Decentralized finance proposed as alternative to traditional financial services

Decentralized finance, or DeFi, seeks to reinvent how financial services are created and maintained. DeFi applications allow users to directly interact with each other to borrow, lend, insure and exchange digital assets without centralized intermediaries, such as banks and custodial exchanges.

More generally, DeFi is a set of financial services offered through smart contract protocols—pieces of computer code that automatically execute transactions when specified conditions are met. DeFi utilizes blockchain platforms, a relatively new nonproprietary innovation allowing bookkeeping without an intermediary. Ethereum, Solana and Avalanche are among the blockchains that support DeFi applications.

The ultimate goal is to increase financial market participation by reducing costs and redistributing profits directly to users.

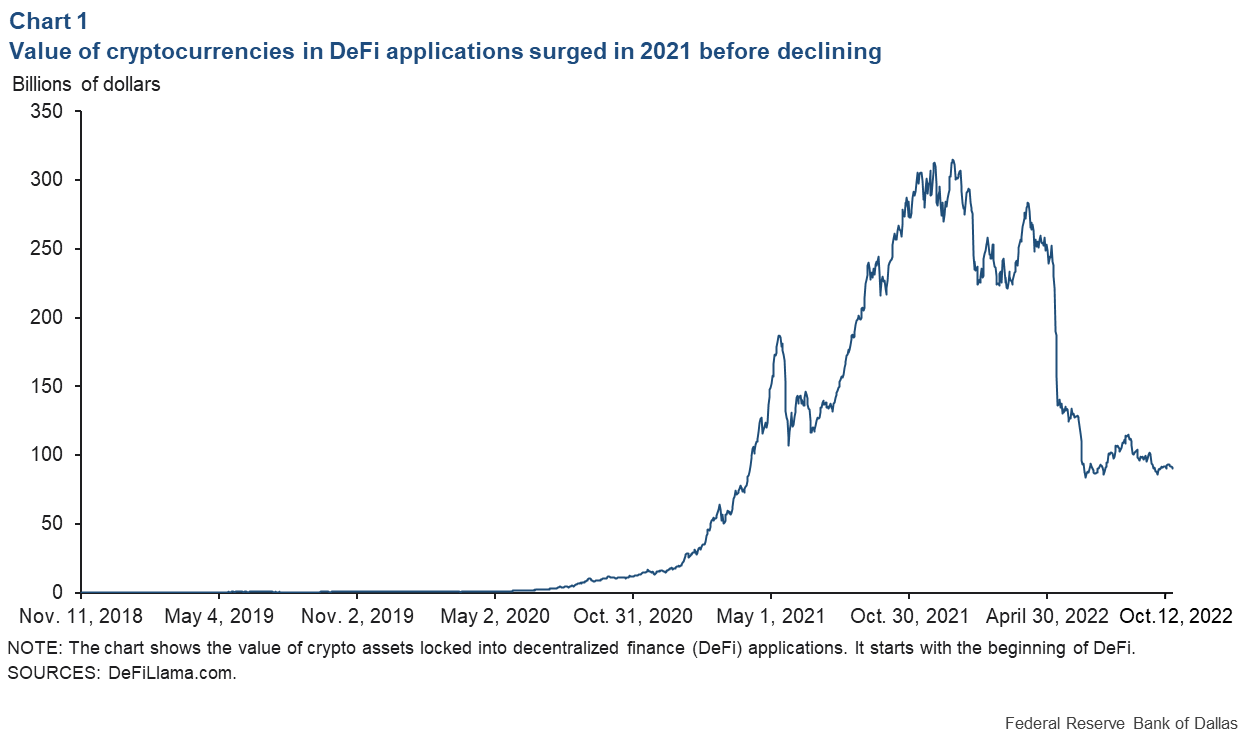

The DeFi user base has grown rapidly since the first applications were developed in 2018. At the peak in 2021, DeFi applications exceeded $300 billion in funds committed to various projects with a transaction volume of more than $1 trillion. Since then, the value of such commitments has decreased, reflecting the large decline in the prices of cryptocurrencies (Chart 1).

DeFi may hold advantages over traditional finance

DeFi could disrupt traditional financial services. Most financial assets are, in fact, already digitalized, easing the transition to decentralized ledgers.

DeFi protocols are permissionless and, thus, open to anyone. In contrast, most retail customers in the traditional finance sector confront severe limits on the types of products they can access and often require authorization. For instance, even very sophisticated investors in derivatives markets (options and futures, for example) often must have credit arrangements that are mostly unavailable to retail investors.

DeFi protocols can seamlessly and transparently interact with each other and stack transactions, akin to “money Lego.” A few lines of code enable an investor to obtain a loan and deploy the proceeds to purchase digital assets.

In principle, digital assets can be transferred between DeFi protocols, drastically reducing the cost for consumers to switch from one financial service to another, increasing competition and social welfare. By comparison, traditional financial transactions are relatively opaque, and financial institutions are siloed behind closed systems that interact poorly, slowly and expensively with one another.

The decentralized nature of blockchain could limit the presence and market power of large incumbents. There is no “secret sauce” or competitive advantage that can be gained by any one developer because the computer code underlying any DeFi project is publicly available, and the developer will eventually share governance of the application with users.

By comparison, a small number of key players control traditional financial markets, creating large counterparty risk and opportunities to manipulate even large markets, as occurred in the early 2010s when some of world’s largest banks were accused of colluding during the LIBOR (London Interbank Offered Rate) interest-rate-setting scandal.

DeFi applications have been developed to replicate and innovate all types of traditional financial services. The highest levels of user participation occur in lending and borrowing and in decentralized exchanges.

Anonymous borrowing, lending in cryptocurrency

A common protocol for borrowing and lending is Compound finance. Operating similarly to a traditional bank, the Compound protocol links cryptocurrency savers to borrowers. In exchange for providing capital, savers receive interest payments, which accrue in real time (hence, the name compound).

In the world of cryptocurrency, all users are anonymous and there is no credit scoring. Minimization of credit risk is achieved by overcollateralization. Because each lending pool created on Compound is managed via a standalone smart contract, some initial parameters are set in advance—for example, the degree of collateralization—before the contract takes effect.

These decisions are essentially made by the users who receive governance rights every time they provide liquidity to lending pools. Notably, once decided, the parameters of the smart contract cannot be easily modified until the lending pool is liquidated and funds are returned to the original lenders.

Because there is no differentiation, every borrower is the same and pays a common interest rate to the lending pool, which changes continuously to balance out variation in the quality of the collateral and availability of lending pool funds. When most of the funds in the pool are lent, the interest rate increases to incentivize loan repayment.

A certain amount of parametrization—or tractability—is needed, for example, to set the collateralization rate associated with each type of asset that can back a loan. In the long term, users would decide these parameters by exercising governance rights obtained over time. Currently, developers retain most of the governance rights.

Yield farming is a central tenet of DeFi lending and of DeFi applications in general. Providers of capital keep ownership of their assets (the cryptocurrency they post to the lending pool) and can capitalize on possible price changes while earning interest.

Becoming a decentralized exchange market maker

Anyone can be a market maker, also known as a liquidity provider, in a decentralized exchange. To do so, participants must provide digital currency of a prescribed value to a trading pool. For example, traders who want to trade bitcoin for a stablecoin (a digital currency that seeks to maintain a stable exchange rate to a traditional currency such as dollars or euros) can interact with the pool by exchanging some amount of one token for some amount of the other.

As traders exchange bitcoin for the stablecoin, the price of bitcoin moves according to a preset and public algorithmic formula that provides a schedule of implicit prices for any quantity that is traded or added to the pool. This is often called an automated market maker.

Digital exchanges rely on both a liquidity provision to produce efficient pricing mechanisms (the larger the pool, the smaller the price impact of any trade) and on arbitrage activity to realign prices. For example, when the implicit exchange price of bitcoin relative to a dollar-denominated stablecoin becomes too low, arbitrageurs will purchase stablecoin in the open market and use it to buy bitcoin on the exchange. They continue doing so until the implicit bitcoin price in the exchange is the same as the price in the open market.

Digital exchanges’ main innovation is allowing any individual to participate in market making, which has historically been one of traditional financial intermediaries’ largest sources of revenue. Moreover, digital exchanges provide an automatic counterparty in the form of the liquidity pool, thus aiming at eliminating counterparty risk. Because a digital exchange ultimately is a smart contract, it cannot extend credit, settlement is instantaneous and trades can be executed only if all funds are immediately available.

As a new technology, DeFi faces operational tests

Like all emerging technologies, DeFi faces technical and economic challenges. Technically, the ability of protocols to support large-scale adoption is very much in question, not only because of the costs associated with supporting the technology, but also because of its ability to handle large volumes of transactions.

From an economics point of view, large-scale adoption would require a profound philosophical change in the way risk is evaluated. For example, DeFi lending markets are completely anonymous and, as such, do not support credit screening, a service traditional banks provide.

Furthermore, smooth functioning of many DeFi applications requires arbitrageurs to step in and realign prices. However, arbitrage as an economic mechanism may face limitations as availability of capital becomes scarce, especially when markets are under stress.

Another salient issue facing the acceleration of DeFi is inherent in its structure. Most DeFi applications adopt a widespread governance structure in which users and original developers share control of rights to the future of the application. For projects that become relatively large, dispersed governance might become a limiting factor.

How much DeFi protocols can, or are allowed to, integrate with a noncrypto economic landscape will depend on whether, and how efficiently, these types of problems can be solved.

About the Author

Alessio Saretto

Saretto is a senior research economist and advisor in the Research Department at the Federal Reserve Bank of Dallas.

The views expressed are those of the authors and should not be attributed to the Federal Reserve Bank of Dallas or the Federal Reserve System.