Firm debt structure can mitigate impact of uncertainty shock

It is no secret that stock prices are sensitive to macroeconomic news suggesting some sort of broad economic development. Stocks especially react to news involving macroeconomic uncertainty.

These stock price movements provide an indication of how the market perceives such news. Moreover, price changes can directly affect consumption and investment decisions. What is less known is how corporate debt structure can help mitigate the negative effects of increased uncertainty on stock prices.

Our research suggests that increased uncertainty caused by the U.S.–China trade war negatively affected stock prices. Moreover, we found evidence that the way a firm structures its debt can mitigate a significant amount of the negative effects from uncertainty shocks, especially for zombie firms (mature firms that are persistently unable to generate enough profits to cover their interest expenses).

Relationship between trade war news and stock prices

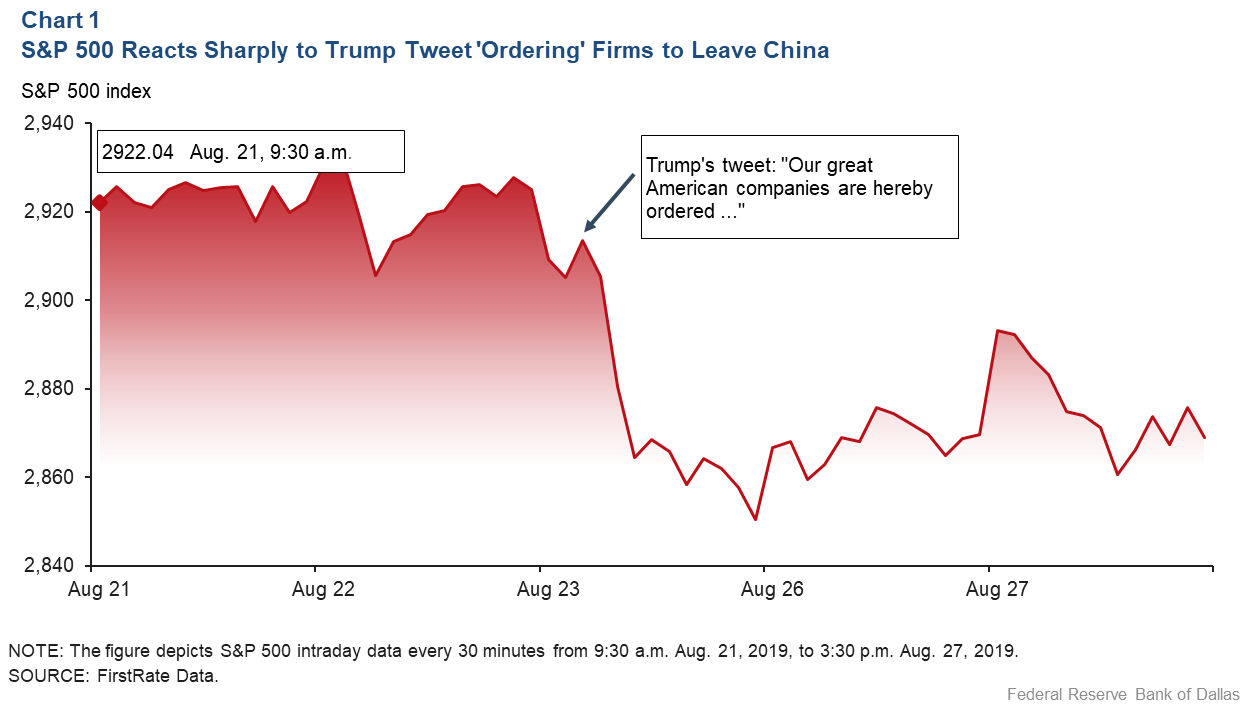

The U.S.–China trade war in 2018 and 2019 created large financial market fluctuations. Chart 1 shows the Standard & Poor’s 500 index in the period surrounding Friday, Aug. 23, 2019, when President Trump tweeted that he “hereby ordered” American companies to “immediately start looking for an alternative to China.”

The index was relatively flat leading up to Aug. 23, but tumbled following the news, closing down about 2.5 percent.

Despite the plethora of channels through which trade war impacts can be transmitted to the macroeconomy, the estimated total effects from these channels are relatively small in comparison to the financial market’s large reaction. The outsized response prompted Lawrence Summers, Treasury secretary from 1999 to 2001, to say that the financial market’s gyrations attributed to the trade war were puzzling.

Nevertheless, policy uncertainty associated with a trade war can raise risk premia, thereby tightening financial conditions. Thus, even without large, immediate effects on macroeconomic variables, uncertainty shocks are a critical part of financial markets and often lead to dramatic stock price movements.

Measuring the effects of uncertainty shocks

Though many factors can affect a firm's risk premium, the timing and magnitude of exogenous shocks to these factors are often difficult to measure. We use the U.S.–China trade war as a laboratory to address this issue.

We systematically collected a series of trade-war-related news events, the precise timing of which is unexpected. Since market prices quickly reflect trade-war news, we can identify the impact of uncertainty shocks from this news using daily financial market data. We study how trade-war-related changes in the Chicago Board Options Exchange's Volatility Index (VIX) drive asset prices on these news-event days.

This approach addresses two big identification challenges: 1) trade-war-related uncertainty is not directly observable—trade-war news on any given day cannot be precisely quantified; and 2) factors apart from trade-war uncertainty continuously influence asset prices.

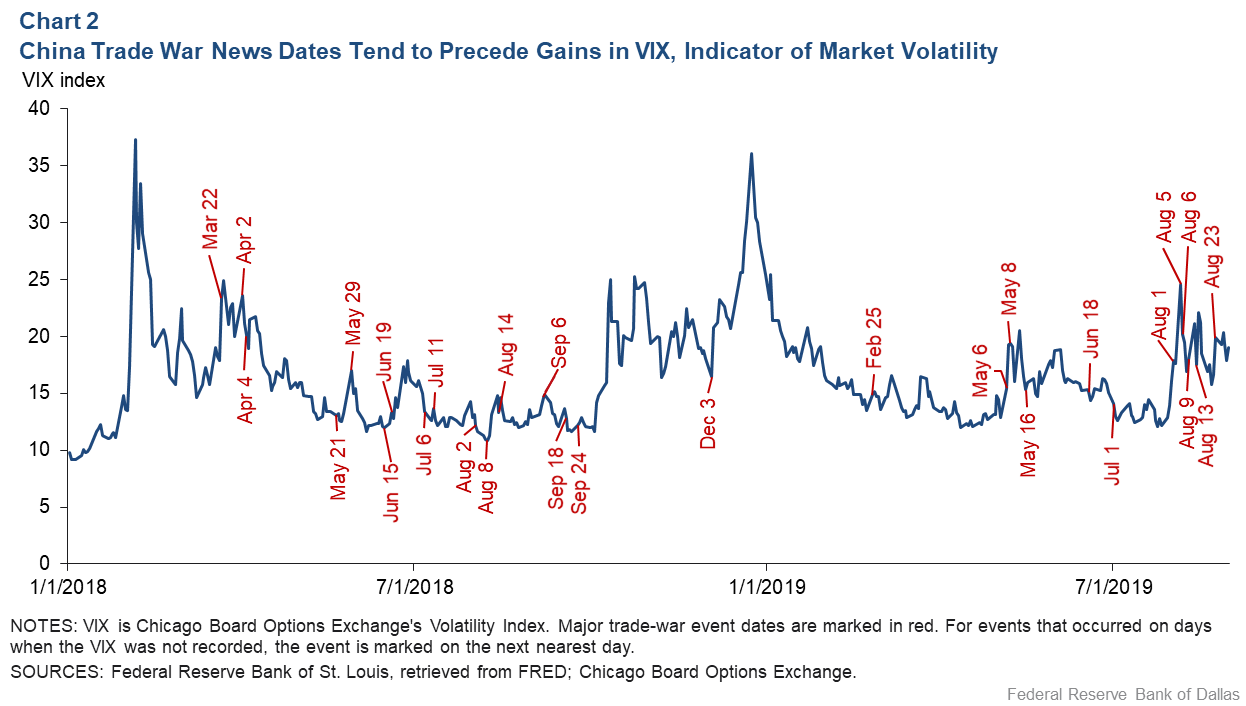

Chart 2 displays the VIX from January 2018 to August 2019, with 28 dates on which there was significant trade-war news.

We found that when trade-war news raised the VIX by 2 percentage points (one standard deviation) per annum, other instruments also reflected greater perceived risk. High-yield spreads increased by 7 basis points (0.07 percentage points), the 10-year Treasury interest rate decreased by 2.6 basis points (meaning safe assets became more valuable), and stock prices decreased by 0.9 percent. The effect on the stock market is equivalent to the Federal Reserve increasing the federal funds target rate by 25 basis points.

We also found that from January 2018 to August 2019, trade-war news accounted for 50 of the 70-basis-point increase in the high-yield spread and about 55 of the 90-basis-point decrease in the 10-year Treasury yield.

Bank debt appears to provide shock mitigation

After identifying the effect of uncertainty shocks on asset prices, we explore whether a firm’s debt structure—specifically, bank debt versus nonbank debt—contributes to the impact of these shocks.

Generally, bank debt poses two conflicting effects when uncertainty increases. On one hand, banks may reduce their loan supply, exacerbating negative impacts on borrowers highly dependent on bank debt. On the other hand, a bank’s informational advantage and personal relationships with its borrowers ease renegotiation, a mechanism we call the financial flexibility channel. This, in turn, can help mitigate the negative uncertainty-shock impacts.

To study the effect of debt structure, we separate 2017 firm debt into bank debt and nonbank debt. We find that firms relying more on bank debt are less susceptible to the uncertainty that comes with trade-war news.

In particular, an uncertainty shock that increases the VIX by 1 percentage point reduces the daily stock value for firms without bank debt by 0.425 percent. However, a one-standard-deviation (0.17) increase in bank leverage (the ratio of bank debt to total assets) can reduce the negative impact on stock value by around 6 percent—from 0.425 percent to 0.4 percent.

Accordingly, firms relying only on bank lending would experience a lower negative impact of 0.275 percent. In contrast, we find that a greater share of nonbank debt amplifies negative effects. These results are consistent with the financial flexibility channel and the ability to renegotiate debt terms.

Bank debt especially benefits zombie firms

Zombie firms are those that consistently cannot generate enough profits to cover their interest expenses and must rely on lenders to stay afloat. In particular, the financial flexibility channel shields zombie firms because they are more likely to value the option to renegotiate their debt, which is easier to do when they are borrowing from a bank than from bondholders, for example.

Quantitatively, we find that for zombie firms, a one-standard-deviation increase in bank debt can mitigate about 45 percent of the negative impact of uncertainty shocks on a firm’s stock value, whereas the mitigating effect of greater bank debt is statistically insignificant for non-zombie firms. This large difference demonstrates the benefits of bank debt usage and the financial flexibility channel for zombie firms.

Overall, our research suggests that uncertainty shocks have immediate effects on the financial market. Greater uncertainty due to the U.S.–China trade war increased high-yield spreads, decreased 10-year Treasury rates and lowered stock prices.

A firm’s debt structure can play a key role in mitigating the harmful impacts of these shocks. When a firm holds more bank debt, it can take advantage of the financial flexibility channel. Specifically, zombie firms can reap the benefits since they rely on lenders to stay afloat. While our approach utilizes the U.S.–China trade war as a laboratory, it can also help us better understand more-recent events, such as the effects of uncertainty associated with COVID-19, global supply-chain disruptions and the Russia–Ukraine conflict.

About the Authors

Ali Ozdagli

Ozdagli is an economic policy advisor and senior economist at the Federal Reserve Bank of Dallas.

Jianlin Wang

Wang is a PhD candidate at the University of California, Berkeley.

Sona Shah

Shah is an intern in the Research Department at the Federal Reserve Bank of Dallas.

The views expressed are those of the authors and should not be attributed to the Federal Reserve Bank of Dallas or the Federal Reserve System.