. Also, we are short staffed and struggling with hiring, retaining and training candidates with the requisite internal motivation to generate value and get the job done without incurring unnecessary costs.

- Our general outlook continues to be bullish, as American energy is needed to replace what Europe is losing from Russian sources. Along with that, however, is some increased level of uncertainty based on economic conditions here in the U.S., with inflation and the associated interest rate hikes from the Fed [Federal Reserve] causing some concern that the economy is potentially in for a hard landing.

- Global and domestic stagflation this year and fear of a mild recession next year have decisions moving a bit slower out of caution.

- Increasing inflation is making profitability more challenging and forecasting expenses more difficult. Further, employees are more apt to work from home with rising gas prices, which has negatively impacted face-to-face collaboration and innovation efforts.

- The economic outlook is very unstable with so many variables undermining the economy. The consumer sentiment is degrading, with growth in the economy slowing down and inflation affecting the consumer’s buying leverage. The question is the probability of recession, which many pundits indicate is already present. Agriculture supplies have accelerated to an extreme level, impacting production inputs and ultimately [resulting in] the reduction in product for market. This is combined with the drought conditions in the Southwest and other areas of crop production areas like the Panhandle. [This is] besides the continuous heat wave affecting about one-third of the country.

- Rising interest rates have led to chaos in capital markets. Property-level fundamentals look solid.

- Increasing rates and uncertainty are affecting business valuations and activity.

- The effects of higher interest rates and fewer viable insurance options are taking a toll on multifamily deal flow. Two of three [deals] we expected to close this month have fallen out. The third only happened because the seller agreed to a huge last-minute price cut. Meanwhile, operating costs are rising faster than rent increases can be realized. Demand in Houston is still good for higher-priced apartments, but we fear this may soon dry up as inflation eats away at newfound spending power.

- It appears that the combination of housing price increases, rising interest rates and sustained inflation will cause housing sales activity to slow and housing price increases to decelerate.

- The oncoming recession appears almost fully baked at this point.

- Construction costs are rising, salaries are rising, interest rates are rising, insurance costs are rising, property taxes are rising, and margins are shrinking.

- The increase in interest rates is causing pain for buyers on purchasing and sellers on loan renewals.

- There is still a shortage of properties on the market. There are many questions from buyers and sellers about the economy and timing to buy a house due to the rise in interest rates.

- We survive by selling stuff—some whole goods and parts, some labor. We can't get any of it!

- Our business is on the rise, but so is our anxiety. Some sectors remain especially weak. Likewise, city officials continue to press for uses that are no longer in the market, including retail.

- I have several proposals in to several companies and have hopes that one will be accepted, which is the reason for our six-month improved outlook and revenue.

- The U.S. economy is looking bad, and recession seems to be around.

- Government procurement activity for professional technical services remains flat with the exception of procurement and R&D [research and development] spending in technology areas such as cybersecurity and AI/ML [artificial intelligence/machine learning].

- High inflation, geopolitical unrest and a failing tone-deaf administration is causing high anxiety.

- We simply cannot keep up with the increasing costs of doing business. By the time we reprice our services, cost increases have already eaten the pricing gains.

- The labor shortage has increased workload and stress.

- There is lots of uncertainty regarding inflation, global economies, supply-chain interruptions, etc.

- The residential and commercial real estate markets are feeling the pressure of the interest rate hikes and are beginning to slow down. Residential orders are down 30 percent year over year, while the commercial orders are showing signs of weakness. This year has been very robust, but the second half of the year may tell a different story.

- The rising interest rates do not yet seem to have had a material impact on the number of transactions.

- Stock market volatility and inflation present challenges for our industry.

- Our main inflationary factor is labor costs. Labor is approximately 43 percent of our expense. Wages for lower unskilled workers has risen approximately 35 percent since January, with the balance rising 10 percent to maintain the differential between unskilled and slightly skilled.

- We are still experiencing severe backorder in supply chain. We have over $14 million in backorders, with numbers staying fairly constant. Many items are showing 12-month backorders.

- The price of our everyday consumables is becoming unsustainable long term (six to eight months). It is not so much the price, but that the rate of the applied price increases seems to be monthly now. We cannot ask our customers to keep paying more every quarter to cover the monthly increases from our suppliers and have no "blowback." Our customers are just as frustrated as we are with the current state of affairs. My fear is these price increases are becoming so reactionary that nobody truly understands what or why the costs are rising.

- My sentiment got worse last month, but this month it hasn't gotten worse again; maybe that is a sign of slight improvement. But my six-month outlook gets increasingly more foggy. Let's just say I have made the tentative "downturn plans." I just hope I don't have to use them.

- Delivery of service is greatly reduced in the travel industry but more important is the total disruption of flight schedules by the airlines due to staffing issues.

- Corporate and government travel has increased 100 percent and has also exceeded the sales forecast for this year.

- Costs are outrunning the ability to adjust for them. Consumers and contractors are resisting the increases. Margins are shrinking fast enough to consider closing.

- Inflation is the major concern.

- We are concerned about inflationary risk, the continued tight labor market and shortage of labor, extraordinary gasoline prices and the teetering bear market. We are balancing the need to save cash with funding growth.

- Inflation has increased our cost of services, but state policy doesn't allow us to increase prices. Any revenue increases are coming through growth in number of students. High uncertainty regarding inflation, health, and world conflict make the future outlook more uncertain than it was a few months ago.

- Concerns remain: Will students return to classrooms? Will new teachers enter the profession? Will existing teachers continue within the profession?

- Gas prices and the price for staple items at the grocery store are killing consumers’ pocketbooks. Help!

- At our food bank, we are experiencing rapidly increasing costs (food, fuel, manpower, equipment, etc.) to operate. At the same time, the demand for emergency food is growing rapidly because poor people are being disproportionately impacted by inflation. This situation is not sustainable.

- We provide cash-pay prices for medical procedures. With inflation pressure and increased sensitivity to it, we feel activity will increase as companies will choose to use our data to steer people to less-expensive providers (a cost-cutting measure).

- We deal primarily with consumer discretionary cosmetic dentistry. Typically, if mid/upper management layoffs aren't occurring, we don't see an impact on patient flow and revenue during down business cycles. However, we haven't had to deal with the psychology of inflation since cosmetic dentistry became popular, so we are interested to see how this plays out.

- We are seeing a drop in volume and, consequently, revenues of about 7 percent when compared with 2021 and with May. I surmise that this may be related to consumer credit card debt, since most of our patients pay up front with credit cards. We are also dealing with an ongoing shortage of IV contrast used in CT scans.

- Extremely tough operating given Fed dual mandate; political leaders looking for almost anyone to berate; too much attention to Putin; would prefer it to be Newton; JIT [just in time], labor costs, shortages feels much like checkmate.

- I can see the impact of inflation on leisure tourism levels in San Antonio. With fewer available dollars, we are seeing very weak business levels.

- All input prices are not up 8 percent; it is closer to 50–80 percent.

- The rapid rise in inflation, challenges with supply chain and lack of applicants to fill open positions are lowering the optimism we projected earlier in the year.

- Food commodities continue to increase at a speed I have never witnessed before. Profit margins are being squeezed, forcing our company to hold back on increasing wages and forcing us to rethink capital expenditures in fourth quarter 2022.

- As prices rise, we are focusing on now.

- Prices for all goods, supplies, cost of goods sold continue to rise, and supply-chain issues still continue to hamper our business.

- We see continued increases in all input prices of labor, raw product and all expenses. Nothing is the same or down; everything is up and climbing. Our property insurance renewal increased by 120 percent with an increase in deductible. General customer activity is better than a year ago but not keeping pace with the increase in all costs. Worrisome signs of slowdown from customers are beginning to appear. We are very concerned about the next few years. I was a young man during the late 70s/80s and recall watching my parents struggle to keep the business open. I fear the die has already been cast for a repeat of that horrible time. If one does not learn from history, then [we are] doomed to repeat it. Hope I'm wrong.

- We are irrevocably committed to opening three new cafe locations in the next six to nine months, and thus revenues, expenditures and inventories will increase. Further expansion/new cafe plans are in suspense pending the results of the next two months.

- I am concerned with a looming recession at a time when I am greatly increasing my capital expenditures by building new locations.

- [We are] headed for a recession.

- The current administration in Washington is out of touch with reality, and the Federal Reserve has grossly mismanaged its affairs and its portfolio. If the Federal Reserve governors had a scintilla of integrity or self-respect, they would resign and admit their failure. However, they will not do so and, therefore, they will lead us into a very serious recession. The Fed caused the inflation by its excessive expansion of its balance sheet and now it cannot quickly reduce its balance sheet without incurring substantial losses, which it does not want to experience.

- Higher prices are creating some demand destruction.

- Although sales increased, it was only on a few large school sales; we are not confident that sales overall will increase regularly. We are skeptical.

- We are experiencing logistics problems. It is difficult to get cargo shipped on a timely basis. We have cargos that were supposed to have shipped three months ago and are still unable to get cargo space to ship out. It created storage space and cash flow problems.

- Rapidly rising inflation and higher prices will be detrimental to the food service industry. Our primary customers are casual dining restaurants, and I would expect them to raise menu prices, which in turn will reduce demand from their patrons.

- With all of the unknowns in the market, sales and margins continue to remain strong when compared with historical levels. Our inventory levels remain at record lows; that leads to us being a little less averse to risk than we would be if our warehouse was full and margins were low because of competitive pressures.

- Inflation and fuel prices are creating an uncertain environment for the retail consumer. We see the fuel prices affecting purchase decisions.

- We are experiencing supply-chain issues.

- Sharply rising mortgage and commercial interest rates are taking a toll on our business. We sell building materials and do some light manufacturing of doors, trusses and stone fabrication.

- Margins will be worsening. Costs are going up on goods, fuel for delivery vehicles, labor and utilities. However, we are not able to pass on higher margins contractually.

- Consumption items are driving up the cost of living—fuel, food, rent and utilities. I’m not sure if interest rates are the problem yet.

- Due to increased interest rates and supply-chain issues, I foresee the residential construction market slowing over the next six months.

- You [the Federal Reserve] messed up waiting so long to raise rates. Now, you’ve royally messed up raising them too fast.

- We service a population of older, nonmobile patients. Many of these patients have chronic illnesses, and they depend on us to deliver their medications to their door. We currently offer this service at no cost, but with gas prices, this is certainly a worry for us.

- The current administration's oil and gas policies are damaging to our Texas economy and the country.

- A significant portion of our business is dependent on new-home construction. If it drops dramatically, we need fewer employees and less inventory. If it stays strong, we need more employees and more inventory. It is very difficult to plan.

- We are working very hard on our growth plans and feel encouraged by recent successes obtaining new business. However, we recognize the role that rapid inflation can play in thwarting our efforts, so while we see improvements in many areas going forward, we also have uncertainty about how inflation may impact our plans.

Historical Data

Historical data can be downloaded dating back to January 2007.

Indexes

Download indexes for all indicators. For the definitions of all variables, see Data Definitions.

Texas Service Sector Outlook Survey |

Texas Retail Outlook Survey |

| Unadjusted | Unadjusted |

| Seasonally adjusted | Seasonally adjusted |

All Data

Download indexes and components of the indexes (percentage of respondents reporting increase, decrease, or no change). For the definitions of all variables, see Data Definitions.

Texas Service Sector Outlook Survey |

Texas Retail Outlook Survey |

| Unadjusted | Unadjusted |

| Seasonally adjusted | Seasonally adjusted |

Questions regarding the Texas Service Sector Outlook Survey can be addressed to Christopher Slijk at christopher.slijk@dal.frb.org.

Sign up for our email alert to be automatically notified as soon as the latest Texas Service Sector Outlook Survey is released on the web.