Mexico’s economy shows mixed signals toward end of 2023

| December 2023 economic report | |||

| GDP, real Q3 '23 |

Employment, formal December '23 |

CPI December '23 |

Peso/dollar December '23 |

| 3.6% q/q | 35,214 jobs m/m | 4.7% y/y | 17.2 |

Mexico’s economy likely grew more than 3 percent in 2023 as the proxy for monthly GDP increased for the ninth consecutive month in November. The consensus forecast for 2023 GDP growth (fourth quarter, year over year) compiled by Banco de México remained the same at 3.1 percent in December (Table 1).

| Table 1 Consensus forecasts for 2023 Mexico growth, inflation and exchange rate |

|||

| November | December | ||

| Real GDP growth in Q4, year over year | 3.1 | 3.1 | |

| Real GDP growth in 2023 | 3.4 | 3.4 | |

| CPI December 2023, year over year | 4.5 | 4.4 | |

| Peso/dollar exchange rate at end of year | 17.7 | 17.6 | |

| NOTE: CPI refers to the consumer price index. The survey period was Nov. 6–13.

SOURCE: Encuesta sobre las Expectativas de los Especialistas en Economía del Sector Privado: Diciembre de 2023 (communiqué on economic expectations, Banco de México, December 2023). |

|||

The latest data available, however, were mixed as exports and retail sales fell while industrial production increased, and employment growth continued to be sluggish. Inflation ticked up, and the peso gained ground against the dollar in December.

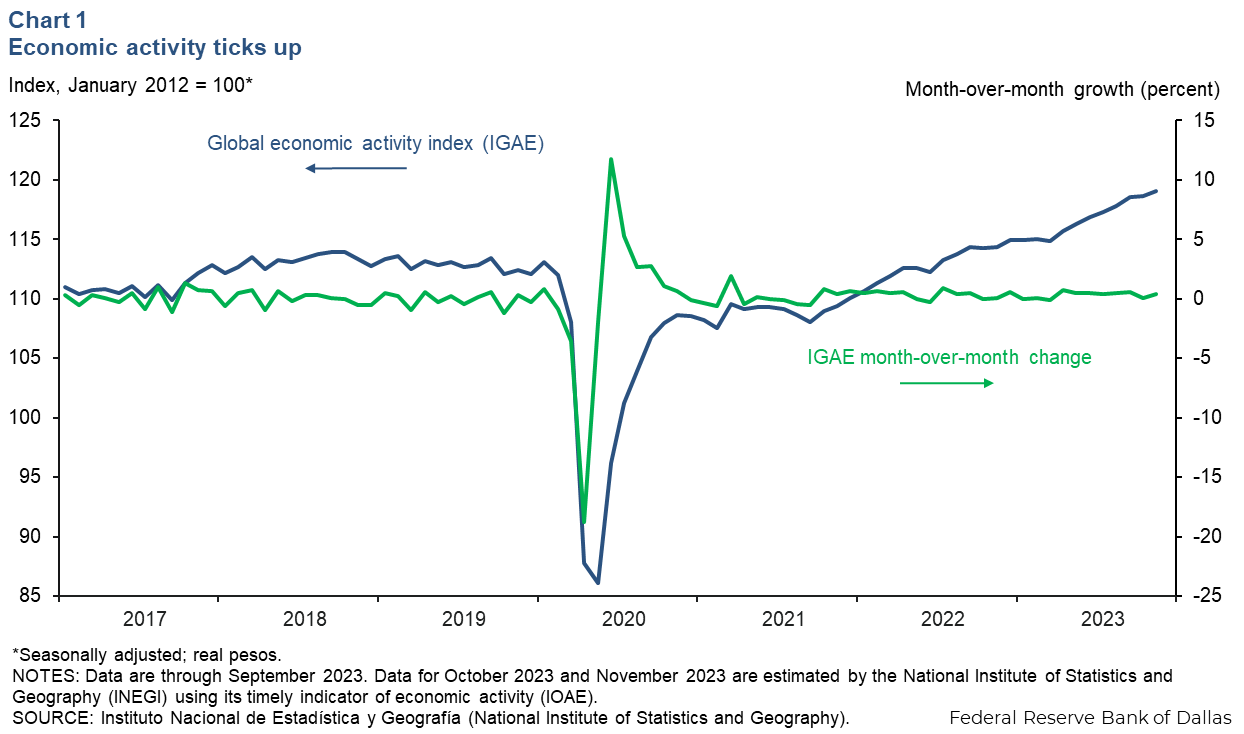

Economic activity rises in November

The global economic activity index (IGAE)—the monthly proxy for GDP growth—rose 0.4 percent month over month in November, up from October’s growth of 0.1 percent (Chart 1). Both the goods-producing sector (including manufacturing, construction and utilities) and the service-providing sector (which includes trade and transportation) increased 0.4 percent in November. On a year-over-year basis, IGAE was up 4.2 percent in November, an uptick from October’s 3.8 percent increase.

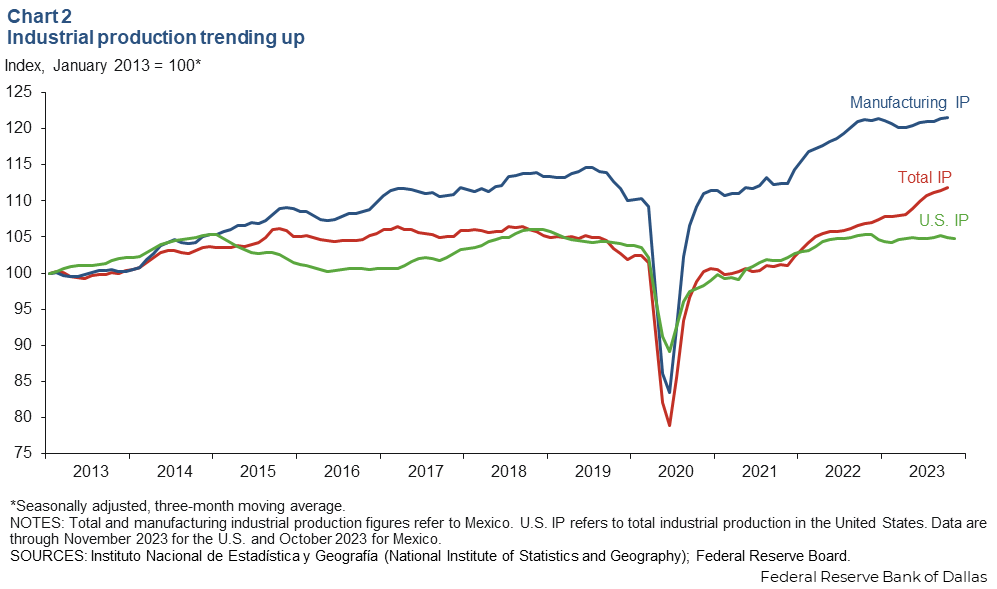

Industrial production picks up

In October, the three-month-moving average of Mexico’s industrial production (IP) index—which includes manufacturing, construction, oil and gas extraction, and utilities—grew 0.4 percent, while manufacturing alone increased 0.2 percent (Chart 2). North of the border, U.S. IP was down 0.2 percent in November after declining 0.3 percent in October. The correlation between IP in Mexico and the U.S. has increased considerably with the rise of intra-industry trade between the two countries since the early 1990s. Mexico’s manufacturing sector could slow down, particularly if U.S. consumer demand decelerates because of high inflation and interest rates.

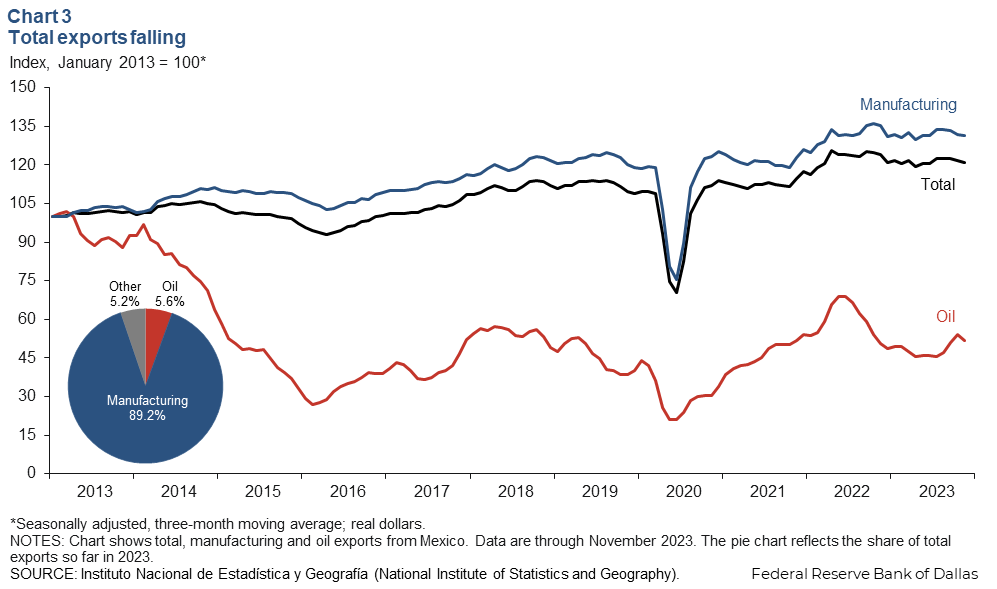

Exports down in November

The three-month moving average of total Mexico exports ticked down 0.7 percent in November (Chart 3). The large manufacturing sector edged down 0.5 percent, and oil exports fell 3.8 percent. Year to date through November, total exports increased 0.2 percent, with oil exports up 7.0 percent and manufacturing up 0.1 percent.

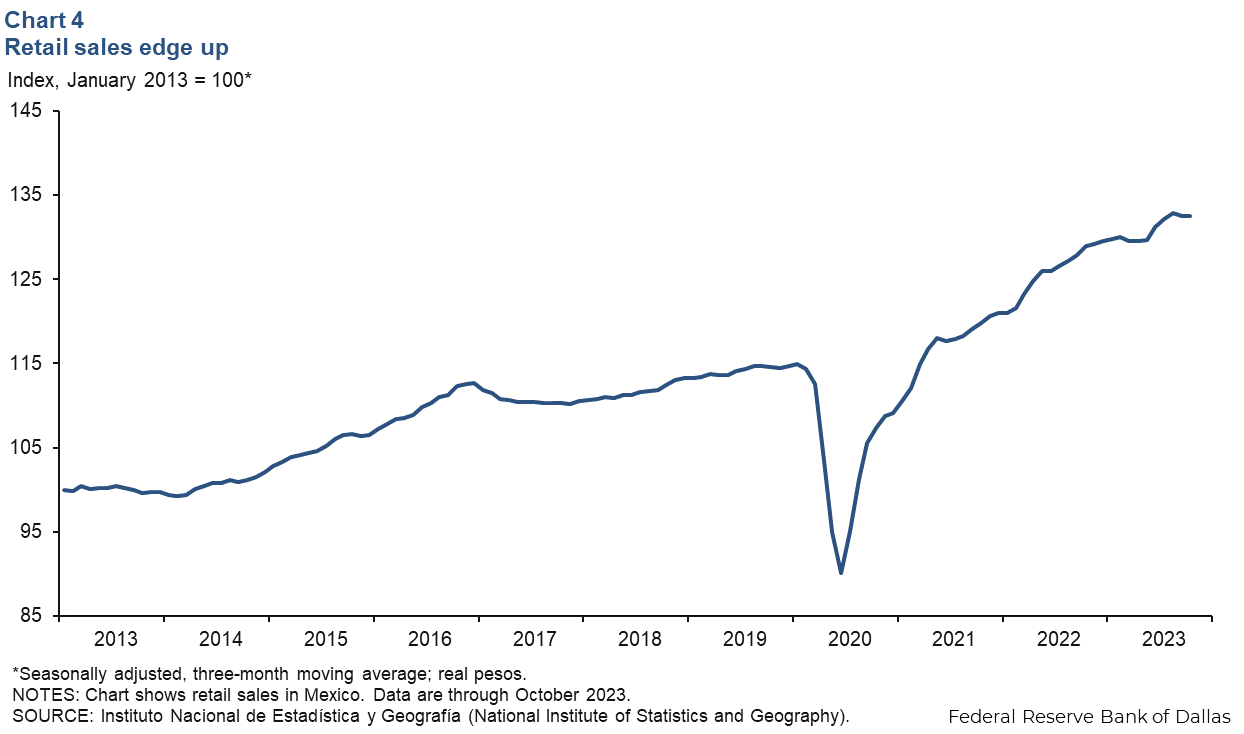

Retail sales increase

The three-month moving average of real retail sales ticked up 0.3 percent in October, the latest data available (Chart 4). The smoothed retail sales index was up 2.8 percent year over year. Sustained growth in remittance flows may be contributing to the elevated level of Mexican retail spending despite high domestic inflation.

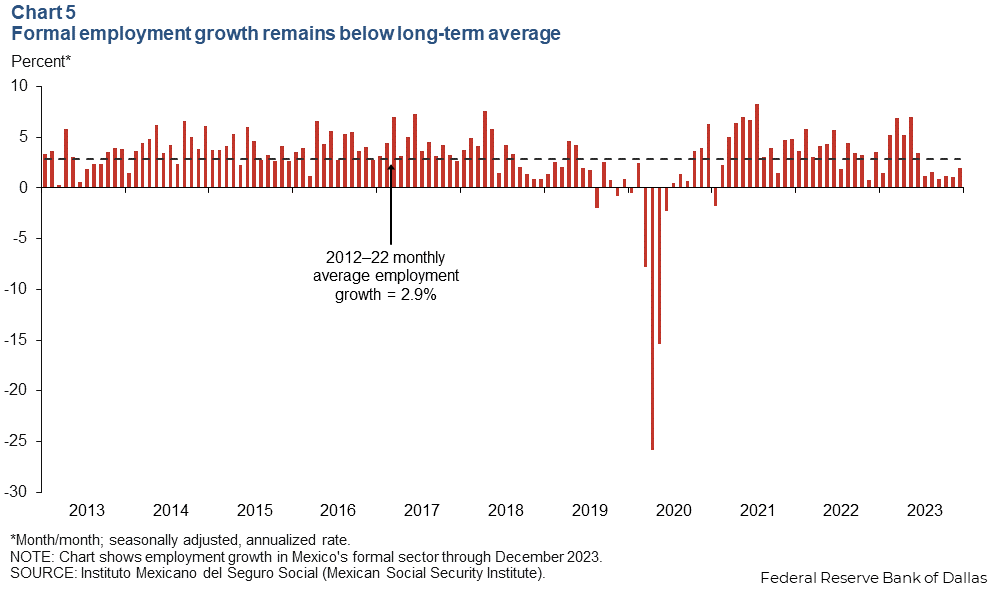

Job gains remain sluggish in December

Formal sector employment—jobs with government benefits and pensions—grew an annualized 1.9 percent (35,000 jobs) in December (Chart 5). Total employment, representing 59.2 million workers and including informal sector jobs, was up 3.0 percent year over year in the third quarter. The unemployment rate in November was 2.8 percent, up from 2.7 percent in October.

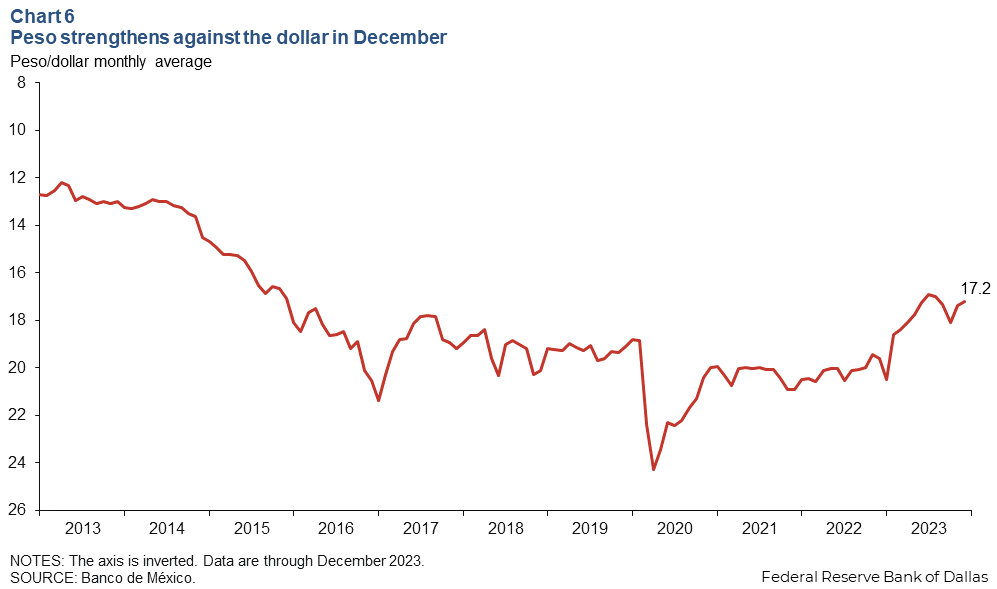

Peso ticks up

The Mexican currency averaged 17.2 pesos per dollar in December, below November’s average of 17.4 pesos per dollar (Chart 6). Mexico’s solid macroeconomic framework, fiscal discipline and prospects for nearshoring investment likely have contributed to the peso appreciation and stability in 2023.

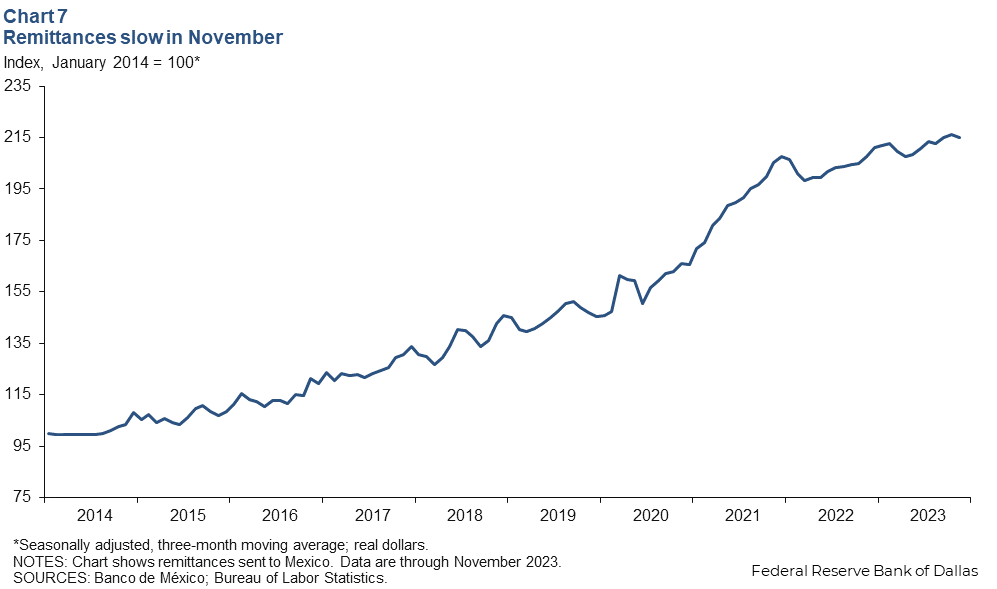

Remittances remain elevated

The three-month moving average of real remittances to Mexico fell 0.5 percent in November after a 0.5 percent increase in October (Chart 7). Nevertheless, remittances are near record highs as U.S. job growth remains strong, boosting the capacity of Mexicans working abroad to send money back home.

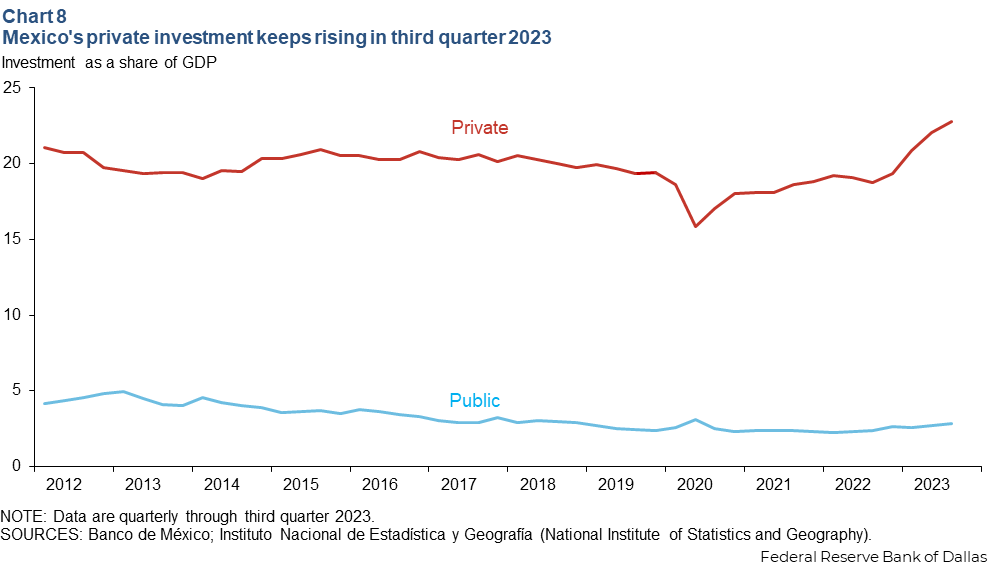

Domestic investment growth consolidates in 2023

Private investment has been on an upward trend since the end of the pandemic, reaching prepandemic levels in third quarter 2021. Private investment was 22.8 percent of GDP in third quarter 2023, up from 18.6 percent in first quarter 2020 (Chart 8). In addition, public investment is finally growing after years of decline, and it has stabilized at 2.8 percent of GDP. The increase in private investment is due to investment catching up after many projects were suspended due to the pandemic. A strong peso also makes imports of machinery and equipment less expensive, and companies are taking this opportunity to replace dated equipment. Finally, some of this domestic investment is in preparation for nearshoring projects, according to multiple sources.

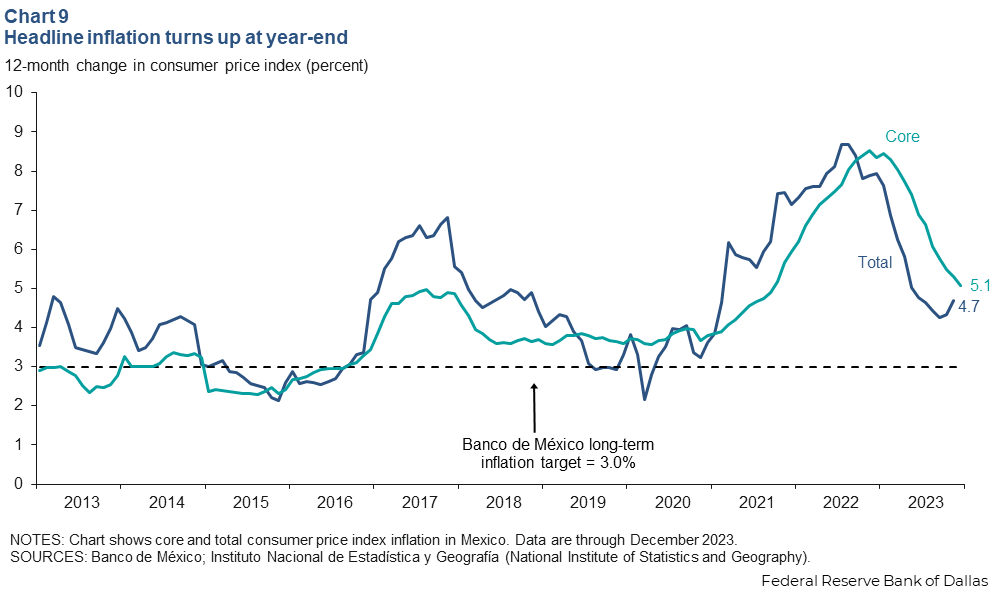

Inflation ticks up

Mexico’s consumer price index (CPI) increased 4.7 percent in December, faster than November’s 4.3 percent rise (Chart 9). However, CPI core inflation, which excludes food and energy, slowed to 5.1 percent. In December, Mexico’s central bank kept its benchmark interest rate steady at 11.25 percent for the sixth consecutive meeting. The central bank noted in a statement that although the inflation outlook remains complicated, progress on lowering the rate of inflation has been made. However, the central bank reiterated that the benchmark interest rate will be held at the current level for some time.

About the authors

Jesus Cañas is a senior business economist in the Research Department at the Federal Reserve Bank of Dallas.

Diego Morales-Burnett is a research analyst in the Research Department at the Federal Reserve Bank of Dallas

The views expressed are those of the authors and should not be attributed to the Federal Reserve Bank of Dallas or the Federal Reserve System.