Dallas Fed Energy Survey

First Quarter | March 25, 2020

Oil Price Collapse Reverberates with Job, Capital Expenditure Cuts

What’s New This Quarter

West Texas Intermediate crude oil prices have fallen from $60 per barrel during the fourth-quarter survey period to $28 per barrel during the first-quarter survey period. (The price per barrel further declined to $24 per barrel during the week ended March 20.)

Special questions this quarter include an annual update to our data on breakeven prices by basin, expected changes in employee head counts for 2020, the impact of the coronavirus (COVID-19) on company outlooks and the ability of firms to remain solvent given lower oil prices.

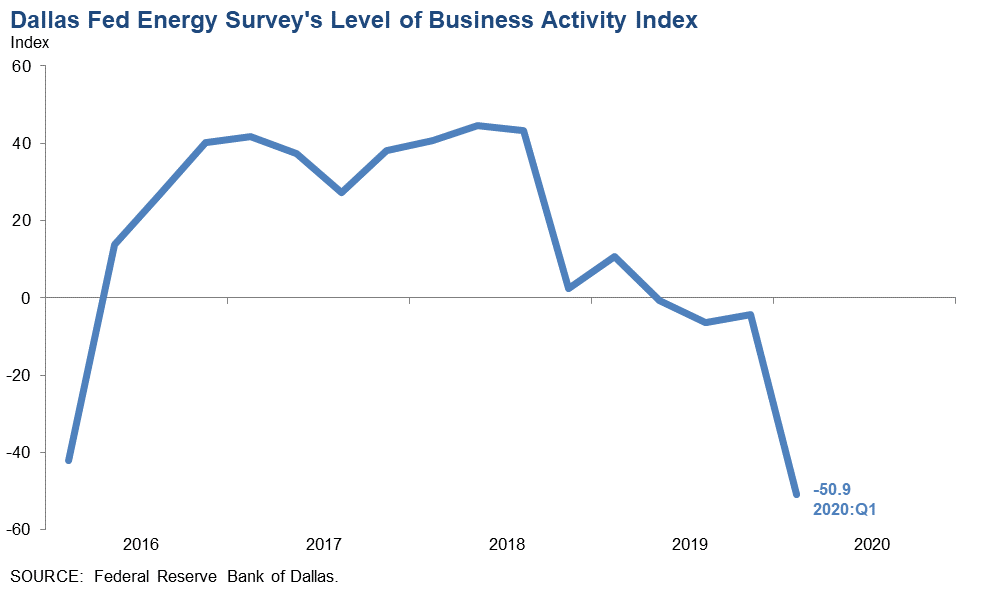

Activity in the oil and gas sector declined significantly in first quarter 2020, according to oil and gas executives responding to the Dallas Fed Energy Survey. The business activity index—the survey’s broadest measure of conditions facing Eleventh District energy firms—plunged from -4.2 in the fourth quarter to -50.9 in the first, the lowest reading in the survey’s four-year history and indicative of significant contraction. Exploration and production (E&P) and oilfield services firms both saw large decreases.

The oil production index plunged 51 points to -26.4, according to E&P executives. It posted its first negative reading since third quarter 2016. The natural gas production index also turned negative, from 15.6 to -21.2. Both indexes suggest that oil and gas production fell relative to the previous quarter.

The index for capital expenditures dropped from 9.1 in the fourth quarter to -49.0 in the first quarter, indicating a reduction in capital spending among E&P firms. The index for the expected level of capital expenditures next year plummeted from 0.9 in the fourth quarter to -61.9 in the first quarter, indicating E&P firms also slashed expectations for capital spending next year.

All indexes pointed to worsening conditions among oilfield services firms. The equipment utilization index fell from -25.8 in the fourth quarter to -47.2 in the first quarter, suggesting an accelerating contraction in equipment utilization. Firms found some relief as input costs fell in the first quarter from 1.7 to -11.3. However, the index of prices received for services slid further into negative territory, from -24.5 to -37.7. The operating margins index also became more negative, from -39.7 to -50.0.

The aggregate employment index posted a fourth consecutive negative reading, declining from -10.0 to -24.0, a signal that jobs contracted further. Additionally, the aggregate employee hours worked index fell from -7.7 to -32.1. The index for aggregate wages and benefits went negative for the first time since third quarter 2016 at -8.2, down from 8.2.

The company outlook index plunged 77 points to -75.0 in the first quarter, indicating an extremely pessimistic outlook. The uncertainty index jumped 38 points to 63.8, pointing to heightened uncertainty regarding firms’ outlooks. Seventy-nine percent of firms reported greater uncertainty.

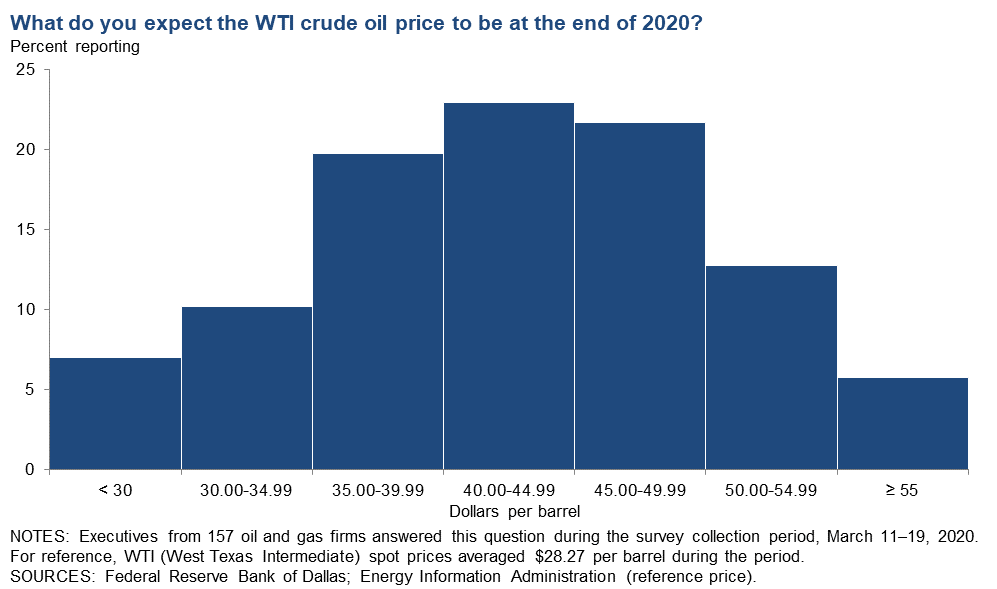

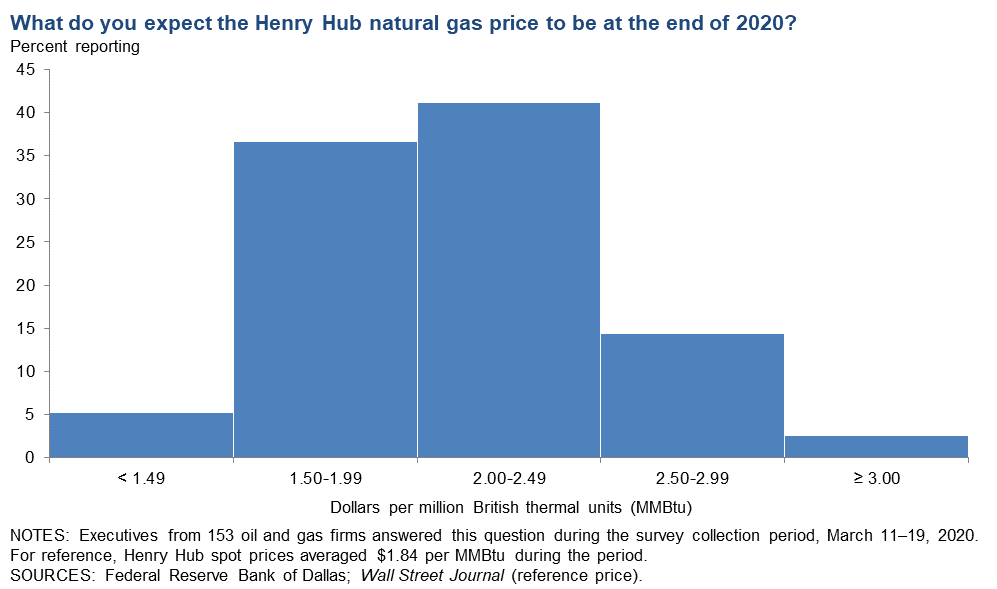

On average, respondents expect a West Texas Intermediate (WTI) oil price of $40.50 per barrel by year-end 2020, with responses ranging from $20 to $65 per barrel. Survey participants expect Henry Hub natural gas prices to be $2.03 per million British thermal units (MMBtu) by year-end. For reference, WTI spot prices averaged $28.27 per barrel during the survey collection period, and Henry Hub spot prices averaged $1.84 per MMBtu.

Next release: June 24, 2020

|

Data were collected March 11–19, and 161 energy firms responded. Of the respondents, 107 were exploration and production firms and 54 were oilfield services firms. The Dallas Fed conducts the Dallas Fed Energy Survey quarterly to obtain a timely assessment of energy activity among oil and gas firms located or headquartered in the Eleventh District. Firms are asked whether business activity, employment, capital expenditures and other indicators increased, decreased or remained unchanged compared with the prior quarter and with the same quarter a year ago. Survey responses are used to calculate an index for each indicator. Each index is calculated by subtracting the percentage of respondents reporting a decrease from the percentage reporting an increase. When the share of firms reporting an increase exceeds the share reporting a decrease, the index will be greater than zero, suggesting the indicator has increased over the previous quarter. If the share of firms reporting a decrease exceeds the share reporting an increase, the index will be below zero, suggesting the indicator has decreased over the previous quarter. |

First Quarter | March 25, 2020

Price Forecasts

West Texas Intermediate Crude

| West Texas Intermediate crude oil price (dollars per barrel), year-end 2020 | ||||

| Indicator | Survey Average | Low Forecast | High Forecast | Price During Survey |

|

Current quarter |

$40.50 |

$20.00 |

$65.00 |

$28.27 |

|

Prior quarter |

$58.54 |

$48.00 |

$75.00 |

$60.19 |

| NOTE: Price during survey is an average of daily spot prices during the survey collection period. SOURCES: Energy Information Administration; Federal Reserve Bank of Dallas. |

||||

Henry Hub Natural Gas

| Henry Hub natural gas price (dollars per MMBtu), year-end 2020 | ||||

| Indicator | Survey Average | Low Forecast | High Forecast | Price During Survey |

|

Current quarter |

$2.03 |

$0.97 |

$4.00 |

$1.84 |

|

Prior quarter |

$2.51 |

$1.35 |

$4.00 |

$2.28 |

| NOTE: Price during survey is an average of daily spot prices during the survey collection period. SOURCES: Federal Reserve Bank of Dallas; Wall Street Journal. |

||||

First Quarter | March 25, 2020

Special Questions

Data were collected on March 11–19; 157 oil and gas firms responded to the special questions survey.

Exploration and Production (E&P) Firms

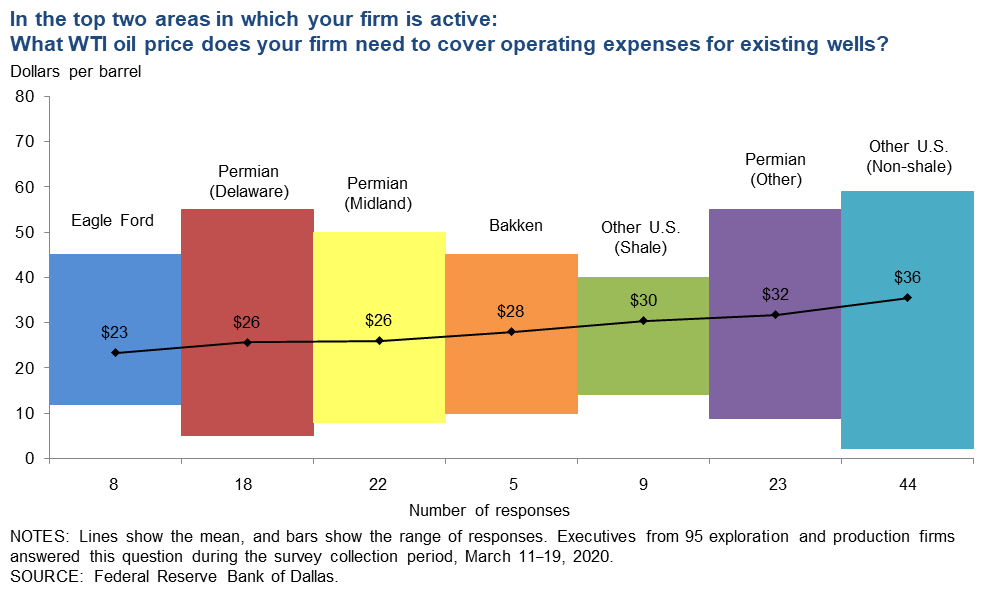

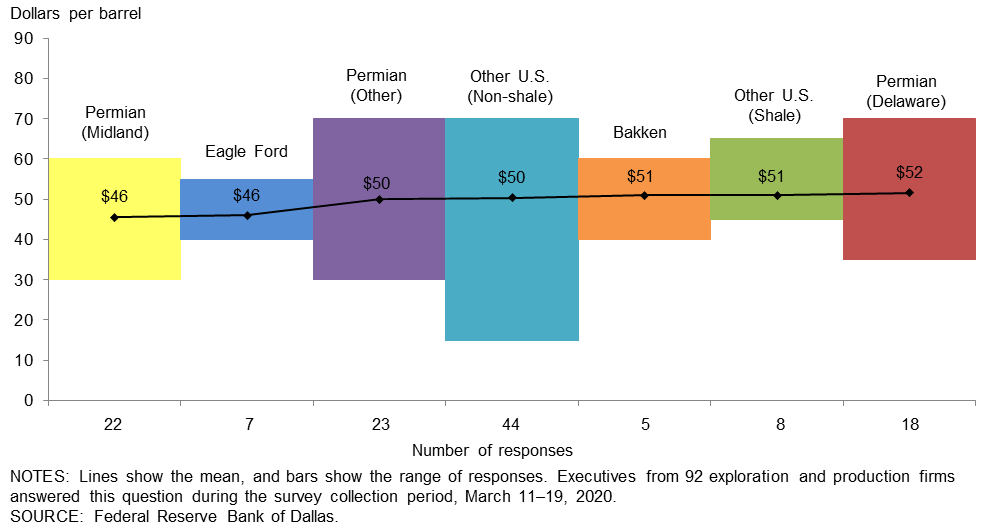

In the top two areas in which your firm is active: What West Texas Intermediate (WTI) oil price does your firm need to cover operating expenses for existing wells?

Average prices necessary to cover operating expenses across regions range from $23 to $36 per barrel. Thirty-five percent of responses were at or below the average WTI spot price for the week ending March 20 ($24 per barrel), signaling many firms can’t cover operating expenses at current prices. Overall, operating expenses are lower than those observed in last year’s first-quarter survey, with the average across the entire sample approximately $30 per barrel, versus $33 last year.

{kind=link}

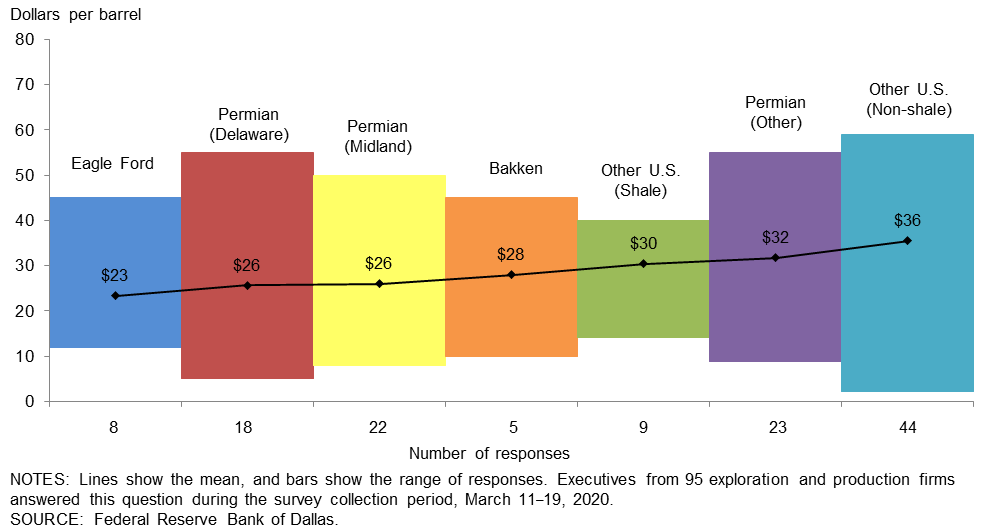

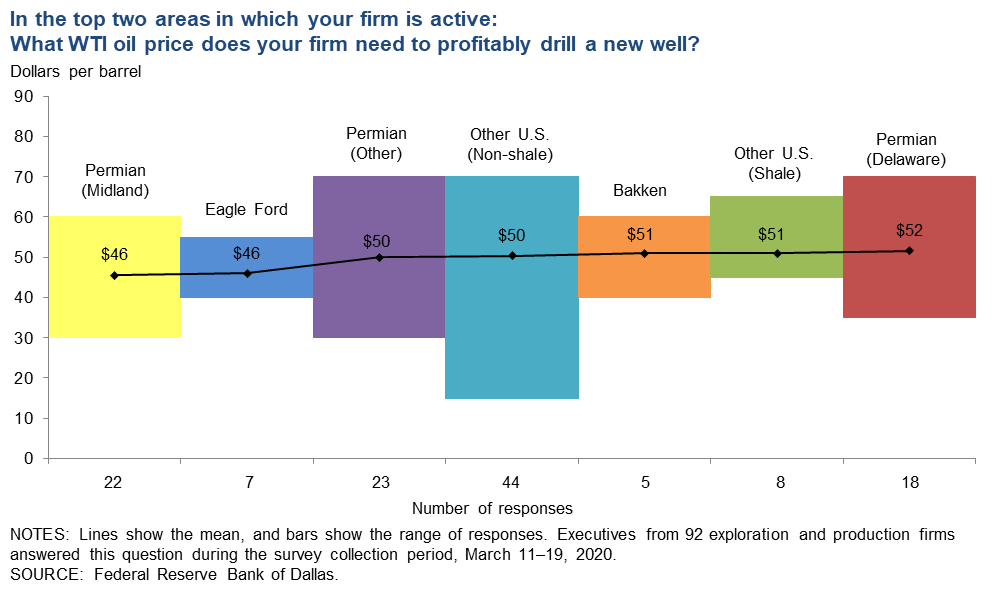

In the top two areas in which your firm is active: What WTI oil price does your firm need to profitably drill a new well?

For the entire sample, firms need $49 per barrel on average to profitably drill, slightly lower than the $50-per-barrel price when the same question was asked last year. Across regions, the average breakeven prices to profitably drill a new well range from $46 to $52 per barrel. Breakeven prices in the Permian Basin average $49 per barrel, $1 lower than last year. For the past four years, Permian (Midland) has been the lowest-cost region. With the recent oil price decline, almost no firms that responded can profitably drill a new well at the average WTI spot price for the week ending March 20 ($24 per barrel).

{kind=link}

All Firms

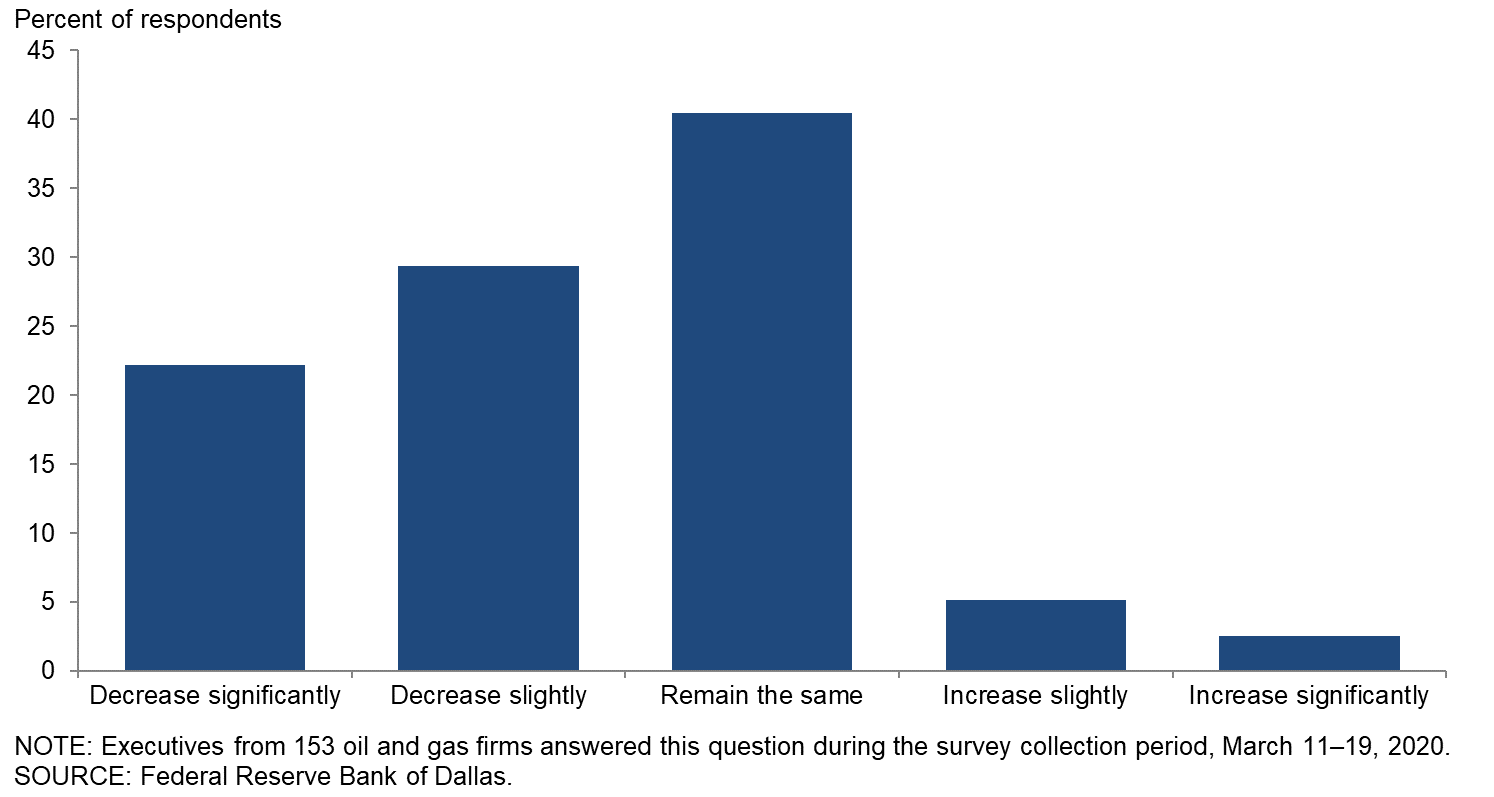

How do you expect the number of employees at your company to change from December 2019 to December 2020?

Slightly over half of executives—51 percent—expect the number of employees at their company to decrease from December 2019 to December 2020. Of those seeing a decrease, 22 percent expect a significant decrease and 29 percent expect a slight decrease. Forty-one percent of executives expect the number of employees to remain close to December 2019 levels. Eight percent anticipate that the number of employees will increase in 2020.

A greater percentage of oil and gas support services firms expect to decrease employment in 2020 compared with E&P firms. Sixty-six percent of support services firms expect to reduce the number of employees in 2020 versus 45 percent for E&P firms. (See table for more detail.)

{kind=link}

| Response | Percent of Respondents | ||

| All Firms | E&P | Services | |

| Decrease significantly | 22 | 15 | 37 |

| Decrease slightly | 29 | 30 | 29 |

| Remain the same | 41 | 48 | 27 |

| Increase slightly | 5 | 7 | 2 |

| Increase significantly | 3 | 1 | 6 |

| NOTES: Executives from 101 exploration and production firms and 52 oil and gas support services firms answered this question during the survey collection period, March 11–19, 2020. The “All Firms” column reports the percentage out of the total 153 responses. Percentages may not sum to 100 due to rounding. SOURCE: Federal Reserve Bank of Dallas. |

|||

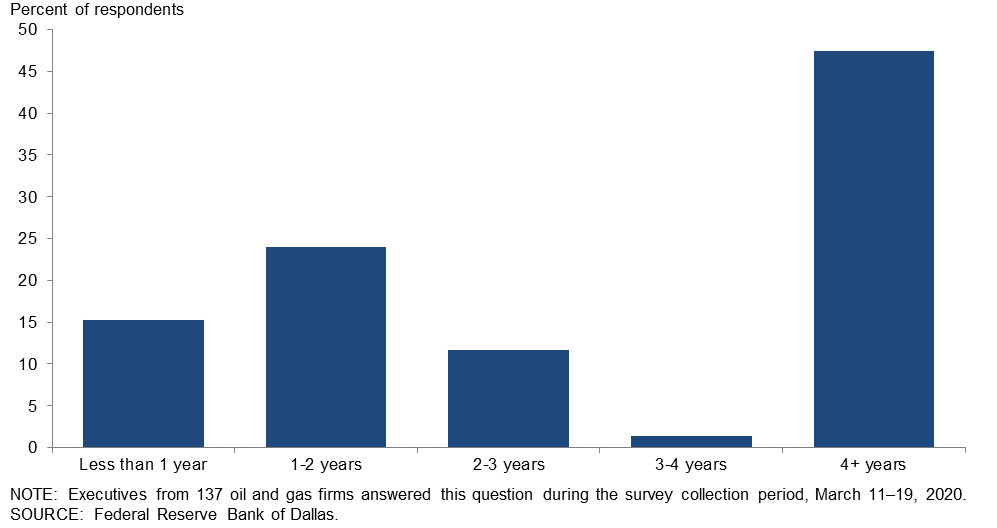

If the WTI price of oil were to fall to $40 per barrel and stay there, how long would you expect your firm to remain solvent?

Forty-seven percent of executives expect their firm to remain solvent for four or more years if oil prices are $40 per barrel. Fifteen percent expect less than one year and 24 percent expect one to two years. The remaining 13 percent of executives expect to remain solvent for two to four years. (Percentages don’t sum to 100 due to rounding.)

{kind=link}

How has the coronavirus (COVID-19) outbreak changed your firm’s outlook in key areas in 2020?

In five out of seven key areas, a majority of executives cut their outlook due to the coronavirus outbreak. Seventy-eight percent of executives revised their company outlook down because of the coronavirus outbreak, of which 49 percent lowered their outlook significantly and 29 percent lowered it slightly. Similarly, 67 percent of executives revised down their expectations for capital expenditures, of which 48 percent lowered their expectations significantly and 19 percent lowered them slightly. Additionally, 70 percent of executives revised down their outlook for business activity, of which 43 percent lowered their outlook significantly and 27 percent lowered it slightly. A majority of executives reported no change in their outlook for supplier delivery time and number of employees.

| Percent of Respondents | ||||||

| Revised significantly down |

Revised slightly down |

No change | Revised slightly up |

Revised significantly up |

Number of responses |

|

| Level of business activity | 43 | 27 | 29 | 1 | 0 | 150 |

| Oil production | 20 | 41 | 38 | 0 | 2 | 96 |

| Utilization of equipment | 36 | 24 | 40 | 0 | 0 | 50 |

| Supplier delivery time | 10 | 19 | 63 | 8 | 1 | 145 |

| Number of employees | 14 | 27 | 59 | 0 | 0 | 149 |

| Capital expenditures | 48 | 19 | 30 | 2 | 0 | 149 |

| Company outlook | 49 | 29 | 21 | 1 | 1 | 150 |

| NOTES: The oil production question was posed to E&P firms only, while utilization of equipment question was posed to oilfield services firms only. Executives from 98 exploration and production firms and 52 oil and gas support services firms answered these questions during the survey collection period, March 11–19, 2020. Percentages may not sum to 100 due to rounding. SOURCE: Federal Reserve Bank of Dallas. |

||||||

Special Questions Comments

Exploration and Production Firms

- COVID-19 does not affect us as much as the oil price war.

- At the time I am completing the survey, West Texas Intermediate is $29.67 on the futures market. I suspect that it will fall to at least $15 per barrel, and perhaps lower, as the Saudis and Russians fight an economic war on each other. My outlook on the domestic oil and gas industry has never been bleaker.

- I have never seen this scenario play out. Increasing oil and gas supplies and the coronavirus induced low demand. This is a double whammy for the industry. Oilfield services costs are expected to drop similar to the level observed during the last downturn of 2015–16. The industry will consolidate, removing a lot of fixed cost and making oilfield activities profitable in due course.

- Oil prices will be $15 before OPEC or Russia cries uncle.

- It is too early to assess with any level of expected accuracy the impact of COVID-19. The consequences of a real pandemic are by any measure far-reaching and not experienced in current memory. It is safe to say that a real pandemic will change the face of the nation and the oil and gas industry in degrees, areas and depths impossible to visualize beforehand.

- As a conventional acquisition and divestiture company, [for us] the industry weakness will provide opportunities to acquire assets.

- The economics for producing natural gas are another disaster. Gas purchasers are adding deductions in Oklahoma. Lessors in West Texas are creating “pseudo-companies” to force operators to contract services through them and then taking a cut on everything. Their 25 percent royalty isn't satisfying enough, so they'll get premature abandonment on their wells instead!

- The price of natural gas has the biggest impact on us.

- This will weed out the Ponzi guys in the shale plays. There’s lots of capital destruction occurring. Bankruptcy will be common if this lasts a year or so. The service industry for fracking will implode. Many good jobs will be lost.

- I believe the coronavirus has been overhyped and has no impact whatsoever on my activities in the oil and gas business, although it does affect the value of the capital reserves on which I rely to ride out periods of low oil prices.

- The duration of the disruption to the global economy caused by the coronavirus is anyone's guess at this point.

- The coronavirus coupled with the Saudi–Russian market share war is a perfect storm and is devastating to the market and our business plans. Fortunately, we are well-hedged through 2021, while many other companies will have their hedges roll off after 2020.

- The turmoil will create its own issues in this business but, properly managed, these are times of opportunities.

- The volatility in product prices and investment sentiment makes long planning almost impossible. Only those projects offering high return (i.e., high risk) will be considered. Nonconventional low-return shales do not appeal to our group.

Oil and Gas Support Services Firms

- We were planning for a soft 2020. Soft would be great now. We are now expecting an almost total stop in business in the coming weeks and months. It is not a pretty picture.

- The outlook does not look good for the oil industry.

- It’s the knock-on effects of COVID-19 in the form of lower demand for oil and gas that are driving our outlook lower at this time.

- COVID-19 is not the biggest problem impacting our business. The Russia–Saudi dispute is our biggest headache!

- It’s not just the virus. It's the pressure from the investment community, and how it's demanding proper returns from the operators. Moreover, there is now a steep drop in commodity prices.

- It is too early to tell on COVID-19.

Additional Comments »

First Quarter | March 25, 2020

Historical data are available from first quarter 2016 to the most current release quarter.

Business Indicators: Quarter/Quarter

| Business Indicators: All Firms Current Quarter (versus previous quarter) |

|||||

| Indicator | Current Index | Previous Index | % Reporting Increase |

% Reporting No Change |

% Reporting Decrease |

|

Level of Business Activity |

–50.9 |

–4.2 |

11.2 |

26.7 |

62.1 |

|

Capital Expenditures |

–49.4 |

–1.8 |

9.4 |

31.9 |

58.8 |

|

Supplier Delivery Time |

–10.8 |

–8.4 |

6.4 |

76.4 |

17.2 |

|

Employment |

–24.0 |

–10.0 |

7.0 |

62.0 |

31.0 |

|

Employee Hours |

–32.1 |

–7.7 |

4.4 |

59.1 |

36.5 |

|

Wages and Benefits |

–8.2 |

8.2 |

11.5 |

68.8 |

19.7 |

| Indicator | Current Index | Previous Index | % Reporting Improved |

% Reporting No Change |

% Reporting Worsened |

|

Company Outlook |

–75.0 |

1.9 |

7.9 |

9.2 |

82.9 |

| Indicator | Current Index | Previous Index | % Reporting Increase |

% Reporting No Change |

% Reporting Decrease |

|

Uncertainty |

63.8 |

26.0 |

79.4 |

5.0 |

15.6 |

| Business Indicators: E&P Firms Current Quarter (versus previous quarter) |

|||||

| Indicator | Current Index | Previous Index | % Reporting Increase |

% Reporting No Change |

% Reporting Decrease |

|

Level of Business Activity |

–53.3 |

5.4 |

9.3 |

28.0 |

62.6 |

|

Oil Production |

–26.4 |

24.7 |

18.9 |

35.8 |

45.3 |

|

Natural Gas Wellhead Production |

–21.2 |

15.6 |

16.3 |

46.2 |

37.5 |

|

Capital Expenditures |

–49.0 |

9.1 |

12.3 |

26.4 |

61.3 |

|

Expected Level of Capital Expenditures Next Year |

–61.9 |

0.9 |

9.5 |

19.0 |

71.4 |

|

Supplier Delivery Time |

–10.6 |

–5.5 |

6.7 |

76.0 |

17.3 |

|

Employment |

–22.8 |

–6.3 |

4.8 |

67.6 |

27.6 |

|

Employee Hours |

–28.5 |

1.8 |

2.9 |

65.7 |

31.4 |

|

Wages and Benefits |

–6.7 |

11.8 |

10.6 |

72.1 |

17.3 |

|

Finding and Development Costs |

–32.7 |

–20.0 |

6.7 |

53.8 |

39.4 |

|

Lease Operating Expenses |

–24.0 |

–1.8 |

7.7 |

60.6 |

31.7 |

| Indicator | Current Index | Previous Index | % Reporting Improved |

% Reporting No Change |

% Reporting Worsened |

|

Company Outlook |

–74.0 |

15.4 |

9.0 |

8.0 |

83.0 |

| Indicator | Current Index | Previous Index | % Reporting Increase |

% Reporting No Change |

% Reporting Decrease |

|

Uncertainty |

66.9 |

16.3 |

81.1 |

4.7 |

14.2 |

| Business Indicators: O&G Support Services Firms Current Quarter (versus previous quarter) |

|||||

| Indicator | Current Index | Previous Index | % Reporting Increase |

% Reporting No Change |

% Reporting Decrease |

|

Level of Business Activity |

–46.3 |

–22.1 |

14.8 |

24.1 |

61.1 |

|

Utilization of Equipment |

–47.2 |

–25.8 |

13.2 |

26.4 |

60.4 |

|

Capital Expenditures |

–50.0 |

–22.4 |

3.7 |

42.6 |

53.7 |

|

Supplier Delivery Time |

–11.3 |

–13.8 |

5.7 |

77.4 |

17.0 |

|

Lag Time in Delivery of Firm's Services |

–20.7 |

–3.5 |

1.9 |

75.5 |

22.6 |

|

Employment |

–26.4 |

–16.9 |

11.3 |

50.9 |

37.7 |

|

Employment Hours |

–38.9 |

–25.4 |

7.4 |

46.3 |

46.3 |

|

Wages and Benefits |

–11.3 |

1.7 |

13.2 |

62.3 |

24.5 |

|

Input Costs |

–11.3 |

1.7 |

5.7 |

77.4 |

17.0 |

|

Prices Received for Services |

–37.7 |

–24.5 |

3.8 |

54.7 |

41.5 |

|

Operating Margin |

–50.0 |

–39.7 |

3.8 |

42.3 |

53.8 |

| Indicator | Current Index | Previous Index | % Reporting Improved |

% Reporting No Change |

% Reporting Worsened |

|

Company Outlook |

–76.9 |

–22.4 |

5.8 |

11.5 |

82.7 |

| Indicator | Current Index | Previous Index | % Reporting Increase |

% Reporting No Change |

% Reporting Decrease |

|

Uncertainty |

57.4 |

44.0 |

75.9 |

5.6 |

18.5 |

Business Indicators: Year/Year

| Business Indicators: All Firms Current Quarter (versus same quarter a year ago) |

|||||

| Indicator | Current Index | Previous Index | % Reporting Increase |

% Reporting No Change |

% Reporting Decrease |

|

Level of Business Activity |

–47.7 |

0.0 |

19.0 |

14.4 |

66.7 |

|

Capital Expenditures |

–48.7 |

–10.0 |

18.0 |

15.3 |

66.7 |

|

Supplier Delivery Time |

–8.8 |

–10.7 |

11.5 |

68.2 |

20.3 |

|

Employment |

–25.0 |

–5.6 |

13.8 |

47.4 |

38.8 |

|

Employee Hours |

–28.0 |

–3.7 |

11.3 |

49.3 |

39.3 |

|

Wages and Benefits |

–4.0 |

22.2 |

19.7 |

56.6 |

23.7 |

| Indicator | Current Index | Previous Index | % Reporting Improved |

% Reporting No Change |

% Reporting Worsened |

|

Company Outlook |

–74.8 |

–10.0 |

8.4 |

8.4 |

83.2 |

| Business Indicators: E&P Firms Current Quarter (versus same quarter a year ago) |

|||||

| Indicator | Current Index | Previous Index | % Reporting Increase |

% Reporting No Change |

% Reporting Decrease |

|

Level of Business Activity |

–47.5 |

9.5 |

17.5 |

17.5 |

65.0 |

|

Oil Production |

–17.0 |

21.2 |

32.0 |

19.0 |

49.0 |

|

Natural Gas Wellhead Production |

–15.2 |

13.3 |

32.3 |

20.2 |

47.5 |

|

Capital Expenditures |

–46.0 |

–2.9 |

21.0 |

12.0 |

67.0 |

|

Expected Level of Capital Expenditures Next Year |

–66.0 |

–12.3 |

7.0 |

20.0 |

73.0 |

|

Supplier Delivery Time |

–6.1 |

–8.7 |

12.1 |

69.7 |

18.2 |

|

Employment |

–21.4 |

–4.8 |

12.6 |

53.4 |

34.0 |

|

Employee Hours |

–25.0 |

–1.9 |

9.0 |

57.0 |

34.0 |

|

Wages and Benefits |

2.0 |

24.7 |

21.6 |

58.8 |

19.6 |

|

Finding and Development Costs |

–36.3 |

–23.6 |

9.8 |

44.1 |

46.1 |

|

Lease Operating Expenses |

–26.5 |

0.9 |

10.8 |

52.0 |

37.3 |

| Indicator | Current Index | Previous Index | % Reporting Improved |

% Reporting No Change |

% Reporting Worsened |

|

Company Outlook |

–76.1 |

3.8 |

8.3 |

7.3 |

84.4 |

| Business Indicators: O&G Support Services Firms Current Quarter (versus same quarter a year ago) |

|||||

| Indicator | Current Index | Previous Index | % Reporting Increase |

% Reporting No Change |

% Reporting Decrease |

|

Level of Business Activity |

–48.0 |

–17.6 |

22.0 |

8.0 |

70.0 |

|

Utilization of Equipment |

–46.0 |

–16.1 |

18.0 |

18.0 |

64.0 |

|

Capital Expenditures |

–54.0 |

–23.3 |

12.0 |

22.0 |

66.0 |

|

Supplier Delivery Time |

–14.3 |

–14.6 |

10.2 |

65.3 |

24.5 |

|

Lag Time in Delivery of Firm's Services |

–22.5 |

–5.5 |

2.0 |

73.5 |

24.5 |

|

Employment |

–32.7 |

–7.0 |

16.3 |

34.7 |

49.0 |

|

Employment Hours |

–34.0 |

–7.0 |

16.0 |

34.0 |

50.0 |

|

Wages and Benefits |

–16.0 |

17.6 |

16.0 |

52.0 |

32.0 |

|

Input Costs |

–20.4 |

1.7 |

10.2 |

59.2 |

30.6 |

|

Prices Received for Services |

–44.0 |

–21.9 |

10.0 |

36.0 |

54.0 |

|

Operating Margin |

–45.9 |

–41.8 |

8.3 |

37.5 |

54.2 |

| Indicator | Current Index | Previous Index | % Reporting Improved |

% Reporting No Change |

% Reporting Worsened |

|

Company Outlook |

–72.4 |

–36.4 |

8.5 |

10.6 |

80.9 |

First Quarter | March 25, 2020

Activity Chart

First Quarter | March 25, 2020

Comments from Survey Respondents

These comments are from respondents’ completed surveys and have been edited for publication. Comments from the Special Questions survey can be found below the special questions.

Exploration and Production (E&P) Firms

- Banks are squeezing the E&P sector, including our company, and demanding we quit drilling to pay down our debt, even though we are in compliance with the terms of our credit agreement. We will likely shut down drilling next month, pay an early termination penalty to our rig contractor, and liquidate excess hedges to pay down debt. We are in survival mode now.

- The administration talks about their great relationship with Russia and Saudi Arabia. Why won’t they place one of their “perfect” phone calls to help negotiate the end of this oil war?

- Catastrophic losses in the price of listed oil and gas securities, along with the collapse in the price of oil and gas, are very discouraging. Prior to [our company] making new capital expenditures, the investment outlook must be more positive. I am scared! In my opinion, the Texas Railroad Commission (TRRC) should institute proration as we had in the 1950s and early 1960s. After proration, the TRRC should negotiate with Russia and OPEC for a production curtailment. This may require changes in federal law.

- I have never seen this scenario play out before. Increasing oil and gas supplies coupled with induced low demand from the coronavirus: a double whammy for the industry.

- The president should immediately demand that the Office of the Comptroller of the Currency waive the leverage test of 4.0 debt/EBITDA [debt to earnings before interest, tax, depreciation and amortization] for all oil and gas credits for the next six months. While we are 100 percent hedged, countless companies in our industry will go bankrupt because loans exceeding 4.0 debt/EBITDA must be classified by the lenders, which will prompt liquidations.

- We are primarily a conventional operator, with no debt.

- We are fresh off the news that Saudi Arabia is going to open up the taps on their oil and flood the market. I imagine that second and third quarter 2020 will be bad due to this news and the coronavirus (COVID-19). As a company, we're hedged pretty well on the oil side for the remainder of 2020, and we're partially hedged in 2021. If this downturn lasts longer than 2021, oil producers with debt could be in real trouble.

- This is the bust we all predicted. Shale doesn't come close to making returns at mid-$50 oil, so activity should be reduced by upwards of 75 percent. Activity will reduce for 12 months, but after companies file for bankruptcy, new company owners (i.e., restructured debt that is now equity) will be forced to drill again because Proved Developed Producing Reserves blowdown will not even cover first-lien debt. Until shale declines as a resource in five years, get ready for the 2015-through-2020 cycle to repeat.

- OPEC-plus [OPEC and select non-OPEC members including Russia] failing to agree on extending current production cuts or increasing the cuts is affecting our business. The coronavirus and its impact on the overall economy are also affecting our business.

- COVID-19 on top of Russia versus Saudi Arabia is having a killer impact on the petroleum industry. The second shoe drops on April 1, 2020, when the production “restraint” agreement by OPEC-plus comes off and the antagonists go for broke in their race to the bottom. The U.S. needs to reenact the prorationing allowables originally set up by the Interstate Oil and Gas Compact Commission to prevent resource waste, maintain tax base and employment, etc. Product price differentials versus indices are still a huge problem. Sources of capital are drying up. It is a tough outlook until 2023.

- I am not in any shale plays. We are engaged in conventional-type production that is shallow and has a low cost to access. Shale has destroyed private equity capital. Coronavirus worries are blown way out of proportion.

- If Russia and Saudi Arabia follow their expression of intent, price projections for crude oil and gas are grossly overstated and the actual pricing that will be experienced will be significantly lower, which will be disastrous for the industry. I do not believe the energy industry, except with respect to the largest producers, has the capital liquidity and reserves to survive a price collapse of the depth and time extent that will be experienced. A lot of producers in the industry will be absorbed by other producers or face liquidation as a result.

- After suffering through five-and-a-half years of weak oil prices, we are now in desperate shape. Oil production is too high for demand. Russia and Saudi Arabia have thrown the market into utter chaos. It’s hard to tell how, or when, we will restore oil prices to a profitable level. As for me, I am shutting in everything I can and cutting general and administrative expenses to minimal levels to try and ride out the storm. Those who are in debt will not survive.

- This is a perfect storm of disaster for the E&P space, as COVID-19 is killing demand, and Saudi Arabia and Russia are accelerating production to gain market share.

- We anticipate quite a bit of short-term pain for the industry but a much healthier outcome on the other side. Many uneconomic programs and wells will be shut, and in the long run, we anticipate a more sustainable price.

- The current price uncertainty makes it impossible to estimate revenue.

- We made a small natural gas acquisition that we had hoped would increase our bottom line. However, with the onslaught of the coronavirus, it may not work as we had anticipated.

- Commodity pricing projections at this time are very difficult due to the current volatility in the market, decreased demand for oil and gas, and the uncertainty as to the duration of the disruption to the economy as a result of the coronavirus pandemic.

- The oil price crash has made our company put everything except essential repairs on hold.

- The coronavirus is affecting all operations in our company.

- We are entering into the single worst reset in energy prices in my lifetime.

- Market uncertainty is an issue for all aspects of moving forward but also creates opportunities. For instance, we are currently closing a significant acquisition in which the downturn is helping facilitate and enabling the close. Good projects that can weather downside prices are gold during such stressful times.

- It is looking to be a bloodbath for most firms.

- Today’s mindset of the energy industry can be described as one of uncertainty, confusion and conflict. The hydrocarbon industries are being demonized by climate change activists, the news media and virtue-seeking politicians. These attitudes and policies are the reason many in the fossil energy industry are developing a siege mentality.

- The gas supply overhang was keeping prices down. Now the coronavirus is dampening demand. Saudi Arabia’s retaliation for not convincing Russia to collude on prices will further impact prices negatively.

- The COVID-19 crisis has changed the dynamics of the industry drastically. Predicting commodity prices is always a difficult exercise, but it’s especially difficult now. For instance, if this crisis passes in the next couple of months, the prices could jump up markedly by the end of the year. If not, we could see even lower prices than they are now.

- We believe 2020 and 2021 may be as bad as the mid-1980s. We are going to cash.

- The perfect-storm scenario is a market correction with a virus. COVID-19 is the most disruptive variable in this equation. I thought the production/consumption ratios would be steady, yet OPEC increased production in response to Russia’s increase. Decreased oil demand due to COVID-19 and increased production results in oversupply. I expect the current administration to expand the amount of crude in the strategic petroleum reserve.

- The future is uncertain due to the effects of Chinese influence over international markets.

- What is the difference between a Texas oilman and a pigeon? The pigeon can put down a deposit on a new Mercedes. For those of us in the distressed-asset side of the oil patch, things are looking up.

- The volume of oil now on the market from Saudi Arabia and Russia has crushed the oil industry. Many small to midsize companies will not survive due to that supply disruption alone. COVID-19 response, while necessary, has and will continue to reduce energy demand. These two factors independently have serious impacts on U.S. producers’ ability to continue to stay in business.

Oil and Gas Support Services Firms

- It is very hard to respond to this survey in the midst of the crisis this week. There is a great deal of uncertainty related to the oil market and how OPEC-plus will act. If the market continues to implode, the United States onshore industry will be decimated.

- Obviously, since the survey came out, the world has gone askew between COVID-19, oil prices collapsing and more. I previously commented that thinking one was making money at $50 per barrel was dreaming and public company accounting. However, it did not and does not work. At $40 per barrel, you’re in the hole; at $30, it is hard to even keep producing existing wells. Nothing can be drilled at $30 per barrel. If Russia and Saudi Arabia hold the line for nine months to a year, they can reassess and then sell oil for $80 per barrel with no competition from the United States shale. The only operating shale left in the United States would be Marcellus and Haynesville. The shutdown of shale oil drilling will support natural gas, and within six to nine months, prices per million cubic feet will rise.

- Uncertainty may be the understatement of the year so far. How can anyone plan in a period such as what we are in now? Further, how do you plan when logic does not play a part in the process? Having been in the oil and gas financial world for nearly 40 years and having seen many up and down cycles, I can honestly say I have never before experienced what has happened recently. What also needs to be stressed is while consumers are feeling relief at the gas pump, the entire industry with thousands of workers is on the brink of shutting down.

- Market uncertainty caused by both the effects of the coronavirus and the recent oil price war between Saudi Arabia and Russia have the current outlook for my company in a tailspin. It feels a lot like the end of 2014 all over again.

- Like every company in the oil and gas space, we have hunkered down. The only certainty we have now is that things will get worse in the coming months. OPEC-plus and COVID-19 have devastated any hope for a 2020 recovery. Survival is the only realistic hope for 2020 in the onshore seismic space.

- The events of the past week regarding the market-share price war between Russia and Saudi Arabia are already starting to affect the outlook to the downside. My company has already put in place hiring and wage freezes given the oil price decline and expected reduction in activity.

- We have no clue what to say about oil and gas prices.

- An air pocket is an understatement. The plunging global demand is intersecting with the supply war between Saudi Arabia and Russia. In just two days, we have already received requests for discounts.

- Uncertainty of supply in conjunction with demand issues that are exacerbated by COVID-19 is creating a temporary, perfect storm. Investors seem to be assuming that the impact will go deep into the summer, beyond where many upstream operators are hedged. 2020 feels pretty ugly right now.

- The concerns are obvious now, but it is difficult to make any meaningful predictions. We’ll probably know how COVID-19 will play out in the next four weeks, but industrial recovery will be slow if the virus is not stopped. Russia and Saudi Arabia will control our level of activity for the rest of the year. The mystery is why they have supported the United States oil and gas industry for the last two years. It was long ago in their best interest to flood the market with oil and shut down the shale boom.

- Our industry needs protection and a price floor, or we will never regain energy independence. Russia and Saudi Arabia will dictate this if the onslaught continues.

- The uncertainty since July of last year with oil and gas companies has been rough. Plus, my customers are insisting for more insurance that is out of reach for my small company of one pickup and flatbed trailer. It is getting very frustrating with so much unknown.

- This is quite possibly the most difficult situation we've seen since we started our company 12 years ago. Our industry outlook is very uncertain as most of our clients appear to have lost their financial footing. Dire is not a strong enough word.

- The OPEC–Russia price battle and COVID-19 stresses have created the most challenging environment I have seen in my career.

- The impact on our business from COVID-19 and the Saudi/Russia pricing war is not yet known. We have not seen any change in our customers' behavior just yet, but we certainly think it will change in the coming one to two months for the worse.

- Business is very slow, and work is not coming in.

- There are unprecedented circumstances surrounding all of us. The need for energy independence has never been greater in America.

Questions regarding the Dallas Fed Energy Survey can be addressed to Michael Plante at Michael.Plante@dal.frb.org or Kunal Patel at Kunal.Patel@dal.frb.org.

Sign up for our email alert to be automatically notified as soon as the latest Dallas Fed Energy Survey is released on the web.