Mexico’s economic growth slows in fourth quarter; outlook weakens

February 17, 2023

| January 2023 economic report | |||

| GDP, real Q4 '22 |

Employment, formal Dec. '22 |

CPI Jan. '23 |

Peso/dollar Jan. '23 |

| 1.6% q/q | 47,000 jobs m/m | 8.0% y/y | 19.0 |

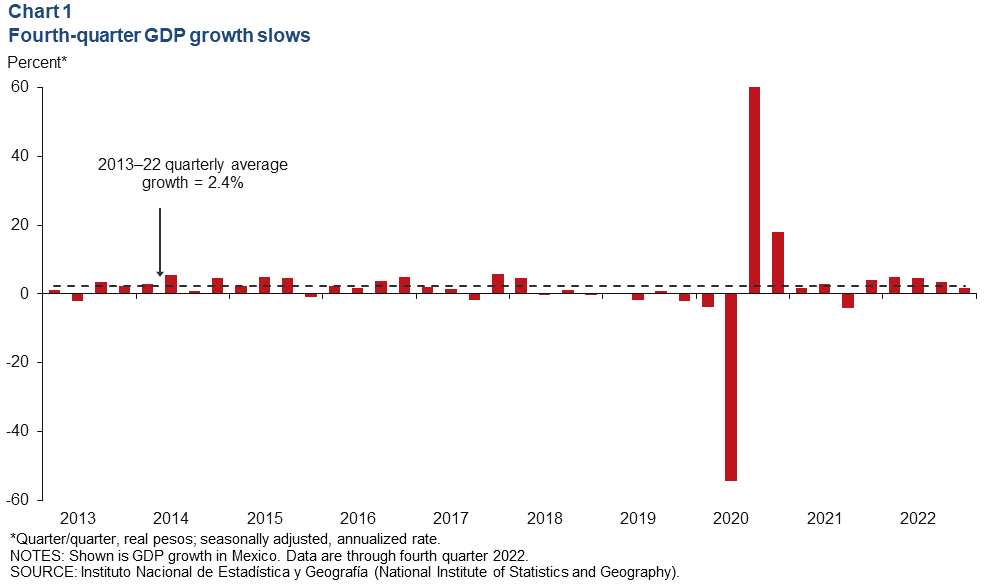

Mexico’s fourth-quarter GDP growth was slower than earlier in 2022, indicating that the Mexican economy was losing momentum. Still, growth was slightly faster than expected as GDP rose an annualized 1.6 percent compared with median expectations of 1.2 percent. In 2022, Mexico’s economy grew 3.7 percent (fourth quarter/fourth quarter) as resilient domestic demand and remaining tailwinds from reopening after COVID were able to mitigate the impact of slowing U.S. economic growth on the local manufacturing sector.

Mexico’s economy is expected to slow considerably this year, as tight monetary conditions will likely weaken domestic demand, and slower U.S. growth will affect Mexican manufacturing exports. The consensus forecast for 2023 GDP (fourth quarter/fourth quarter), compiled by Banco de México, indicates dismal growth of only 0.7 percent (Table 1).

The latest data available show industrial production, retail sales and employment increased while exports fell. In January, the peso strengthened against the dollar, and inflation picked up steam.

| Table 1 Consensus forecasts for 2023 Mexico growth, inflation and exchange rate |

|||

| December | January | ||

| Real GDP growth (Q4/Q4) |

0.7 |

0.7 |

|

| Real GDP (average year/year) |

0.9 |

1.0 |

|

| CPI (Dec. '23/Dec. '22) |

5.1 |

5.2 |

|

| Exchange rate—pesos/dollar (end of year) |

21.0 |

20.7 |

|

| NOTE: CPI refers to consumer price index. The survey period was Jan. 19–30. SOURCE: Encuesta sobre las Expectativas de los Especialistas en Economía del Sector Privado: Enero de 2023 (communiqué on economic expectations, Banco de México, January 2023). |

|||

Growth in economic activity slows in fourth quarter

According to preliminary estimates, Mexico’s fourth-quarter GDP rose an annualized 1.6 percent, considerably slower than 3.6 percent growth the previous quarter (Chart 1). The goods-producing sector (manufacturing, construction, utilities and mining) increased 1.6 percent, while the service-providing sector (wholesale and retail trade, transportation and business services) grew 0.8 percent. Agriculture output jumped 8.0 percent.

Industrial production grows at year-end

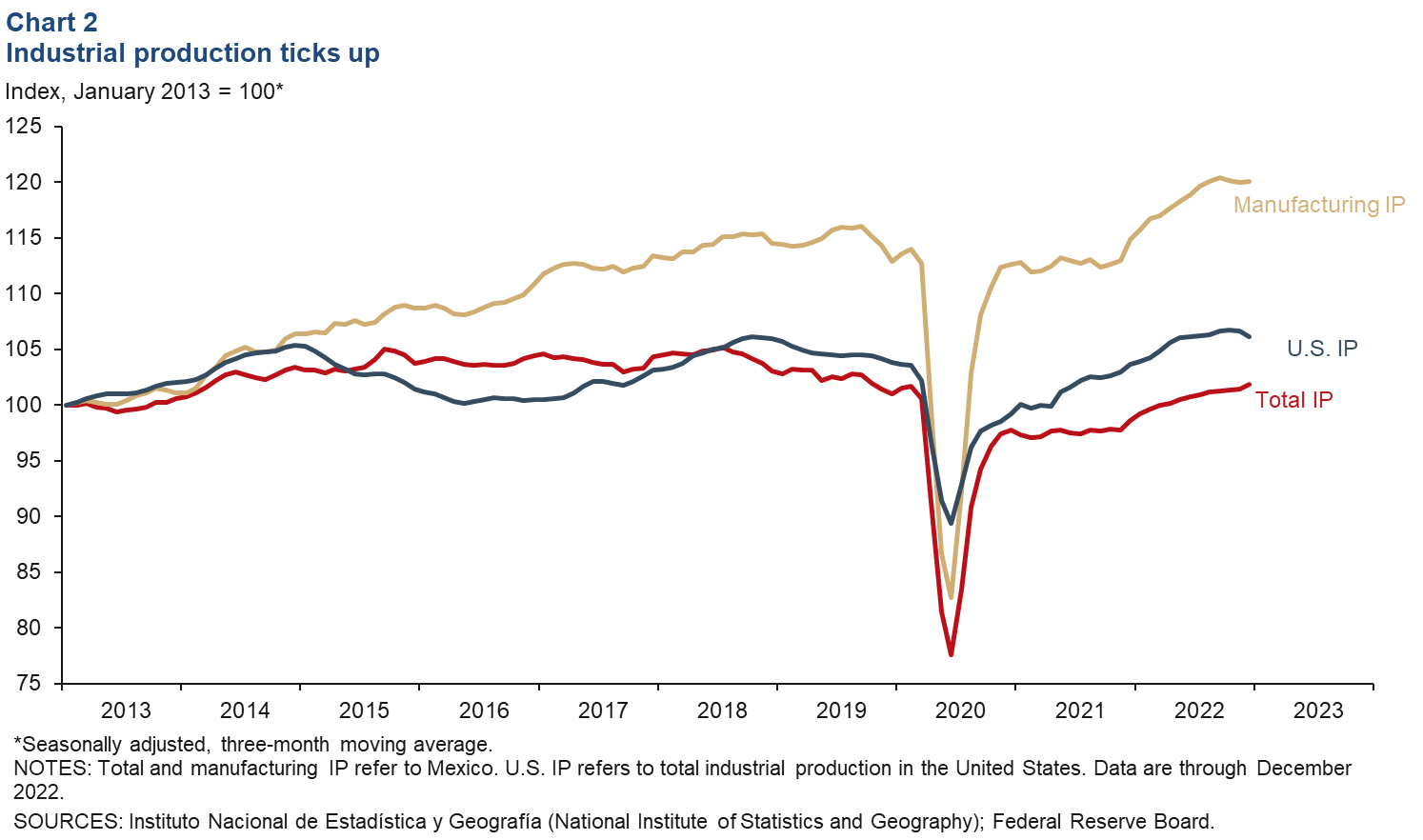

In December, the three-month-moving average of Mexico’s industrial production (IP) index—which includes manufacturing, construction, oil and gas extraction, and utilities—ticked up 0.4 percent, while the smoothed manufacturing IP index was up 0.1 percent (Chart 2). On an unsmoothed, month-over-month basis, IP was up 0.7 percent in December after rising 0.2 percent in November, while manufacturing rose 0.5 percent in both November and December. North of the border, U.S. IP fell 0.4 percent in December after falling 0.1 percent in November. The correlation between IP in Mexico and the U.S. has increased considerably with the rise of intra-industry trade between the two countries since the early 1990s. Mexico’s manufacturing sector could experience a slowdown in 2023, particularly if U.S. consumer demand decelerates as a result of high inflation and the high cost of credit.

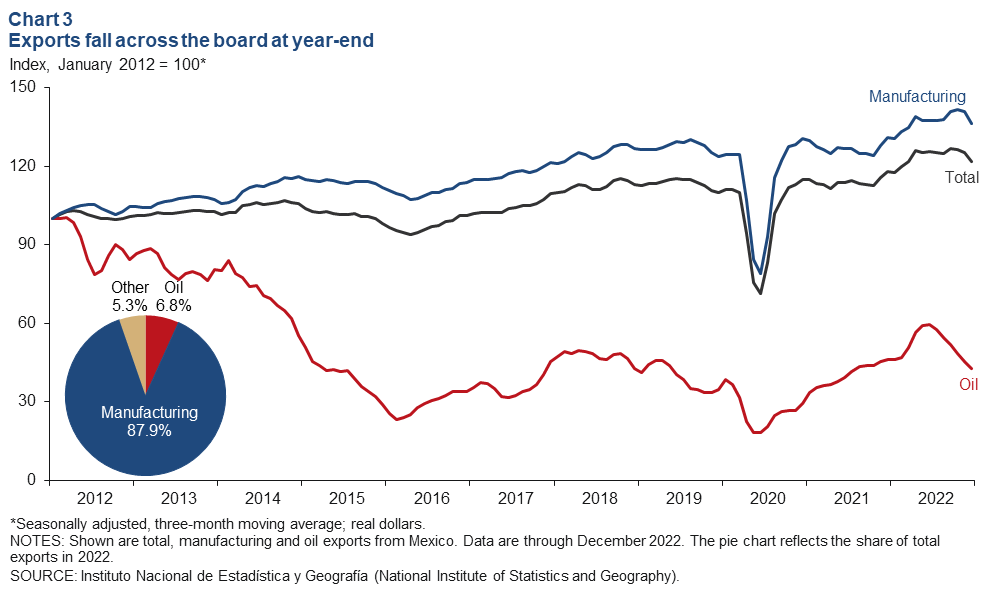

Exports fall in December but up in 2022

The three-month moving average of total real Mexican exports was down 3.0 percent month over month in December (Chart 3). Oil exports declined by 5.5 percent, and the much-larger manufacturing sector saw a decline of 3.2 percent. On a month-over-month and unsmoothed basis, total exports declined 1.6 percent in December, while oil exports rose 11.2 percent and manufacturing exports fell 2.8 percent. The rise in oil prices contributed to growth in oil exports earlier in 2022, but exports declined toward the end of the year as prices retreated. Total exports increased 8.3 percent in 2022, with manufacturing growing 8.0 percent and oil exports climbing 24.0 percent.

Retail sales tick up in November

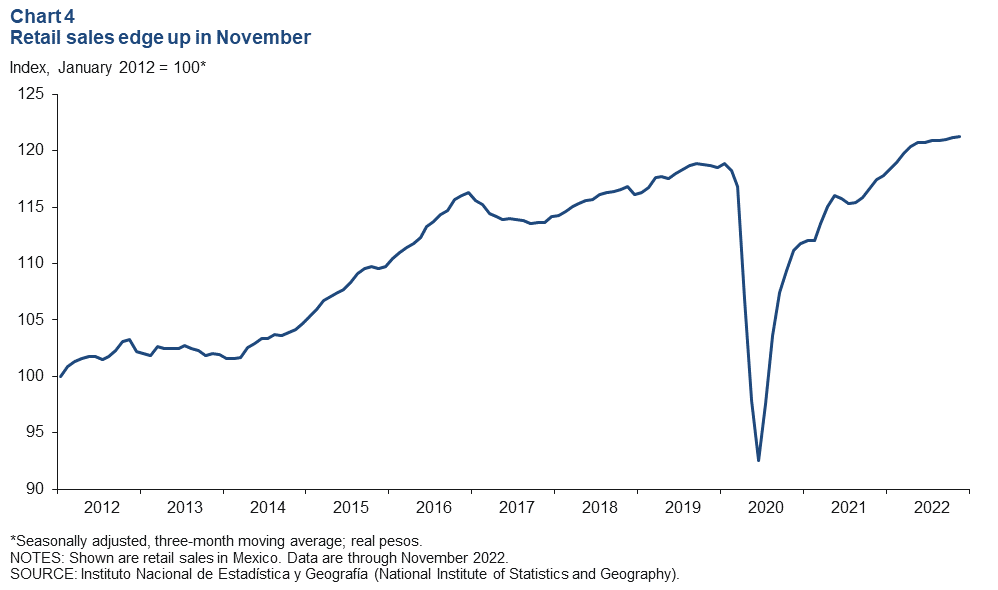

The three-month moving average of real retail sales rose 0.1 percent in November after rising 0.2 percent in October (Chart 4). On a month-over-month and unsmoothed basis, sales fell by 0.2 percent. Retail sales are still 3.7 percent above prepandemic levels despite sky-high inflation, perhaps due to record-high remittances.

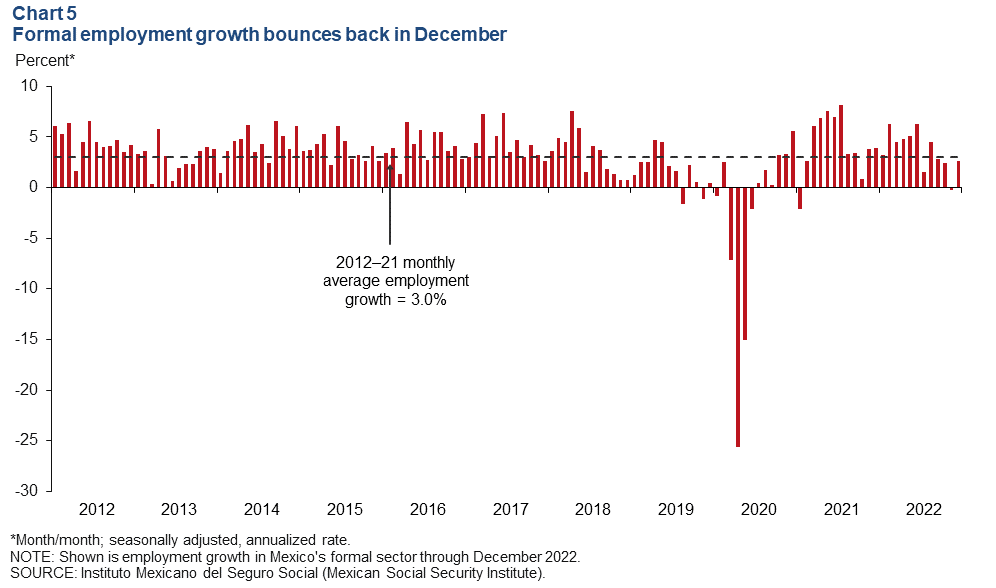

Employment rises in December

Formal sector employment—jobs with government benefits and pensions—rose an annualized 2.6 percent in December (47,000 jobs) after posting a decline of 0.3 percent in November (Chart 5). In 2022, employment grew 3.6 percent by adding 750,000 jobs during the year. Compared with prepandemic levels, employment was up 4.3 percent. Total employment, representing 57.4 million workers and including informal sector jobs, was up 2.9 percent year over year in the third quarter. The unemployment rate in December was 3.0 percent, unchanged from November’s reading.

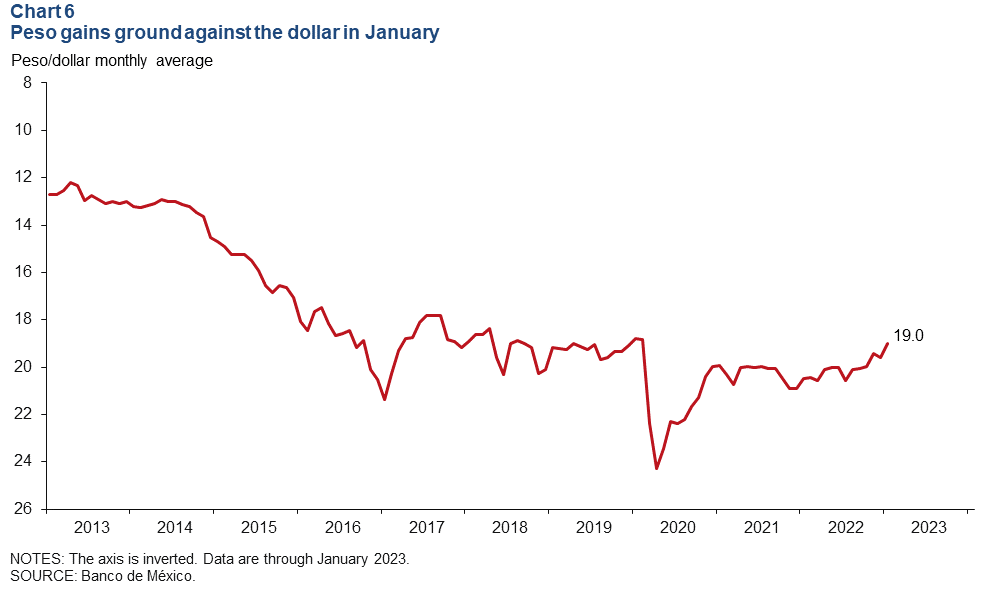

Peso strengthens further against the dollar in January

The Mexican currency averaged 19.0 pesos per dollar in January, stronger than December’s average of 19.6 pesos per dollar (Chart 6). In January, the peso was only 0.7 percent shy of its prepandemic value in February 2020 due to strong appreciation in the second half of 2022. The peso has been under pressure due to high inflation and increased uncertainty regarding domestic and global growth. However, it has remained relatively stable over the last two years as Mexico’s central bank has aggressively raised domestic interest rates in anticipation of and in response to U.S. interest rate hikes this year and stubbornly high inflation.

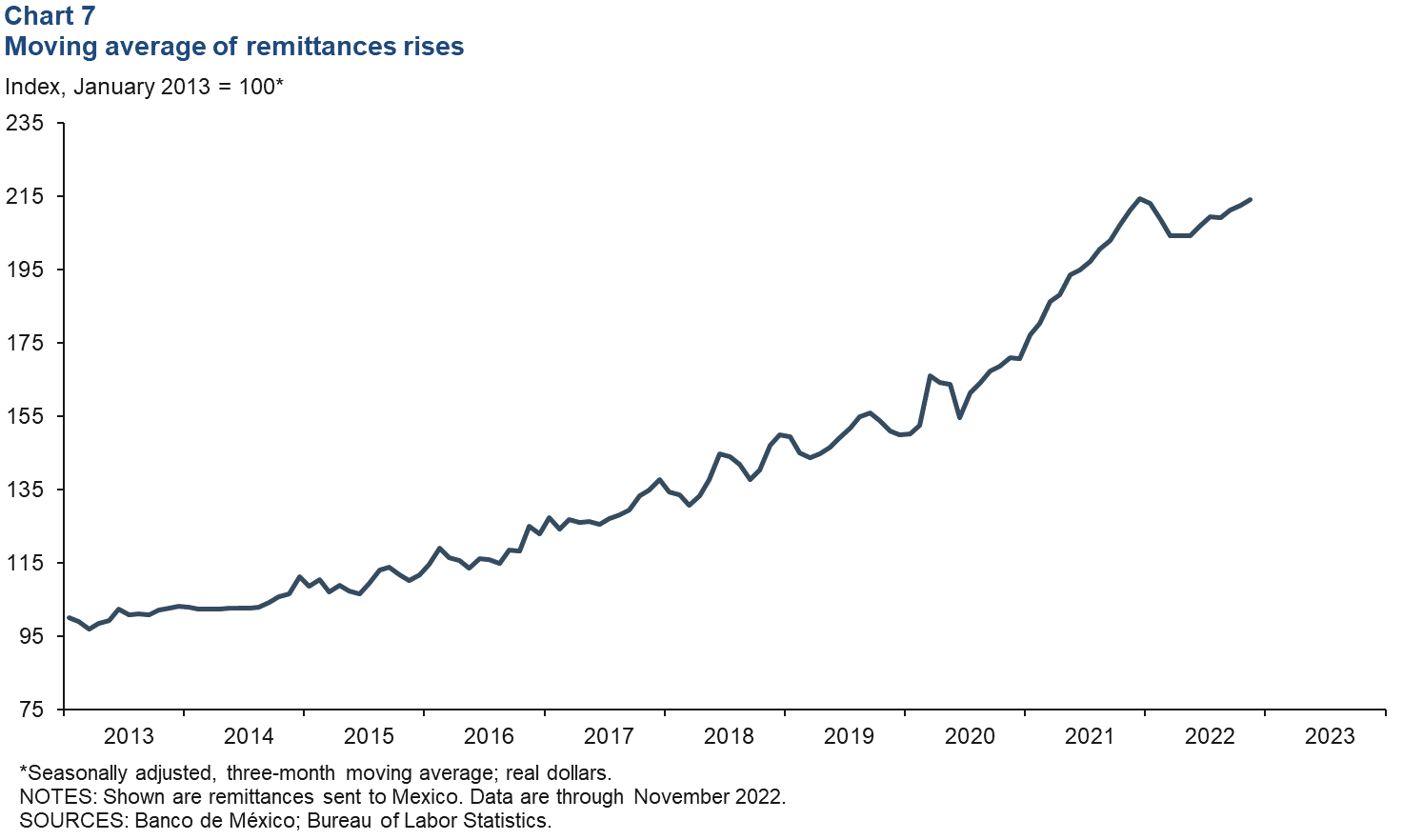

Remittances rise in November

The three-month moving average of real remittances rose by 0.7 percent in November after also rising 0.7 percent in October (Chart 7). On a month-over-month unsmoothed basis, remittances fell by 2.9 percent in November after rising 1.7 percent in October. Most likely, remittance flows to Mexico slowed at the beginning of 2022 due to high inflation in the U.S. and elsewhere, which eroded disposable income, including funds for remittances. However, remittances to Mexico bounced back in May and have been on an upward trend since then.

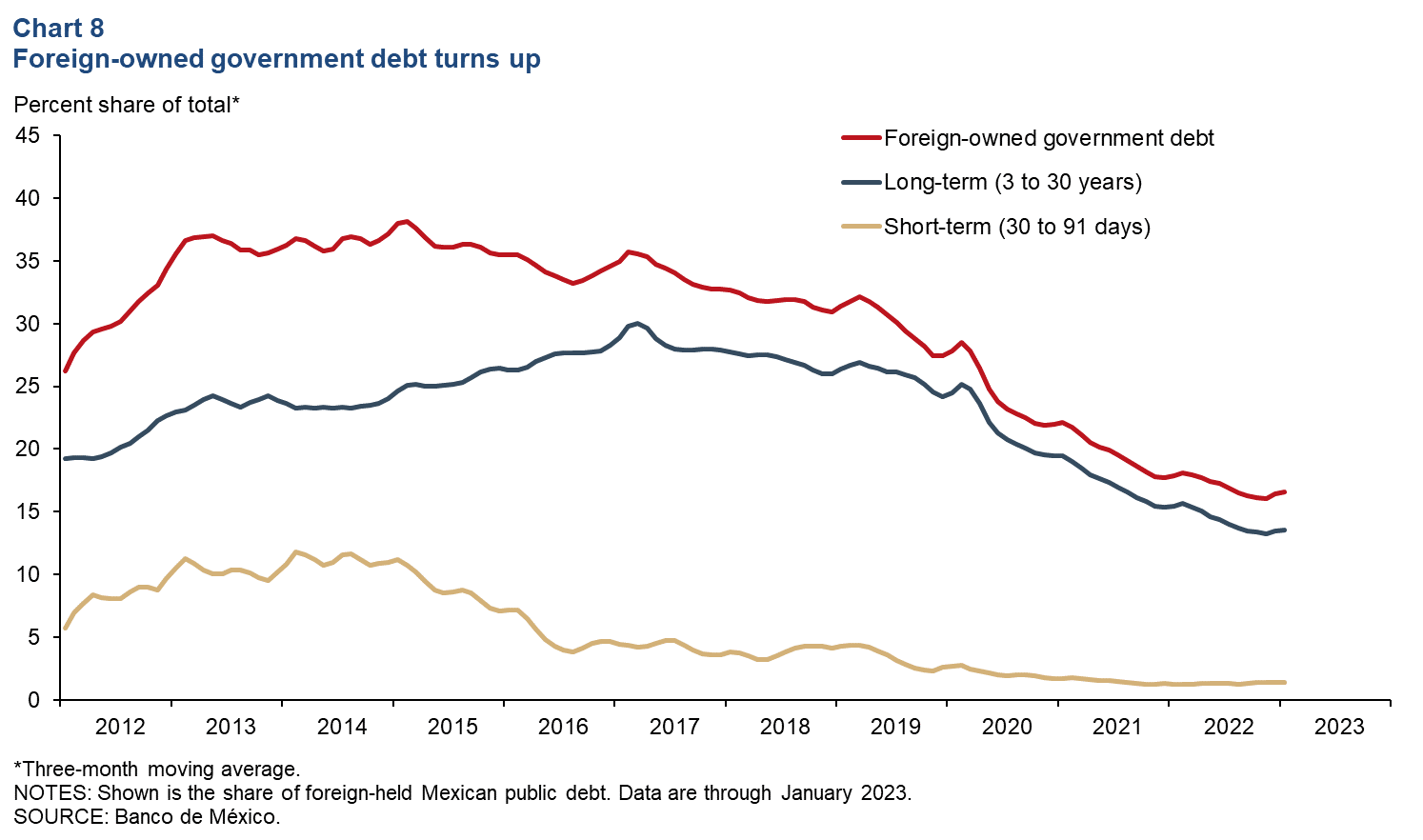

Foreign-owned debt ticks up in December

The three-month moving average of foreign-owned Mexican government securities ticked up to 16.6 percent in January (Chart 8). The extent of nonresident holdings of government debt is an indicator of Mexico’s exposure to international investors and a sign of confidence in the Mexican economy. It’s noteworthy that the measure has been on a downward trend since peaking in early 2015. Long-term government securities make up 82.0 percent of foreign‐owned Mexican public debt.

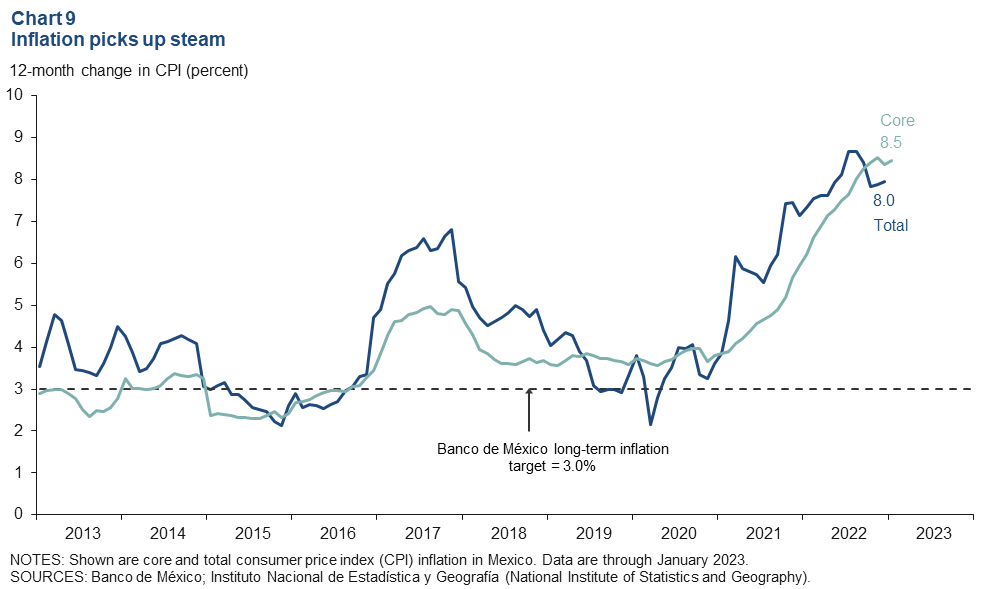

Inflation picks up in January

Mexico’s consumer price index (CPI) increased 8.0 percent in January over the prior 12 months, up from from December’s 7.9 percent rise. CPI core inflation, which excludes food and energy, rose further to 8.5 percent in the 12 months ending in January (Chart 9). On Feb. 9, Mexico’s central bank raised its benchmark interest rate by 50 basis points to 11.0 percent. Price growth in processed food, beverages and tobacco is pushing core inflation up and continues to worry policymakers at Mexico’s central bank. The central bank said that it could deliver a smaller hike at its next meeting, suggesting continued increases were in the pipeline.

About the Authors

Jesus Cañas

Cañas is a senior business economist in the Research Department at the Federal Reserve Bank of Dallas.

Ana Pranger

Pranger is a research analyst in the Research Department at the Federal Reserve Bank of Dallas

The views expressed are those of the authors and should not be attributed to the Federal Reserve Bank of Dallas or the Federal Reserve System.