Auto industry on road to recovery from pandemic

COVID-19 has sent shockwaves through every part of the economy, including the passenger-vehicle market. After a series of disruptions in March and April that coincided with the widespread viral outbreak in the U.S., the auto industry has entered a recovery period, though its path forward remains uncertain.

Overcoming supply shortages during early pause

The greatest initial concern for the industry during the pandemic was the threat of supply shortages. The virus first appeared overseas, where factories producing parts and equipment shut down. COVID-19 broadly hit the U.S. in March, its impact spreading across the market.

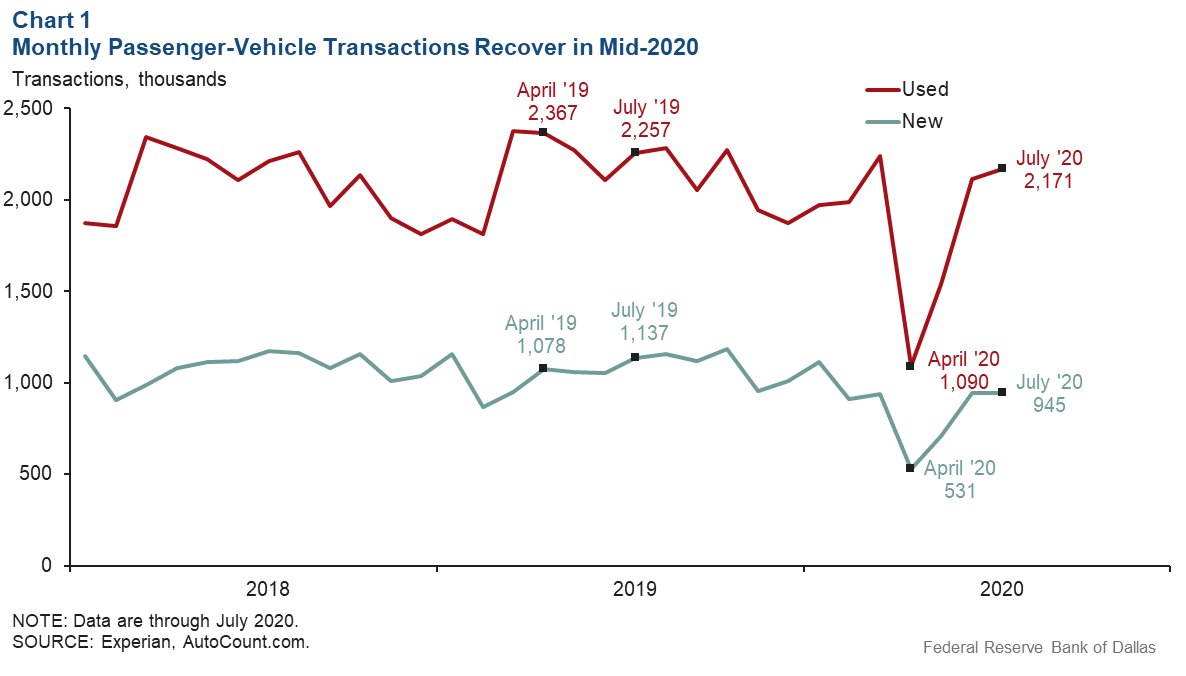

Vehicle manufacturers reacted by closing or slowing operations and laying off or furloughing workers. Dealer activities diminished, and consumer demand plummeted. U.S. vehicle transactions in April were down 53 percent from prior-year levels, according to AutoCount market reports by Experian, best known for its credit reports (Chart 1). This decline was consistent for both new vehicles (down 51 percent) and used ones (down 54 percent). Vehicles financed in April 2020 were 48 percent below April 2019 levels, while leases were down 61 percent.

Market quickly adapts

As the economy gradually reopened during the summer following its near shutdown in the spring, vehicle sales began climbing toward pre-COVID-19 levels. The number of both new- and used-vehicle transactions in July returned to January and February levels—before the widescale outbreak in the U.S. Used vehicles in particular rebounded robustly, with July sales just 4 percent below year-ago levels. New vehicles remained down 17 percent. Several factors have contributed to the overall bounce back.

Many essential workers seeking to avoid infection turned away from ridesharing and public transit, as a personal vehicle became viewed as one of the safest ways to get around in a pandemic. Even the use of micro-mobility modes of transportation—shared bikes, scooters and skateboards—by urban dwellers declined sharply across major U.S. cities.

Although fewer people need to commute to work because many office workers are telecommuting, a recent study shows that residents in large cities may want to escape perceived virus hotbeds for short getaways or move to less-populated areas. Consumers often fear that traveling by airplane or train may carry health risks and view road trips in private vehicles to work or vacation destinations as a safe alternative. Some consumers are buying their first cars.

Moreover, many consider owning a vehicle less costly than before, the result of added consumer cash via federal fiscal stimulus checks and low gasoline prices.

Lower borrowing rates have provided additional incentives—the average auto loan interest rate in June 2020 was 4.9 percent, 1.2 percentage points lower than prior-year levels for new vehicles. Interest rates on used vehicles averaged 9.2 percent, down almost a half-percentage point. At the same time, the average length of a loan rose by one month for new and used vehicles, to 67 months.

Tight inventories impact vehicle affordability

Automakers have tried to meet the increasing demand by boosting production, which had been disrupted in the spring and left inventories low. However, new- and used-vehicle inventories remain tight. Because demand has outpaced supply, the price for new and used vehicles is rising.

Comparing June 2020 with June 2019, the average amount financed increased to $35,637 from $32,346 for new vehicles and to $20,969 from $20,371 for used ones. This is not a deviation from the trend—prices have increased in the past several years. However, the jump in 2020 was more than $3,000 for new vehicles, much larger relative to previous years.

Not surprisingly, the average loan-to-value of new vehicles purchased increased by 4 percentage points while slipping 1 percentage point for used vehicles. Despite the lower average interest rate and longer average loan terms, auto loan borrowers—especially those who purchased a new vehicle—are paying more each month.

The impact of the pandemic on individuals has varied largely across education levels, race and ethnicity, as well as industries of employment. The incomes of those with lower public-contact jobs have not changed much from the pre-pandemic period, while others face greater uncertainties moving forward.

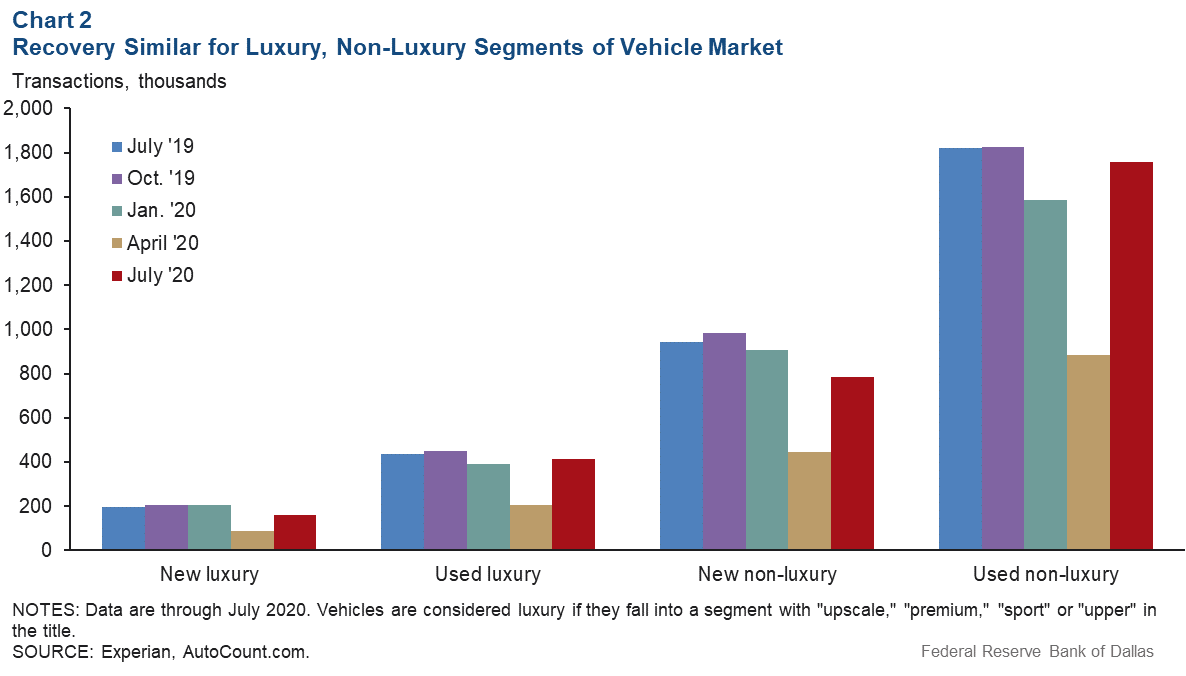

Some argue that the end of the pandemic recession may be a K-shaped recovery—higher-income professional workers are recovering well, while low-wage workers continue to struggle. This trend hasn’t been apparent in the auto market. Sales in luxury segments have bounced back; the recovery in non-luxury segments has been similarly strong (Chart 2).

Automakers are striving to meet the higher-end demand. But on the other end of the spectrum, financial distress can be overwhelming for those who need a vehicle for work and to get around and cannot find affordable options.

Disconcerting auto loan repayment trend

The total outstanding auto loan balance was $1.34 trillion at the end of June 2020, according to the New York Fed Consumer Credit Panel/Equifax. This auto loan balance accounted for 9.4 percent of all consumer loan debt in the U.S.—ranking third behind mortgages and student loans.

The serious delinquency rate—the percent of those loans 90-plus days past due–has hovered around 20 percent for auto loans taken out by subprime consumers who had an Equifax risk score lower than 620. More borrowers took out loans exceeding the value of the vehicles that they purchased, and many borrowers chose lower monthly payments at the expense of longer terms.

The delinquency rate has not increased from pre-COVID levels possibly because of a combination of lender accommodation and consumers choosing to pay down outstanding loan balances with stimulus payment proceeds.

Consumer, lender behaviors cloud future prospects

Some vehicle loans are pooled together into securities that are then sold to investors. When that occurs, it’s difficult for borrowers to modify their interest rate or loan amount through their lenders. Also, the underwriting of auto loans has become more stringent since May, after a loosening in March and April. New loans are more likely to be originated to prime borrowers. Lenders expect the performance of existing loans to deteriorate as federal stimulus and lender accommodation ends.

The auto market has been recovering from the initial shock from the COVID-19 pandemic as consumers and firms shift their behaviors. The recovery path is still full of uncertainties as the pandemic evolves and federal and local public policies respond.

About the Authors

Carlee Crocker

Crocker is a research analyst in the Research Department at the Federal Reserve Bank of Dallas.

Wenhua Di

Di is a senior research economist in the Research Department of the Federal Reserve Bank of Dallas.

The views expressed are those of the authors and should not be attributed to the Federal Reserve Bank of Dallas or the Federal Reserve System.