Mexico’s economy contracts in third quarter, outlook weakens further

| November 2025 economic report | |||

| GDP, real Q3 '25 |

Employment, formal November '25 |

CPI November '25 |

Peso/dollar November '25 |

| -1.1% q/q | 15,100 jobs m/m | 3.8% y/y | 18.42 |

Mexico’s GDP contracted in the third quarter, reflecting a 5.9 percent (annualized) decline in manufacturing output and a pullback in investment amid uncertainty about U.S. trade policy. The consensus forecast for 2025 real GDP growth compiled by Banco de México was 0.4 percent in December, unchanged from November (Table 1). The latest data available were mixed. While exports, industrial production and employment grew, output was flat and foreign direct investment declined. The peso was stable against the dollar, and inflation remained elevated.

| Table 1 Consensus forecasts for 2025 Mexico growth, inflation and exchange rate |

|||

| November | December | ||

| Real GDP growth in Q4, year over year | 1.0 | 1.0 | |

| Real GDP growth in 2025 | 0.4 | 0.4 | |

| CPI December 2025, year over year | 3.7 | 3.8 | |

| Peso/dollar exchange rate at end of year | 18.70 | 18.50 | |

| NOTES: CPI refers to the consumer price index. The survey period was December 3-8.

SOURCE: Encuesta sobre las Expectativas de los Especialistas en Economía del Sector Privado: Diciembre de 2025 (communiqué on economic expectations, Banco de México, December 2025). |

|||

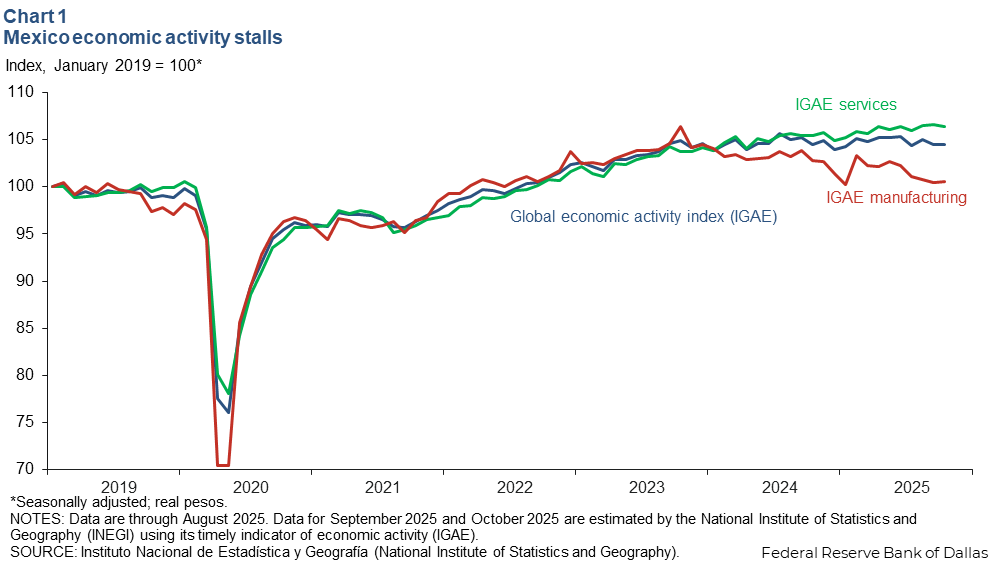

Output flat, dragged by manufacturing slowdown

The global economic activity index (IGAE), the monthly proxy for GDP growth, held steady in October after falling 0.5 percent in September (Chart 1). The goods-producing sector (including manufacturing, construction and utilities) was flat after declining for four straight months, while the service-related activities (including trade and transportation) ticked down 0.2 percent. The IGAE was unchanged year over year.

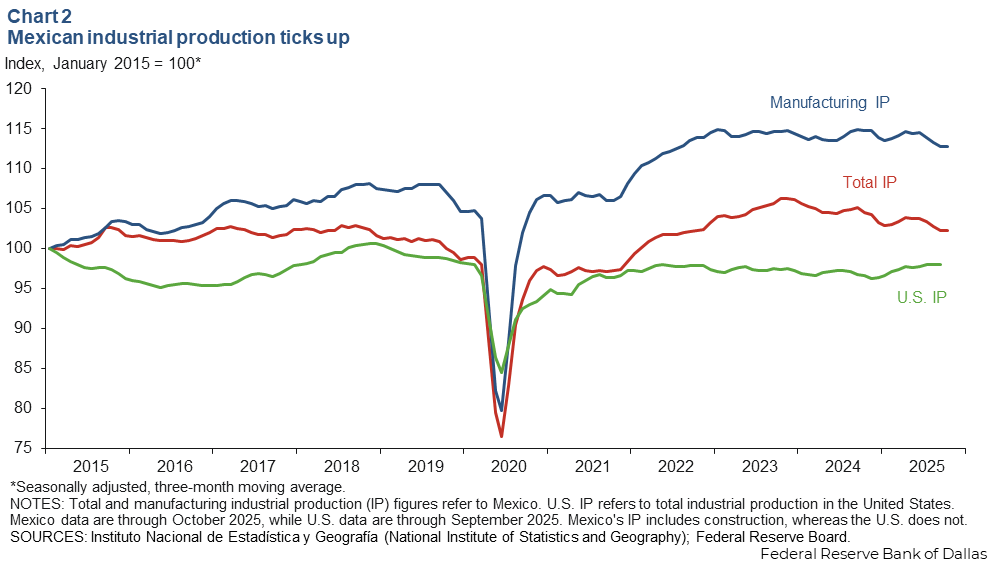

Industrial production increases slightly in October

The three-month moving average of Mexico’s industrial production (IP) index, which includes manufacturing, construction, oil and gas extraction and utilities, rose 0.1 percent in October (Chart 2). Meanwhile manufacturing IP was flat. In the U.S., the three-month moving average of IP remained unchanged in September.

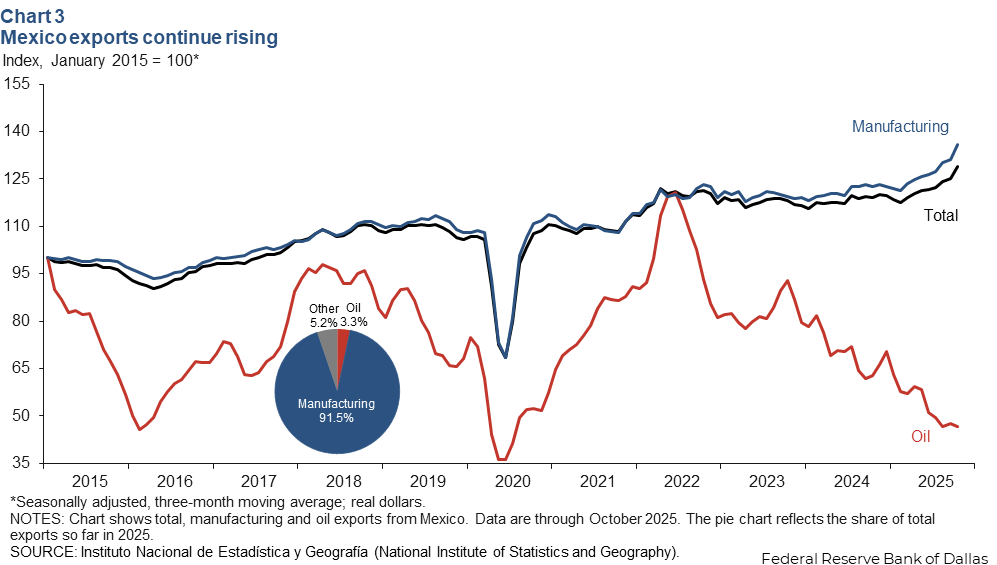

Total exports rise rapidly, driven by manufacturing

The three-month moving average of Mexico’s total exports increased 3.1 percent in October (Chart 3). The manufacturing sector, which accounts for most exports, increased 3.5 percent, while oil exports fell 2.1 percent. On a year-over-year basis, the smoothed total exports index increased 8.4 percent, while manufacturing exports increased 10.9 percent, but oil exports decreased 25.8 percent. Year to date, however, total exports grew 4.1 percent, while manufacturing exports expanded 6.1 percent and oil exports contracted 26.1 percent in October.

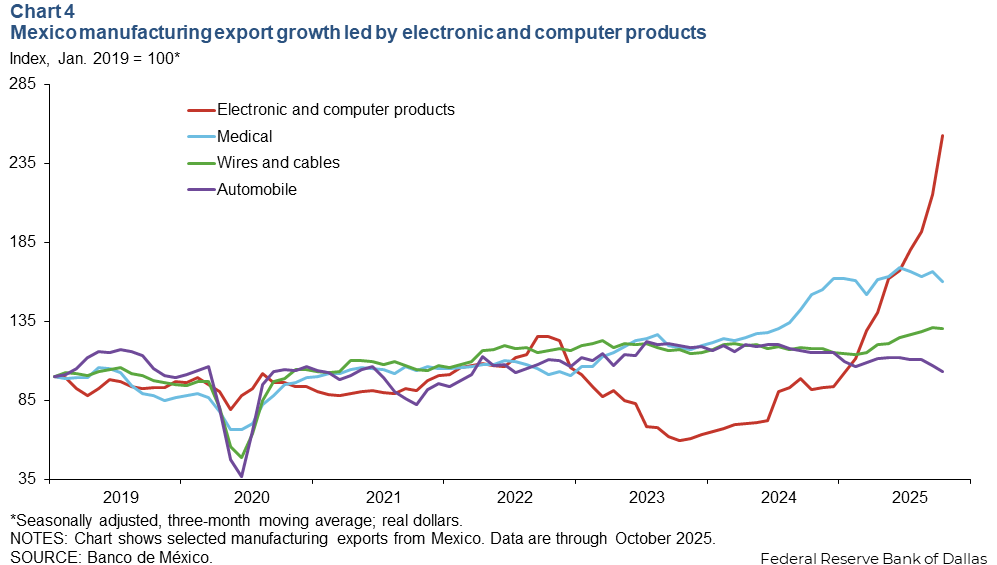

The rise in manufacturing exports was primarily driven by computer and electronic products (servers, cable and wires for servers) and medical equipment manufacturing (Chart 4). This increase is driven by robust growth in AI-related infrastructure investment in the U.S., Mexico’s top trading partner.

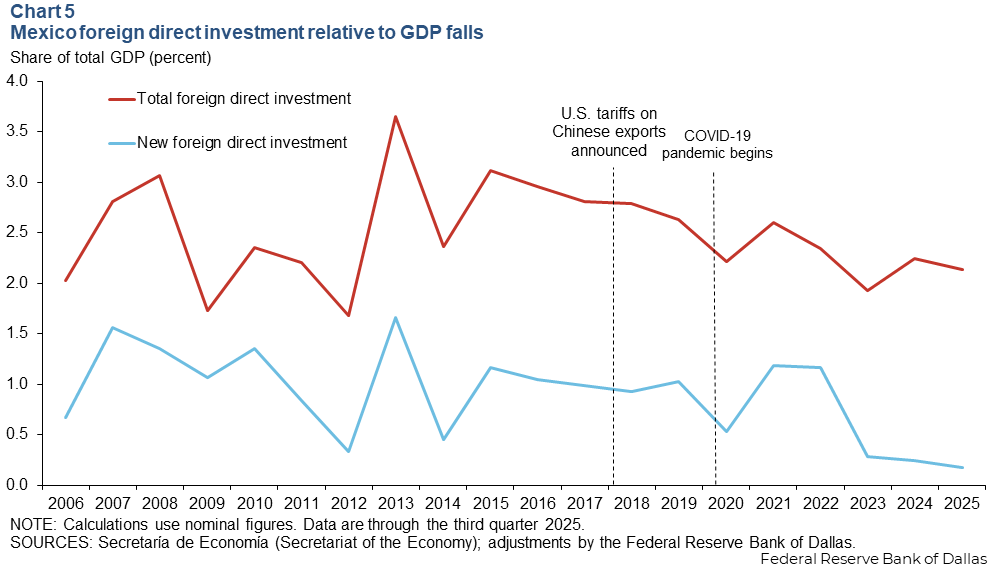

Foreign direct investment continues declining as a share of GDP in the third quarter

Foreign direct investment (FDI) relative to Mexico’s GDP fell again in 2025 after rebounding in 2024. However, the 2024 pickup in FDI was mainly due to the reinvestment of profits as new FDI has been falling since 2022 (Chart 5). The weakness in FDI this year is due to the dramatic change in U.S. tariff policy and uncertainty about the future of U.S.-Mexico-Canada Agreement.

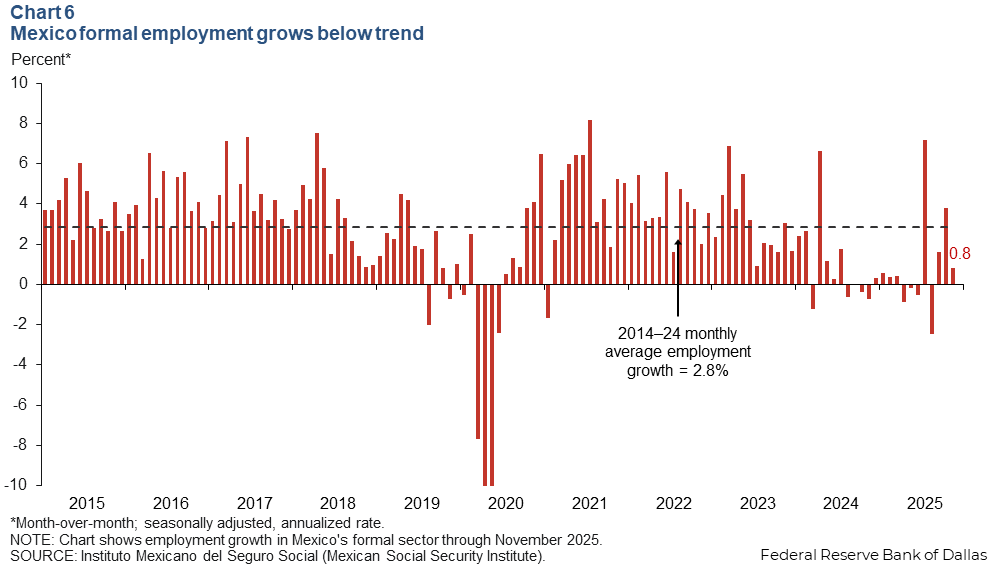

Employment growth decelerates in November

Formal employment (jobs with government benefits and pensions) grew an annualized 0.8 percent (15,100 jobs) in November after growing 3.8 percent in October (Chart 6). Compared to a year ago, employment grew a mere 0.9 percent. The unemployment rate, which tracks only the formal sector, ticked down to 2.6 percent in October.

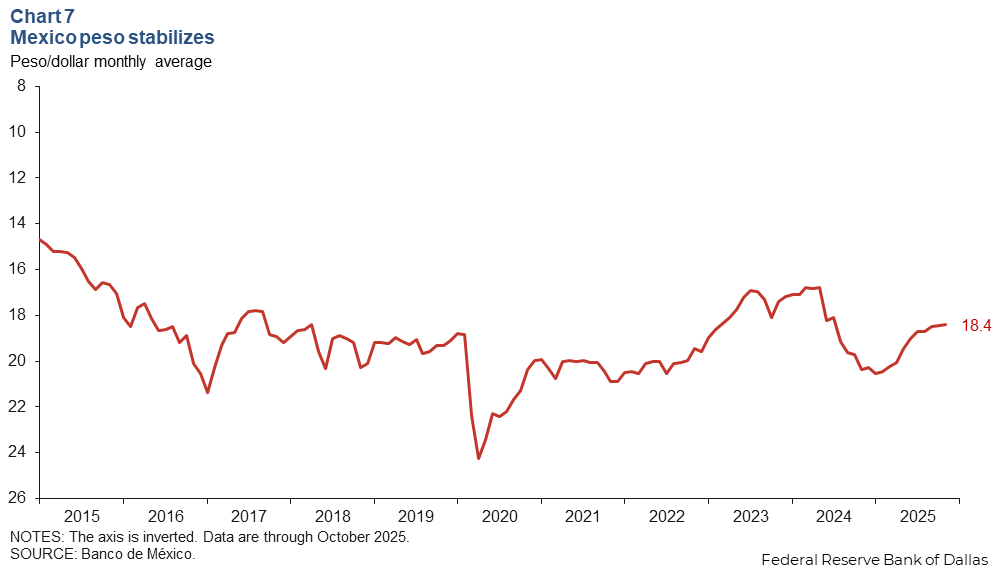

Exchange rate unchanged

The Mexican currency averaged 18.4 pesos per dollar in November and October (Chart 7). The peso has gained ground against the dollar since the start of 2025.

Inflation accelerates in November

Mexico’s consumer price index (CPI) grew 3.8 percent in November over the prior 12 months from 3.6 percent in October (Chart 8). Core CPI inflation, which excludes food and energy, rose 4.4 percent, up from 4.3 last month. Meanwhile, services inflation at 4.5 percent remained elevated and increased. In December, Mexico’s central bank lowered its benchmark rate by another 25 basis points to 7.0 percent, in line with market expectations. The central bank expects inflation to persist and foresees reaching its 3.0 percent target by third quarter 2026.

About the authors

Jesus Cañas is a senior business economist in the Research Department of the Federal Reserve Bank of Dallas.

Luis Torres is a senior business economist in the San Antonio Branch of the Federal Reserve Bank of Dallas.

Diego Morales-Burnett is a research analyst in the Research Department at the Federal Reserve Bank of Dallas.