Mexico’s economy continues growing through second quarter

| May 2024 economic report | |||

| GDP, real Q1 '24 |

Employment, formal May '24 |

CPI May '24 |

Peso/dollar June '24 |

| 1.1% q/q | 35,264 jobs m/m | 4.7% y/y | 18.2 |

Mexico’s economy continued growing steadily through the second quarter, according to the monthly GDP proxy. However, high inflation and the recent increase in political uncertainty remain headwinds for the Mexican economy. Despite these challenges, the consensus forecast for 2024 GDP growth (fourth quarter/fourth quarter), compiled by Banco de México, remained around 2 percent in May (Table 1).

| Table 1 Consensus forecasts for 2024 Mexico growth, inflation and exchange rate |

|||

| April | May | ||

| Real GDP growth in Q4, year over year | 2.2 | 2.1 | |

| Real GDP growth in 2024 | 2.2 | 2.1 | |

| CPI December 2024, year over year | 4.2 | 4.3 | |

| Peso/dollar exchange rate at end of year | 17.9 | 17.8 | |

| NOTE: CPI refers to the consumer price index. The survey period was May 23–29.

SOURCE: Encuesta sobre las Expectativas de los Especialistas en Economía del Sector Privado: Mayo de 2024 (communiqué on economic expectations, Banco de México, May 2024). |

|||

The latest data available show industrial production was flat, while exports and retail sales increased. Employment also grew but at a slower rate than the previous month. The peso lost value against the dollar, and inflation remained elevated.

Output steadily increasing

The global economic activity index (IGAE)—the monthly proxy for GDP growth—rose a mere 0.3 percent month over month in May after falling 0.3 percent in April (Chart 1). Both the goods-producing sector (including manufacturing, construction and utilities) and service-related activities (including trade and transportation) increased 0.4 percent. The IGAE was up 2.0 percent year over year.

Industrial production flat

The three-month moving average of Mexico’s industrial production (IP) index, which includes manufacturing, construction, oil and gas extraction, and utilities, did not change in April (Chart 2). Manufacturing IP declined 0.1 percent. North of the border, the three-month moving average of U.S. IP was up slightly (0.2 percent) in May.

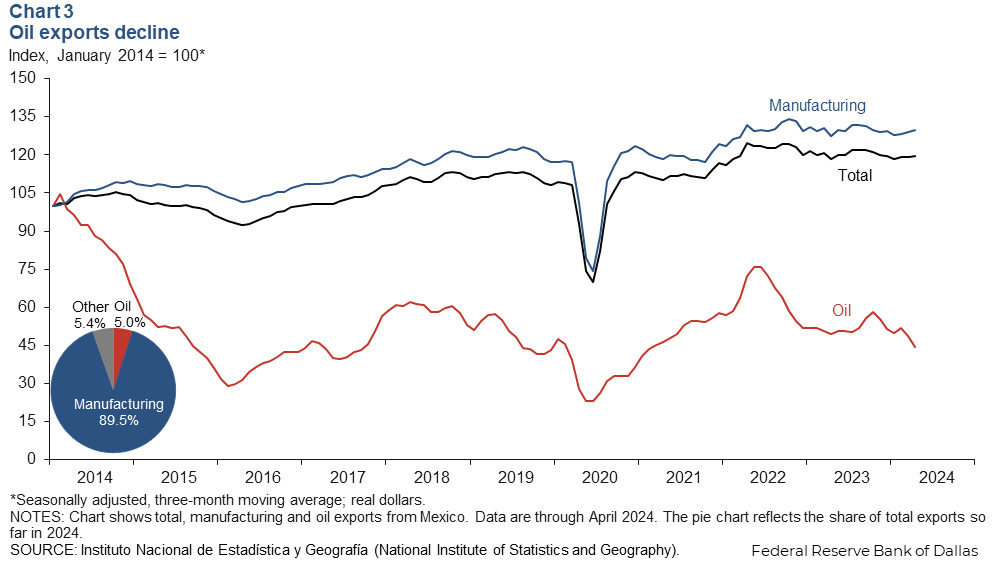

Exports tick up

The three-month moving average of total Mexico exports edged up 0.1 percent in April (Chart 3). While the much-larger manufacturing sector increased 0.6 percent, oil exports fell 9.3 percent in April. Total exports fell 1.1 percent during the first four months of 2024 compared with the same period a year ago, with oil exports down 8.7 percent and manufacturing down 0.7 percent.

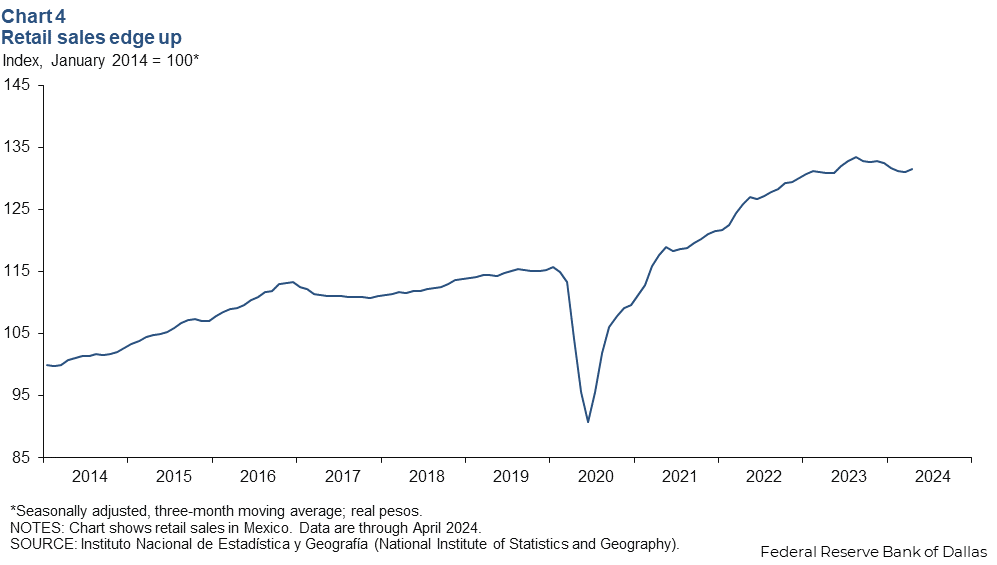

Retail sales rise in April

The three-month moving average of real retail sales increased 0.3 percent in April, the latest data available (Chart 4). In addition, the smoothed retail sales index was up 0.5 percent year over year.

Payroll expansion slows

Formal sector employment, meaning jobs with government benefits and pensions, grew an annualized 1.9 percent (35,000 jobs) in May, after strong growth the previous month (Chart 5). Total employment, representing 59.1 million workers and including informal sector jobs, was up 1.1 percent year over year in the first quarter. The unemployment rate held steady at 2.6 percent in April.

Peso loses ground against the dollar in June

The Mexican currency averaged 18.2 pesos per dollar in June, down from May’s value of 16.8 pesos per dollar (Chart 6). The peso has been trending up steadily since early 2022; however, it depreciated 8 percent in June as a result of volatility after Mexico’s presidential election and the possibility of a judicial reform proposed by the outgoing administration.

Peso real exchange rate above long-term average

The real exchange rate measures how expensive a foreign country is relative to the home country at the prevailing nominal exchange rate. Therefore, a country’s real exchange rate is often expected to gravitate toward its long-term average in order to avoid significant trade and foreign investment distortions. Mexico’s real exchange rate was 27 percent above its long-term average as of April 2024 (Chart 7). The recent depreciation of the peso in June could help reduce that gap.

Remittances to Mexico edge up in April

The three-month moving average of real remittances to Mexico increased 0.7 percent in April after falling 2.6 percent in March (Chart 8). Total remittances through April were down 0.3 percent compared with the same period a year ago. The U.S. economy is expected to experience slower employment growth this year, which may further impact the capacity of Mexicans working abroad to send money back home.

Inflation continues to be elevated

Mexico’s CPI moved slightly down to 4.7 percent in May from the prior 12 months, less than the 4.8 percent reading in April (Chart 9). CPI core inflation, which excludes food and energy, continued slowing, to 4.2 percent. CPI core inflation has slowed since early 2023; however, services inflation persists, keeping overall inflation above the central bank’s 3.0 percent target rate. In June, Mexico’s central bank kept the overnight rate constant at 11.0 percent. In the statement, the central bank said the disinflationary process is likely to continue due to the ongoing weakness in the economy. However, the recent peso depreciation is pushing up the inflation forecasts, they noted.

About the authors

Jesus Cañas is a senior business economist in the Research Department of the Federal Reserve Bank of Dallas.

Diego Morales-Burnett is a research analyst in the Research Department at the Federal Reserve Bank of Dallas.