Blockchain technology aims to expand role of digital transactions on internet

Despite the technological innovations the internet has brought, most economic transactions require the presence of at least one central intermediary that often controls the terms of trade.

Intermediaries are banks, insurance companies and other economic agents that profit from interfacing between providers of services and final users to facilitate transactions. However, they do so at a cost while sometimes raising some fundamental concerns.

First, the presence of a middleman can lead to market power that potentially can be abused. Second, there is the possibility of fleeting commitment and the potential for conflict of interest. Finally, almost all existing intermediaries use opaque proprietary platforms that prevent interoperability and, thus, create “walled gardens.” For example, Apple strictly controls which mobile phone applications can be installed on its operating system.

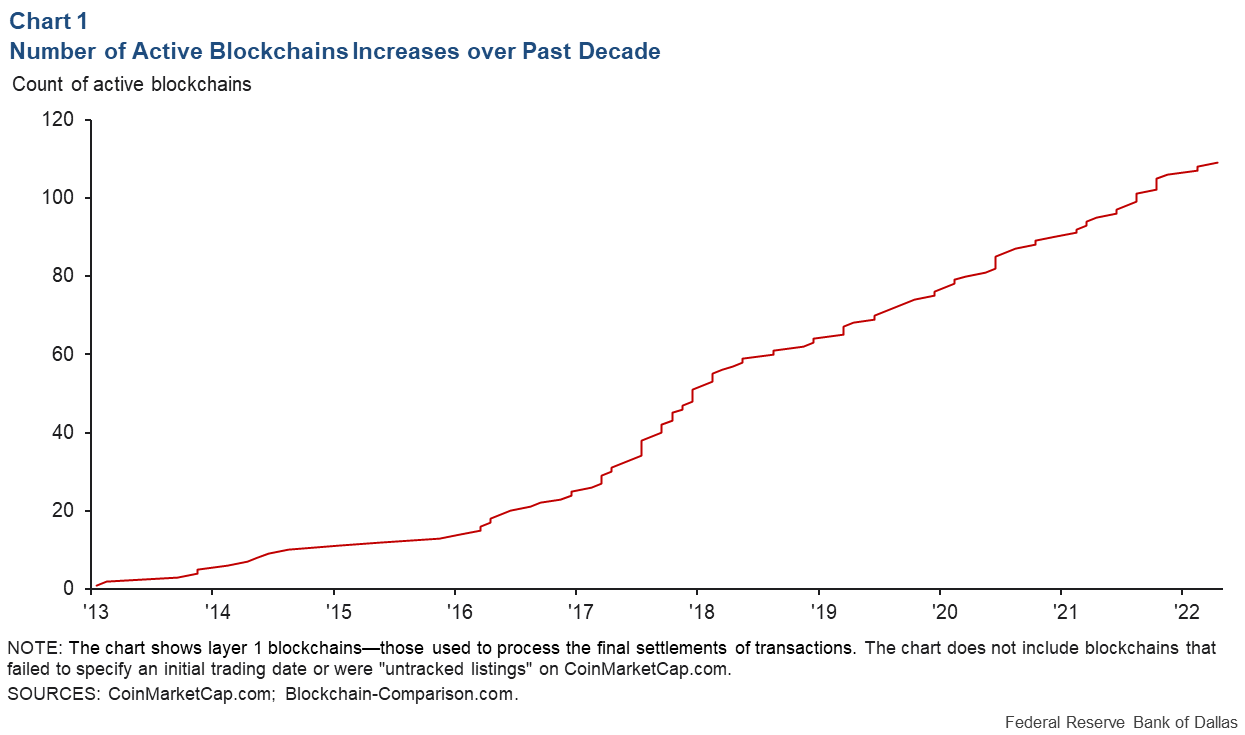

Blockchain technology, a relatively recent development, promises to address some of these structural problems. In simple terms, a blockchain is a ledger on which transactions are organized and recorded, much in the same way they would be in an accounting ledger (Chart 1). Blockchain applications are being developed for a multitude of endeavors, among them finance, supply chain-management, gaming, digital identity, land titling and the arts.

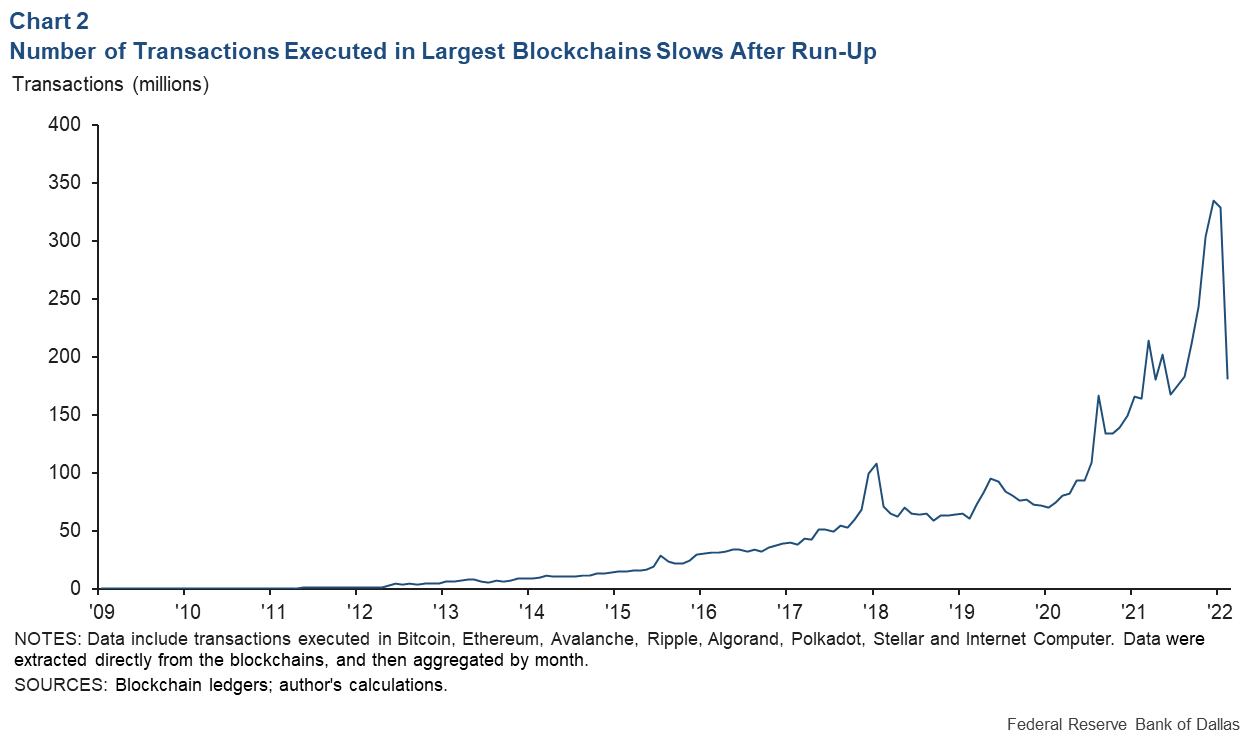

Although the number of blockchain initiatives has steadily increased over the past decade, most of the activity, measured by the number of transactions, is concentrated in the largest chains, such as Bitcoin and Ethereum. They have moderately contracted in recent months (Chart 2).

Eliminating the middleman

In a traditional intermediated and centralized ledger, a single entity is responsible for approving, viewing, auditing and deleting transactions. For example, if you do not pay with cash, only your bank or credit card company can “edit” your account by approving every transaction you make. In a blockchain, governance is decentralized. Users interact with each other through a protocol that is available for anyone to use.

Because many people can edit the ledger, an economic mechanism is required to guarantee that no one illicitly alters its content. Thus, a transaction is recorded only if enough agents—called validators—agree that the transaction, in fact, occurred. In order to align the interests of the validators with the interests of the users, the network rewards validators in the form of a token (commonly referred to as cryptocurrency) that loses value if the integrity of the ledger is violated.

Initially, blockchain technology was envisioned primarily for digital payments—“a peer-to-peer electronic cash system” in the words of Satoshi Nakamoto , the inventor of the Bitcoin protocol. To support the digital payment system, a digital token (bitcoin) was created in lieu of traditional currency, under the assumption that its value would depend on people’s willingness to accept it as a medium of exchange. Since then, many more tokens that serve as the currency for other blockchains have been created.

One important feature is that, similar to a physical coin, a digital token can be directly controlled by the owner without centralized intermediation. This is possible because a digital currency has a unique unforgeable identifier, a public key, that only the legitimate owner of the currency can transfer.

This type of peer-to-peer system differs from traditional electronic payment systems, which rely on traditional fiat currencies (dollars, euros and pounds, for example) that are, in the end, a liability of the central bank that issues them. A traditional electronic payment system simply connects financial institutions and merchants but still eventually requires a net settlement at the central bank level.

‘Smart contracts’ automatically execute transactions

Most blockchains work seamlessly with smart contracts—programs that are automatically executed when specified conditions are met. This is because they process digitally native transactions with digitally native currency.

Smart contracts are key to the application of decentralization through blockchains because they automatically follow predetermined rules. Imagine a bank that does not make a subjective judgment about whether someone should or should not get a loan but only lends money if the borrower has enough collateral.

In the span of a few years, blockchain technology has evolved from Bitcoin to a new economic system, Web 3.0, in which decentralized applications use smart contracts to allow users to interact with each other and exchange value securely and anonymously without relying on a centralized intermediating platform.

A unique feature of blockchain is the high level of transparency and decentralization of its infrastructure. All protocols are built through open-sourced collaborations among a decentralized network of developers.

No one owns or controls the protocols, which are managed and updated by all stakeholders through a consensus system. The code used by the protocols is public and available for anyone to see, audit and copy. Transactions are visible for anyone to monitor and verify.

Legolike packaging of financial transactions

Another important characteristic is the concept of composability—"money Legos,” as it is metaphorically known. Because of the open-source nature of the protocols and their interoperability, multiple transactions can be stacked on top of each other—like Lego pieces—to create faster, cheaper and more convenient products.

For example, this composability may soon allow you to get a home-equity loan, exchange dollars into euros, buy a flat in Paris, hedge the currency risk with futures, and donate any unused funds to charity. The entire sequence of collection will require just a few lines of code executed by smart contracts in a decentralized ledger that is not owned by anyone and is collectively operated by individuals anonymous to one another.

Navigating new challenges

A number of challenges remain with blockchain. Finding consensus across a large network of users in a decentralized environment can be slow and expensive. The larger the network, the more expensive it becomes to operate.

Thus, the main feature that makes blockchain appealing—its decentralized structure—could become the main obstacle to its wider adoption. Not coincidentally, most of the recent innovations have been geared toward creating faster and more efficient protocols, increasing their ability to scale applications.

The global scope of blockchains presents another challenge. By design, anyone in the world can access and participate in these peer-to-peer networks. At the same time, laws, regulations and practices significantly differ across countries. To thrive, blockchain initiatives will have to find ways to create regulatory compliance mechanisms that differ from the traditional consolidated approach that centralized businesses take.

For example, there is no identity on the blockchain, and every user is identified by public/private key pairs. This is a core feature of blockchain technology, and it does not fit well with existing anti-money-laundering practices. At the same time, blockchain technology is fully transparent and transactions are traceable. Bad actors can be identified and prevented from operating in most protocols and from off-ramping to the traditional financial system.

While the resources devoted to blockchain technology development have increased dramatically the past few years, the technology’s ultimate success depends on whether blockchain protocols can interact with the current economic landscape and how that occurs.

About the Author

Alessio Saretto

Saretto is a senior research economist and advisor in the Research Department at the Federal Reserve Bank of Dallas.

The views expressed are those of the authors and should not be attributed to the Federal Reserve Bank of Dallas or the Federal Reserve System.