What the closure of the Strait of Hormuz means for the global economy

The ongoing military conflict between Iran and the United States and Israel has raised concerns about a major disruption of global oil supplies driven by geopolitical events. This conflict has involved attacks on oil infrastructure in neighboring countries, including Saudi Arabia, Kuwait and the United Arab Emirates.

More significantly, the conflict prompted a closure of the Strait of Hormuz, through which most oil produced in the Persian Gulf is exported. Initially, this closure was mainly driven by the need to adjust insurance contracts for oil tankers. However, the ultimate concern has been attacks on oil shipping in the Strait causing unsustainable losses or shipwrecks closing the shipping lanes.

From the point of view of the rest of the world, a disruption of oil exports from the Persian Gulf is equivalent to a disruption of oil production in the Gulf. From the point of view of oil producers in the Gulf, the difference is largely academic because as soon as local oil storage fills up, oil producers have no choice but to shut in their oil wells if the oil cannot be stored or exported. This is why many oil producers, starting with Iraq and Kuwait, started curtailing their production in early March 2026.

A complete cessation of oil exports from the Gulf region amounts to removing close to 20 percent of global oil supplies from the market, about 80 percent of which is shipped to Asia. Oil importers unable to access oil from the Persian Gulf have to turn to other oil suppliers, putting upward pressure on oil prices worldwide.

How the current oil supply disruption compares to earlier geopolitical shocks

Major oil supply shortfalls driven by geopolitical events such as wars or revolutions previously occurred following the Yom Kippur War in 1973, the Iranian Revolution in 1979, the outbreak of the Iraq–Iran War in 1980 and the Persian Gulf War in 1990. What makes the closure of the Strait of Hormuz different from these earlier oil supply shortfalls is first and foremost its magnitude. For example, in 1973 and 1990 only a little more than 6 percent of global oil supplies was removed from the market and in 1979 and 1980 only about 4 percent. Today, we are concerned with a shortfall close to 20 percent, making this geopolitical event three to five times larger.

This is the first time the Strait has been closed. While some observers in 1990 grew concerned that Iraq would take over Saudi Arabia and control of the Persian Gulf, these concerns never materialized. Likewise, the oil price increase in 1979 was more about the anticipation of a major disruption of global oil supplies after the Iranian Revolution rather than an actual oil supply shortfall.

New research quantifies role of geopolitical risk

A recent Federal Reserve Bank of Dallas study formally models how geopolitically driven oil production shortfalls affect the price of oil and global economic fluctuations. Geopolitical risk involves downside risk to oil production and upside risk to the price of oil. The model accounts for the fact that major geopolitical oil supply disruptions are rare and occur with a time-varying probability.

Even the mere anticipation of a geopolitically driven oil production shortfall may generate a surge in the price of oil and a global economic contraction, regardless of whether the event in question materializes. The same is true of the realization of an oil supply disruption driven by geopolitical events. The main difference is that the former involves building oil inventories in anticipation of higher oil prices, while the latter involves drawing down oil inventories.

How the closure of the Strait of Hormuz impacts the global economy

In this article, we adapt our earlier analysis to study the effects of Iran closing the Strait of Hormuz. While our model does not account for all features of the current oil crisis (for example, we do not model the disruption of natural gas and fertilizer exports from the Persian Gulf), it captures the key economic mechanisms related to oil.

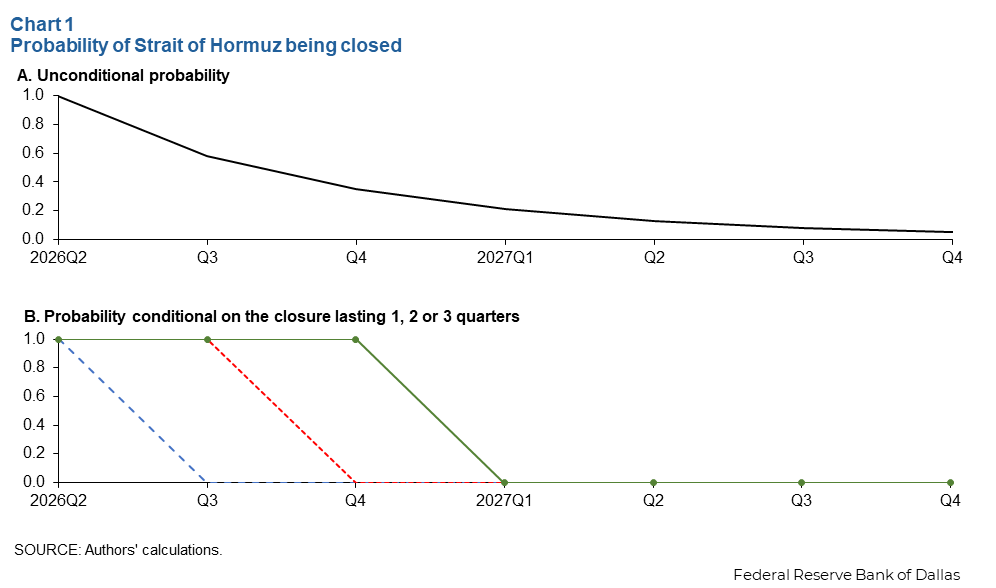

Suppose the Strait of Hormuz shuts down in second quarter 2026 for the duration of the quarter, which is the closest our quarterly model can get to mirroring the actual shutdown that occurred late in the first quarter. Market participants in the model understand that the probability of a closure in the second quarter is 100 percent. Beyond this quarter, however, the probability that the Strait remains closed steadily declines.

How fast this probability declines depends on the expected duration of the closure. For example, if the closure persists in expectation for three quarters, corresponding to the length of the 1973 oil supply disruption, there is only a 58 percent probability of the Strait remaining closed in third quarter 2026. In fourth quarter 2026, that probability further declines to 35 percent, and so forth (Chart 1, panel A). Larger or lower expected durations would push these probabilities up or down.

We do not make any projections about how long the closure will actually last, but for the purposes of discussion, we can make assumptions to illustrate the potential impact. For example, suppose the Strait reopens in third quarter 2026, after only one quarter (Chart 1, panel B). In that case, the probability of a closure is 100 percent on impact, before dropping to zero in third quarter 2026 and beyond. Alternatively, the Strait may remain closed with 100 percent probability for two or three quarters before reopening.

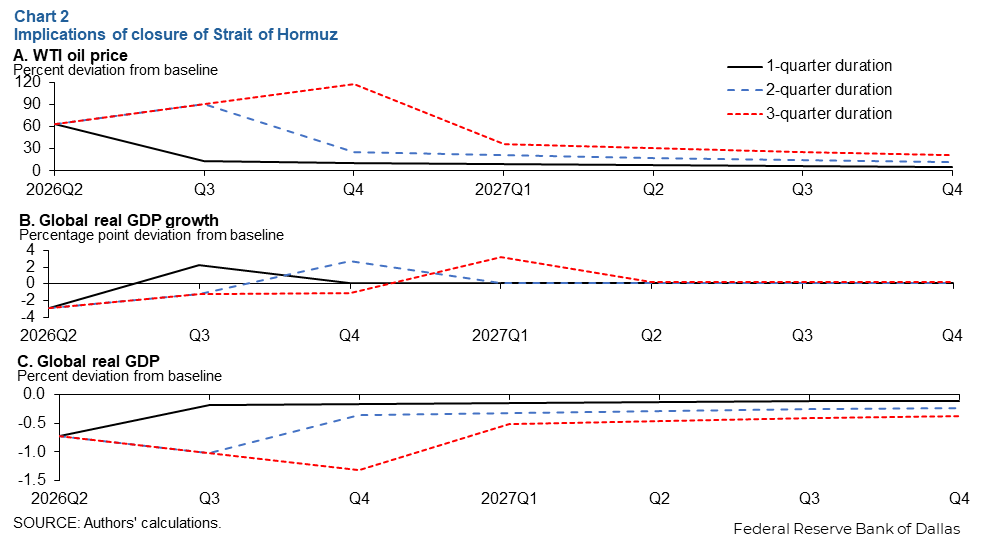

Regardless of the likelihood of the Strait reopening in the future, the model implies that a closure of the Strait of Hormuz that removes close to 20 percent of global oil supplies from the market during second quarter 2026 is expected to raise the average West Texas Intermediate (WTI) price of oil to $98 per barrel and lower global real GDP growth by an annualized 2.9 percentage points in second quarter 2026 (Chart 2).

The subsequent effects depend on when oil shipments resume. For example, if the Strait reopens after one quarter, the oil price drops to $68 per barrel and growth increases 2.2 percentage points in third quarter 2026. While the oil price drop causes growth to recover, the level of real GDP remains 0.2 percent below its pre-closure level even by year-end 2026 and 0.1 percent below its initial level by year-end 2027. The positive growth response in third quarter 2026 reflects the increased availability of oil and the resulting decline in the price of oil.

When the oil supply shortfall lasts longer than one quarter, richer dynamics arise. Extending the closure to two quarters causes the oil price to rise further to $115 per barrel in third quarter 2026 before falling to $76 per barrel in fourth quarter 2026 (Tables 1, 2). The impact on real GDP growth only turns positive in fourth quarter 2026. If shipping resumes after three quarters, the oil price will rise even further before declining, reaching as high as $132 per barrel by year-end. The impact on growth will remain negative through year-end 2026.

| One-quarter closure | Two-quarter closure | Three-quarter closure | |

| Q1 | $60 | $60 | $60 |

| Q2 | $98 | $98 | $98 |

| Q3 | $68 | $115 | $115 |

| Q4 | $67 | $76 | $132 |

| NOTES: Quarter 1 is the average West Texas Intermediate (WTI) price over the three months ended in January. The closure of the Strait of Hormuz is assumed to start in the second quarter. | |||

| One-quarter closure | Two-quarter closure | Three-quarter closure | |

| Q1 | 0 | 0 | 0 |

| Q2 | -2.9 | -2.9 | -2.9 |

| Q3 | +2.2 | -1.2 | -1.2 |

| Q4 | +0.1 | +2.7 | -1.1 |

| Q4/Q4 | -0.2 | -0.3 | -1.3 |

| NOTE: Closure of the Strait of Hormuz is assumed to start in the second quarter. | |||

Thus, fourth-quarter-over-fourth-quarter global real GDP growth in 2026 could fall 0.2 percentage points if the oil supply disruption remains limited to one quarter or 0.3 percentage points if it lasts two quarters. The reduction would increase to 1.3 percentage points if the disruption persists for three quarters. These results are useful for thinking about possible paths the economy might take in response to the ongoing struggle to control the Strait of Hormuz.

There are factors outside of the model that could cause the oil price increase to be more substantial than our model suggests. For example, dislocations in the oil tanker market and rising insurance rates for oil tankers or shifts in the market expectation of how long the Strait will remain closed could shift the oil price path higher, with implications for economic growth.

Implications for U.S. GDP growth

While the model underlying these scenarios is global, the case can be made that the effects of higher oil prices on U.S. GDP growth will be of similar magnitude to the global effects. Although the U.S. economy for many decades was heavily dependent on imported petroleum, since the shale oil boom the U.S. petroleum trade balance has been close to balanced. This makes the U.S. economy not so different from a global economy model in which there is no trade in oil by construction.

How the supply disruption may be alleviated

A key parameter of our analysis is the shortfall of oil expressed as a percentage of global oil production. For example, reducing the shortfall from 20 percent to 10 percent would lessen the effect on quarterly global real GDP growth from -2.9 percentage points to -1.6 percentage points at annualized rates.

One way the oil supply shortfall could potentially be reduced is by Saudi Arabia increasing the flow of oil on the East-West pipeline from the Persian Gulf to the Red Sea. The capacity of the Yanbu port would allow Saudi Arabia to redirect about 4 million barrels of oil per day from the Persian Gulf for transport by oil tankers from the Red Sea, corresponding to about one-fifth of the global supply shortfall.

One obvious concern with this approach is the port in question is within range of both Iranian and Houthi missiles from Yemen, as are the waterways in the Red Sea. The other concern is that shipping this oil south past the Bab el-Mandeb Strait to Asia exposes oil tankers to attacks by the Houthis, while shipping it north through the Suez Canal limits the tanker size and requires redirecting the oil toward Europe rather than Asia where it is most needed.

There is also a short pipeline in the United Arab Emirates bypassing the Strait of Hormuz to the port of Fujairah on the Gulf of Oman. That pipeline as well as the port, however, have already come under Iranian attack, making it difficult for the existing flows to be maintained, never mind increased.

Another partial remedy would be for countries such as China to negotiate deals with Iran to allow tankers carrying oil exports to China to pass through the Strait. There are indications that India has negotiated a similar deal recently.

Finally, another possible path forward is oil traffic resuming in a hostile environment, not unlike during the Tanker War of the 1980s, at the height of which on average one tanker was struck every day. As long as the tanker losses do not become unsustainable and as long as the Straits of Hormuz and Bab el-Mandeb do not become impassable because of shipwrecks, one would expect the shortage of oil to be reduced in the medium term in this case.

While it may take some time to fully restore the flow of oil through the Strait of Hormuz, a key insight from our model is that merely reducing the shortfall of oil could substantially damp the impact on the global economy. Until we reach this point, however, there is likely to be a significant impact on real activity that is unevenly distributed across the globe.

About the authors

Lutz Kilian is a vice president in the Research Department and director of the Center for Energy and the Economy at the Federal Reserve Bank of Dallas.

Michael Plante is an assistant vice president in the Research Department at the Federal Reserve Bank of Dallas.

Alexander W. Richter is a vice president in the Research Department at the Federal Reserve Bank of Dallas.