Rising hedge fund leverage affects monetary policy implementation

Monetary policy implementation seeks to bring money market rates in line with the Federal Open Market Committee’s (FOMC’s) target range. While administered rates help to anchor money markets, market rates still depend on who borrows, who lends and how easily funds can flow between them.

In this article, we show that the structure of the Treasury and repurchase agreement (repo) markets has changed over the past decade in ways that alter how administered rates pass through to market rates.

In particular, leveraged trades in the Treasury market have become an important new source of repo demand. The cash-futures basis trade has grown from a niche strategy to the primary driver of hedge fund Treasury holdings, while swap spread positions are believed to have also increased. These trades matter because they entail a net funding demand on dealers that isn’t present for other types of hedge fund Treasury trades. Dealers must source this funding from money market funds and other cash providers, and the provision of these funds is costly. It takes up dealer balance sheet capacity and limited lending capacity from money market funds. As hedge fund demand increases, secured funding rates rise relative to administered rates as compensation for dealer balance sheet costs and scarce cash-provider lending capacity.

Because these trades are collateralized, the funding pressure they create falls on repo rates and does not pass through fully into the federal funds rate. The result is that during periods where leveraged funding demand expands, spreads widen between secured and unsecured rates. Divergence between these rates makes the choice of operating target—as discussed in Logan and Schulhofer-Wohl (“Options for modernizing the FOMC’s operating target interest rate,” 2025)—a matter of increasing relevance.

We present evidence consistent with the importance of hedge funds in monetary policy implementation. Using both quarterly data on hedge fund net repo borrowing and weekly Commodity Futures Trading Commission (CFTC) data on short Treasury futures positions, we show that expansions in net-funding-demand activity are associated with wider spreads between secured rates and both administered rates and the federal funds rate, even after controlling for the quantity of reserves. The coefficients we estimate imply the expansion of leveraged Treasury relative value activity over the past decade is associated with 10–20 basis points of widening in repo-market spreads. However, it is difficult to interpret these coefficients causally since interest in the basis trade is driven in part by other factors such as asset manager demand (Barth et al., “Reaching for Duration and Leverage in the Treasury Market,” 2024) and net Treasury supply (d’Avernas, Petersen and Vandeweyer, “The Central Bank’s Balance Sheet and Treasury Market Disruptions,” 2025). Nevertheless, the differential pattern across spreads combined with the role of hedge funds as the ultimate recipient of most net repo lending is consistent with levered trades’ increasingly important role in the determination of these rates.

Levered hedge fund trades expanded to absorb Treasury supply

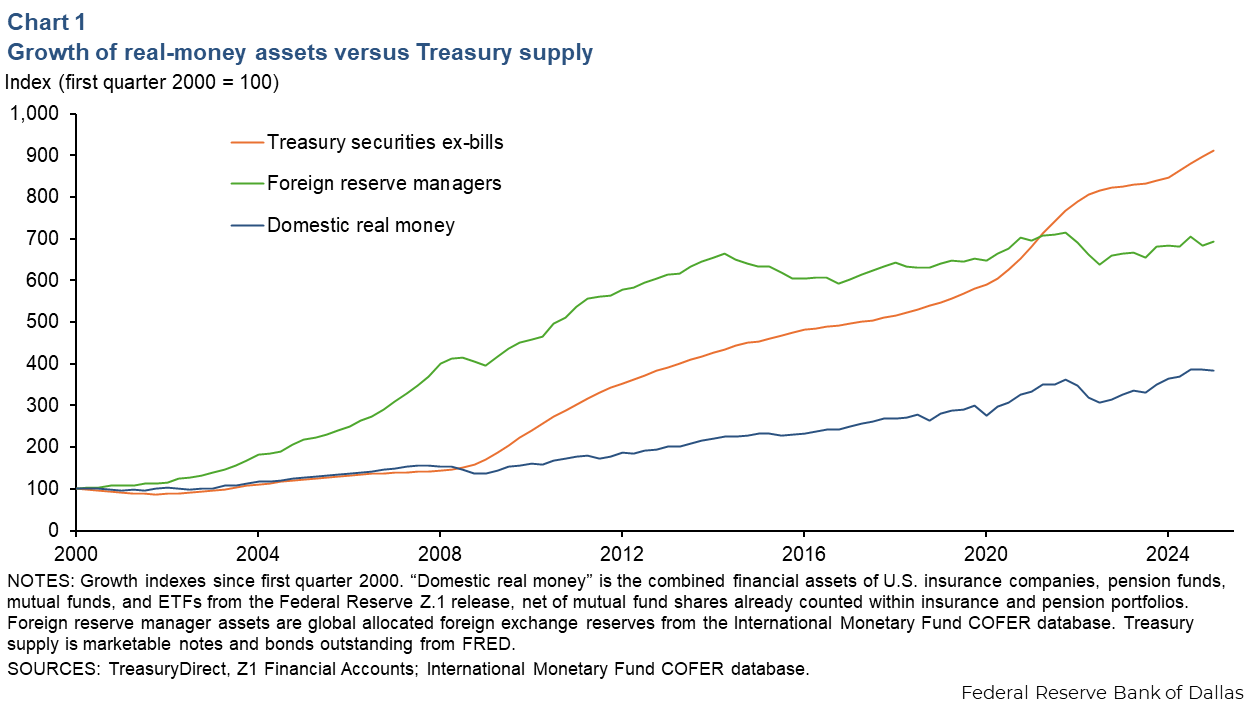

The expansion of hedge funds’ Treasury positions occurs as Treasury supply has substantially outpaced the growth of traditional real-money buyers. Chart 1 indexes the growth since first quarter 2000 in marketable Treasury notes and bonds outstanding, foreign reserve manager assets and the combined assets of U.S. insurance companies, pension funds, mutual funds and ETFs. Treasury notes and bonds outstanding have grown roughly ninefold by 2025, foreign reserve manager assets roughly sevenfold, while domestic real-money assets have reached only about four times their 2000 level. For brevity, we set aside the role of foreign investors other than reserve managers, though we note that as documented by Etra and Setser (“The Disappearing Japanese Bid for Global Bonds,” 2023), similar impacts on repo demand arise from foreign buyers of Treasuries hedging their exchange-rate risk. The gap between Treasury supply and asset growth of real money investors that traditionally absorbed it has increasingly created a role for hedge funds.

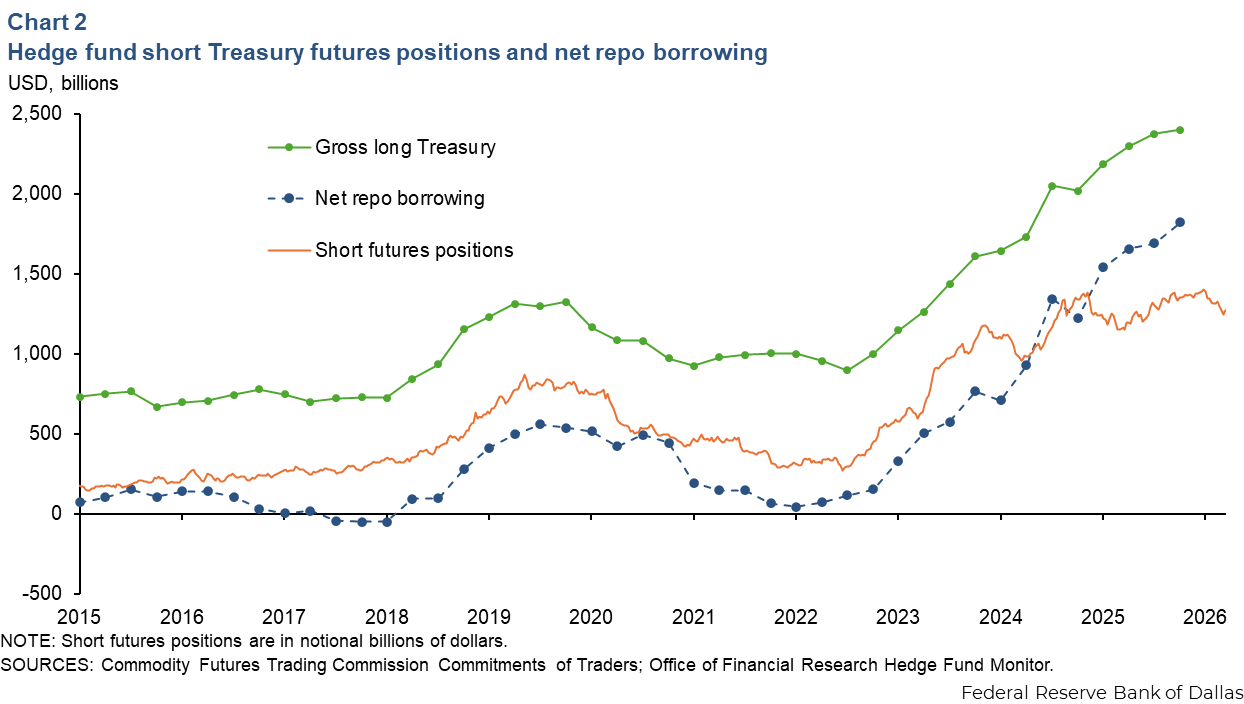

As a result, hedge funds have become a key marginal buyer of Treasuries. Hedge funds’ long Treasury exposures have expanded from roughly $600 billion in 2014 to $2.4 trillion at the end of 2025 (Chart 2). This coincides with evidence that hedge funds have become an important marginal source of demand, especially around Fed purchases and sales of Treasuries (Cordes and Ferris, “Who Buys Treasuries When the Fed Reduces its Holdings,” 2024; Barth et al., “The Cross-Border Trail of the Treasury Basis Trade,” 2025).

The expansion of Treasury positions primarily represents activity in the cash-futures basis trade and the swap spread trade. The cash-futures basis trade is a bet that cash securities are undervalued relative to their futures price. Barth and Kahn (“Hedge funds and the Treasury cash-futures basis trade,” 2025) estimate that roughly 60 percent of the increase in hedge funds’ Treasury positions over recent years is linked to the basis trade. Meanwhile, the swap spread trade, which has become a more prominent driver of hedge fund Treasury demand in 2024 and 2025 (Perli, “Recent Developments in Treasury Market Liquidity and Funding Conditions,” 2025), is a bet that cash securities are undervalued relative to a similar maturity interest rate swap. In the basis trade, a hedge fund will short a Treasury future and go long a cash Treasury. In a swap spread trade a hedge fund will enter into a pay-fixed, receive-floating swap and go long a cash Treasury.

There is important commonality in these two trades. Both involve hedge funds’ substantial net borrowing demand from dealers, as in both cases the funds’ long cash Treasury position is funded in the repo market. Hedge funds’ net repo borrowing has expanded dramatically in recent years. It reached roughly $1.8 trillion by year-end 2025, more than doubling since the start of 2024. This expansion initially coincided with the rise of the basis trade in 2023 and 2024. More recently, net repo borrowing has continued to rise even as short futures positions have remained roughly flat. While reliable estimates of activity in the swap spread trade are not available, the continued rise in repo borrowing without a parallel rise in short futures coincides with increased anecdotal activity in the swap spread trade leading up to April 2025.

It is useful to distinguish two categories of hedge fund Treasury trades.

Net-funding-demand trades—the cash-futures basis and swap spread trades—pair a long cash Treasury financed in repo with a short position in a derivative. Because the short leg is not in cash, the repo borrowing translates one-for-one into net demand on money markets.

Cash-neutral relative value trades go long one cash Treasury and short another, borrowing in repo against the long and lending through reverse repo against the short. Thus, they generate little net demand for cash and should not move money market spreads. In fact, these trades are often provided to hedge funds as netted packages, where cash is never exchanged (Hempel et al., “Why Is So Much Repo Not Centrally Cleared?” 2023). Our empirical strategy below isolates the net-funding-demand component using two complementary proxies: hedge fund net repo borrowing from Form-PF (quarterly, reported with a lag), and leveraged-fund short Treasury futures positions from the CFTC Commitments of Traders (weekly).

The supply of cash

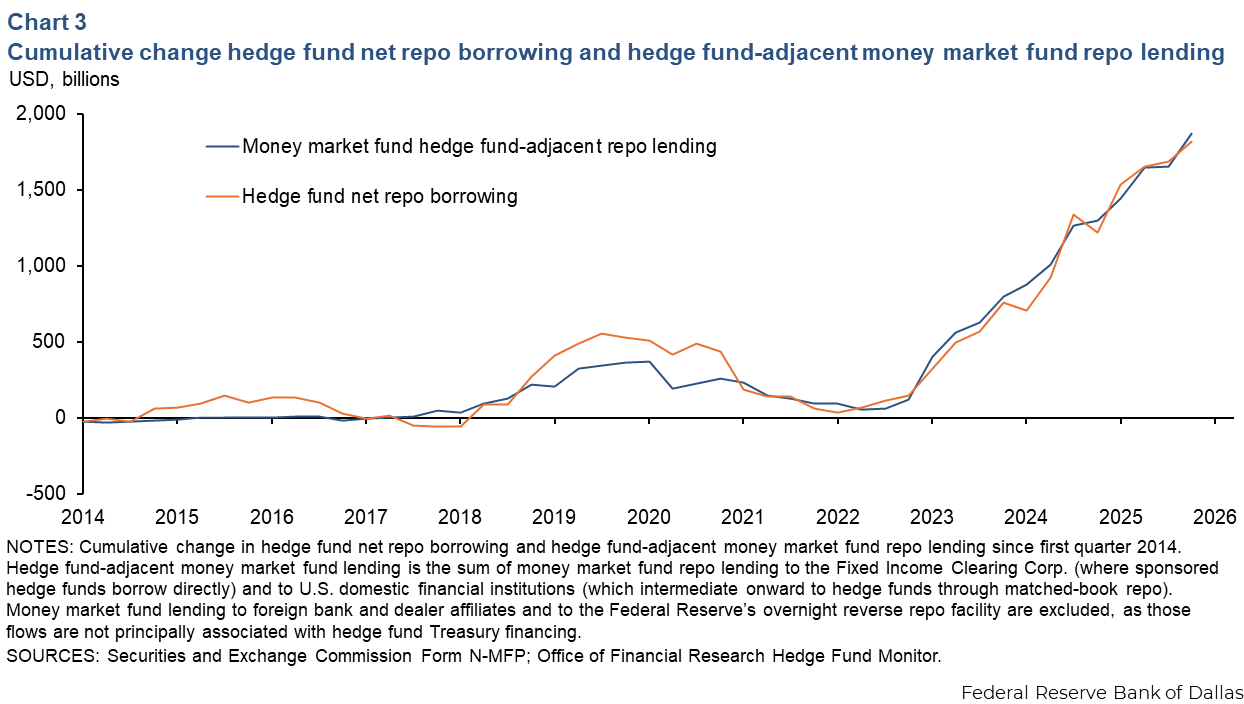

The net-funding demand of hedge funds would not matter for monetary policy implementation if repo funding could be provided to hedge funds elastically. It cannot. Dealers, the immediate suppliers of cash to hedge funds, operate under balance-sheet constraints that impede them from absorbing increases in repo demand on their own books. As shown by Hempel, Kahn and Shephard (“The $12 Trillion US Repo Market: Evidence from a Novel Panel of Intermediaries,” 2025), large dealers run nearly matched books, with roughly 85 cents of every dollar of repo borrowing offset by a corresponding reverse-repo position. Dealers transmit hedge fund borrowing demand to ultimate cash providers rather than providing the cash themselves.

Chart 3 shows this pass-through directly. Cumulative changes in hedge fund net repo borrowing and money market fund private repo lending have grown nearly in lockstep since 2014, with a simple linear regression showing an incremental increase in money market fund lending passes through roughly dollar for dollar into hedge fund borrowing.

Ultimate cash providers—principally money market funds—face their own constraints. Money market funds are limited by investment mandates and Securities and Exchange Commission regulation. Meanwhile, as highlighted by Levy and McCormick (“Domestic banks are inelastic providers of marginal funding to repo markets,” 2026), banks only allocate additional capital to repo lending in response to persistently higher spreads. The result is that increases in hedge fund borrowing raise pressure on secured rates, as supply cannot costlessly adjust to meet additional demand.

Relative value quantities drive repo spreads

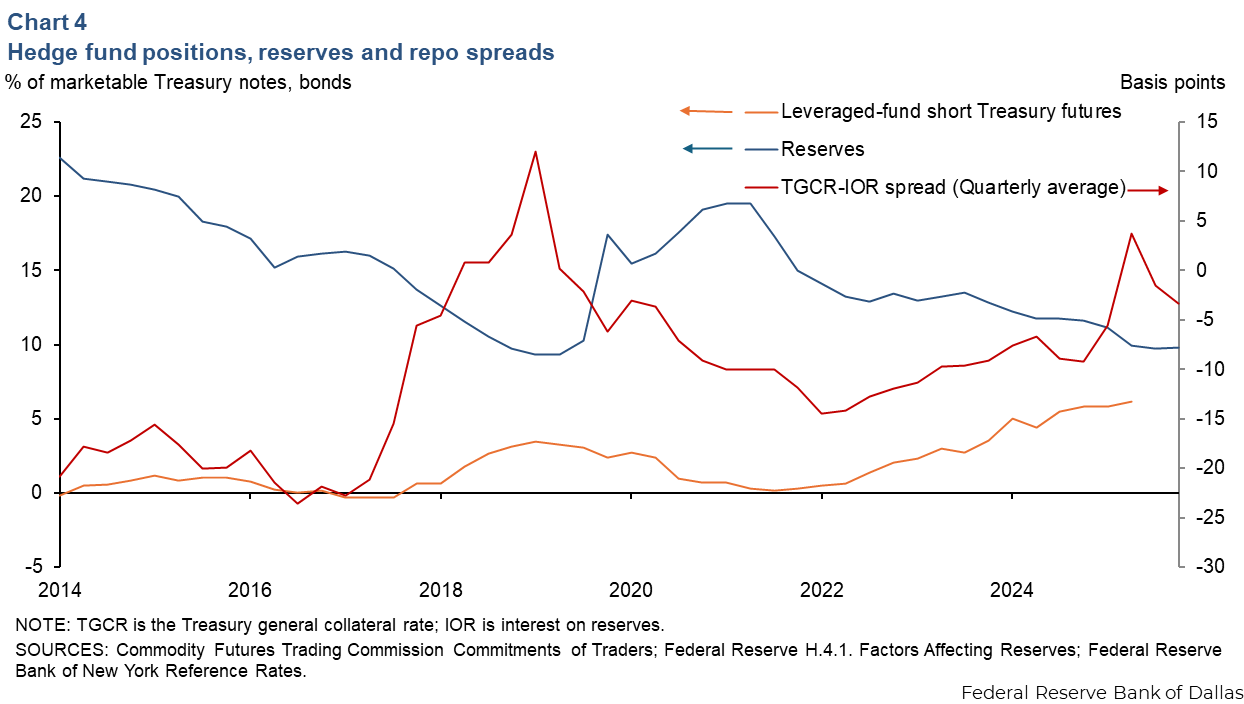

How does hedge fund demand affect rates? If the marginal repo borrower is a leveraged Treasury relative value hedge fund, then expanding that borrowing should widen spreads between secured rates and either administered rates or unsecured benchmarks, while leaving the unsecured-versus-floor margin unaffected. Chart 4 shows hedge fund short futures positions and bank reserves, both scaled by marketable Treasury notes and bonds, alongside the spread between the triparty general collateral rate (TGCR) and the interest on reserve balances (IORB). While these spreads widen as expected when reserves are low, we show below that they also correlate with leveraged fund demand even when controlling for the level of reserves.

Table 1 quantifies these patterns with quarterly ordinary least squares (OLS) regressions of four money market spreads on hedge fund repo activity, controlling linearly for reserve scarcity and net coupon issuance. The specification includes both net repo borrowing (repo minus reverse repo) and gross repo balance sheet (repo plus reverse repo) as separate regressors, testing the taxonomy from the prior section directly. If only net-funding-demand trades move spreads, then net repo should significantly affect money market spreads while gross balance sheet should not.

| Variable | GCF-IORB | TGCR-IORB | TGCR-EFFR | EFFR-IORB | |

| Hedge fund net repo | 3.10** (2.63) |

2.23** (2.54) |

1.73** (2.41) |

0.50 (1.28) |

|

| Hedge fund gross repo | -1.68** (-2.21) |

0.06 (0.09) |

-0.16 (-0.40) |

0.22 (0.63) |

|

| Reserves | -1.50*** (-3.52) |

-1.02*** (-3.07) |

-0.12 (-0.49) |

-0.90*** (-7.53) |

|

| No. of observations | 46 | 46 | 46 | 46 | |

| R² | 0.61 | 0.75 | 0.54 | 0.86 | |

| Adjusted R² | 0.58 | 0.73 | 0.50 | 0.84 | |

| NOTES: Quarterly ordinary least squares, third quarter 2014 through fourth quarter 2025 (common 45-observation sample); start set by New York Fed tri-party general collateral rate (TGCR) back-history. Spreads are quarterly averages of daily values, in basis points. Hedge fund net repo, hedge fund gross repo and reserves expressed as percentages of marketable Treasury notes and bonds outstanding. Specifications also include net coupon issuance scaled by lagged notes and bonds outstanding. Newey-West heteroscedasticity and autocorrelation consistent (HAC) standard errors with four-quarter bandwidth; t-statistics in parentheses. * p<0.10, ** p<0.05, *** p<0.01. GCF is general collateral finance repo rate; EFFR is effective federal funds rate; IORB is interest on reserve balances; TGCR is triparty general collateral rate. SOURCES: Depository Trust and Clearing Corp; TreasuryDirect; Office of Financial Research Hedge Fund Monitor; Federal Reserve Bank of New York Reference Rates; Federal Reserve H.4.1. Factors Affecting Reserves. |

|||||

The results match the prediction. Hedge fund net repo is positive and significant for the three spreads involving a secured rate: a 1-percentage-point rise in hedge fund net repo as a share of Treasury notes and bonds widens (general collateral finance ) GCF-IORB by roughly 3 basis points, (triparty general collateral rate) TGCR-IORB by 2 basis points and TGCR-EFFR (effective federal funds rate) by 2 basis points. We additionally note that weekly regressions using first differences and CFTC data on leveraged-fund short Treasury futures positions provide similar results. Meanwhile, the coefficient on EFFR-IORB is statistically indistinguishable from zero, showing hedge fund repo borrowing transmits through the secured side specifically and not through the unsecured-versus-floor margin. Gross repo is insignificant in three of four columns, consistent with cash-neutral relative value trades not affecting spreads. Reserve scarcity operates on a different margin: Reserves load strongly on EFFR-IORB and TGCR-IORB but not on the secured-versus-unsecured wedge.

These effects are quantitatively large. Applying the net repo coefficients to the cumulative rise in hedge fund net repo borrowing from near zero in 2014 to roughly 6 percent of Treasury notes and bonds by year-end 2025 implies 10 to 20 basis points of secured-market spread widening over the period. We emphasize that these are conditional correlations rather than causal estimates. However, the differential pattern across spreads—hedge fund activity on the secured side, reserve scarcity on the spread of all rates to IORB—is consistent with the mechanism described above.

Levered absorption of Treasuries affects the secured–unsecured wedge

The structure of the U.S. repo market has been reshaped over the past decade by the emergence of large, leveraged hedge fund positions in cash-futures basis and swap spread trades. These positions are funded almost entirely in the repo market, and the resulting demand for cash has become a quantitatively important driver of rates in secured funding markets. Because dealer balance sheets cannot absorb this demand and ultimate cash providers face their own constraints, expansion of hedge fund leverage feeds through into wider spreads between secured and unsecured rates and between secured rates and administered policy rates.

A central message of the analysis is that different spreads within the money market complex respond to different forces. Reserve scarcity, the conventional driver of money market spreads in the post-2008 floor system, affects the level of money market rates as a whole and operates through the spreads between those rates and IORB. The wedge between secured and unsecured rates, by contrast, is largely insulated from reserve scarcity at a quarterly frequency and has become increasingly responsive to the size of hedge fund net repo borrowing, with the response specifically tied to the net-funding-demand component of hedge fund Treasury activity rather than to balance-sheet usage per se. As Treasury supply continues to expand, the role of levered holders of Treasuries in driving demand for secured funding will continue to warrant careful monitoring.

About the authors

R. Jay Kahn is a principal economist with the Board of Governors of the Federal Reserve System.

Matthew McCormick is a principal financial economist in the Research Department at the Federal Reserve Bank of Dallas.