Mexico’s economic momentum continues; outlook improves

| August 2023 economic report | |||

| GDP, real Q2 '23 |

Employment, formal August '23 |

CPI August '23 |

Peso/dollar September '23 |

| 3.4% q/q | 20,000 jobs m/m | 4.6% y/y | 17.3 |

Mexico’s real GDP grew at a revised annualized 3.4 percent in the second quarter, about the same as the previous quarter’s gains of 3.3 percent. This is the seventh consecutive quarter the Mexican economy has expanded, and growth is generally surprising to the upside. Given stronger-than-expected growth so far this year, the consensus forecast for 2023 GDP growth (fourth quarter, year over year) compiled by Banco de México rose to 2.4 percent in September (Table 1). Meanwhile, the average annual GDP growth forecast for 2023 rose from 3.0 percent in August to 3.2 percent in September.

| Table 1 Consensus forecasts for 2023 Mexico growth, inflation and exchange rate |

|||

| August | September | ||

| Real GDP growth in Q4, year over year | 2.1 | 2.4 | |

| Real GDP growth in 2023 | 3.0 | 3.2 | |

| CPI December 2023, year over year | 4.7 | 4.7 | |

| Peso/dollar exchange rate at end of year | 17.8 | 17.6 | |

| NOTE: CPI refers to the consumer price index. The survey period was Sept. 19–28. SOURCE: Encuesta sobre las Expectativas de los Especialistas en Economía del Sector Privado: Septiembre de 2023 (communiqué on economic expectations, Banco de México, September 2023). |

|||

The latest data available show industrial production, exports, retail sales and employment increased. Inflation continued easing, and the peso retreated some against the dollar in September.

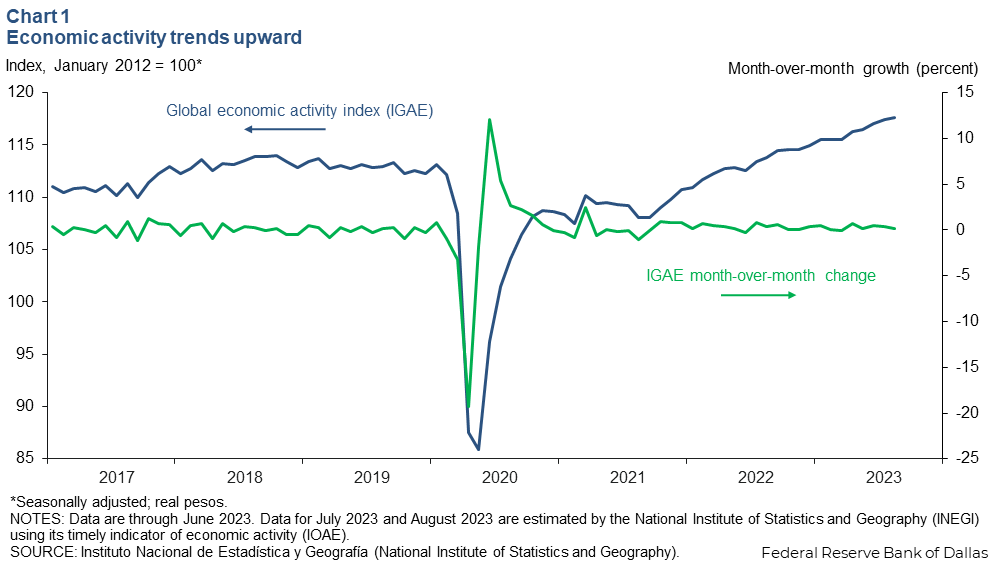

Economic activity improves

The global economic activity index (IGAE)—the monthly proxy for GDP growth—grew 0.2 percent month over month in August (Chart 1). The pickup in activity was mainly due to the goods-producing sector (including manufacturing, construction and utilities), which increased 0.5 percent in July and 0.2 percent in August. Growth in service-related activities (including trade and transportation) was steady at 0.2 percent in July and August. The IGAE rose 3.4 percent year over year in August.

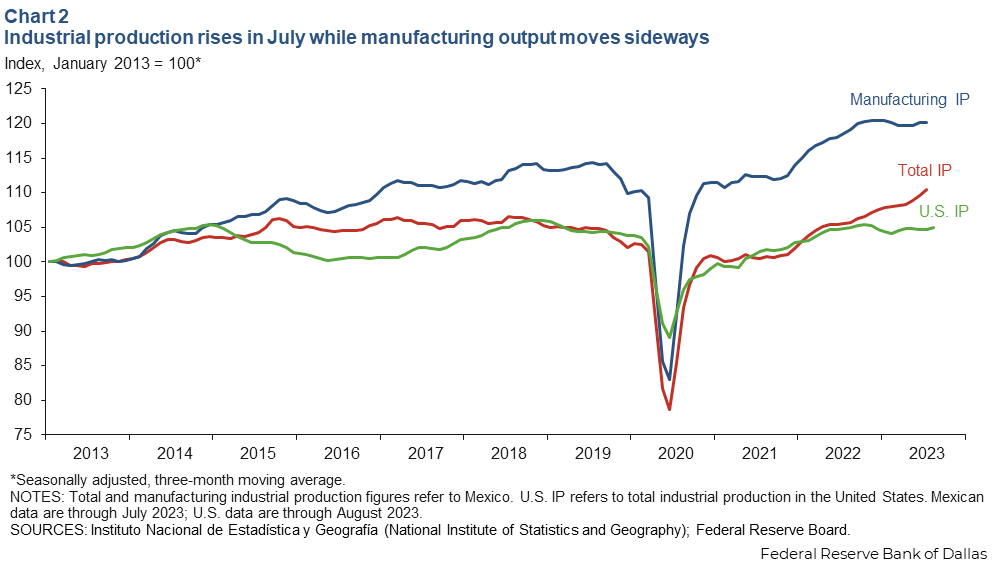

Industrial production picks up

The three-month moving average of Mexico’s industrial production (IP) index, which includes manufacturing, construction, oil and gas extraction, and utilities, rose 0.7 percent in July, while the smoothed manufacturing IP index was flat (Chart 2). North of the border, the smoothed U.S. IP index grew 0.2 percent in August after holding steady in July. U.S. and Mexican IP have become more correlated with the rise of intra-industry trade between the two countries since the early 1990s. If U.S. consumer demand decelerates further this year in an environment of elevated inflation and higher credit costs, Mexico’s manufacturing sector could slow.

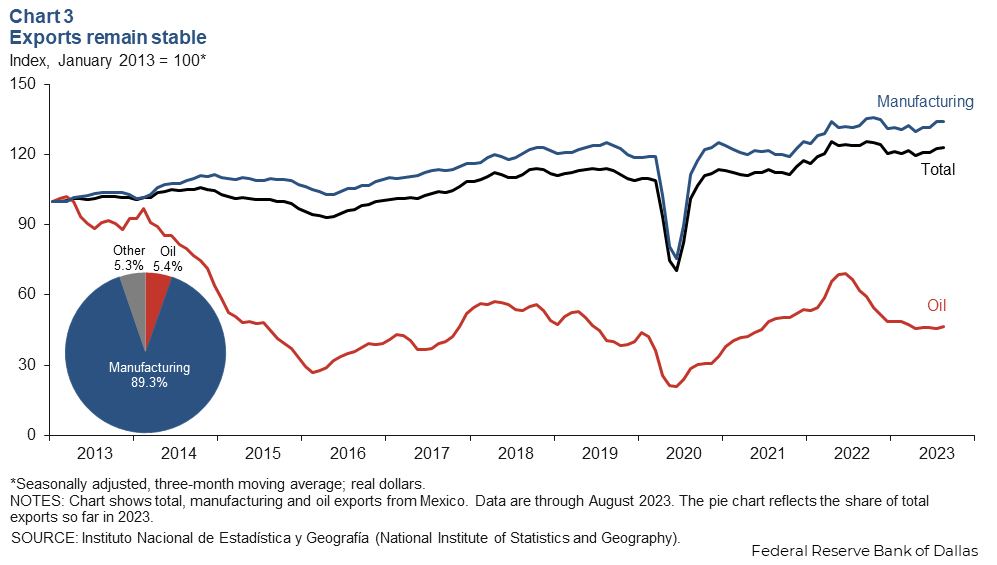

Exports little changed

The three-month moving average of total Mexico exports increased 0.3 percent in August while oil exports grew 2.1 percent. The much larger manufacturing sector edged up 0.1 percent (Chart 3). Year to date through August, total exports dropped 0.8 percent, with manufacturing exports increasing 1.3 percent and oil exports falling 25.5 percent compared with the same period in 2022. The overall decline is likely due to slowing global demand.

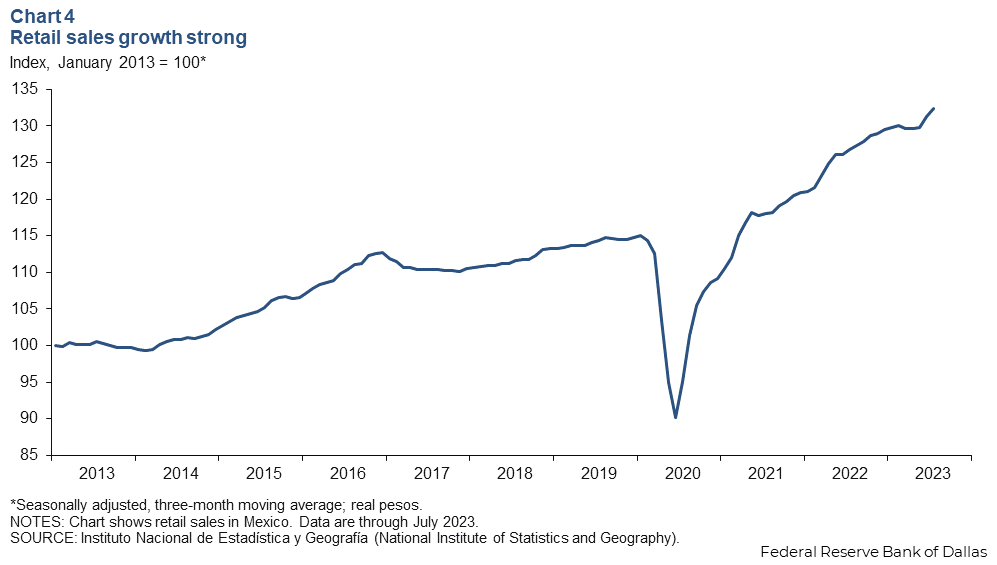

Retail sales continue to climb

The three-month moving average of real retail sales jumped 0.8 percent in July, the latest data available (Chart 4). Year over year, the smoothed retail sales index was up 2.8 percent. Sustained growth in remittance flows may be contributing to the elevated level of Mexican retail spending despite high domestic inflation. Mexico’s domestic market has been relatively strong and could help mitigate a fall in manufacturing exports if the U.S. economy slows down.

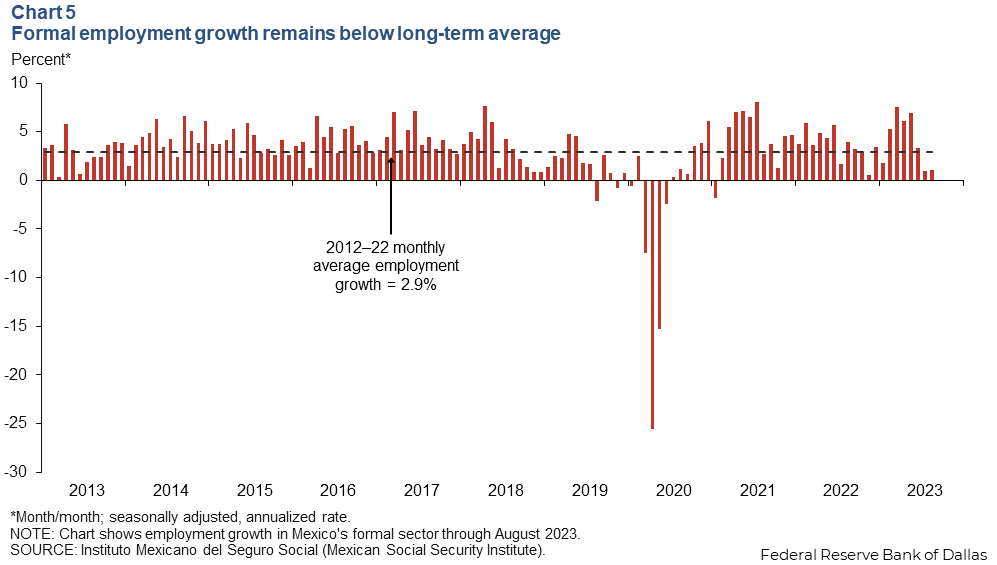

Job gains sluggish in August

Formal sector employment—jobs with government benefits and pensions—grew an annualized 1.1 percent (20,000 jobs) in August (Chart 5). Total employment, representing 58.5 million workers and including informal sector jobs, was up 1.9 percent year over year in second quarter 2023. The unemployment rate in August was 2.7 percent, down from 2.9 percent in July.

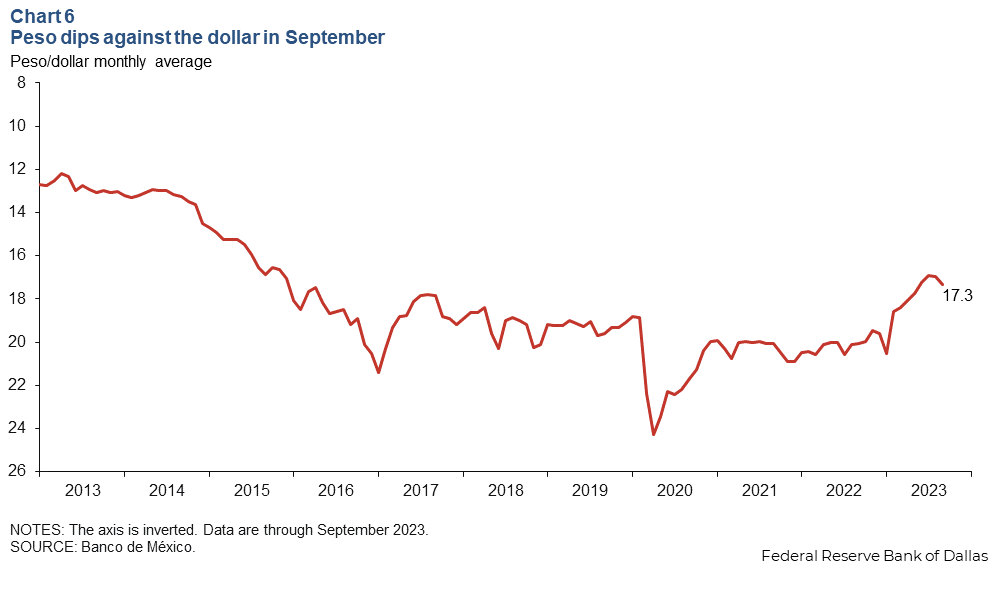

Peso ticks down in September

The Mexican currency averaged 17.3 pesos per dollar in September, below August’s average of 17.0 pesos per dollar (Chart 6). The peso weakened slightly after strengthening for six months in a row. Mexico’s solid macroeconomic framework, fiscal discipline and prospects for nearshoring investment likely have contributed to the peso appreciation and stability this year.

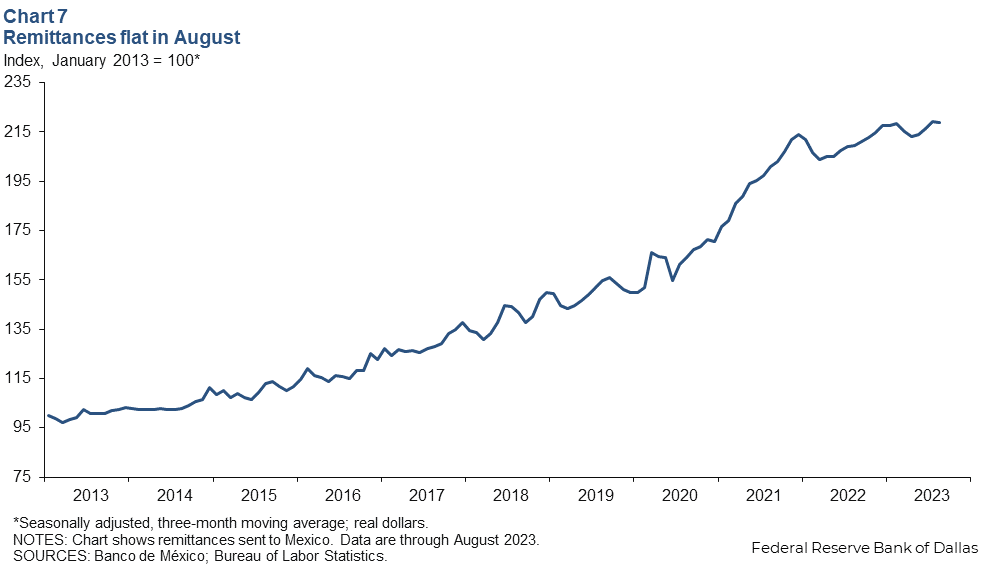

Remittances stay elevated

The three-month moving average of real remittances to Mexico was little changed in August after increasing 1.4 percent in July (Chart 7). Remittances are close to record highs as U.S. job growth remains strong, boosting the capacity of Mexicans working abroad to send money back home.

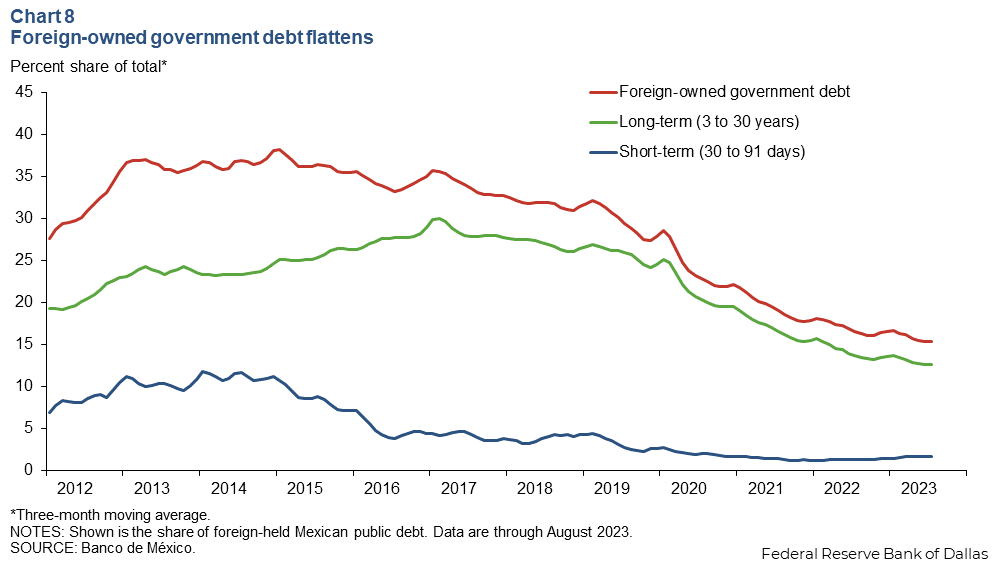

Foreign-owned debt holds steady

The three-month moving average of foreign‐owned Mexican government securities held steady in August after consistently falling since March 2023 (Chart 8). The extent of government debt held by nonresidents is an indicator of Mexico’s exposure to international investors and a sign of confidence in the Mexican economy. The measure has been on a downward trend since 2015. Long-term government securities make up 82 percent of foreign-owned Mexican public debt.

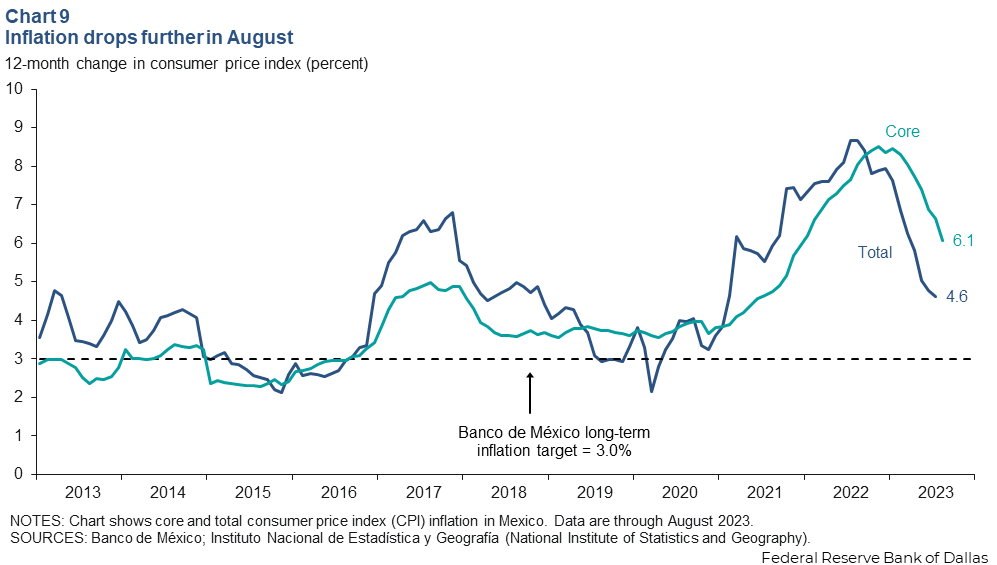

Inflation continues slowing in August

Mexico’s consumer price index (CPI) increased 4.6 percent in August, slower than July’s 4.8 percent rise (Chart 9). CPI core inflation, which excludes food and energy, also slowed, to 6.1 percent. In September, Mexico’s central bank kept its benchmark interest rate steady at 11.25 percent. The central bank noted in a statement that the diminishing negative impact resulting from the pandemic and geopolitical conflicts, along with the tight monetary policy stance, have contributed to inflation’s downward trend. The central bank expects inflation to converge to the 3 percent target by second quarter 2025.

About the authors

Jesus Cañas is a senior business economist in the Research Department at the Federal Reserve Bank of Dallas.

Diego Morales-Burnett is a research analyst in the Research Department at the Federal Reserve Bank of Dallas

The views expressed are those of the authors and should not be attributed to the Federal Reserve Bank of Dallas or the Federal Reserve System.