How the Saudi decision to launch a price war is reshaping the global oil market

In the second week of March, the already fragile global oil market was rocked by Saudi Arabia’s announcement that it would expand oil production to unprecedented levels, signaling an end to its price cooperation with Russia. In response, Russia announced that it would boost oil output as well, albeit to a much smaller extent.

Saudi Arabia’s decision was a response to the dislocation in the global oil market caused by the outbreak of the coronavirus (COVID-19) against the backdrop of an already weak global economy. It is unclear whether this decision will yield better outcomes for Saudi Arabia than its passive accommodation of other oil producers did after the last global oil price decline, which started in June 2014.

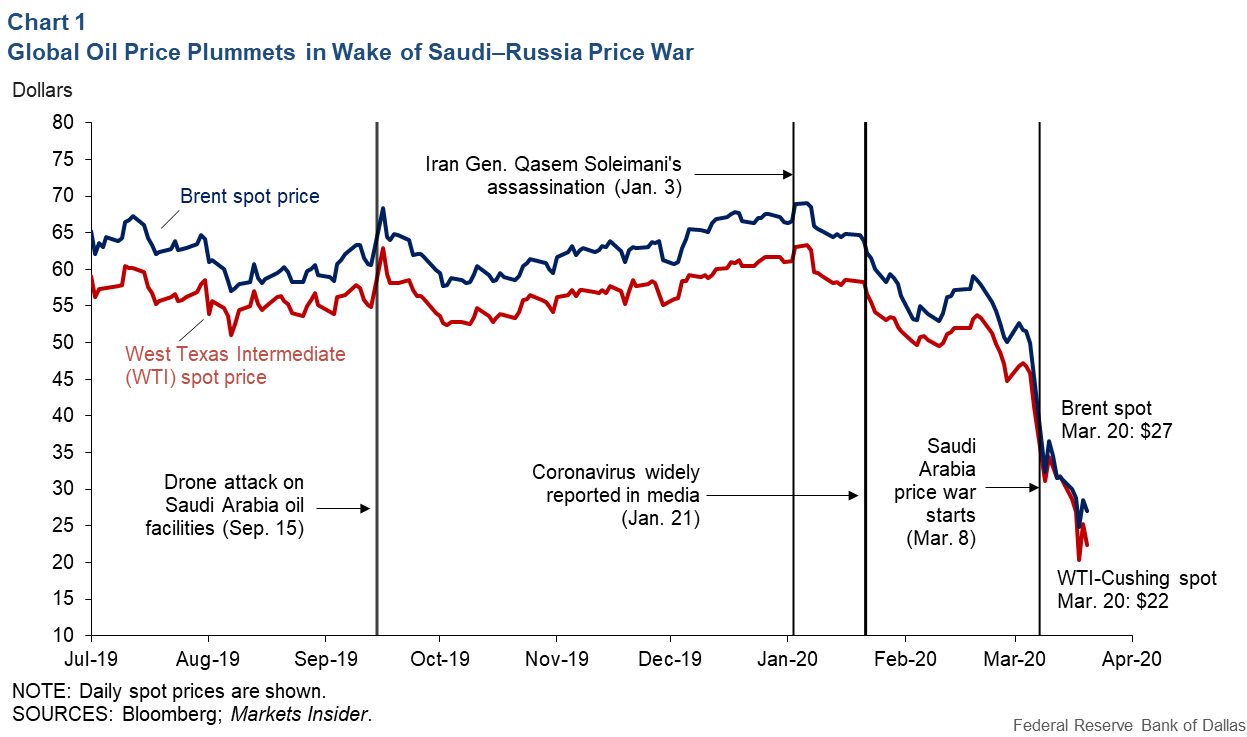

The resulting drop in the oil price from about $35 to near $20 has further exacerbated the financial stress experienced by U.S. oil producers in Texas, Oklahoma and other oil-producing regions, which were already reeling from sharp reductions in fuel demand caused by the coronavirus (Chart 1).

Who is best prepared for the long haul?

In a world of contracting oil demand, one might expect producers with the lowest breakeven price to survive and those with high breakeven prices to exit the market. The breakeven price is the oil price at which production becomes profitable. If a low-cost producer participates in a coordinated production cut, that producer cedes market share to less-competitive producers and effectively subsidizes these higher-cost producers. Not surprisingly, no competitive oil producer is keen on being in that position.

This raises the question of who the most competitive oil producers are. Saudi Arabia is commonly thought to be able to produce oil at a price as low as $10 per barrel from some fields, with Russia arguably requiring an average price of $20 or $30. These numbers have not been independently verified, but we can say with some confidence that Saudi Arabia’s cost of production tends to be lower than Russia’s and that both countries have comparatively low costs by international standards.

The focus on production costs does not tell the full story, however, because both Saudi Arabia and Russia need a high enough price not only to recoup their production costs, but also to cover their governments’ fiscal deficits. The “cost” of maintaining the political regimes in Saudi Arabia and Russia is substantially higher than their cost of oil production would suggest.

For example, it is widely believed that Russia requires $45 per barrel or higher to break even fiscally, while Saudi Arabia requires an even higher price in the long run. While oil producers may adjust their budgets to some extent, this tends to undermine their domestic political support and their ability to intervene in neighboring countries.

This comparison is further complicated by the fact that it is possible for an oil producer with large hard-currency reserves (or with access to external borrowing) to sustain a price war for months or years, even as the oil price falls below production costs. Both Russia and Saudi Arabia have been building a war chest of hard-currency reserves. Russia is believed to have a cushion of $436 billion as of January 2020, whereas Saudi Arabia retains a cushion of $491 billion, down from a peak of over $725 billion in June 2014.

Finally, Saudi Arabia enjoys the added advantage that it can partially compensate for lower oil prices by exporting larger quantities, while Russia lacks the spare capacity for large production increases. Russia, on the other hand, may benefit from a decline in the value of the ruble relative to the U.S. dollar as the dollar price of oil declines, which lowers the cost of paying domestic oil workers. This makes it difficult to predict whether Saudi Arabia or Russia will blink first in this test of wills.U.S. oil producers in a weak position

The production costs of U.S. oil producers, as in other countries, vary from one location to another and, in addition, from one firm to the next. A recent survey conducted by the Federal Reserve Bank of Dallas shows that the breakeven price of oil producers in the district ranges from $46 per barrel to $52 per barrel, with an average close to $49. This means that few oil producers will be profitable if oil prices stay below $30 for the remainder of the year. Unprofitable companies will be unable to attract enough capital to continue operations.

Unlike the state-owned oil companies in OPEC countries, U.S. oil producers are not state actors and cannot count on government subsidies when oil prices fall. Even though the Trump administration has reportedly considered low-interest government loans to oil companies affected by the price war, any such aid would pale in comparison to the subsidies available to the state-owned oil companies of Saudi Arabia and Russia.

Thus, a year of global oil prices at or below $30 is expected to push many U.S. oil companies into bankruptcy. Prolonged lower prices would accelerate this process. Consolidation in the U.S. shale oil industry is likely to be limited by the prospect of low future oil prices and the lack of capital for major acquisitions among the surviving companies.What’s the endgame?

It stands to reason that Saudi Arabia and Russia would terminate the price war as soon as U.S. shale oil production has been greatly diminished. This would provide an opportunity for coordinated supply cuts among the remaining oil producers and for persistently higher oil prices.

As prices rise, however, capital markets would view U.S. oil producers as financially viable once again, making an eventual U.S. shale oil production comeback likely. Thus, it seems unlikely that this price war will permanently vanquish the U.S. shale oil sector.

Moreover, a Saudi victory may prove to be Pyrrhic. Saudi Arabia already experienced a major drawdown in its foreign exchange reserves following the sharp decline in the price of oil after June 2014. If Saudi Arabia exhausts its hard-currency reserves with an extended price war, it will be unable to similarly threaten U.S. shale oil producers and other oil producers in the future. Thus, the global oil market will never be the same.

About the Author

Lutz Kilian

Kilian is a senior economic policy advisor in the Research Department at the Federal Reserve Bank of Dallas.

The views expressed are those of the authors and should not be attributed to the Federal Reserve Bank of Dallas or the Federal Reserve System.