Mexico’s economic growth continues slowing; outlook worsens

December 31, 2021

Mexico’s gross domestic product (GDP) contracted an annualized 1.7 percent in third quarter 2021, a downward revision from the initial estimate of a 0.8 percent decline. In addition, the monthly proxy for GDP decelerated in the fourth quarter. The consensus forecast for GDP growth in 2021, compiled by Banco de México, was revised down from 4.0 percent in November to 3.8 percent in December. The consensus forecast for GDP growth in 2022 is 3.0 percent (fourth quarter/fourth quarter).[1]

The latest data available show that exports fell, but employment, retail sales and industrial production improved. The peso lost ground against the dollar, while inflation soared to a 20-year high in November.

As in the rest of the world, new COVID-19 cases are on the rise in Mexico. However, new average daily infections are only 15 percent of the peak reported in mid-August. The vaccination rate has improved to 58 percent of the population.

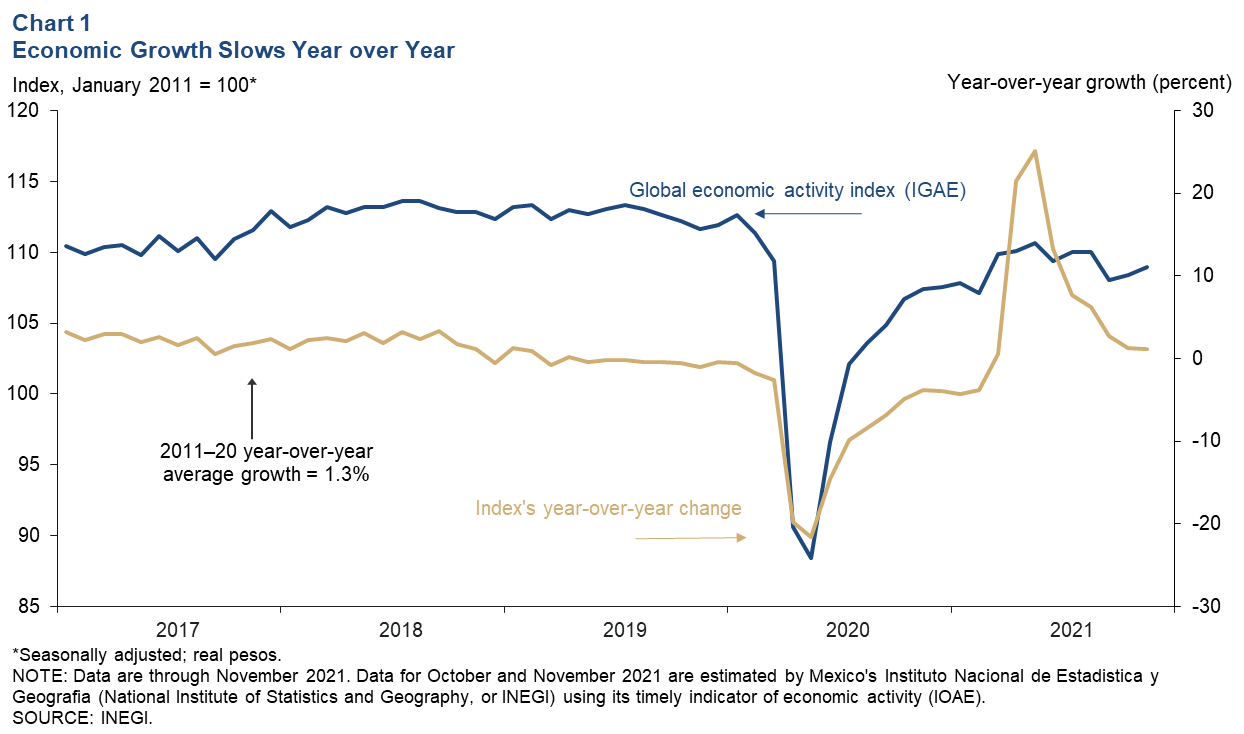

Economic growth slowing since September

Year-over-year growth in Mexico’s global economic activity index—the monthly proxy for GDP—slowed from 2.8 percent in September to 1.2 percent in November (Chart 1). Service-related activities (including trade and transportation) grew 1.1 percent in November after expanding 2.2 percent in September. Goods-producing industries (including manufacturing, construction and utilities) increased 1.4 percent in November after expanding 4.0 percent in September.

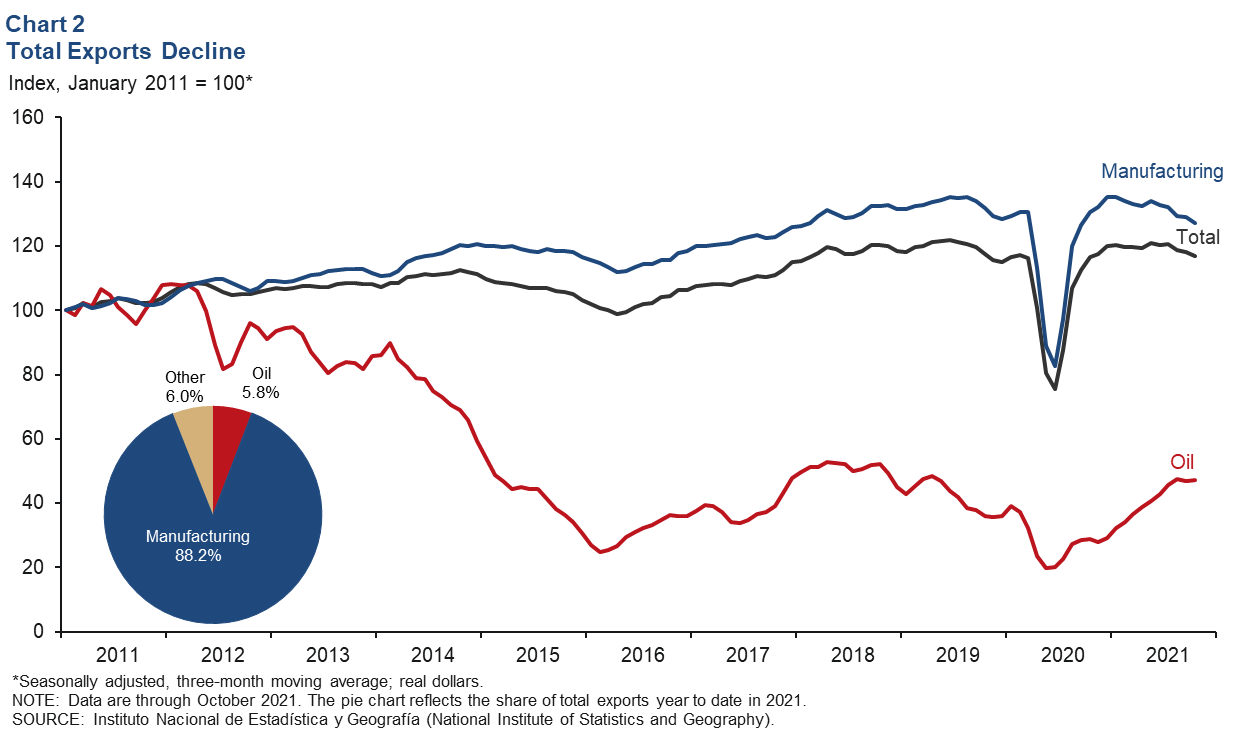

Exports slip in October

The three-month moving average of total exports fell 1.1 percent in October as oil exports grew 0.9 percent but the dominant manufacturing category decreased 1.4 percent (Chart 2). On a month-over-month basis, total exports declined 0.8 percent in October as manufacturing exports decreased 2.3 percent but oil exports rose 10.4 percent. Mexico’s total monthly exports in October were up 6.6 percent compared with prepandemic levels in February 2020.

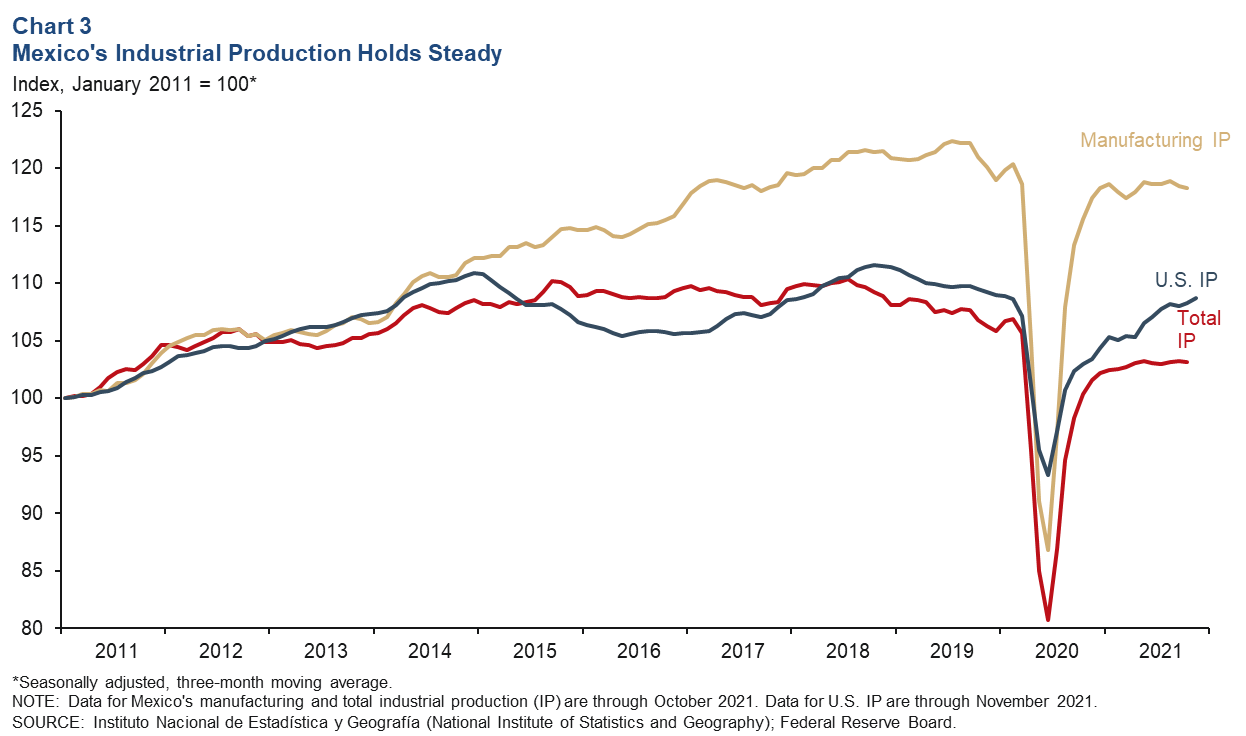

Industrial production little changed

The three-month moving average of Mexico’s industrial production (IP) index—which includes manufacturing, construction, oil and gas extraction, and utilities—was relatively flat and manufacturing IP dipped in October (Chart 3). On a month-over-month basis, IP was up 0.6 percent in October, and the manufacturing index grew 1.8 percent. North of the border, growth of U.S. IP slowed to 0.5 percent in November from 1.7 percent in October. The three-month moving average of U.S. IP was up 0.4 percent in November. The correlation between IP in Mexico and the U.S. increased considerably with the rise of intra-industry trade between the two countries.

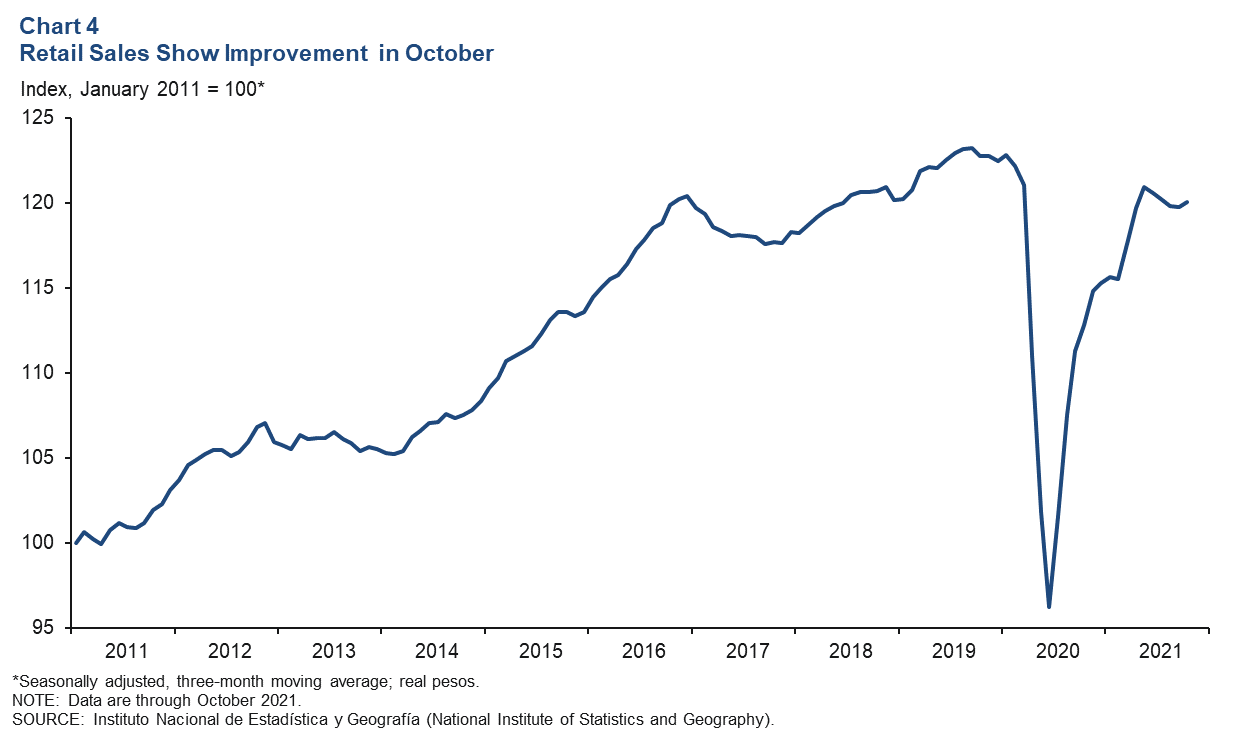

Retail sales increase in October

The index of real retail sales in Mexico increased 0.2 percent based on a three-month moving average through October (Chart 4). On a month-over-month basis, retail sales increased 0.3 percent in October, nearly the same rate as in September. October retail sales were down 0.8 percent from prepandemic levels in February 2020.

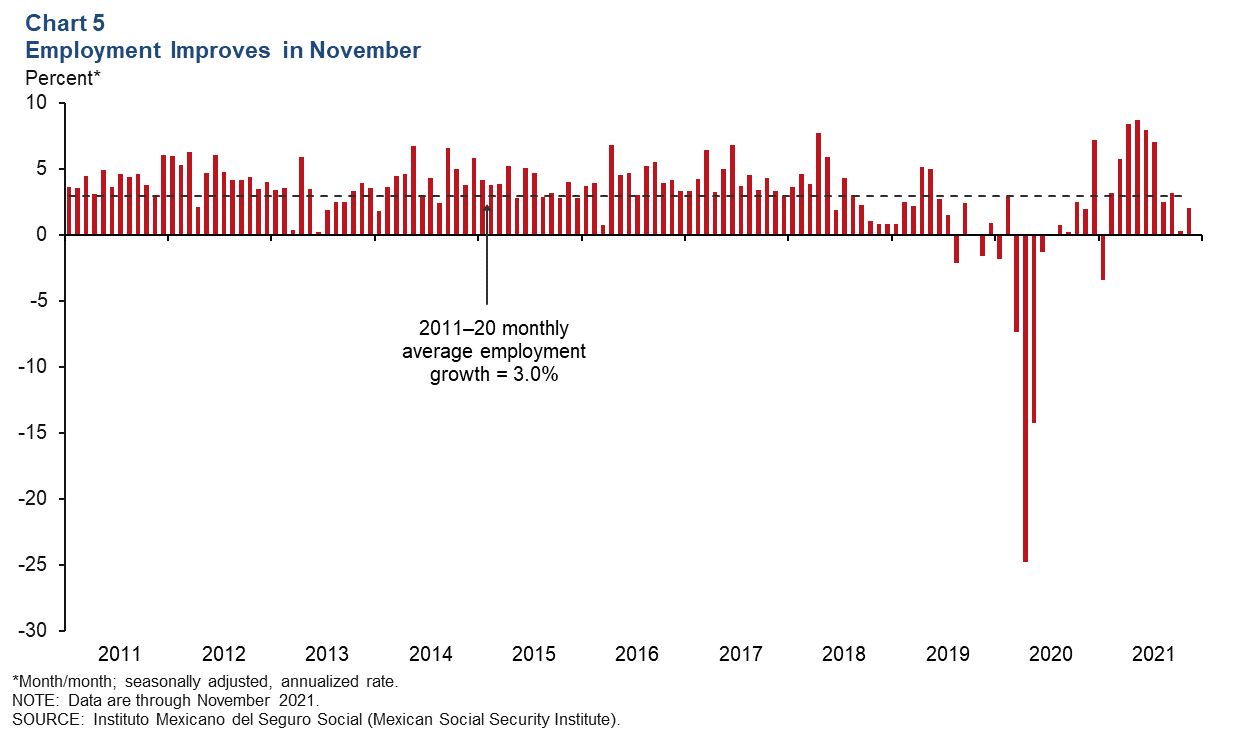

Payrolls expand

Formal sector employment—jobs with government benefits and pensions—grew an annualized 2.0 percent (34,600 jobs) in November after increasing 0.3 percent in October (Chart 5). Year-over-year employment grew 4.3 percent in November. Total employment, representing 56 million workers and including informal sector jobs, increased 9.9 percent year over year in third quarter 2021, based on the most recent data. The unemployment rate in October was 3.9 percent, unchanged from September.

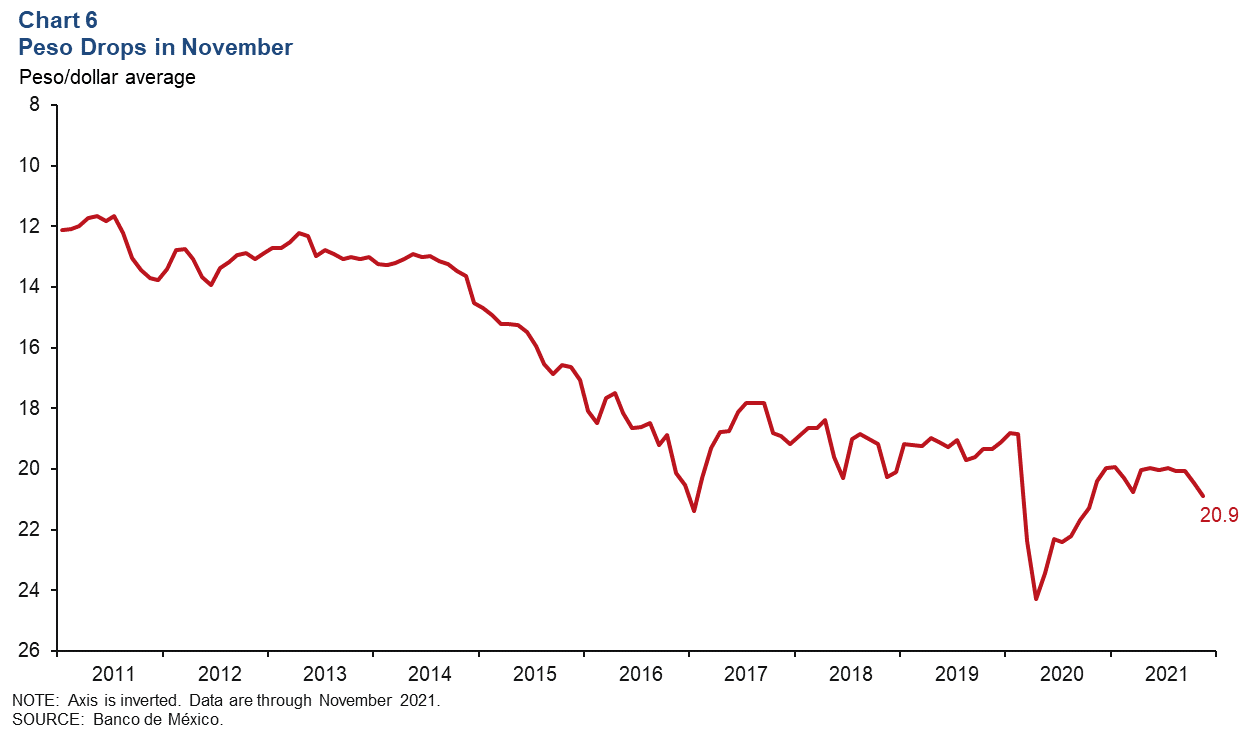

Peso loses ground against the dollar

The Mexican currency declined for the second consecutive month, averaging 20.9 pesos per dollar in November. The peso is down 9.8 percent from the prepandemic level in February 2020 (Chart 6). The peso has been under pressure due to persistently higher average inflation in Mexico than in the U.S. and, more recently, increased uncertainty regarding domestic and global growth.

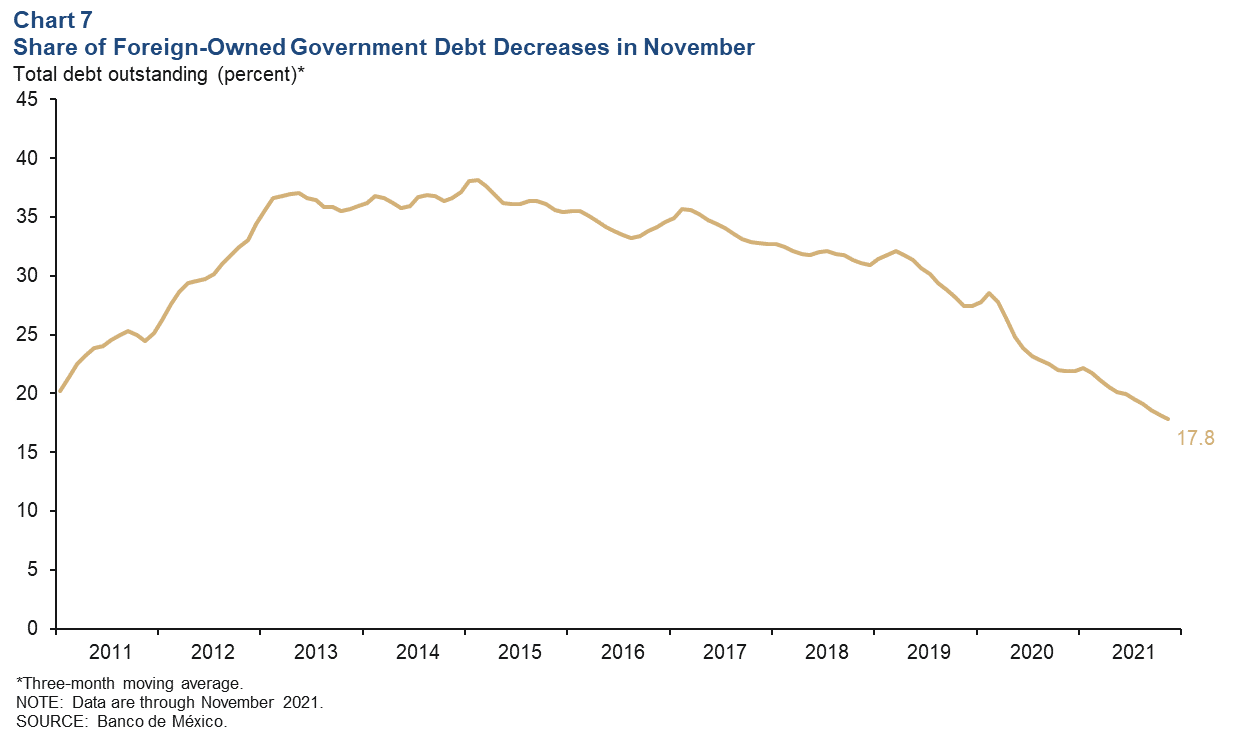

Foreign-owned government debt continues to fall

The share of foreign‐owned Mexican government securities fell to 17.4 percent in November, the lowest level since September 2010. The three-month moving average decreased to 17.8 percent (Chart 7). The extent of nonresident holdings of government debt is an indicator of Mexico’s exposure to international investors and a sign of confidence in the Mexican economy.

Inflation increases further

Mexico’s consumer price index (CPI) increased 7.4 percent in November over the prior 12 months, growing at a slightly faster rate than October’s 6.2 percent (Chart 8). CPI core inflation (excluding food and energy) rose 5.7 percent in November over the previous 12 months. In December, Banco de México increased the benchmark interest rate by 50 basis points to 5.5 percent. In the public announcement accompanying the interest rate decision, the central bank cited persistent global and domestic inflationary pressures and challenges posed by tightening global monetary and financial conditions as factors.

Note

- The consensus GDP forecast is calculated as a fourth quarter/fourth quarter growth rate. However, based on average year-over-year quarterly growth, the forecast is 5.6 percent for 2021 and 2.8 percent for 2022. See Encuesta sobre las Expectativas de los Especialistas en Economía del Sector Privado: Diciembre de 2021 (communiqué on economic expectations, Banco de México, December 2021). The survey period was Dec. 8–13.

About the Authors

Cañas is a senior business economist, and Coia is a research analyst in the Research Department at the Federal Reserve Bank of Dallas.