Persistence of house-price growth highlights geographic, credit factors

Growth in house prices is highly persistent and therefore more predictable than that of other assets, such as stocks.

Inertia in house-price growth, however, is not stable over time or across regions. Inertia has substantially increased since the mid-1990s in many areas in the U.S. though, and the patterns vary widely geographically.

Understanding how and why house-price growth exhibits different persistence over time and across regions is crucial for assessing the impact of housing markets on the economy. House prices can affect household consumption, labor mobility and employment, and the effects of monetary policy.

In a recent paper, we examine the persistence of house-price growth across U.S. regions (279 metropolitan statistical areas (MSAs)) over the past four decades. We investigate two possible factors behind the changes in persistence—extrapolative expectation of future house prices (previous activity foretelling the future) and credit supply expansion. Our results show that the changes in the inertia in house-price growth are better aligned with the credit supply expansion.

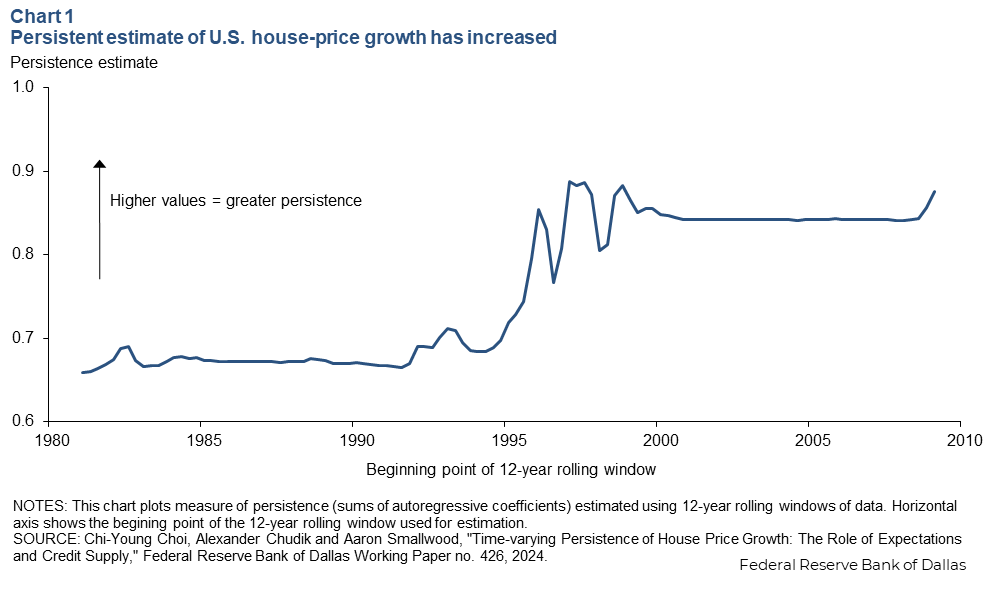

U.S. house-price growth became more persistent

There are several measures that could be used to evaluate the “persistence” or inertia in house-price growth. One of the most commonly used measures is the sum of coefficients in an autoregressive model, in which the current growth rate is estimated solely based on past growth rates.

Using national house-price data from the Federal Housing and Finance Agency, this measure of persistence began rising in the mid-1990s, peaked in the early 2000s and has subsequently remained relatively stable (Chart 1). The increase in persistence occurred before the onset of the 2000s housing cycle, which began before the mid-decade housing bust.

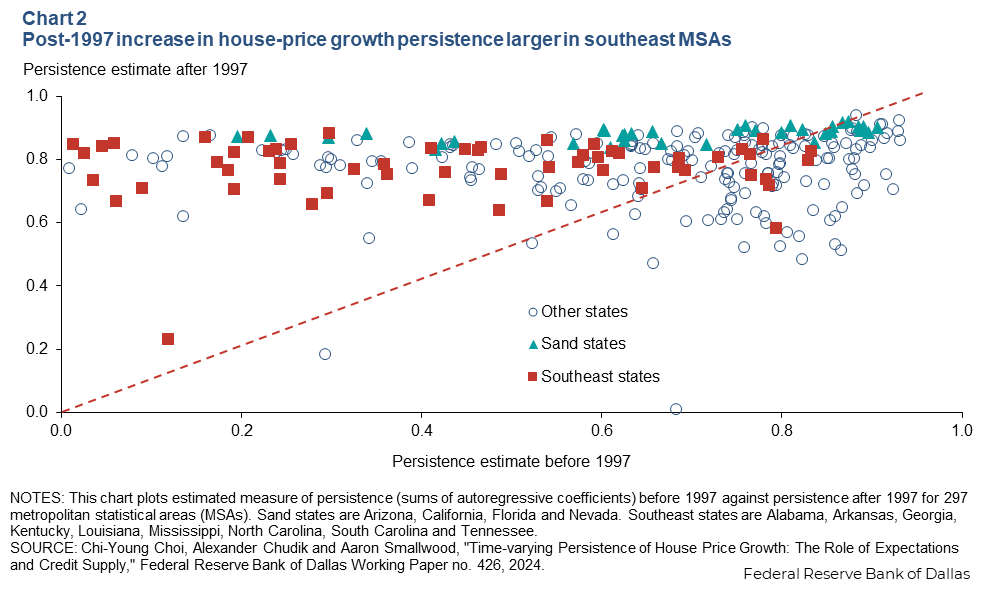

An increase in persistence is also observed in many (but not all) regions within the U.S. Interestingly, the rise in persistence is especially noticeable in cities located in the southeast states that previously exhibited lower levels of persistence, slower house-price growth rates and fewer housing supply restrictions (Chart 2). Persistence has also been notable in what are collectively called sand states— Arizona, California, Florida and Nevada—relatively rapidly growing, warm weather areas.

Factors behind the time-varying persistence

Does time variation in the persistence of house-price growth make the occurrence and duration of housing bubbles more unpredictable? This ultimately hinges on the factors driving the time-varying persistence of house-price growth.

Movements in conventional housing market fundamentals, such as income and population density, are neither large enough to reconcile with the observed variation in persistence of house-price growth, nor do they explain the geographical heterogeneity in the evolution of persistence.

We investigate a couple of additional factors—extrapolative (backward-looking) expectation of future house prices and credit supply expansion. The house-price academic literature recognizes both as influential.

Intuitively, extrapolative expectations can contribute to persistence, owing to the influence of recent house-price changes on expectations in the housing market. For example, potential buyers take rapid price appreciation in the recent past as pointing to further rapid price appreciation in the future, thus boosting housing demand.

Credit supply expansion, typically driven by financial innovations or deregulation, could also affect the dynamics of house prices. We use per capita bank deposit growth as a proxy for credit supply expansion.

To test whether either of these factors explains over time and across metros the variation in the persistence of house-price growth, we estimate time-varying persistence coefficients for each MSA. We then regress those on measures of MSA-level credit supply and a proxy for extrapolative expectations, as well as other controls.

Our results show that credit supply is meaningfully linked to the geographic and time variation in the persistence of urban house-price growth. By contrast, extrapolative expectations—which we proxy with recent price growth—do not play a statistically significant role.

Changing dynamics of house prices complicate monetary policy

Understanding the effects of monetary policy is by no means an easy task, even in the absence of structural shifts in the economy. On the surface, more persistent house-price growth suggests more enduring effects of housing markets on the economy.

Moreover, large geographic disparities in the persistence of house-price growth indicate that monetary policy will have heterogenous effects across different regions in the U.S. Understanding the implications of time-varying house-price dynamics for monetary policy is left to future research endeavors.

About the authors

Chi-Young Choi is professor of economics in the Department of Economics at the University of Texas at Arlington.

Alexander Chudik is an assistant vice president in the Research Department at the Federal Reserve Bank of Dallas.

Aaron Smallwood is associate professor of economics in the Department of Economics at the University of Texas at Arlington.