Houston Economic Indicators

Houston business-cycle and leading indexes pointed to a growing economy in May. Employment, particularly mining-related jobs, accelerated, but the U.S. rig count and oil prices have fallen in recent months. Manufacturers reported negative impacts from tariffs, while measures of global manufacturing showed signs of slowing—including for Houston trade partners. Taken together, the outlook for the region remains positive.

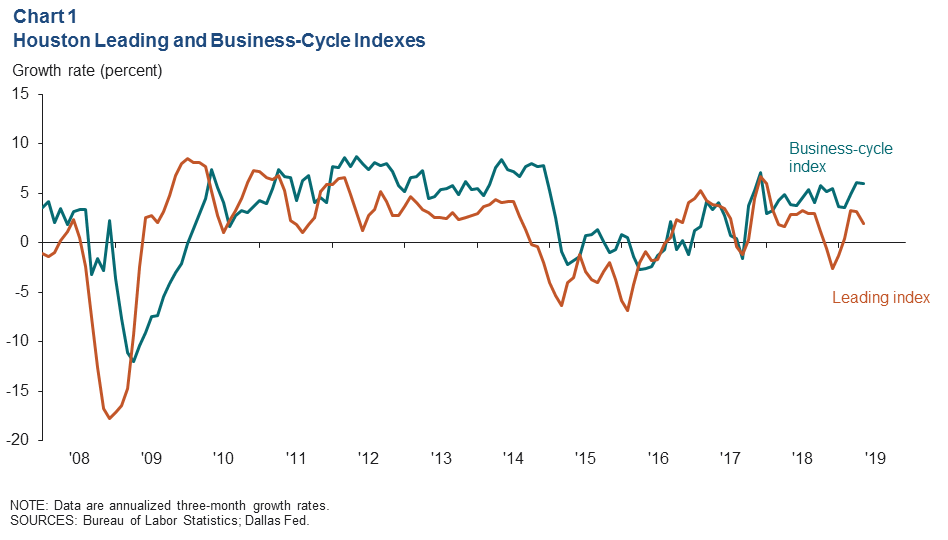

Business-Cycle Index

The Houston Business-Cycle Index grew 6.0 percent over the three months ending in May, owing to strong—but thus far unbenchmarked—employment data (Chart 1). This suggests that the region’s economy has been expanding at a healthy pace in 2019 and that the region accelerated from the nearly 4.8 percent growth rate in second half 2018.

An index of leading indicators for Houston employment growth slowed to a rate of nearly 2.0 percent for the three months ending in May. This implies positive but modestly slower employment growth ahead, particularly over the next three to 10 months.

Employment

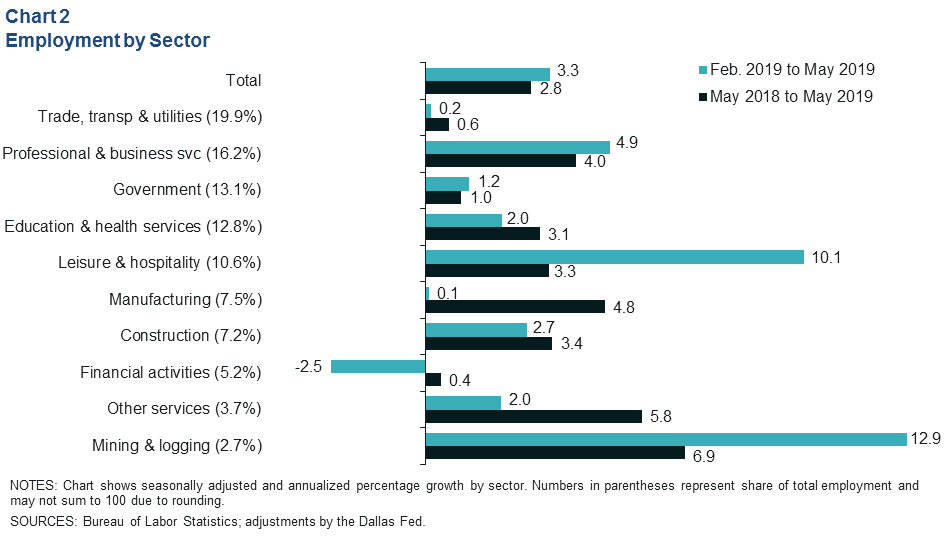

The number of jobs in the Houston Economy grew 3.3 percent (about 25,800 jobs) from February to May, up from 2.0 percent growth for the three months ending in February (Chart 2). While the mining sector logged the fastest growth rate, leisure and hospitality added the most jobs (7,900). Most of the remaining gains came from professional and business services (6,100; mostly from professional, scientific and technical jobs). The only industry to contract was financial activities (-1,100).

The May Houston unemployment rate held steady at April’s record low of 3.5 percent. Texas overall also had an unemployment rate of 3.5 percent in May, while the U.S. rate was 3.6 percent.

Energy

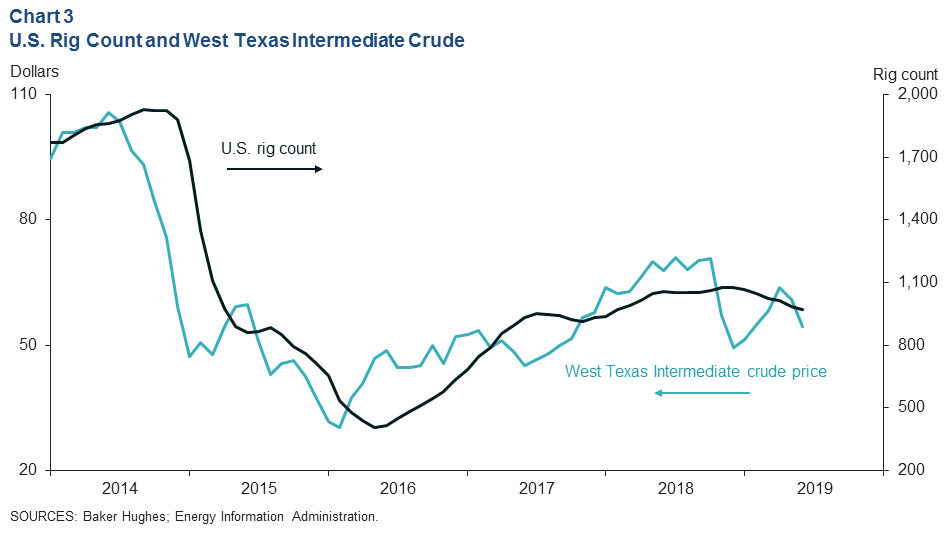

Drilling Extends Decline as Oil Prices Slip

The U.S. rig count slipped to an average of nearly 970 rigs in June, a drop of 108 rigs from the three-year high of 1,077 in December (Chart 3). Fluctuations in monthly drilling activity tend to follow changes in monthly oil prices with a lag of about three months. However, efforts to rein in capital spending, ongoing improvements in efficiency and productivity, and expectations for a significant expansion of pipeline capacity in the second half of 2019 are likely contributing to the recent erosion of the rig count.

West Texas Intermediate (WTI) crude oil slipped nearly $10 per barrel from April to June as signs of rising inventories and concerns about the pace of global demand growth weighed on the price. At $54.47 per barrel in June, WTI was still above the average price needed to drill a new well, particularly in the Permian Basin. However, some producers reported needing higher prices to drill profitably and may be slow to expand their drilling schedules should crude prices linger at these lower levels.

Mining Jobs Accelerate

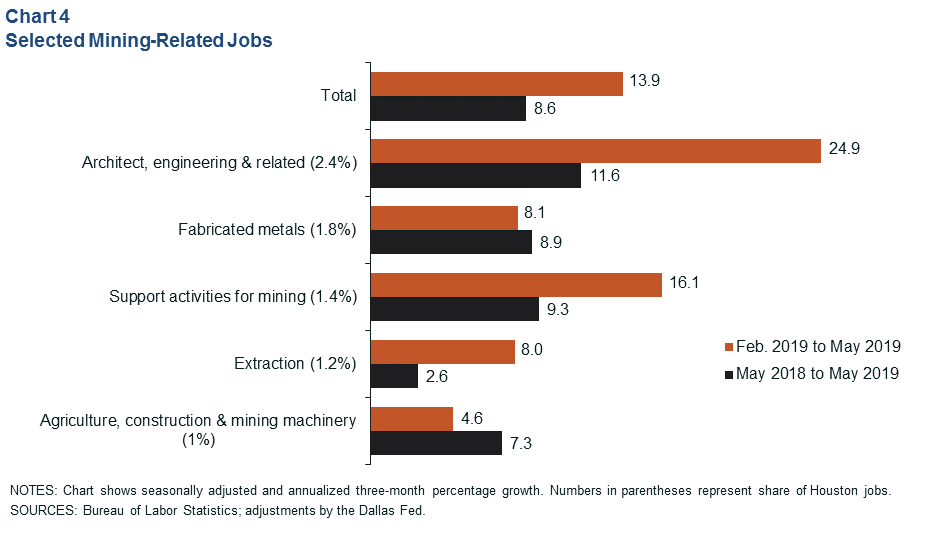

The malaise in drilling activity has not slowed the growth rate of mining-related employment in Houston. Looking at mining-specific jobs, support activities for mining (1,600 jobs; mostly oilfield services companies) and extraction (700; mostly exploration and production firms) accelerated in recent months (Chart 4).

Sectors that are not mining-specific but tend to fluctuate in tandem with the energy industry were mixed. Architecture, engineering and related services (4,100) added more jobs than any other mining-related sector, accelerating markedly in the recent data. However, this may also be attributed in part to improvements in segments like the engineering procurement and construction industry.

Conversely, manufacturing jobs slowed moderately the past three months when compared with year-over-year growth. Both fabricated metals (1,100), and agriculture, construction and mining machinery (400) are connected to the mining supply chain. In fact, across respondents to the April Dallas Fed Manufacturing Survey, 20.1 percent of Texas manufacturing firms reported receiving more than 10 percent of revenues directly from the oil and gas industry (probably more so in Houston given the metro’s industry mix). However, Houston manufacturers are facing other headwinds.

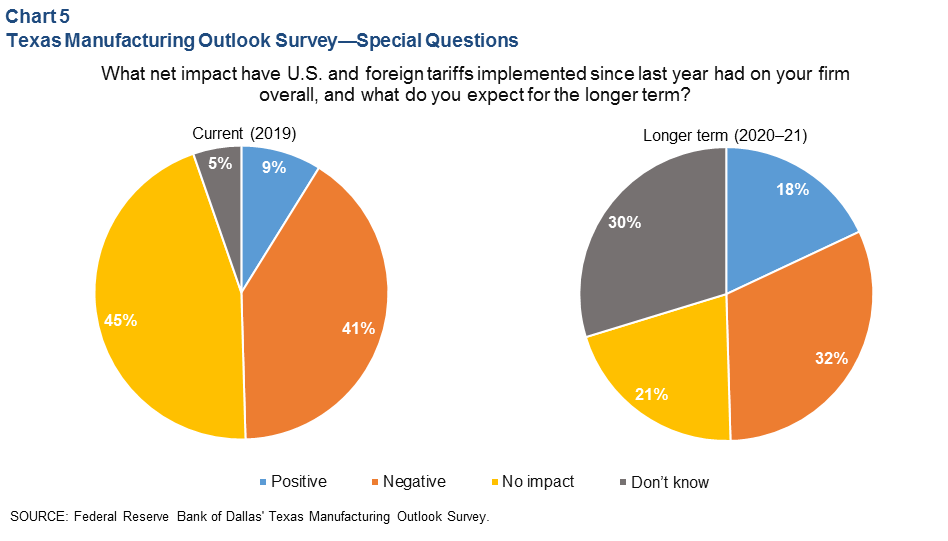

Tariffs Impact Texas Manufacturing

Responses to the June 2019 Dallas Fed Manufacturing Survey special questions indicated that 41 percent of Texas manufacturing firms were negatively impacted by tariffs over the past year (Chart 5); 62 percent said tariffs will have either a negative or uncertain impact on their business over the next two calendar years. In 2018, Texas manufacturers surveyed earned 11 percent of their revenues from customers outside the U.S.

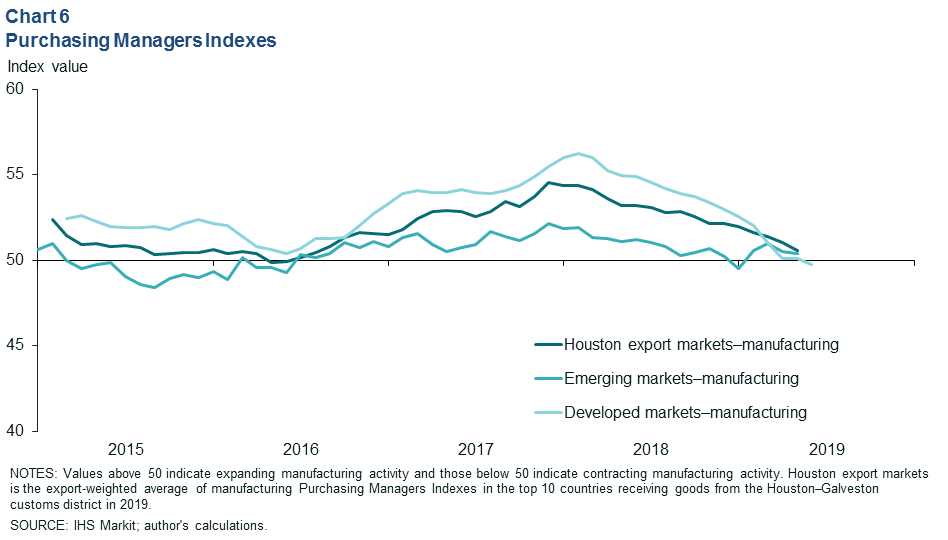

International Purchasing Managers Indexes

Purchasing Managers Indexes (PMI) are useful barometers of growth in manufacturing output around the world. Aggregate PMIs for emerging and developed markets fell to readings just above 50 in April and May 2019, indicating nearly flat manufacturing output (Chart 6). Readings below 50 suggest a contraction in manufacturing output, and early data for developed markets in June 2019 show manufacturing just below neutral at 49.7.

To put this in a local context, manufacturing PMIs have also eroded for the Houston–Galveston customs district’s top 10 export destinations, which accounted for 53 percent of the value of district exports year to date in 2019. A weighted average of these nations’ indexes fell to 50.6, their lowest combined reading since August 2016. Many of the products exported through local ports are intermediate goods—distillate fuels, plastic resins and machinery—that are shipped abroad for further processing.

NOTE: Data may not match previously published numbers due to revisions.

About Houston Economic Indicators

Questions can be addressed to Jesse Thompson at jesse.thompson@dal.frb.org. Houston Economic Indicators is posted on the second Monday after monthly Houston-area employment data are released.