Oil market’s tightening in February seemingly defies fundamentals

Surging oil prices in February have raised hopes that the worst may be over for oil markets, though recent evidence suggests that the recovery will not last.

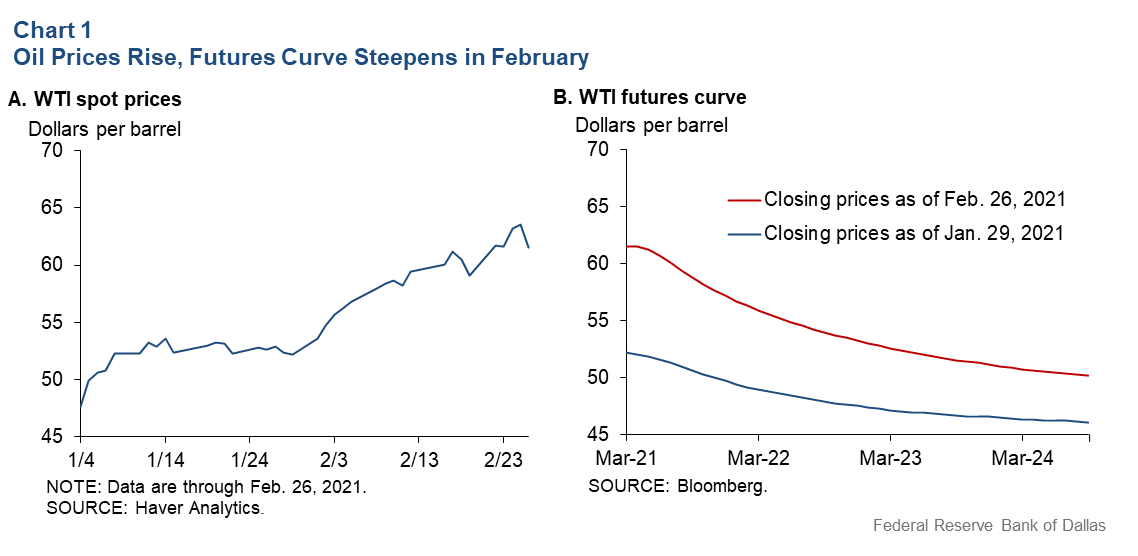

The front-end futures price of oil increased about 18 percent in February, while the backwardation of the futures curve—which refers to the price of near-term contracts exceeding that of longer-term contracts—has increased (Chart 1). This development is difficult to reconcile with oil market fundamentals.

Changes in economic fundamentals

There has been no shortage of possible explanations for this oil price surge. Expectations for higher production later in 2021 from OPEC+ (OPEC members and their allies such as Russia) and a possible relaxation of sanctions on Iran help explain why longer-dated futures prices have not risen as much as near-term prices. Such expectations do not explain the substantial rise in the front end of the curve, however.

Some observers blamed the recent price increases on Saudi Arabia’s decision on Jan. 5 to cut production by an extra 1 million barrels a day in February and March 2021, which quickly pushed the price of West Texas Intermediate oil to $56 per barrel. As Chart 1 shows, however, the price stabilized in the weeks that followed. There is no evidence that this decision helps explain the further oil price increase in February.

Another possibility is that global demand for oil unexpectedly strengthened in February, but this view runs counter to the narrative that OPEC+ delayed its production increases because of unexpectedly low global oil demand. It is also at odds with the travel restrictions, curfews and lockdowns imposed in many European countries starting in December.

While demand for petrochemical products has recovered due to robust growth in China, that rebound was expected and priced in. Unlike for the price of metals such as copper, which has benefited from expectations of an energy transition toward renewables, there is no compelling evidence of an unexpected increase in the demand for oil since the end of January 2021.

Nor can the depreciation of the trade-weighted U.S. real exchange rate since April 2020 explain this oil price increase. Estimates in a study by Lutz Kilian and Xiaoqing Zhou suggest that this depreciation can explain at most $1 of the $9 increase in the price of oil in February 2021.

The accelerating pace of COVID-19 vaccinations in the U.S. is often cited as a reason for higher oil demand in early 2021. However, for U.S. oil demand to increase substantially, the population needs to reach herd immunity, which is unlikely before late 2021. Thus, positive vaccine news is expected to stimulate oil demand only later in 2021.

All else equal, this would be associated with an increase in the oil futures price at longer maturities, not at shorter maturities. Much the same reasoning applies to the argument that the recent oil price increase reflected the anticipation of the recently approved $1.9 trillion federal stimulus measure.

For positive news about the future economy to cause a simultaneous increase in the front end of the futures curve, market participants would have to expect an increase in the price of oil later this year. If so, market participants would seek to buy and store cheap oil now in anticipation of rising prices. The problem is that traders can only make money by buying oil now if they can lock in a sale at a higher price in the future. Given the backwardation of the futures curve, this is not possible.

Financial market developments

This leaves increased demand for oil futures contracts by financial traders as another explanation. There has been much talk in the press about buying commodities as a hedge against U.S. inflation. The problem is that only longer-maturity contracts are likely to protect against rising inflation—and only if one believes that the price of oil will rise sufficiently, which seems inconsistent with expectations of higher OPEC production later in 2021.

It is possible, of course, that the surge in the front-end futures price merely reflects a shift in market sentiment, underpinned by ample liquidity and reinforced by technical traders. This raises the question of how the oil futures curve could have become so steep if there were substantial excess oil inventories available for immediate use. One likely explanation is that conventional measures have grossly overstated the level of excess oil inventories.

Falling excess oil inventories

Standard measures of the oil inventories accumulated since 2019 suggest a massive overhang. Most of these excess inventories are inferred from consumption data for non-Organization for Economic Cooperation and Development (OECD)-member countries, where data limitations are particularly severe.

These data are suspect because direct measures of oil inventories with more limited coverage suggest a much faster decline in global excess oil inventories. For example, by the end of 2020, data from the International Energy Agency (IEA) indicate a much slower decline in excess inventories relative to the end of 2019 (-24 percent) than direct measures compiled by the Energy Intelligence Group (-42 percent).

Moreover, the IEA-based inventory data do not account for the possibility that a substantial part of the crude inventory build in non-OECD countries was added to strategic oil reserves or to commercial oil stocks controlled by governments.

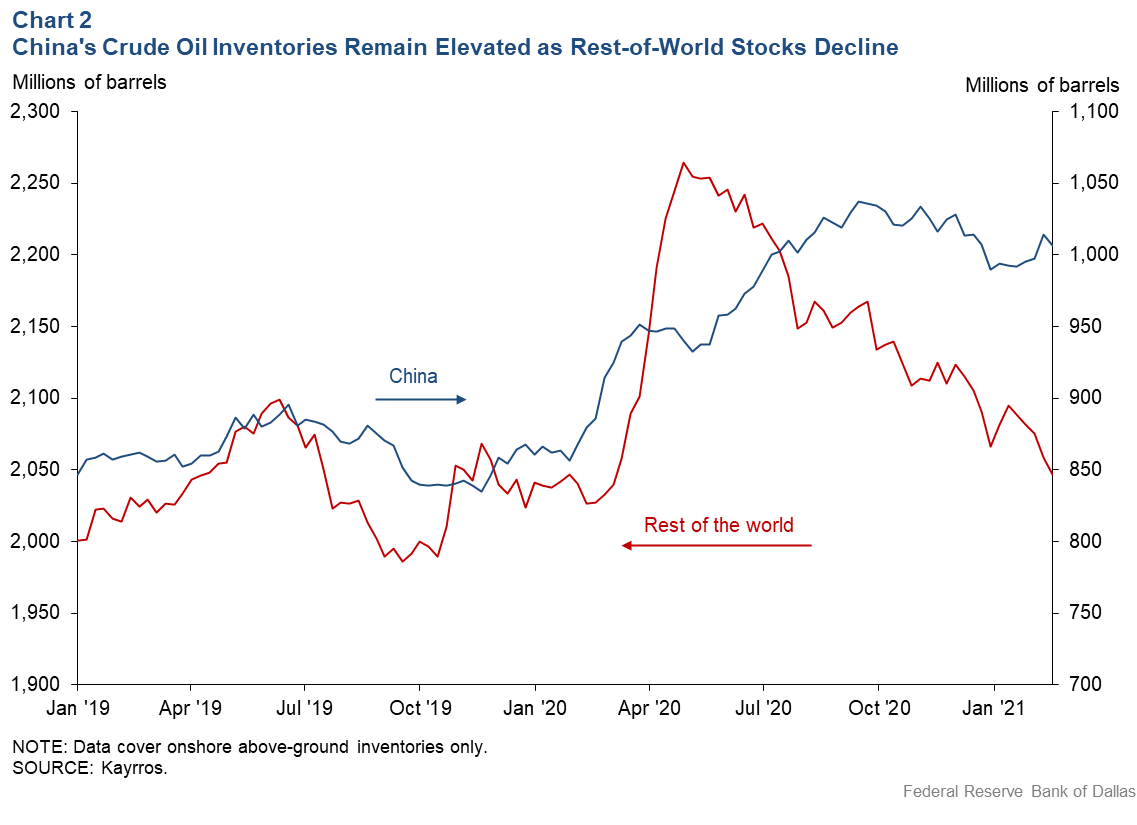

The data analytics firm Kayrros reports a notable difference between Chinese above-ground oil inventories as measured by satellite data, which have remained stubbornly high, and above-ground oil inventories in the rest of the world, which have declined closer to the level prevailing at the end of 2019 (Chart 2).

Since both OECD and non-OECD inventories are subject to the same price signals, the likely explanation is that a substantial share of Chinese commercial oil stocks has become part of China’s strategic reserves (broadly defined) and may never be worked off, except in a national emergency. Moreover, there are indications that non-OECD countries have taken advantage of low oil prices in 2020 to stock up their below-ground strategic reserves.

The bottom line is that estimates of excess oil inventories based on the IEA data are likely overstating the true amount of inventory available to the market. This means that the market may be closer to having worked off excess inventories than commonly thought. For example, the Energy Information Administration reports that U.S. oil inventories have declined dramatically to only 14 million barrels more than in February 2019. These data are instructive because the U.S. has the lowest storage cost and, hence, its storage tends to empty last.

Implications for oil prices

In this environment, no major fundamental shocks may be needed to move the oil price. As it becomes harder for market participants to find crude oil in the spot market, the front-month oil futures price increases, especially with production responses from the U.S. and OPEC+ subdued for the time being. Thus, trading activities in oil futures markets that normally would only move the price by a few dollars may easily cause a more sustained shift in the front end of the curve.

At the same time, the high likelihood of OPEC+ eventually increasing production explains why longer-dated oil futures prices have not increased nearly as much. There is every reason to suspect that the recent surge in the spot price of oil may prove short-lived, since OPEC+ is unlikely to tolerate price levels that would allow the U.S. shale oil sector to fully recover.

The decision by OPEC+ in early March 2021 to extend most of its current production cuts by one month, while further pushing up the front end of the curve, has merely delayed the expected decline in oil prices later in 2021 but has not fundamentally changed market expectations.

About the Authors

Lutz Kilian

Kilian is a senior policy adviser in the Research Department at the Federal Reserve Bank of Dallas.

Michael Plante

Plante is a senior economist and adviser in the Research Department at the Federal Reserve Bank of Dallas.

The views expressed are those of the authors and should not be attributed to the Federal Reserve Bank of Dallas or the Federal Reserve System.