Entry, exit of firms amplify the business cycle

When new businesses are created, they generate new jobs. When unprofitable businesses close, employees lose their jobs. Given the connection between firm entry and exit and changes in employment, it is natural to ask how this entry and exit affects the broader business cycle.

For example, to what extent do business shutdowns exacerbate economic downturns through increased unemployment? Can this mechanism explain the asymmetric patterns in macroeconomic data? It appears that the entry and exit of businesses—including of the type resulting from the COVID-19 outbreak—play an important but underappreciated role in the dynamics of employment and the macroeconomy.

In recent work, we study business behavior and the business cycle through the lens of a macroeconomic model similar to those used by researchers and policymakers around the world. We pay particular attention to two special properties of our framework: the link between business entry and exit and the dynamics of the unemployment rate and, secondly, the consequences of entry and exit on output.

Macroeconomic volatility and asymmetry

When an economy goes into recession, profits decline, and some businesses shut down. As a result, a fraction of workers quickly become unemployed and output growth slows. In contrast, as the economy recovers and enters a boom phase, employment growth occurs slowly as new and existing businesses increase their workforces. This mechanism causes asymmetry in the dynamics of employment and output growth over time.

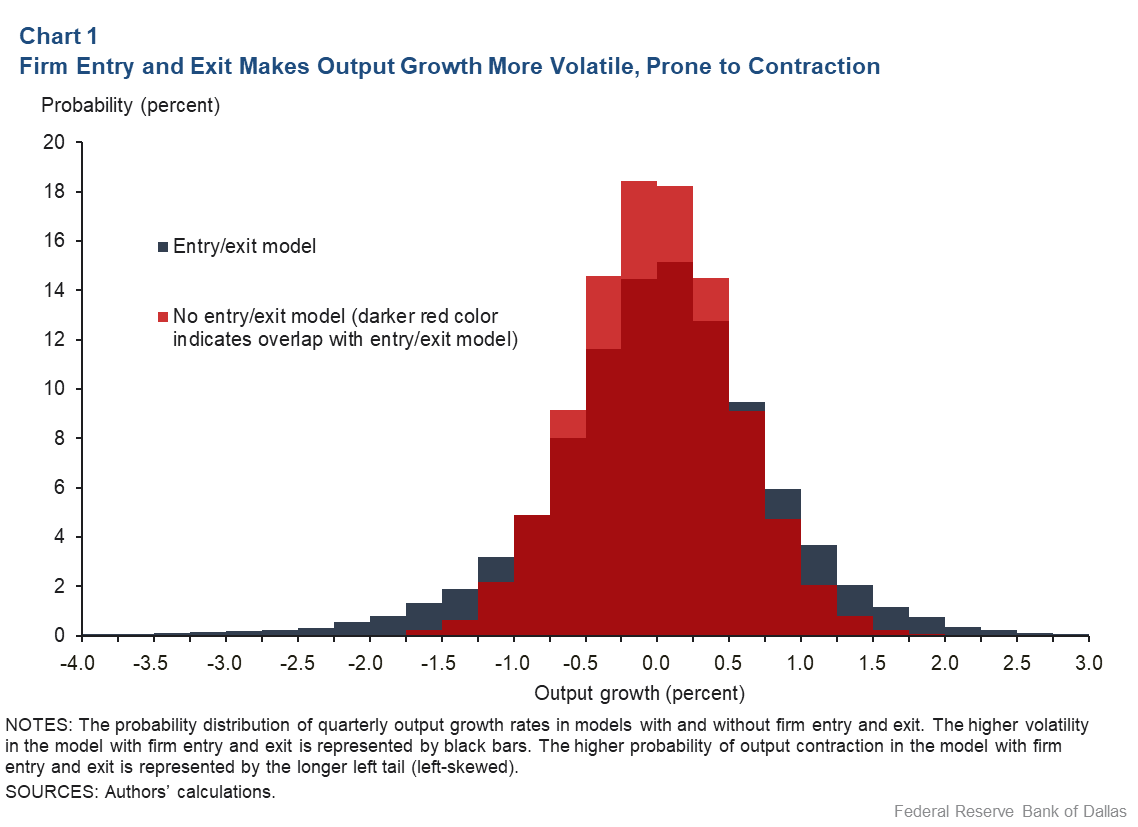

Chart 1 demonstrates the significance of firm entry and exit for the business cycle. It shows the probability distribution of simulated quarterly output growth rates in the theoretical models with firm entry and exit (black bars) and without entry or exit (red bars). Negative growth rates are more likely associated with a recession, whereas positive growth rates correspond to boom periods. A wider probability distribution indicates the model predicts more volatile output growth rates.

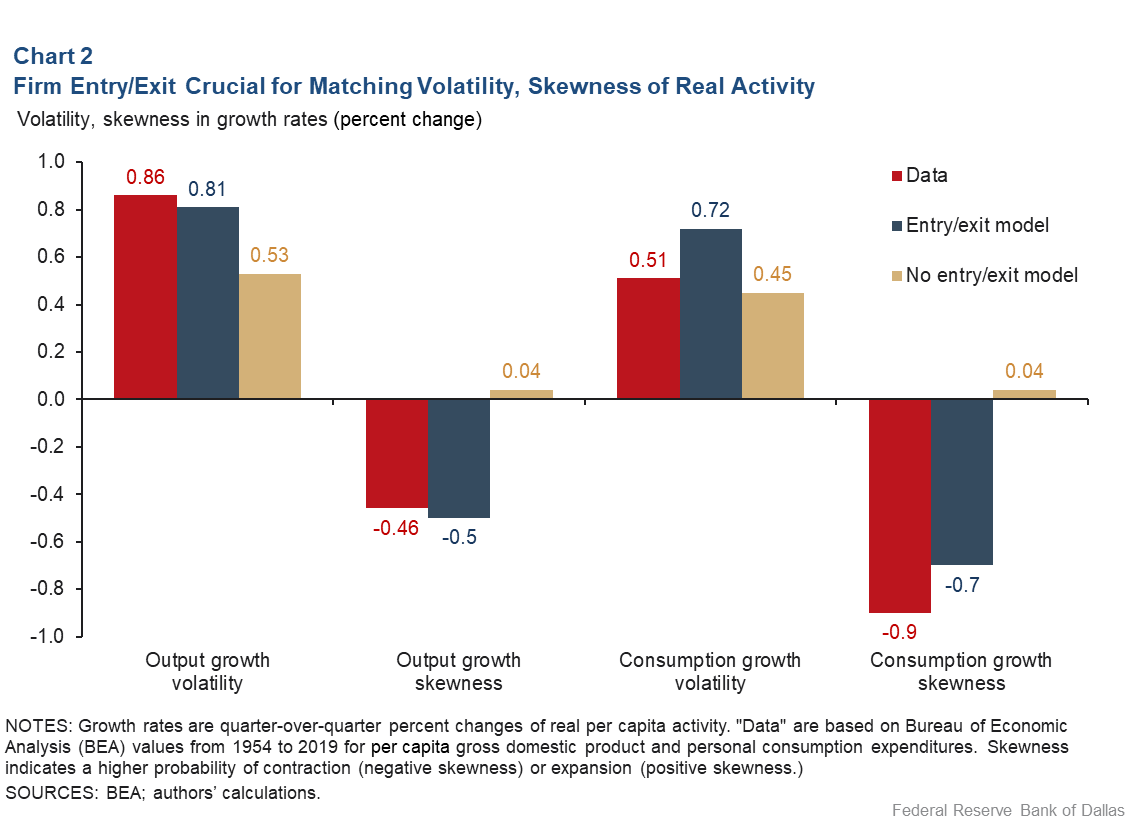

Chart 1 shows that the model with firm entry and exit predicts output growth rates that are more volatile than the model without entry or exit. Chart 2 shows the model with entry and exit closely matches the volatility of output growth rates as measured by per capita U.S. gross domestic product (GDP) from 1954 to 2019, according to the Bureau of Economic Analysis (BEA). After removing entry and exit, the model significantly underpredicts the volatility of output growth. This indicates that the entry and exit mechanism is an important explanation for both recessions and boom periods over the business cycle.

A probability distribution with a longer left than right tail indicates there is a higher probability of contraction (a negative output growth rate) than expansion (positive output growth rates). A distribution with that feature is negatively skewed. Chart 1 shows that the model with firm entry and exit predicts output growth rates that are negatively skewed; the model without entry or exit predicts symmetric growth rates.

In other words, the risk of a recession (negative growth) is higher than an economic boom (highly positive growth). Chart 2 shows the firm entry and exit model closely matches the skewness in the data, whereas the model that excludes this mechanism essentially generates no skewness.

Chart 2 shows that similar insights apply to consumption growth. The firm entry and exit model predicts consumption growth rates that are more volatile and negatively skewed than the model without firm entry or exit. The negative skewness is consistent with data on per capita U.S. personal consumption expenditures on nondurable goods and services from 1954 to 2019, as reported by the BEA.

Macroeconomic tail risk

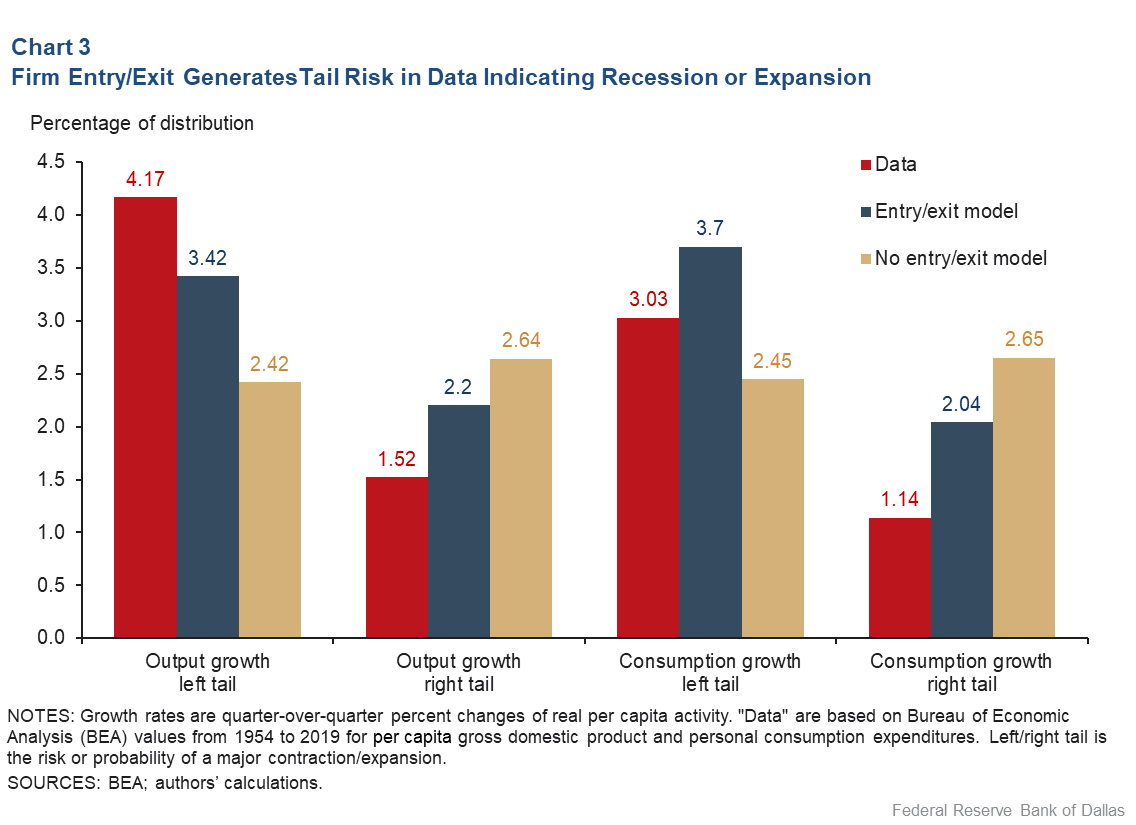

To measure the relative likelihood and severity of recessions versus booms, consider the notion of tail risk, which is the probability of an extreme outcome. Tail risk is measured relative to a normal distribution—a symmetric set of outcomes that cluster around the mean—which has a total tail risk of 5 percent (a 2.5 percent chance that an extremely low or high outcome occurs).

Chart 3 depicts tail risks in both the data and models with and without business entry and exit. The data feature significant left tail risk, meaning there is an elevated probability of extremely low realizations of output or consumption growth. The firm entry and exit model has the same feature.

When the economy enters a recession, some businesses shut down and unemployment increases. As a result, continuing businesses face lower demand and do not need to maintain as large a workforce. This leads to a drop in new vacancies, which amplifies the drop in unemployment and output growth.

Interaction with the COVID-19 pandemic

The sudden drop in economic activity caused by the COVID-19 crisis and ensuing stay-at-home policies has led to rising unemployment and sharply declining business profits. Our model is useful for analyzing how these prevailing conditions could affect the economy’s response to further deterioration—for example, disrupted supply chains and production processes or lower labor productivity arising from the pandemic.

The entry and exit margin is a source of significant amplification. Further economic disruption when profits are already low causes a sweep of business shutdowns. This leads to a larger and more persistent increase in unemployment and decrease in output growth relative to a situation where firms did not close.

These results suggest that policymakers should focus on ensuring that businesses are able to survive the crisis in addition to increasing demand for goods and services by sending checks to families to replace incomes of unemployed workers.

About the Authors

The views expressed are those of the authors and should not be attributed to the Federal Reserve Bank of Dallas or the Federal Reserve System.