Interest rate volatility contributed to higher mortgage rates in 2022

The Federal Reserve aggressively tightened monetary policy in 2022, responding to high and persistent inflation. The resulting borrowing cost increase for households and firms was generally anticipated. However, fixed-rate mortgage interest rates were especially sensitive to the policy regime change.

We find that interest rate volatility and the unique nature of mortgage instruments were important contributors to last year’s outsized mortgage rate moves.

Fed rapidly tightened monetary policy

The Federal Reserve began the current monetary policy cycle at its March 2022 meeting by raising the federal funds rate target by 0.25 percentage points, to 0.25–0.50 percent. As inflation remained persistently elevated, the central bank continued lifting the target at subsequent meetings. The rate stood at 4.25–4.50 percent at year-end.

The Federal Reserve views changes to the federal funds rate’s target range as its primary means of adjusting monetary policy. However, the central bank also started reducing the size of its balance sheet—which includes Treasuries and mortgage-backed securities—in June 2022 by limiting reinvestment of principal payments on its maturing holdings.

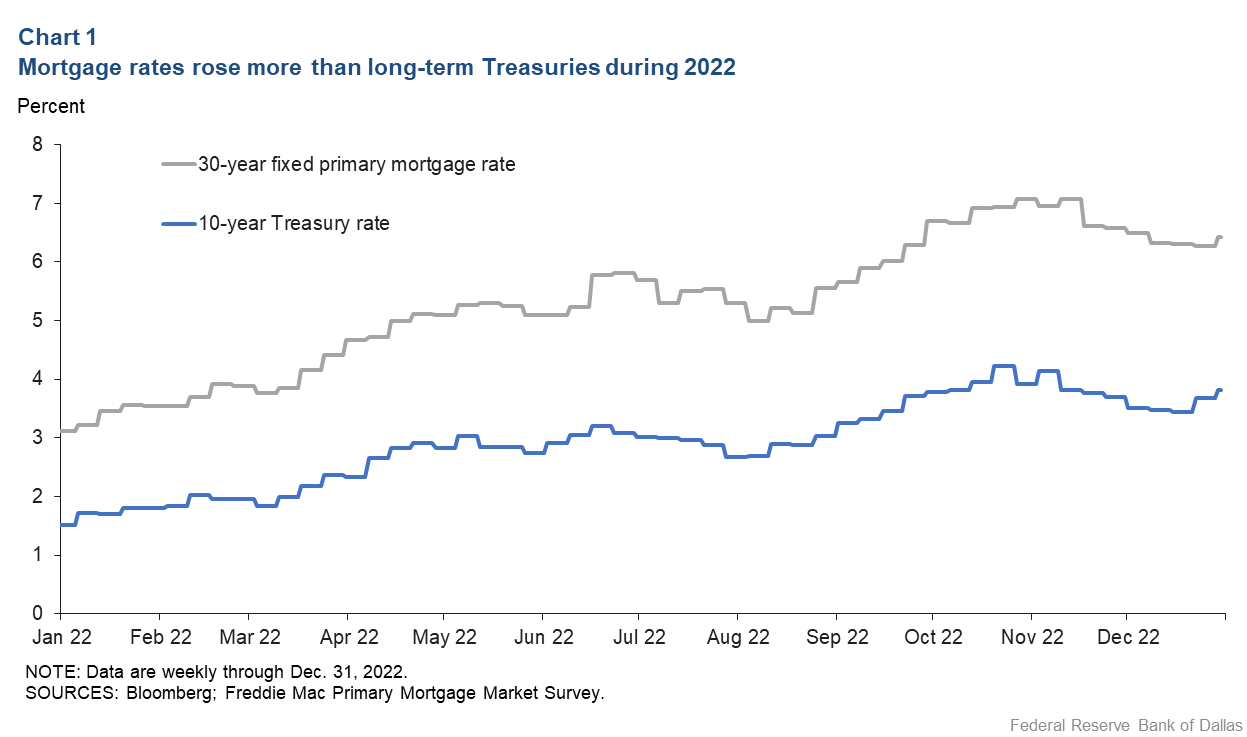

The response of long-term interest rates to this tightening cycle has been less pronounced than the rise in the policy rate. The 10-year Treasury rate started 2022 at about 1.6 percent, peaked at around 4.2 percent in late October, and stood at almost 3.8 percent at year-end. So, while the federal funds rate target went up 375 basis points (3.75 percentage points), the benchmark long-term Treasury rate moved up only 220 basis points.

One might think that home mortgage rates would closely track long-term Treasury rates. That hasn’t been the case (Chart 1).

The average 30-year fixed-rate mortgage began 2022 at 3.1 percent, peaked in late October at 7.1 percent and ended the year at 6.4 percent. While both 10-year Treasuries and mortgages increased over the year, their difference was 60 basis points at the start of the year, widened to as much as 190 basis points in October, and stood at 150 basis points at year-end. What accounts for the significant widening between the two?

Decomposing mortgage interest rates

Mortgage interest rates that households pay to purchase or refinance homes are known as “primary rates.” A commonly cited measure of these interest rates comes from Freddie Mac’s Primary Mortgage Market Survey, the data source for Chart 1. This weekly report provides the average interest rates for first-lien conventional, conforming fixed-rate mortgages with a loan-to-value of 80 percent. Conventional conforming mortgages are those eligible for securitization—or resale to investors—through Freddie Mac and Fannie Mae. These two government-sponsored enterprises (GSEs) accounted for almost 60 percent of new mortgages during 2022.

The basis for primary rates is the secondary-market interest rates paid to investors holding uniform mortgage-backed securities (UMBS) guaranteed by Fannie Mae or Freddie Mac. UMBS are created and traded with coupons (interest payments to investors) in 50-basis-point increments. The secondary rate consistent with a UMBS at par value (typically, face value) is known as the “current coupon” rate.

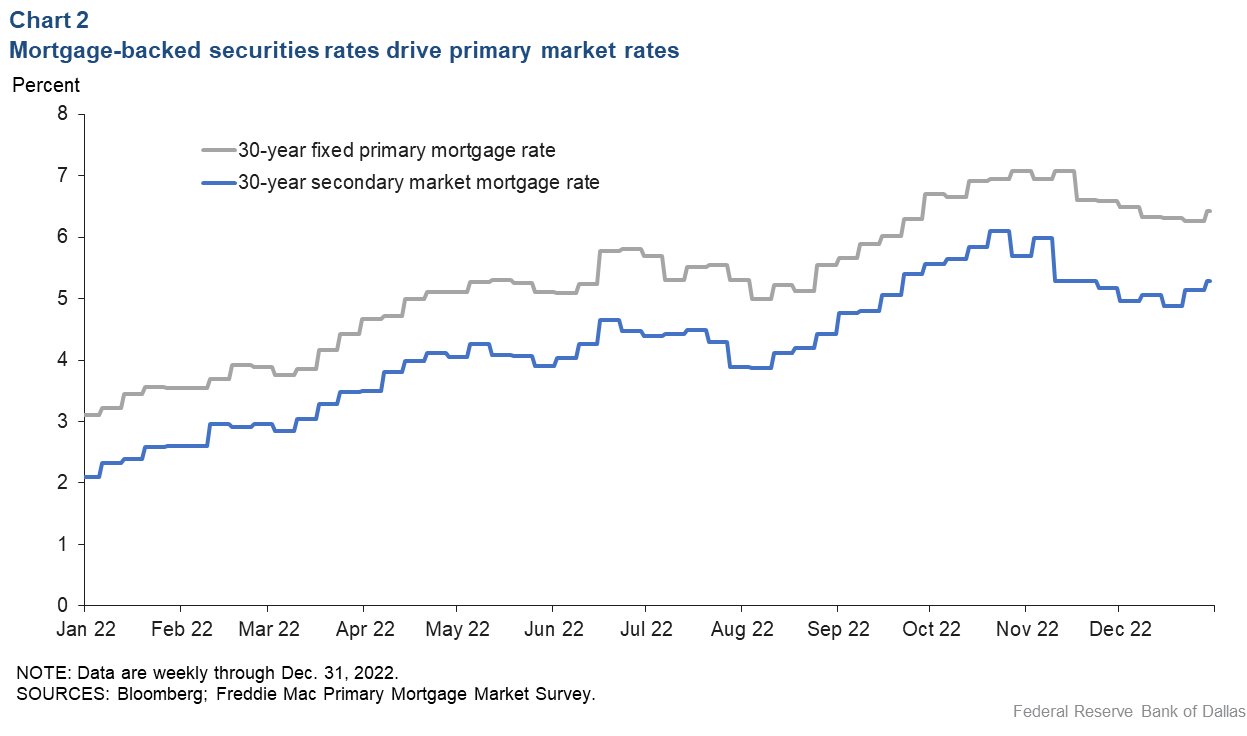

Chart 2 displays the primary-mortgage-market rate (what homeowners pay) and the secondary-market rate (paid to UMBS investors) during 2022. The difference between the two series—or the “primary–secondary spread”— reflects several factors.

First, all conventional conforming mortgage borrowers pay 25 basis points for loan servicing. Second, Fannie Mae and Freddie Mac charge guarantee fees to ensure timely payment of principal and interest on UMBS. Finally, loan originators need to cover their costs, including a return on equity, which may vary over time due to mortgage demand. The primary–secondary spread, which averaged around 105 basis points during 2022, did not exhibit a trend that could account for the widening relative to long-term Treasury rates during the period.

Chart 2 illustrates that the large increase in primary mortgage rates during 2022 was driven by secondary-market rates. Conceptually, one can think of secondary-market rates as reflecting the sum of a long-term risk-free rate (for convenience, we show the 10-year Treasury rate) plus the cost of a call option that allows borrowers to prepay their mortgages at any time without penalty.

This continuous prepayment option is costly to lenders because it is exercised more often when it benefits the borrower at the expense of the lender, as borrowers refinance into lower-rate loans. The difference between the secondary-market rate and longer-dated Treasury rates can be thought of as the cost of the prepayment option.

Interest rate volatility widens mortgage spreads

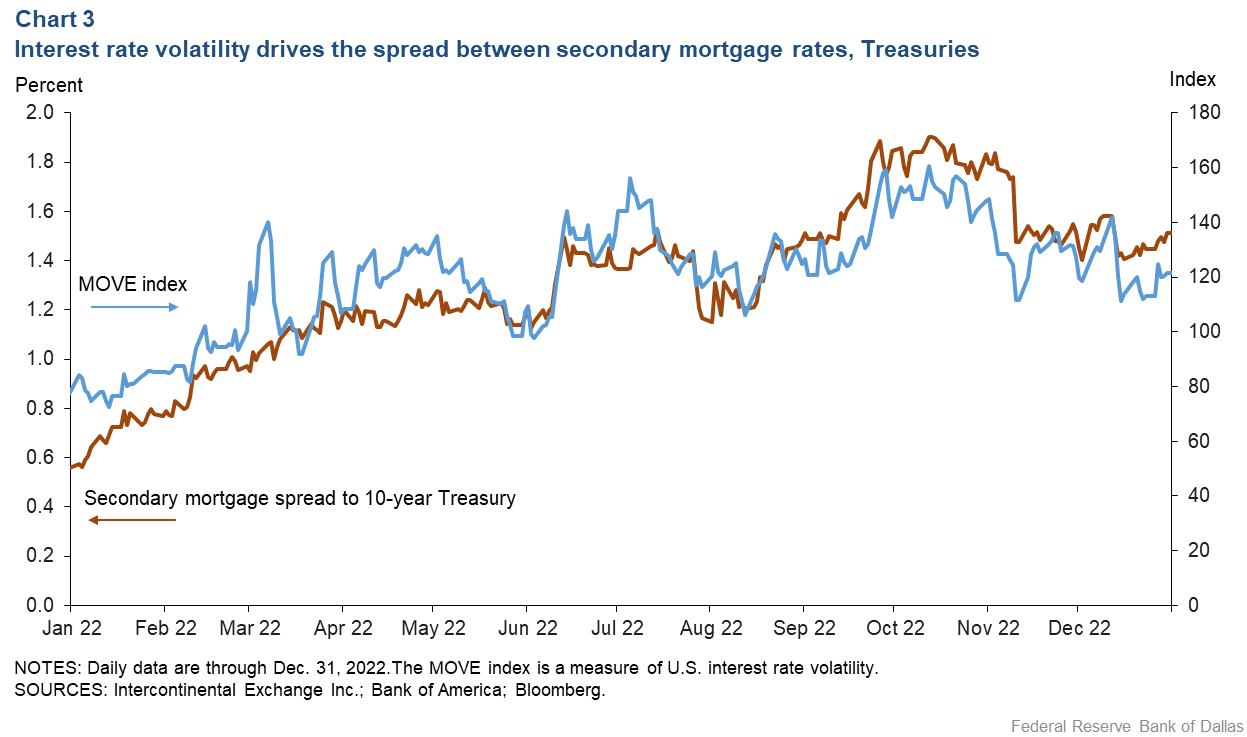

Option values increase with the volatility of the underlying asset value. This is because greater volatility increases the likelihood that the asset’s price will reach a level that renders the option valuable. In this case, mortgage prepayment options rose in value because of increased underlying interest rate volatility.

Chart 3 plots the difference between the secondary-mortgage-market rate less the 10-year Treasury rate against a widely cited measure of interest rate volatility— the MOVE index. The MOVE index tracks the level of Treasury rate volatility over one month that is implied by options on Treasury securities. Such option-implied rate volatility can be thought of as reflecting uncertainty about the future path of underlying interest rates.

Increased uncertainty about the future path of Treasury rates over much of 2022 translated into increased values of the mortgage prepayment option, boosting the spread between mortgage-backed securities and long-dated Treasuries. As markets became more confident about the future path of interest rates at year-end 2022, option-implied Treasury volatility fell, and the spread between mortgage-backed securities and Treasuries followed.

The role of interest rate uncertainty

While the increase in mortgage rates during 2022 was primarily driven by the rise in risk-free Treasury rates, it was amplified by increases in the cost of the mortgage prepayment option, which reflected broader uncertainty about the future path of interest rates.

About the authors

W. Scott Frame is a vice president in the banking and finance group in the Research Department at the Federal Reserve Bank of Dallas.

Matthew McCormick is a senior financial sector advisor in the Research Department at the Federal Reserve Bank of Dallas.

The views expressed are those of the authors and should not be attributed to the Federal Reserve Bank of Dallas or the Federal Reserve System.