Texas Manufacturing Outlook Survey

December 30, 2019

Texas Manufacturing Activity Expands Modestly

What’s New This Month

For this month’s survey, Texas business executives were asked supplemental questions on wages, prices and tariffs. Results for these questions from the Texas Manufacturing Outlook Survey, Texas Service Sector Outlook Survey and Texas Retail Outlook Survey have been released together. Read the special questions results.

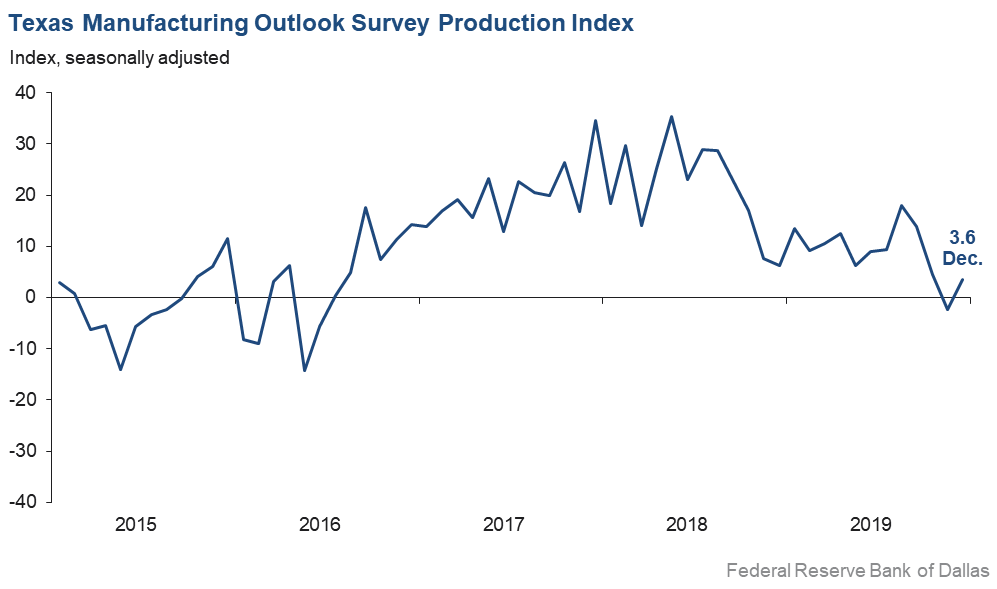

Growth in Texas factory activity resumed in December, according to business executives responding to the Texas Manufacturing Outlook Survey. The production index, a key measure of state manufacturing conditions, rebounded to 3.6 after dipping into negative territory last month.

Most other measures of manufacturing activity also rebounded in December. The new orders index rose from -3.0 to 1.6. The growth rate of orders index moved up but remained in negative territory for a third consecutive month, coming in at -5.0. The capacity utilization index shot up 13 points to 7.8, and the shipments index rose from -4.5 to 3.0.

Perceptions of broader business conditions were mixed in December. The general business activity index remained slightly negative at -3.2, while the company outlook index inched up three points to 1.3. Both indexes have oscillated between positive (expansionary) and negative (contractionary) territory this year. The index measuring uncertainty regarding companies’ outlooks receded 12 points to 5.6, its lowest reading since March.

Labor market measures suggested rising employment levels and slightly longer workweeks this month. The employment index rose from 0.9 to 6.2, indicative of a pickup in hiring. Eighteen percent of firms noted net hiring, while 12 percent noted net layoffs. The hours worked index rebounded to 2.6 after dipping into negative territory last month.

Input prices and wages rose in December, though upward pressure continued to ease, and selling prices were largely unchanged. The raw materials index declined three points to 14.5, while the wages and benefits index fell seven points to 14.6. The finished goods prices index edged down to 0.7.

Expectations regarding future business conditions remained optimistic in December. The index of future general business activity was largely unchanged at 6.4, while the index of future company outlook edged down to 13.9. Most other indexes for future manufacturing pushed further into positive territory.

Next release: Monday, January 27

|

Data were collected Dec. 16–24, and 109 Texas manufacturers responded to the survey. The Dallas Fed conducts the Texas Manufacturing Outlook Survey monthly to obtain a timely assessment of the state’s factory activity. Firms are asked whether output, employment, orders, prices and other indicators increased, decreased or remained unchanged over the previous month. Survey responses are used to calculate an index for each indicator. Each index is calculated by subtracting the percentage of respondents reporting a decrease from the percentage reporting an increase. When the share of firms reporting an increase exceeds the share reporting a decrease, the index will be greater than zero, suggesting the indicator has increased over the prior month. If the share of firms reporting a decrease exceeds the share reporting an increase, the index will be below zero, suggesting the indicator has decreased over the prior month. An index will be zero when the number of firms reporting an increase is equal to the number of firms reporting a decrease. Data have been seasonally adjusted as necessary. |

December 30, 2019

Results Summary

Historical data are available from June 2004 to the most current release month.

| Business Indicators Relating to Facilities and Products in Texas Current (versus previous month) | ||||||||

| Indicator | Dec Index | Nov Index | Change | Series Average | Trend* | % Reporting Increase | % Reporting No Change | % Reporting Decrease |

Production | 3.6 | –2.4 | +6.0 | 10.4 | 1(+) | 24.5 | 54.6 | 20.9 |

Capacity Utilization | 7.8 | –5.3 | +13.1 | 8.1 | 1(+) | 21.8 | 64.2 | 14.0 |

New Orders | 1.6 | –3.0 | +4.6 | 6.4 | 1(+) | 21.7 | 58.2 | 20.1 |

Growth Rate of Orders | –5.0 | –9.3 | +4.3 | 0.1 | 3(–) | 16.2 | 62.6 | 21.2 |

Unfilled Orders | –5.4 | –7.7 | +2.3 | –2.9 | 6(–) | 11.1 | 72.4 | 16.5 |

Shipments | 3.0 | –4.5 | +7.5 | 9.2 | 1(+) | 23.8 | 55.4 | 20.8 |

Delivery Time | –7.0 | –4.6 | –2.4 | –0.5 | 3(–) | 8.7 | 75.6 | 15.7 |

Finished Goods Inventories | –12.3 | –10.6 | –1.7 | –3.1 | 9(–) | 8.5 | 70.8 | 20.8 |

Prices Paid for Raw Materials | 14.5 | 17.8 | –3.3 | 24.7 | 45(+) | 21.5 | 71.5 | 7.0 |

Prices Received for Finished Goods | 0.7 | 1.9 | –1.2 | 6.4 | 4(+) | 10.2 | 80.3 | 9.5 |

Wages and Benefits | 14.6 | 21.1 | –6.5 | 18.8 | 125(+) | 15.9 | 82.8 | 1.3 |

Employment | 6.2 | 0.9 | +5.3 | 6.6 | 36(+) | 18.2 | 69.8 | 12.0 |

Hours Worked | 2.6 | –4.3 | +6.9 | 2.8 | 1(+) | 16.7 | 69.2 | 14.1 |

Capital Expenditures | 15.3 | 4.5 | +10.8 | 7.0 | 40(+) | 23.3 | 68.7 | 8.0 |

| General Business Conditions Current (versus previous month) | ||||||||

| Indicator | Dec Index | Nov Index | Change | Series Average | Trend** | % Reporting Improved | % Reporting No Change | % Reporting Worsened |

Company Outlook | 1.3 | –2.1 | +3.4 | 7.2 | 1(+) | 17.7 | 65.9 | 16.4 |

General Business Activity | –3.2 | –1.3 | –1.9 | 2.9 | 3(–) | 12.2 | 72.4 | 15.4 |

| Indicator | Dec Index | Nov Index | Change | Series Average | Trend* | % Reporting Increase | % Reporting No Change | % Reporting Decrease |

Outlook Uncertainty† | 5.6 | 17.1 | –11.5 | 9.7 | 19(+) | 19.6 | 66.4 | 14.0 |

| Business Indicators Relating to Facilities and Products in Texas Future (six months ahead) | ||||||||

| Indicator | Dec Index | Nov Index | Change | Series Average | Trend* | % Reporting Increase | % Reporting No Change | % Reporting Decrease |

Production | 36.9 | 31.3 | +5.6 | 38.7 | 130(+) | 49.1 | 38.8 | 12.2 |

Capacity Utilization | 35.8 | 35.8 | 0.0 | 35.5 | 130(+) | 43.9 | 48.0 | 8.1 |

New Orders | 32.6 | 28.7 | +3.9 | 36.5 | 130(+) | 42.9 | 46.8 | 10.3 |

Growth Rate of Orders | 26.8 | 19.3 | +7.5 | 26.9 | 130(+) | 35.6 | 55.6 | 8.8 |

Unfilled Orders | 0.0 | 5.7 | –5.7 | 4.0 | 1() | 11.9 | 76.2 | 11.9 |

Shipments | 30.1 | 26.2 | +3.9 | 37.5 | 130(+) | 42.3 | 45.6 | 12.2 |

Delivery Time | 4.1 | 2.7 | +1.4 | –1.9 | 3(+) | 12.4 | 79.3 | 8.3 |

Finished Goods Inventories | 8.0 | –0.9 | +8.9 | –0.5 | 1(+) | 22.0 | 64.0 | 14.0 |

Prices Paid for Raw Materials | 14.1 | 25.9 | –11.8 | 33.9 | 129(+) | 24.2 | 65.7 | 10.1 |

Prices Received for Finished Goods | 10.2 | 7.5 | +2.7 | 19.6 | 47(+) | 20.4 | 69.4 | 10.2 |

Wages and Benefits | 28.4 | 36.5 | –8.1 | 38.3 | 187(+) | 34.3 | 59.8 | 5.9 |

Employment | 17.8 | 20.6 | –2.8 | 22.3 | 85(+) | 30.1 | 57.6 | 12.3 |

Hours Worked | 9.6 | 11.1 | –1.5 | 9.4 | 43(+) | 20.5 | 68.6 | 10.9 |

Capital Expenditures | 20.1 | 9.8 | +10.3 | 20.1 | 121(+) | 33.0 | 54.1 | 12.9 |

| General Business Conditions Future (six months ahead) | ||||||||

| Indicator | Dec Index | Nov Index | Change | Series Average | Trend** | % Reporting Increase | % Reporting No Change | % Reporting Worsened |

Company Outlook | 13.9 | 17.0 | –3.1 | 21.1 | 47(+) | 25.8 | 62.3 | 11.9 |

General Business Activity | 6.4 | 7.3 | –0.9 | 14.5 | 3(+) | 17.8 | 70.8 | 11.4 |

*Shown is the number of consecutive months of expansion or contraction in the underlying indicator. Expansion is indicated by a positive index reading and denoted by a (+) in the table. Contraction is indicated by a negative index reading and denoted by a (–) in the table.

**Shown is the number of consecutive months of improvement or worsening in the underlying indicator. Improvement is indicated by a positive index reading and denoted by a (+) in the table. Worsening is indicated by a negative index reading and denoted by a (–) in the table.

†Added to survey in January 2019.

Data have been seasonally adjusted as necessary, with the exception of the outlook uncertainty index, which does not yet have a sufficiently long time series to test for seasonality.

December 30, 2019

Production Index

December 30, 2019

Comments from Survey Respondents

These comments are from respondents’ completed surveys and have been edited for publication.

Chemical Manufacturing

- The decline in business is due partly to year-end inventory reductions by customers but primarily due to the decline in oilfield activity.

- The decrease in automobile sales (worldwide) affects our customers’ businesses.

Primary Metal Manufacturing

- Our customer base still feels lots of “uncertainty” in regards to overall business levels.

- Parts of the economy have weakened. Other parts are still strong. All in all, 2020 will be a good year.

Fabricated Metal Product Manufacturing

- We are continuing to grow because of the poor condition of our water and wastewater infrastructure and the increasing need for emergency repairs.

- It seems that the general level of confidence is improving slightly and that maybe the sky is not falling.

Machinery Manufacturing

- Pricing pressure has increased.

- The end of the year is slow and steady; however, we think the orders will pick up significantly in the first quarter of 2020.

Computer and Electronic Product Manufacturing

- There is persistent uncertainty.

- With the next round of tariffs suspended indefinitely, our uncertainty of costs has decreased.

Transportation Equipment Manufacturing

- Over the next six months, we plan to increase sales and production due to an investment of stocking in a European country to expedite product into the customer’s hands.

- Our industry has weakened and our outlook forecast is soft for 2020.

Apparel Manufacturing

- We could not get material from the mill because of a testing failure. We will have to make up the delay in the first quarter of next year. This should be a very temporary situation.

Printing and Related Support Activities

- There is a chronic shortage of semiskilled and skilled machine operators.

- We were crazy busy in November, which sort of explains why December activity is lower. We had tons of overtime, and now it’s way more manageable. Billing will be way less in December than November as well, but that is in big part to having such a “hooray” November.

Historical Data

Historical data can be downloaded dating back to June 2004.

Indexes

Download indexes for all indicators. For the definitions of all variables, see Data Definitions.

| Unadjusted |

| Seasonally adjusted |

All Data

Download indexes and components of the indexes (percentage of respondents reporting increase, decrease, or no change). For the definitions of all variables, see Data Definitions.

| Unadjusted |

| Seasonally adjusted |

Questions regarding the Texas Manufacturing Outlook Survey can be addressed to Emily Kerr at emily.kerr@dal.frb.org.

Sign up for our email alert to be automatically notified as soon as the latest Texas Manufacturing Outlook Survey is released on the web.