Trade diversion has helped ease the impact of the embargo on Russian oil

Many observers expected trade sanctions against Russia to substantially raise the price of oil. Tanker traffic data suggest that global oil markets have been more resilient than anticipated. A good portion of the Russian oil destined for export to the West is finding its way to Asia.

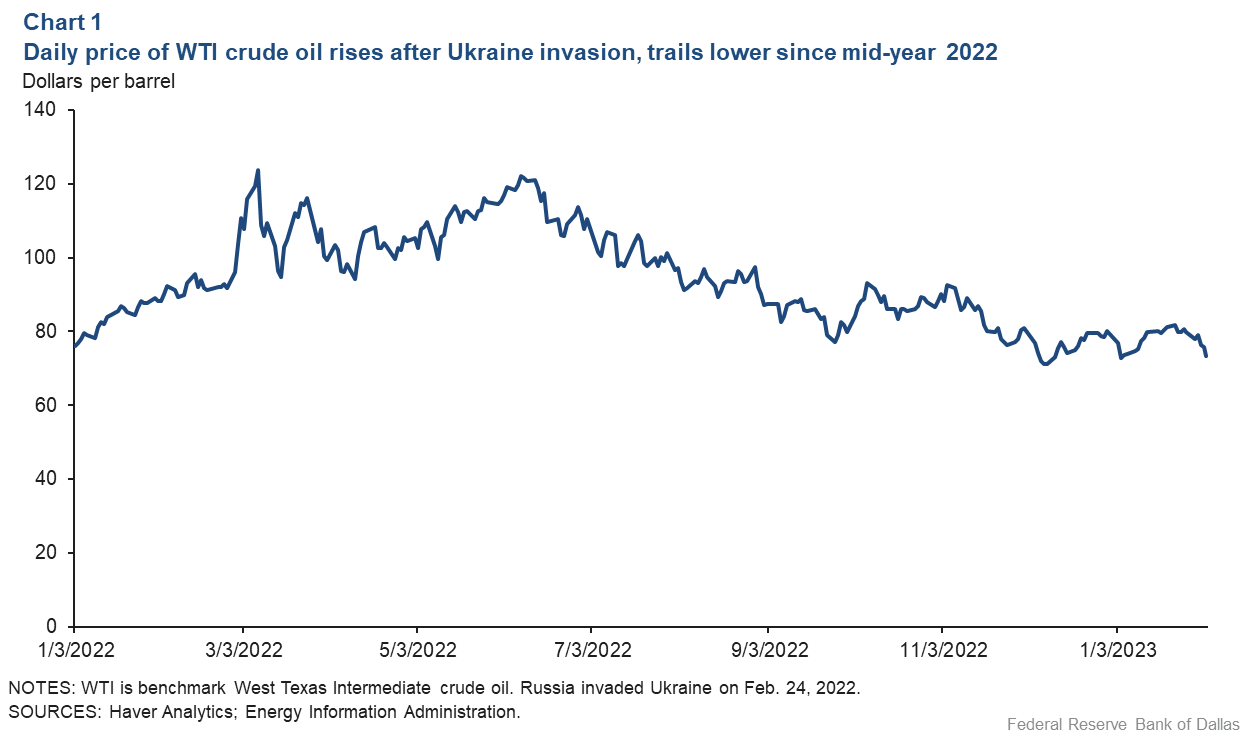

Much has been made of the effect of Russia’s invasion of Ukraine on the price of oil. However, the price of oil was already drifting upward well before the invasion in late February 2022—driven by growing demand for oil, as the global economy recovered from the COVID downturn. This trend continued into mid-2022 (Chart 1).

As global demand growth slowed in the second half of the year, the price of oil began falling, reaching levels by October 2022 not far from where it had started the year. The decision by OPEC to reduce its oil supply in October only temporarily raised the price, as expected demand continued to weaken.

In other words, the price of oil in 2022 was driven first and foremost by global demand. The invasion’s only effect was to create volatility, notably in March and April 2022, when the price of oil spiked relative to trend in response to concerns about imminent Russian oil supply disruptions that never materialized.

There is little evidence in Chart 1 to support the narrative that higher oil prices in 2022 were driven by shortfalls of Russian oil that producers in the rest of the world were unable to offset. Nor is there evidence in more-recent data that the onset of the embargo on Russian oil has had much effect in early 2023. This conclusion is consistent with data for Russian oil exports by tanker provided by TankerTrackers.com.

Effects of the oil embargo that started in December 2022

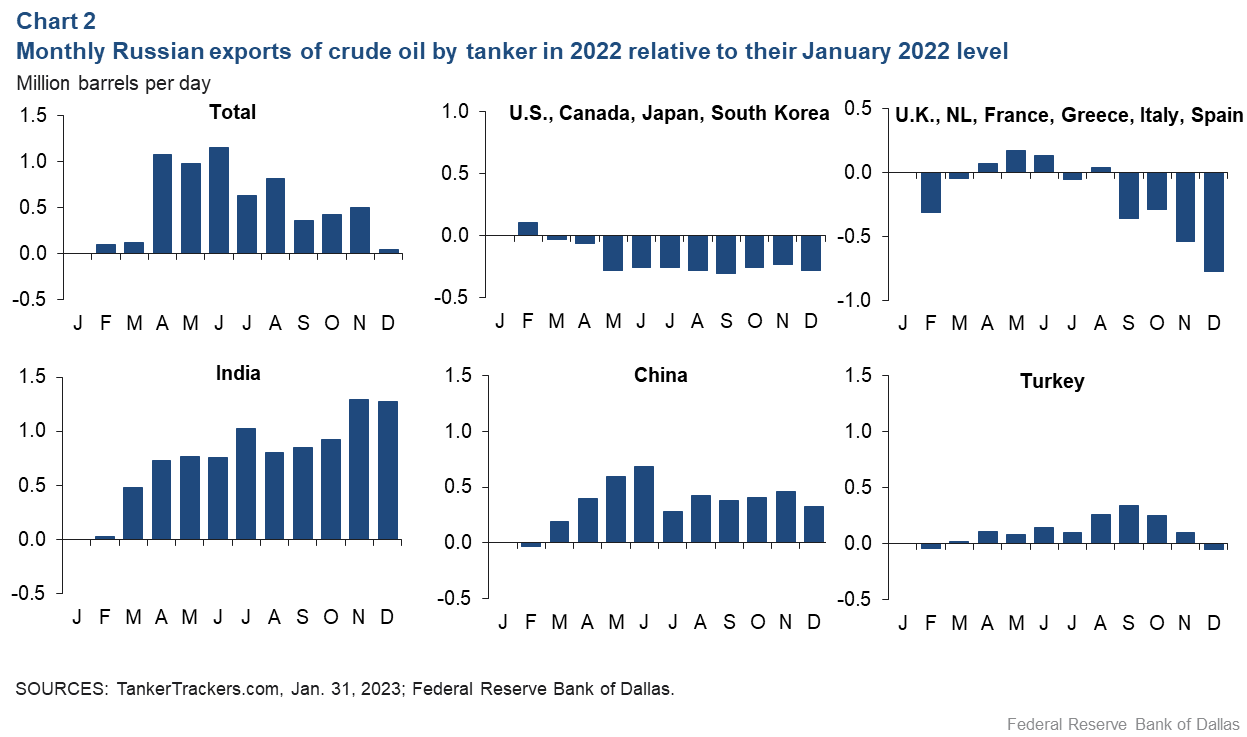

As recently as 2021, Russia exported 4.7 million barrels of crude oil per day (mb/d) to the rest of the world, along with 2.8 mb/d of petroleum products. Some of the crude oil exports to Europe and Asia relied on oil pipelines, which were operating near full capacity before the invasion.

Since the pipeline exports of about 0.8 mb/d to Europe remained stable in 2022 and pipeline exports to Asia could not be increased, much of the adjustment of export flows relied on oil tankers loading Russian oil at Black Sea and Baltic Sea ports as well as ports in the Arctic and East Asia.

Total Russian oil tanker exports during 2022 increased substantially despite reduced deliveries to the West (Chart 2). Russia was not only able to divert crude oil originally destined for Europe and its allies to countries not participating in the embargo but was able to raise its overall oil tanker export volume by as much as 40 percent.

The main beneficiaries of this shift were India, China and Turkey. For example, India’s imports of Russian oil in 2021 were not material, but the country took full advantage of heavily discounted imports of Russian crude in 2022, allowing it to cut back on other oil imports and to export low-cost refined products to the West, blunting the impact of oil sanctions on product markets.

In the aggregate, Russia—far from reducing the supply of its crude to the rest of the world after January 2022—increased that supply and did so at prices lower than those available elsewhere. This, if anything, provided a global stimulus while helping finance the Russian war effort. It also helps explain why the West Texas Intermediate price did not remain elevated relative to trend after the initial uncertainty about the impact of the Russian invasion had died down.

What happened in Europe

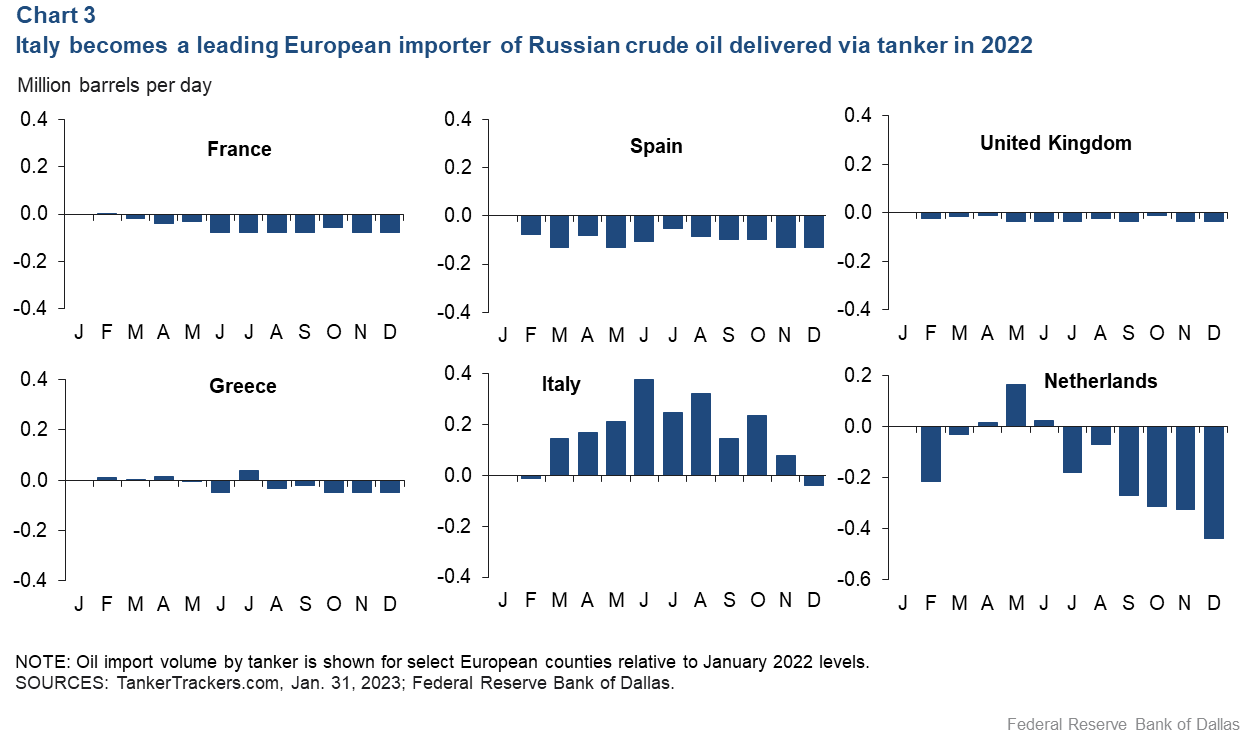

Oil markets might have been tighter in 2022 had it not been for some European countries continuing to import Russian crude oil and—in some cases—even increasing their imports. Italy, in particular, took the opportunity to stock up on discounted Russian oil, while many other European countries, with varying degrees of success, gradually reduced their imports (Chart 3).

By January 2023, these flows declined to a trickle with limited exports continuing to reach Italy, the Netherlands and Spain despite the embargo. Meanwhile, pipeline exports of Russian oil to Europe also dropped substantially.

However, preliminary data indicate that total Russian exports by oil tanker in January 2023 recovered to near 4 mb/d, about 1 mb/d higher than in December 2022 when bad weather delayed shipments. This suggests that Russia has been able to divert most of the oil formerly shipped to Europe by pipeline, coupled with only modest oil production cuts.

The outlook for 2023

The tanker traffic data indicate that the impact of the crude oil embargo on oil prices and on the global economy is likely to be fairly benign in 2023, absent a strong surge in demand. The fact that the $60 price cap on Russian crude—imposed in December 2022 as part of the trade sanction regime—was too high to be binding undoubtedly helped reduce the frictions in the tanker market, as did India’s decision to proceed without Western insurance and Russia’s move to expand its own tanker fleet.

With the European Union product embargo taking effect in February 2023, there is less reason for optimism about product markets. While it appears that the price cap for products has been set above the current market price for Russian products, one key difference is that refined products such as diesel can only be shipped in “clean” tankers that are in shorter supply than the “dirty” tankers used to ship crude oil. If the available product tankers are used for longer runs to Asia rather than to European ports, the effective fleet size shrinks.

Another key difference is that markets for diesel and jet fuel are already stressed, as global transportation demand has recovered. An interesting question is whether Russia will choose to lower its refining output and exports in favor of higher exports of crude oil. That could help Russia deal with the product tanker shortage, while allowing India and China, in particular, to increase their exports of products made from Russian crude—alleviating the global shortage of diesel and jet fuel.

About the Authors

Lutz Kilian

Kilian is a senior policy adviser in the Research Department at the Federal Reserve Bank of Dallas.

Kunal Patel

Patel is a senior business economist in the Research Department at the Federal Reserve Bank of Dallas.

The views expressed are those of the authors and should not be attributed to the Federal Reserve Bank of Dallas or the Federal Reserve System.