Falling oil prices drag down U.S. business investment

The dramatic decline in the price of oil has led to massive investment reductions by U.S. oil and gas producers. We expect at least a 35 percent drop in such investment between the first and second quarters of 2020 in real (inflation-adjusted) terms, which will reduce nonresidential business fixed investment by 6 percentage points alone.

The outlook for capital expenditures in 2020 is highly uncertain but skewed to the downside.

Oil and gas investment especially important

The oil and gas sector has become increasingly important for U.S. business fixed investment. Between 2010 and 2019, the sector spent $1.2 trillion drilling and completing wells—increasing U.S. crude oil production by nearly 140 percent.

Over that same period, the oil and gas sector’s share of U.S. nonresidential business fixed investment (an important component of gross domestic product) averaged 6.4 percent, nearly double prior-decade levels.

Coming into 2020, many exploration and production firms faced an inability to produce attractive returns amid heavy debt burdens and an oversupplied oil market. Investors had grown skeptical of the sector. Even before the coronavirus (COVID-19) crisis and oil price collapse, firms had planned to cut annual capital expenditures 10–15 percent relative to 2019 levels.

Crisis impact and lack of storage

Due to the COVID-19 pandemic and an oil-supply surge from Saudi Arabia, the benchmark West Texas Intermediate (WTI) crude oil price dropped from $50–$55 per barrel in February to the $20s in late March. This is far below the $46 to $52 that companies on average need to profitably drill new wells, according to the Dallas Fed Energy Survey. Although hedging—using financial instruments in the oil futures market to ensure revenue—allows some firms more breathing room during low-price periods, the overall impact to revenue for many firms is shattering.

On top of the problems with wellhead economics, many companies need to shut in existing production as oil storage capacity is reached. Global oil consumption is expected to drop from more than 100 million barrels per day in fourth quarter 2019 to 76 million barrels in second quarter 2020, according to the International Energy Agency. Consequently, refineries are processing significantly less crude oil. This backs up the flow of oil to the wellhead, which helped create "negative" prices in the oil futures market on April 20.

Accelerating capital expenditure decline in second quarter

Recent company announcements suggest declines in planned investments from 20 percent by some larger firms to nearly 100 percent by smaller ones. On balance, we estimate that these cuts sum to a decline of roughly 40 percent year over year.

Most of the impact will be felt in second quarter 2020. Business contacts and announcements by public companies show firms ending oilfield activities very quickly, with capital expenditure cuts frontloaded mostly in the second quarter. Concerns about physical storage constraints will likely speed this process. Most companies have left the door open for additional cuts. Some mention that they may ramp up spending later this year if WTI prices go above $30 with an improved outlook.

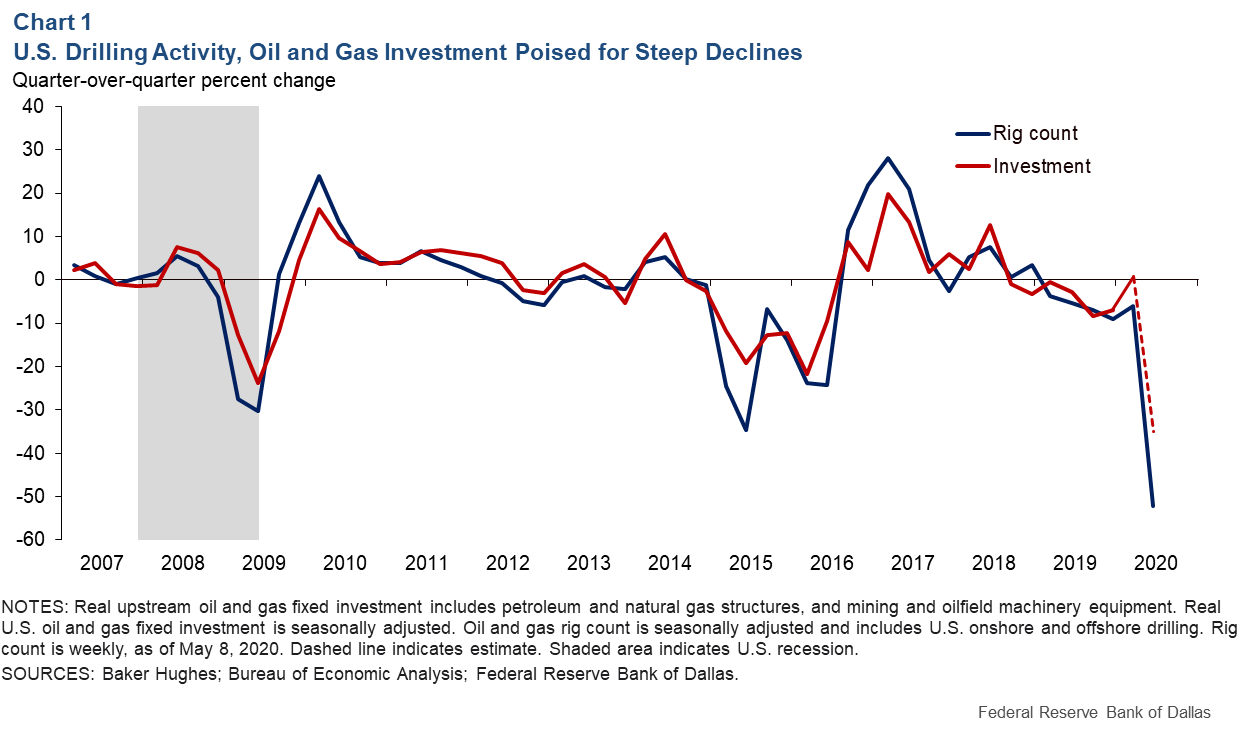

We expect industry capital expenditures to slide by about 35 percent during the second quarter (Chart 1). That would be steeper than the declines experienced in first quarter 2016 (the last time WTI prices collapsed) and during the oil bust of 1986.

The expenditure reductions are already evident in the U.S. rig count, which closely correlates with capital spending. Onshore rigs fell from 768 on March 6 to 359 as of May 8. While some companies can drop rigs immediately, others have contracts with drilling companies and leasehold obligations to fulfill before releasing rigs gradually over the next one to two months. For that reason, though the spending cuts will be largest in second quarter, they should continue into the third quarter.

Impact on U.S. business investment

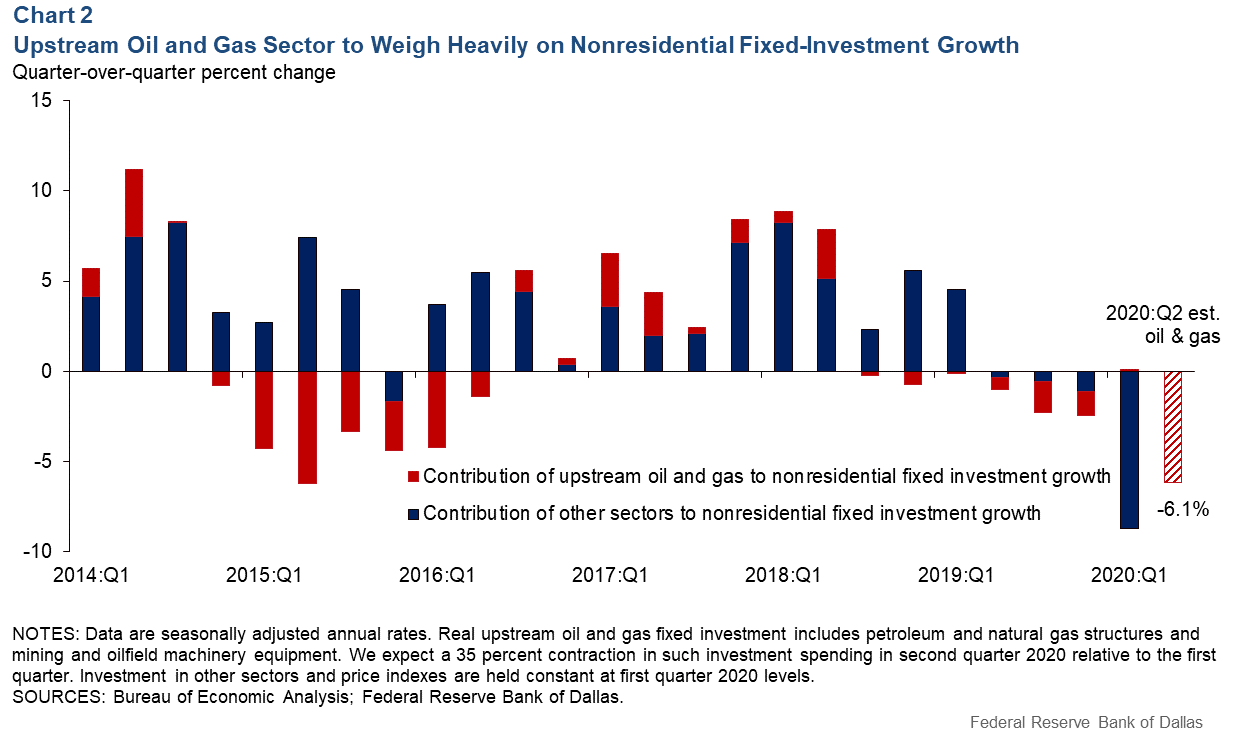

The decline in oil and gas capital expenditures will be a major drag on U.S. business fixed investment in second quarter 2020. We estimate that investment declines in the energy sector alone may lead to a 6.1-percentage-point decline in U.S. fixed investment in the second quarter.

Chart 2 shows the contribution of the sector to quarter-over-quarter fixed-investment growth. This does not account for changes in investment in other sectors during second quarter 2020, which likely also have been adversely affected by COVID-19.

The drag from oil and gas investment is likely larger than the 2014–16 period when oil prices dropped by nearly two-thirds from peak to trough, and the sector pulled down U.S. nonresidential fixed investment by about 6 percentage points. Equally, the sector weighed heavily on business investment in 2009 during the Great Recession.

Uncertain outlook

Oil and gas investment in the second half of 2020 will depend on price expectations, global storage capacity and market conditions. Industry contacts stress that the trajectory of the pandemic and its implications for global oil consumption will influence firms’ planning. Most report a very uncertain outlook.

The sudden reduction in spending also comes at a crucial time for the industry. While U.S. oil production growth was already on the verge of leveling off due in part to the steep output-decline rate of existing wells, the drilling slowdown makes it likely that U.S. output will struggle to reach its previous highs in coming years.

About the Authors

Garrett Golding

Golding is a business economist in the Research Department at the Federal Reserve Bank of Dallas.

Martin Stuermer

Stuermer is a senior research economist in the Research Department at the Federal Reserve Bank of Dallas.

Jesse Thompson

Thompson is a senior business economist in the Houston Branch of the Federal Reserve Bank of Dallas.

The views expressed are those of the authors and should not be attributed to the Federal Reserve Bank of Dallas or the Federal Reserve System.