Texas Service Sector Outlook Survey

Growth in service activity continues as price and wage pressures pick up in August

For this month’s survey, Texas business executives were asked supplemental questions on wages, prices and the impact of the recent heat wave. Results for these questions from the Texas Manufacturing Outlook Survey, Texas Service Sector Outlook Survey and Texas Retail Outlook Survey have been released together. Read the special questions results.

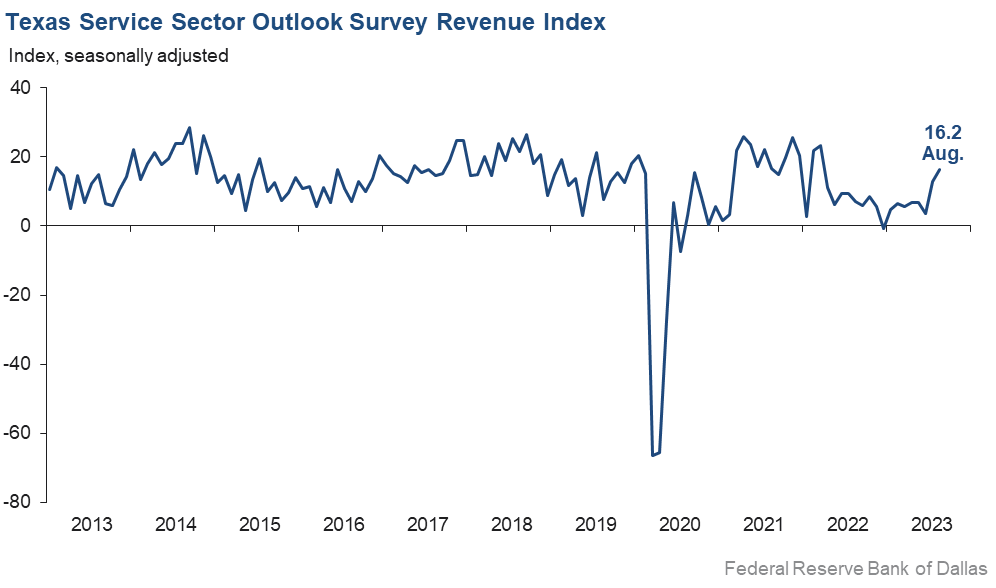

Texas service sector activity expanded at a slightly faster pace in August compared with the prior month, according to business executives responding to the Texas Service Sector Outlook Survey. The revenue index, a key measure of state service sector conditions, increased three points to 16.2.

Labor market indicators pointed to steady growth in employment and workweeks. The employment index remained stable at 9.3, indicating the same employment growth as the previous month. The part-time employment index increased three points to 2.8, while the hours worked index was relatively unchanged at 2.4.

Perceptions of broader business conditions worsened slightly in August. The general business activity index increased two points but remained negative at -2.7. The company outlook index edged down to -1.2. The outlook uncertainty index was unchanged at 11.6—below the series average of 13.5.

Price and wage pressures increased in August. The input prices index rose from 31.7 to 37.8, and the selling prices index increased four points to 14.2, as both indexes remained above their series averages. The wages and benefits index also increased four points to 20.4, the highest level since January and above its average reading of 15.8.

Respondents’ expectations regarding future business activity held steady in August. The future general business activity index was relatively unchanged at 3.9. The future revenue index improved two points to 37.3. Other future service sector activity indexes such as employment and capital expenditures displayed mixed movements but remained in positive territory reflecting expectations for continued growth in the next six months.

Texas Retail Outlook Survey

Texas retail sales see little growth

Retail sales were flat in August, according to business executives responding to the Texas Retail Outlook Survey. The sales index, a key measure of state retail activity, inched up from -2.4 to -0.6, with the near-zero reading suggestive of no change in sales from last month. Retailers’ inventories grew at a faster rate, with the index increasing from 12.0 to 17.2.

Retail labor market indicators reflected steady growth in employment and continued shortening of workweeks in August. The employment index was unchanged at 3.0. The part-time employment index was also largely unchanged at -1.7 while the hours worked index fell from -7.6 to -10.1.

Retailers’ perceptions of broader business conditions continued to worsen in August, though pessimism waned. The general business activity index increased from -18.1 to -4.0, and the company outlook index rose six points to -4.5. The outlook uncertainty index fell from 24.6 to 16.9.

Price and wage pressures increased in August. The selling prices index rose eight points to 16.5, and the input prices index increased seven points to 26.9. The wages and benefits index jumped from 10.5 to 19.0.

Expectations for future retail growth improved in August. The future sales index moved up from 15.1 to 20.3, and the future general business activity index ticked up two points to 6.6. Other indexes of future retail activity such as employment also remained in positive territory, reflecting expectations for continued growth in retail activity later in the year.

The Texas Retail Outlook Survey is a component of the Texas Service Sector Outlook Survey that uses information only from respondents in the retail and wholesale sectors.

Next release: September 26, 2023

Data were collected August 15–23, and 279 Texas service sector business executives, of which 61 were retailers, responded to the survey. The Dallas Fed conducts the Texas Service Sector Outlook Survey monthly to obtain a timely assessment of the state’s service sector activity. Firms are asked whether revenue, employment, prices, general business activity and other indicators increased, decreased or remained unchanged over the previous month.

Survey responses are used to calculate an index for each indicator. Each index is calculated by subtracting the percentage of respondents reporting a decrease from the percentage reporting an increase. When the share of firms reporting an increase exceeds the share reporting a decrease, the index will be greater than zero, suggesting the indicator has increased over the prior month. If the share of firms reporting a decrease exceeds the share reporting an increase, the index will be below zero, suggesting the indicator has decreased over the prior month. An index will be zero when the number of firms reporting an increase is equal to the number of firms reporting a decrease. Data have been seasonally adjusted as necessary.

Texas Service Sector Outlook Survey

Historical data are available from January 2007 to the most current release month.

| Business Indicators Relating to Facilities and Products in Texas Current (versus previous month) | ||||||||

| Indicator | Aug Index | Jul Index | Change | Series Average | Trend* | % Reporting Increase | % Reporting No Change | % Reporting Decrease |

Revenue | 16.2 | 12.9 | +3.3 | 11.0 | 8(+) | 32.9 | 50.4 | 16.7 |

Employment | 9.3 | 9.2 | +0.1 | 6.6 | 5(+) | 20.4 | 68.5 | 11.1 |

Part–Time Employment | 2.8 | –0.6 | +3.4 | 1.5 | 1(+) | 7.6 | 87.6 | 4.8 |

Hours Worked | 2.4 | 3.5 | –1.1 | 2.8 | 2(+) | 8.1 | 86.2 | 5.7 |

Wages and Benefits | 20.4 | 16.7 | +3.7 | 15.8 | 39(+) | 22.9 | 74.6 | 2.5 |

Input Prices | 37.8 | 31.7 | +6.1 | 27.8 | 40(+) | 40.9 | 56.0 | 3.1 |

Selling Prices | 14.2 | 9.9 | +4.3 | 7.6 | 37(+) | 20.4 | 73.4 | 6.2 |

Capital Expenditures | 9.2 | 8.9 | +0.3 | 10.1 | 37(+) | 17.0 | 75.2 | 7.8 |

| General Business Conditions Current (versus previous month) | ||||||||

| Indicator | Aug Index | Jul Index | Change | Series Average | Trend** | % Reporting Improved | % Reporting No Change | % Reporting Worsened |

Company Outlook | –1.2 | 0.5 | –1.7 | 4.7 | 1(–) | 12.5 | 73.8 | 13.7 |

General Business Activity | –2.7 | –4.2 | +1.5 | 2.9 | 15(–) | 15.2 | 66.9 | 17.9 |

| Indicator | Aug Index | Jul Index | Change | Series Average | Trend* | % Reporting Increase | % Reporting No Change | % Reporting Decrease |

Outlook Uncertainty | 11.6 | 10.9 | +0.7 | 13.5 | 27(+) | 21.9 | 67.9 | 10.3 |

| Business Indicators Relating to Facilities and Products in Texas Future (six months ahead) | ||||||||

| Indicator | Aug Index | Jul Index | Change | Series Average | Trend* | % Reporting Increase | % Reporting No Change | % Reporting Decrease |

Revenue | 37.3 | 35.6 | +1.7 | 37.6 | 40(+) | 49.4 | 38.4 | 12.1 |

Employment | 27.9 | 29.7 | –1.8 | 23.3 | 40(+) | 39.3 | 49.4 | 11.4 |

Part–Time Employment | 3.6 | 5.4 | –1.8 | 6.8 | 4(+) | 12.2 | 79.2 | 8.6 |

Hours Worked | 10.3 | 2.2 | +8.1 | 5.9 | 40(+) | 15.0 | 80.3 | 4.7 |

Wages and Benefits | 42.4 | 41.8 | +0.6 | 37.4 | 40(+) | 46.3 | 49.8 | 3.9 |

Input Prices | 47.8 | 43.8 | +4.0 | 44.7 | 200(+) | 52.0 | 43.9 | 4.2 |

Selling Prices | 28.2 | 25.9 | +2.3 | 24.7 | 40(+) | 35.5 | 57.2 | 7.3 |

Capital Expenditures | 14.9 | 12.6 | +2.3 | 23.2 | 39(+) | 23.6 | 67.7 | 8.7 |

| General Business Conditions Future (six months ahead) | ||||||||

| Indicator | Aug Index | Jul Index | Change | Series Average | Trend** | % Reporting Improved | % Reporting No Change | % Reporting Worsened |

Company Outlook | 9.6 | 11.9 | –2.3 | 15.8 | 3(+) | 22.2 | 65.2 | 12.6 |

General Business Activity | 3.9 | 4.4 | –0.5 | 12.5 | 2(+) | 20.2 | 63.5 | 16.3 |

Historical data are available from January 2007 to the most current release month.

| Business Indicators Relating to Facilities and Products in Texas Retail (versus previous month) | ||||||||

| Indicator | Aug Index | Jul Index | Change | Series Average | Trend* | % Reporting Increase | % Reporting No Change | % Reporting Decrease |

| Retail Activity in Texas | ||||||||

Sales | –0.6 | –2.4 | +1.8 | 4.3 | 4(–) | 28.1 | 43.2 | 28.7 |

Employment | 3.0 | 3.2 | –0.2 | 1.9 | 3(+) | 17.0 | 69.0 | 14.0 |

Part–Time Employment | –1.7 | –1.3 | –0.4 | –1.6 | 2(–) | 5.5 | 87.3 | 7.2 |

Hours Worked | –10.1 | –7.6 | –2.5 | –1.9 | 9(–) | 3.3 | 83.3 | 13.4 |

Wages and Benefits | 19.0 | 10.5 | +8.5 | 11.2 | 37(+) | 21.4 | 76.2 | 2.4 |

Input Prices | 26.9 | 20.3 | +6.6 | 22.6 | 40(+) | 37.0 | 52.9 | 10.1 |

Selling Prices | 16.5 | 8.4 | +8.1 | 13.9 | 39(+) | 31.5 | 53.5 | 15.0 |

Capital Expenditures | 3.7 | –0.2 | +3.9 | 8.0 | 1(+) | 14.2 | 75.3 | 10.5 |

Inventories | 17.2 | 12.0 | +5.2 | 2.5 | 15(+) | 32.0 | 53.2 | 14.8 |

| Companywide Retail Activity | ||||||||

Companywide Sales | 0.3 | –11.9 | +12.2 | 5.6 | 1(+) | 26.2 | 48.0 | 25.9 |

Companywide Internet Sales | 0.0 | –6.7 | +6.7 | 4.5 | 1() | 15.5 | 69.0 | 15.5 |

| General Business Conditions, Retail Current (versus previous month) | ||||||||

| Indicator | Aug Index | Jul Index | Change | Series Average | Trend** | % Reporting Improved | % Reporting No Change | % Reporting Worsened |

Company Outlook | –4.5 | –10.4 | +5.9 | 2.3 | 18(–) | 10.2 | 75.1 | 14.7 |

General Business Activity | –4.0 | –18.1 | +14.1 | –1.6 | 2(–) | 12.8 | 70.4 | 16.8 |

| Outlook Uncertainty Current (versus previous month) | ||||||||

| Indicator | Aug Index | Jul Index | Change | Series Average | Trend* | % Reporting Increase | % Reporting No Change | % Reporting Decrease |

Outlook Uncertainty | 16.9 | 24.6 | –7.7 | 11.2 | 27(+) | 20.3 | 76.3 | 3.4 |

| Business Indicators Relating to Facilities and Products in Texas, Retail Future (six months ahead) | ||||||||

| Indicator | Aug Index | Jul Index | Change | Series Average | Trend* | % Reporting Increase | % Reporting No Change | % Reporting Decrease |

| Retail Activity in Texas | ||||||||

Sales | 20.3 | 15.1 | +5.2 | 31.2 | 3(+) | 36.0 | 48.3 | 15.7 |

Employment | 11.0 | 14.2 | –3.2 | 12.9 | 40(+) | 24.5 | 62.0 | 13.5 |

Part–Time Employment | –0.2 | –8.2 | +8.0 | 1.5 | 9(–) | 11.3 | 77.2 | 11.5 |

Hours Worked | 0.7 | –3.7 | +4.4 | 2.6 | 1(+) | 10.8 | 79.1 | 10.1 |

Wages and Benefits | 31.0 | 25.2 | +5.8 | 29.1 | 40(+) | 36.2 | 58.6 | 5.2 |

Input Prices | 32.8 | 17.0 | +15.8 | 34.1 | 40(+) | 41.4 | 50.0 | 8.6 |

Selling Prices | 20.7 | 11.3 | +9.4 | 29.5 | 40(+) | 32.8 | 55.2 | 12.1 |

Capital Expenditures | 10.1 | 0.0 | +10.1 | 17.2 | 1(+) | 18.6 | 72.9 | 8.5 |

Inventories | 9.1 | 10.7 | –1.6 | 10.8 | 40(+) | 29.3 | 50.5 | 20.2 |

| Companywide Retail Activity | ||||||||

Companywide Sales | 15.4 | 22.3 | –6.9 | 29.7 | 3(+) | 34.2 | 47.0 | 18.8 |

Companywide Internet Sales | 15.6 | 17.7 | –2.1 | 21.7 | 2(+) | 26.7 | 62.2 | 11.1 |

| General Business Conditions, Retail Future (six months ahead) | ||||||||

| Indicator | Aug Index | Jul Index | Change | Series Average | Trend** | % Reporting Improved | % Reporting No Change | % Reporting Worsened |

Company Outlook | 3.9 | 5.1 | –1.2 | 15.5 | 3(+) | 15.9 | 72.1 | 12.0 |

General Business Activity | 6.6 | 5.0 | +1.6 | 11.0 | 2(+) | 20.4 | 65.8 | 13.8 |

*Shown is the number of consecutive months of expansion or contraction in the underlying indicator. Expansion is indicated by a positive index reading and denoted by a (+) in the table. Contraction is indicated by a negative index reading and denoted by a (–) in the table.

**Shown is the number of consecutive months of improvement or worsening in the underlying indicator. Improvement is indicated by a positive index reading and denoted by a (+) in the table. Worsening is indicated by a negative index reading and denoted by a (–) in the table.

Data have been seasonally adjusted as necessary.

Texas Service Sector Outlook Survey

Texas Retail Outlook Survey

Texas Service Sector Outlook Survey

Comments from survey respondents

These comments are from respondents’ completed surveys and have been edited for publication.

- Transaction work is still very slow. Uncertainty over interest rates is still a drag on the market.

- Productivity is down with hybrid work conditions. Wage inflation is still an issue, and worker retention still weighs on employers, requiring more overhead to manage perks such as flex hours, remote work and training.

- We are seeing the first signs of clients (chemical producers, manufacturers) tightening their spending. We are expecting the slowdown to hit us in first quarter 2024.

- Cost-cutting measures have led to increased profitability for us. The recurring nature of our revenue is a source of solace at times of uncertainty.

- We are seeing more general business activity and interest in our services as compared to the past six months. However, buyers are more price-sensitive due to the current state of the economy and higher interest rates.

- The market is slipping into expansion.

- We anticipate not filling employee vacancy through normal turnover if revenue decreases slightly. We do not anticipate any forced reduction in staff.

- There is just no good news about the commercial real estate market these days. With the uncertainty of interest rates, we are having a difficult time pricing acquisitions, which is causing everyone to take a pause. We thought we were headed for a soft landing, but with Germany's and now China's economic slowdown, we do not know how this is going to happen. The consumer is racking up credit card debt, resisting the Federal Reserve efforts to slow inflation, which we are afraid is leading us into stagflation at some point.

- Activity has continued to remain strong despite interest rate increases, continuing difficulties with hiring and retaining key staff, and concerns about a pending recession. Input prices are still being passed along in the form of price increases, although that is expected to become more difficult. Not seeing any companies losing money, yet.

- Overall, still a strong labor market. Good candidates are hard to find, but companies taking longer to make hiring decisions combined with a tight labor market make it tough for search and staffing firms to create revenue.

- Uncertainty about inflation and the political climate in Washington is creating risk.

- Skilled labor is still hard to find for our business. We have increased our hiring pay by 22 percent and cannot find qualified candidates. Overall, business activity is stable. The corporate aviation market seems to have picked up, with many requests for quotes going into fourth quarter, which is a good sign.

- The wages cannot attract workers to this service. We have tons of work and no one to do it.

- There is still much concern about a potential recession. This combined with the almost certainty of another rate increase before the end of the year means access to expansion capital will be difficult.

- We continue to see softness in occupancy, while we are able to modestly drive the occupancy rate.

- We are still having staffing concerns. We hope to hire more part-time staff that can work 20 to 30 hours to help address the staffing shortage.

- Political challenges at the federal level continue to spook decision-makers at the local level.

- Inflation and interest rates are hitting the low-income sector of the economy disproportionately hard.

- [We are] optimistic for a turnaround in commercial real estate investment beginning the middle of next year now that the Federal Reserve may be at the end of the cycle raising interest rates. Once market participants feel certainty of that, more equity and debt capital will become available to fuel acquisitions and new development, but it’s not happening overnight.

- Low housing inventory and high interest rates are a challenge.

- For us, it is clear that the interest rate hikes have far exceeded their intended outcome. The repercussions will be swift and severe without relief.

- Failing clients (multifamily owners) are costing us, but as these go away more are coming in. Legal expenses are way up.

- We are getting feedback from a lot of construction customers that said projects are being won/awarded, but actual construction is being delayed due to funding factors related to rising interest rates.

- We are insurance brokers, and the cost of property insurance is going up for almost everyone due to losses and Maui wildfires, hail in Texas, etc.

- Demand for commercial real estate lease space is expected to decrease over the next six months.

- We have had a very small increase in business, likely the result of others giving up.

- Next year we are seeing continued growing interest in productivity software/platforms with advanced capabilities from the federal government and private sector. They need automated efficiency to sustain operations and get more productivity from new employees/contractors. Wage inflation persists, so they are looking for more cost-effective methods.

- Everything feels very stable at the moment.

- Elections on both sides of the border are an increasing risk factor.

- We are still experiencing commodity shortages with some precious metal assemblies and specialty steel. Industrial semiconductors remain challenging, and overall demand for electrical power distribution and control assemblies remains strong, with demand outstripping supply. We have announced a $100 million-plus manufacturing expansion in East Texas to help increase supply.

- We have a new customer in Ecuador. When the opposition candidate was murdered last week, it caused the customer to pull back and wait until the elections are over to determine how they will proceed.

- Demand for new and used vehicles continues to be strong despite higher interest rates, although consumers are much more price- and interest-rate sensitive. Inventories are growing at all brands, some more than others. Domestic brand inventory is growing fastest, but a United Auto Workers strike could stall that growth.

- It is difficult to forecast based on issues facing us that are beyond our control. Example: United Auto Workers contract, interest rates, regulation, supply-chain issues.

- Maintaining our preferred inventories has again become very challenging. With the potential of the United Auto Workers labor strike, our outlook has deteriorated.

- We seemed to be in a holding pattern. Margins are decreasing, and customer traffic is decreasing. Diligent follow-up on internet leads is imperative in order to keep sales from decreasing. The consumer is becoming more cautious.

- Productivity has been tough with extreme temperatures, but business activity seems to be picking up. [There are] still a lot of issues to deal with like finding qualified workers.

- Inflation and drug prices are constantly rising, but our reimbursements are not.

- In health care, there are only a few ways to stay relevant and turn a profit, so we have chosen to create new technology. The only concern is bureaucracy, or rather quasi-bureaucracy, that can stifle our progression. Some of the major pharmacy benefit managers and large pharmacy chains own entities that control the highway by which information is transmitted between pharmacies. We feel that this is too much power, and the method is inefficient. Hopefully, the government will not provide even more power and leverage to them so we can focus on moving the health care industry into the 21st century.

- Lack of supply in the labor market is becoming very difficult for us to deal with.

- It is more a day-by-day right now in retail. We have lots of factors affecting business such as extreme heat, as people aren't out and walking in the store. In addition, customers are waiting on sales versus paying full price.

- Business was good in August, but we expect September to decline. We need to bring workers back to the office; no one works on Friday anymore. We used to have a very busy Friday lunch and happy hour—not anymore, and it won't change until offices are more densely populated.

- Cost of goods sold continues to increase beyond our ability to raise prices. Continued very soft business travel and low activity in downtown are serious drags on our revenue.

- Things have been consistent, no big swings in any direction or particular sector. Employee retention has improved as well as work candidates. We expect that business will slow down in six months after the holidays, but it is a normal trend.

- We are starting to see inflation and higher rates impact consumer spending.

Historical Data

Historical data can be downloaded dating back to January 2007.

Indexes

Download indexes for all indicators. For the definitions of all variables, see data definitions.

Texas Service Sector Outlook Survey |

Texas Retail Outlook Survey |

| Unadjusted | Unadjusted |

| Seasonally adjusted | Seasonally adjusted |

All Data

Download indexes and components of the indexes (percentage of respondents reporting increase, decrease, or no change). For the definitions of all variables, see data definitions.

Texas Service Sector Outlook Survey |

Texas Retail Outlook Survey |

| Unadjusted | Unadjusted |

| Seasonally adjusted | Seasonally adjusted |

Questions regarding the Texas Service Sector Outlook Survey can be addressed to Jesus Cañas at jesus.canas@dal.frb.org.

Sign up for our email alert to be automatically notified as soon as the latest Texas Service Sector Outlook Survey is released on the web.