Life insurers’ preference for familiar bond issuers limits COVID-19 shock transmission

Companies that need to borrow cash often face a decision: incur bank debt or sell bonds.

At first glance, it appears that the relationships inherent in borrowing from a bank differ substantially from those involved in the sale of bonds in the public debt market. Our research suggests that these dissimilarities are not what they initially appear to be—something that is especially apparent during periods of market strain such as the COVID-19 market shock in 2020.

Taking it to the bank or selling bonds

Bank debt is exchanged through an informationally intensive vetting process. Previous academic work has examined the moral hazard that emerges when many characteristics of the borrowing firm’s viability are private.

Banks manage this risk by scrutinizing the debtor’s financial statements, if available. They also monitor these debtors and obtain valuable private information by building a lending relationship. This relationship, in turn, reduces asymmetric information, which potentially creates benefits for borrowers. If a bank is willing to extend financing, the recipient firm’s creditworthiness appears enhanced. For these reasons, bank debt is often called relationship lending.

By comparison, selling corporate bonds in the public debt market is viewed as lending at arm’s length because investors face higher costs of discovering and monitoring borrower information. Investigation of potential debtors is conducted primarily by analyzing publicly available information.

For example, the Securities Act of 1933 requires that companies file a prospectus when issuing bonds. All public investors have access to this document along with credit ratings and the financial statements of companies whose shares are exchange traded. Investors also face higher costs of renegotiating because these debt holders are often widely dispersed.

It may seem that bank and bond financing are divergent choices. Firms that opt for bank debt develop an ongoing relationship. Bank debt, in the form of term loans and credit lines, is generally supplemented with financial services that continue to involve borrower and lender. Banks in turn monitor and assess the borrower’s riskiness. In contrast, firms that opt for selling bonds take a relatively impersonal approach. Informational discovery is more costly to bondholders, who can access only public information.

However, our recent research suggests that this distinction is imperfect. Relationship lending is a feature of the bond market, too, and it has consequences for economic stability.

Relationships exist in public market for corporate bonds

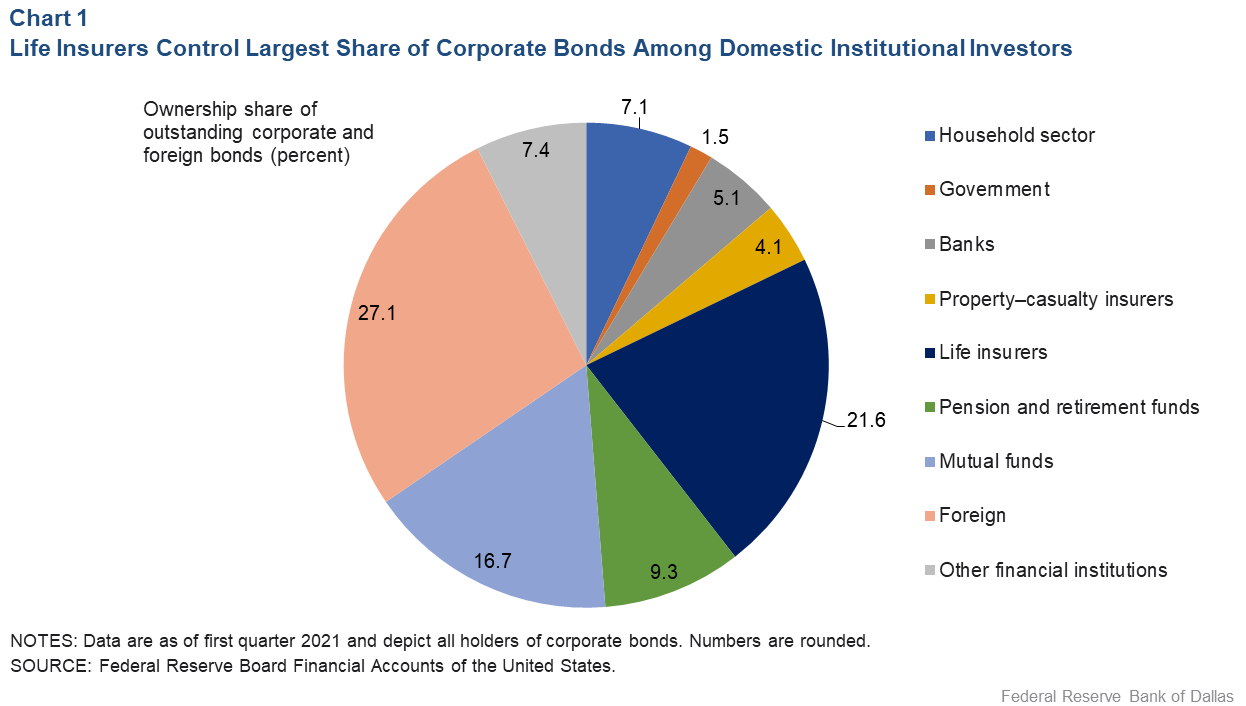

Life insurance companies, the largest institutional investors in corporate and foreign bonds, provide a convenient way to study the lending ties in the corporate bond market. These insurers account for nearly a quarter of outstanding bonds (Chart 1).

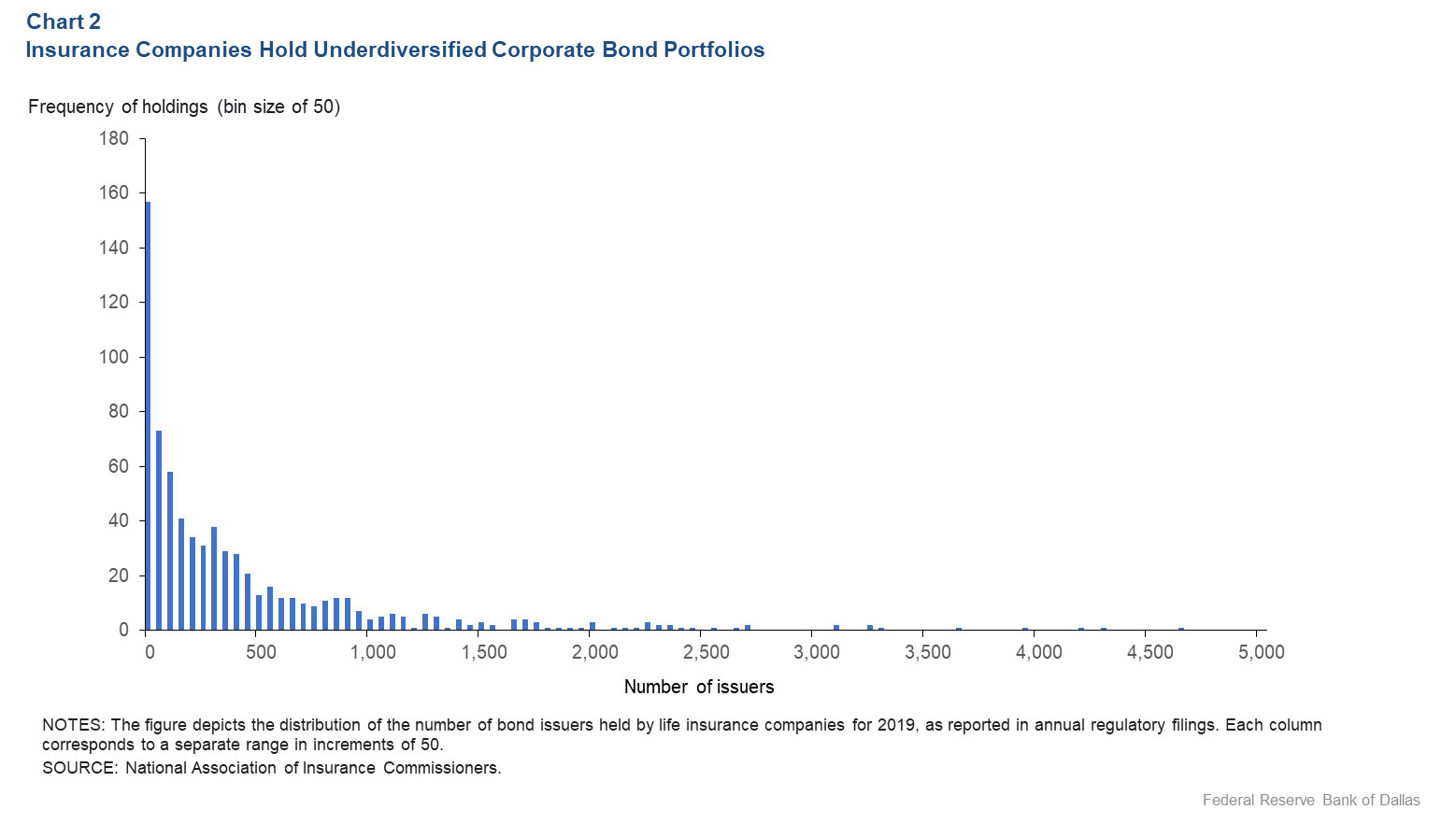

Modern portfolio theory suggests that the idiosyncratic risk associated with individual investments can be tempered by holding a diversified portfolio. The National Association of Insurance Commissioners provides insurance companies with a regulatory incentive to diversify their portfolios by prescribing lower risk-based capital charges for life insurance companies that purchase bonds from a larger number of issuers. Accordingly, if the corporate bond market is characterized by arm’s length lending, one would expect that insurance companies typically hold a well-diversified portfolio.

Chart 2 shows the number of insurance companies (vertical axis) that held the debt of a given number of issuers (horizontal axis) during 2019, as an example.

Most insurance companies hold debt from fewer than 250 bond issuers. Thus, life insurers seem to have incentive to concentrate their corporate public debt investments within a subset of issuers—despite the risks of holding an undiversified portfolio and regulatory incentives to discourage this behavior. This pattern points to the possibility of a familiarity-based lending relationship between life insurance companies and their debtors in the corporate bond market.

Consistent with this argument, we find that insurance companies tend to extend funds to firms with which they have a lending history. If the share of a particular issuer’s outstanding bonds held by an insurance company increases 1 percentage point, this insurance company buys about 0.2 percentage points more of the next bond issue from the same issuer.

This finding is robust when controlling for the rating and duration of the debt as well as other potential relationship-lending considerations, such as the state in which the issuer is incorporated or the industry in which the issuer operates.

Relationship lending stabilizes financial markets

Life insurance companies hold bonds for the long term and do not alter their investment behavior in response to transitory market changes. Moreover, the incentives of life insurers differ markedly from those of other institutional investors, such as corporate bond mutual funds. The latter are beholden to customers and can experience significant outflows during economic downturns. Therefore, we expect debtor firms that life insurance companies favor during public debt sales will fare better following bad macroeconomic shocks.

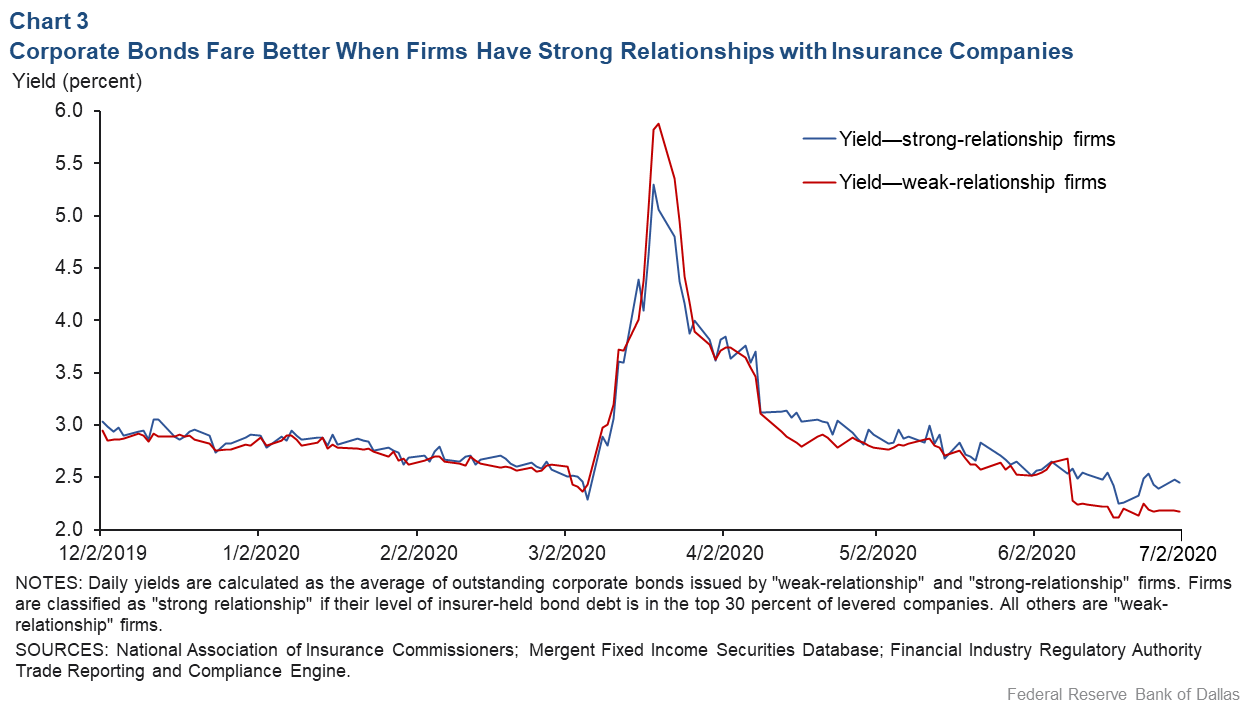

To test whether relationships impact economic performance, we use the surge in bond yields during the COVID-19 crisis in first quarter 2020 as a natural experiment.

Corporate bond yields experienced a rapid increase in early 2020 before they declined following the opening of the Federal Reserve’s corporate credit facilities on March 23. Chart 3 shows the yields of investment-grade corporate bonds, which constituted over 90 percent of the corporate bond holdings of life insurance companies around this time.

We divide these bonds into two equally weighted portfolios based on the share of the issuing corporate parent’s bonds held by the life insurance sector. While the average yields of both portfolios moved in tandem until their spike in early March, the COVID-19 shock led to a much smaller increase in the bonds’ yield when life insurers were a more important investor.

Our work shows that familiarity shapes the bond market more than is commonly believed. Despite regulations that encourage diversification and informational symmetry among buyers, insurance companies tend to lend to their current borrowers.

The notion that bond issuers borrow at arm’s length overlooks this reality. Moreover, this bondholder–issuer relationship moderates the effect of transitory economic shocks such as those associated with the onset of COVID-19. These facts also suggest that monetary policy may have a differential impact across companies depending on their profile of debt ownership.

About the Authors

The views expressed are those of the authors and should not be attributed to the Federal Reserve Bank of Dallas or the Federal Reserve System.