The Paycheck Protection Program: Conditional Success or Unconditional Failure?

The Coronavirus Aid, Relief, and Economic Security (CARES) Act became law in March 2020, marking an initial federal response to the emerging economic disruption from the COVID-19 pandemic.

The Paycheck Protection Program (PPP) managed by the U.S. Small Business Administration (SBA) was a key provision of the law. It sought to stabilize small business finances and maintain employment. The CARES Act and a companion measure, the Health Care Enhancement Act, provided $669 billion in assistance. Two initial rounds of PPP fund disbursement were completed in swift succession, with more than 90 percent of these funds provided by the first week of May 2020.

This article, based on my working paper, explores two questions. First, how well-targeted were the initial PPP funds to local areas experiencing the greatest labor market stress? Second, did the extent of PPP funding help reduce local unemployment rates during 2020?

The answer to the first question—did the funds aid most-stressed areas—appears to be “no,” and to the second question—reducing local unemployment rates—a qualified “yes.”

PPP sought to provide rapid relief to small businesses

For a program of its size and complexity, the implementation of the PPP was remarkably rapid. Just days after the CARES Act became law, the SBA published borrower guidelines. They explained the application process, loan terms and conditions for possible loan forgiveness.

Two-year loans were available at 1 percent interest and could be obtained through the existing network for SBA 7(a) loans—the primary assistance program for small businesses. Lenders were federally insured depository institutions and participating Farm Credit System institutions.

Almost $500 billion of the PPP loan disbursements appeared on the banks’ quarterly regulatory filings (call reports) as of June 30, 2020, with negligible amounts funneled through other institutions. Thus, the banking system provides a nearly comprehensive means of looking at the program.

PPP loan forgiveness, a key feature of the program, was conditioned on maintaining existing payrolls or quickly rehiring workers while maintaining the employees’ previous salaries. If payroll or salaries declined, the forgiven amount would decline as well.

Prospective lenders were incentivized to participate through a generous origination fee structure that ranged between 1 percent (for loans exceeding $2 million) and 5 percent (for loans below $350,000).

COVID-19 recession unemployment surge unprecedented

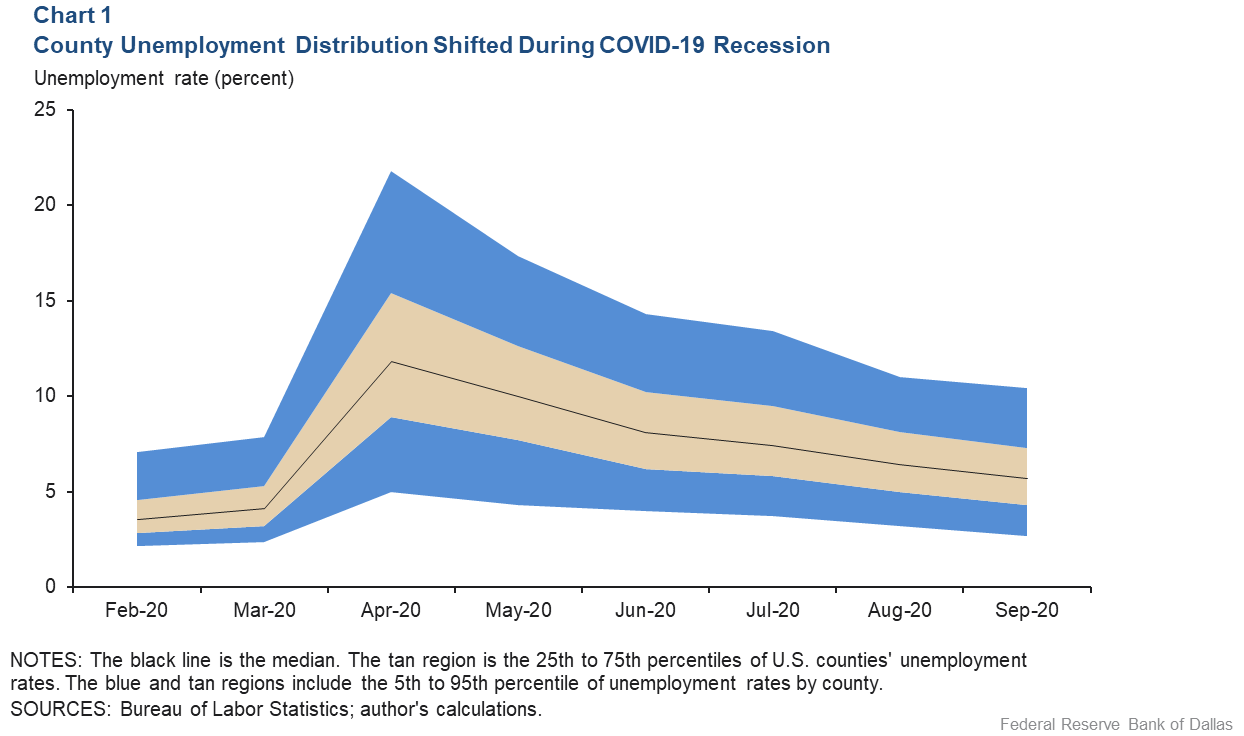

The labor market disruption at the onset of the COVID-19 pandemic was unprecedented in its abruptness and intensity. The national unemployment rate jumped from 3.5 percent in February to 14.8 percent in April, exceeding the post-World-War-II peak of 10.8 percent in 1982.

The initial unemployment surge was geographically broad based and quite asymmetric—moderate jobless increases among counties with relatively modest county-level unemployment rates; skyrocketing jobless rates in the hardest-hit counties (Chart 1). Following the initial surge in April, unemployment rates declined through September, the latest month evaluated.

As this process unfolded, the cross-county unemployment rate distribution compressed, implying that the hardest-hit counties on average recovered somewhat faster.

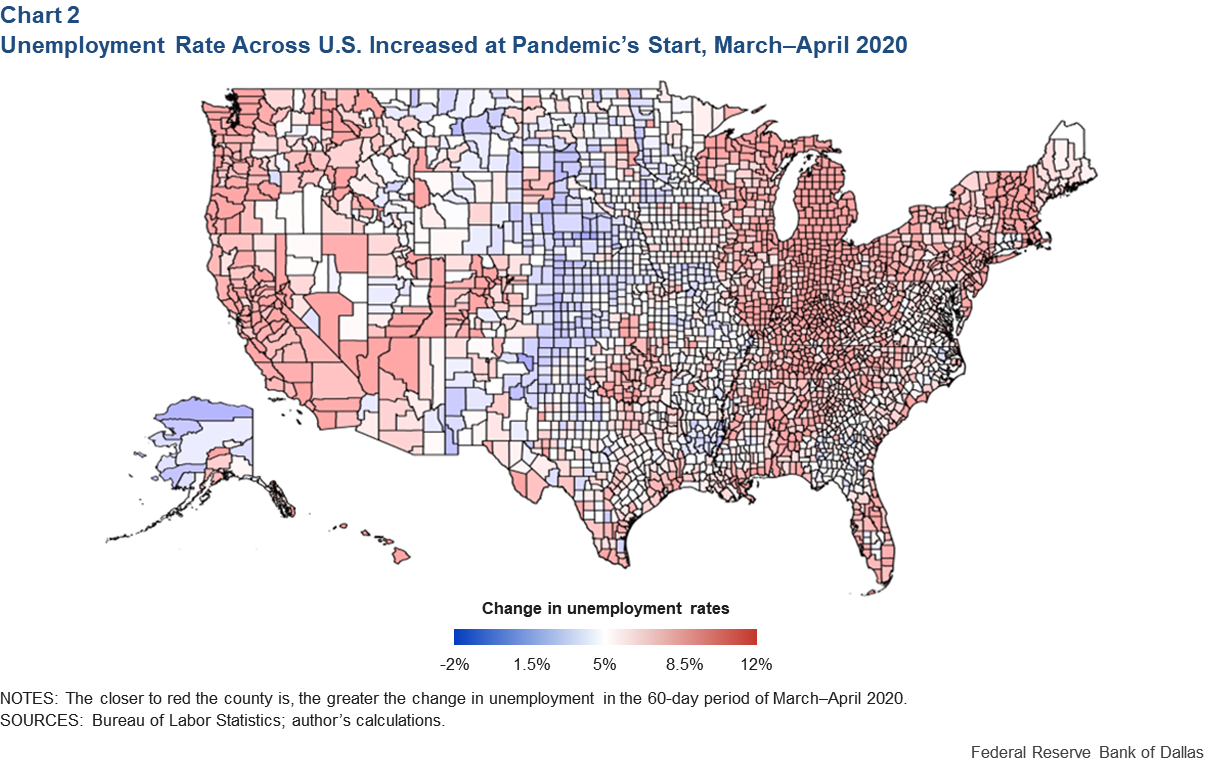

The West Coast, the Northeast and the Midwest were the most affected from March to April 2020 (Chart 2). By contrast, the middle of the country experienced the smallest unemployment increases, with unemployment actually decreasing in a handful of counties.

Given such differences in unemployment dynamics, did the PPP funds go primarily to the hardest-hit counties?

PPP loans didn’t necessarily flow to counties hardest hit by unemployment

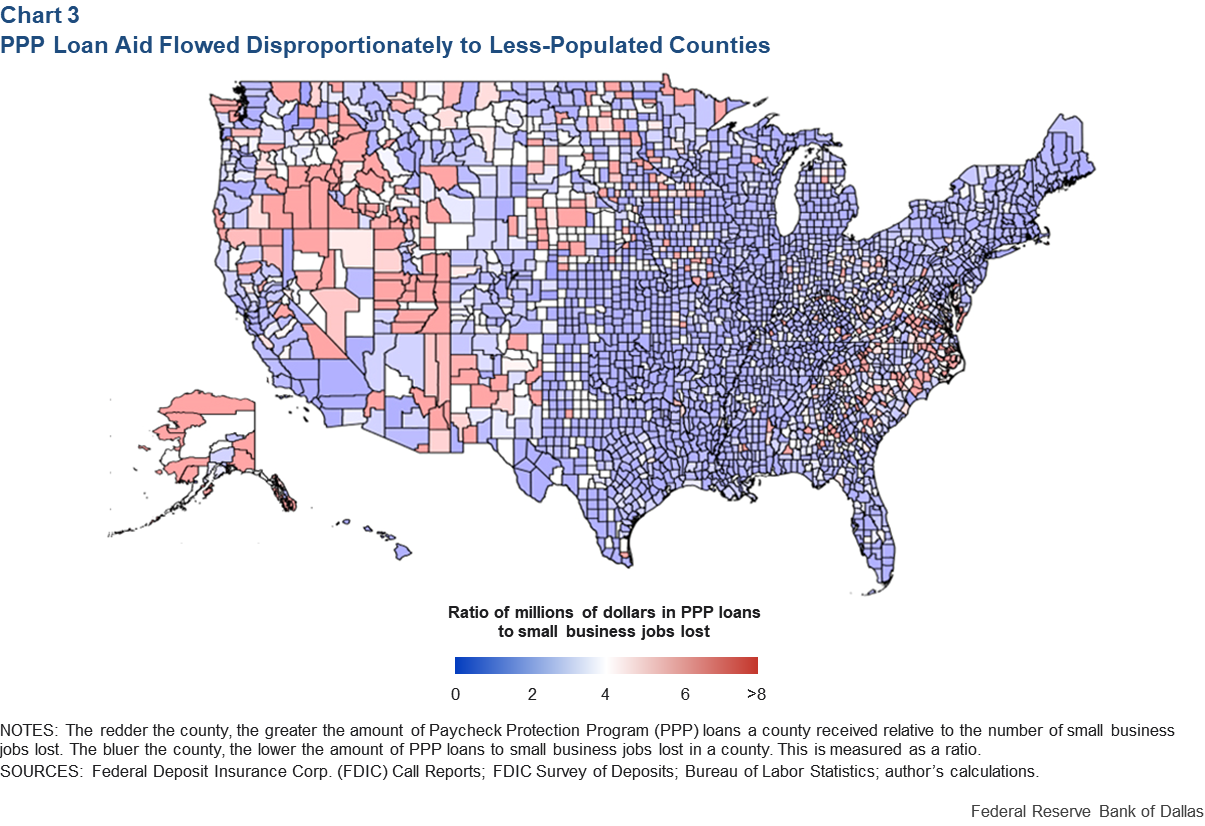

Commercial banks reported their total PPP lending in call reports. While the precise location of bank PPP lending is unknown, it can be estimated by assuming that lending is distributed across counties in proportion to a bank’s county-level deposits.

The preponderance of PPP loans per job lost was uneven—greater in the relatively sparsely populated areas of the Mountain West and relatively less in more populous areas of California, the Northeast and the Midwest (Chart 3). All were among the hardest hit by the initial surge in unemployment.

Overall, the relationship between the severity of the labor market disruption due to the pandemic and subsequent PPP funding per job lost appears to be negative—hard-hit areas got less PPP support.

Formal empirical evidence in the working paper corroborates this informal visual analysis. This finding echoes another paper (“Did the Paycheck Protection Program Hit the Target?”) published in 2020 that found a similar relationship at the state level.

Both papers showed that, on average, PPP loans did not flow to areas hardest hit by the unemployment shock resulting from the pandemic.

My research shows that the factors associated with higher PPP lending per job lost at the county level are low population, low bank profitability and low banking competition. These features are common to rural areas.

The PPP aided labor market recovery

Did counties that received relatively large infusions of PPP loans subsequently experience faster labor market recoveries? My work studies the responses of county unemployment rates between May and September 2020 and finds that the answer depends on the approach chosen to investigate this question. Assuming that all county unemployment rates respond to PPP infusions in the same fashion, those with larger PPP loan concentrations appear to have experienced slightly higher subsequent unemployment rates.

However, once unemployment rate responses are allowed to vary by their demographic and banking characteristics, the answer changes. Counties with higher PPP loan infusions experienced faster subsequent unemployment rate declines particularly where banks had high levels of liquidity before the recession began and where there were relatively small but well-educated populations.

Economically, the program may have been quite expensive: On average, spending an extra $50,000 per job lost during the initial surge in unemployment could lower subsequent unemployment rates by 0.2 percent.

Limited results for quickly implemented program

The PPP was designed and implemented in record time given its size and complexity. It provided small business funding at a time of unprecedented labor market disruption and economic uncertainty. A byproduct of this implementation speed was insufficient program targeting to aid the areas hardest hit by the initial surge in unemployment accompanying the COVID-19 recession.

Labor market effects of PPP loans need to be analyzed with caution, given the diverse experiences of counties. Taking that into account suggests counties with higher PPP funding per job lost experienced moderately lower unemployment rates for up to five months after the program’s implementation.

By that measure, the first two rounds of the PPP undertaken in the first half of 2020 were a qualified success.

About the Author

Pavel Kapinos

Kapinos is a senior research economist in the Supervisory Risk and Surveillance Department at the Federal Reserve Bank of Dallas.

The views expressed are those of the authors and should not be attributed to the Federal Reserve Bank of Dallas or the Federal Reserve System.