Big federal stimulus, home-value spike won’t ease next slump

In March 2020, the Texas and U.S. economies entered a short but deep recession from which it would take over two years to recover. Payroll employment fell at a historically unprecedented pace in second quarter 2020, throwing millions of people out of work. Many businesses shut down or curtailed operations, all to slow the spread of COVID-19.

The abrupt action prompted a short but very abrupt recession with a historically low number of available jobs. The downturn affected everyone, especially women and people of color.

A historic wave of mostly federal fiscal support, largely deficit-financed, subsequently aided individuals, schools, businesses, and state and local governments. The federal assistance propelled the national debt to new heights. Surging property taxes from rising home prices helped boost property tax revenue, providing a secondary lifeline.

Now, as the country contemplates the possibility of another economic downturn, this recent experience raises a question: To what extent are local, state and national governments well-prepared over the near term to provide economic support? Financial backstops employed during the pandemic—the product of borrowed money and rapidly increasing home valuations—may not be as readily accessible.

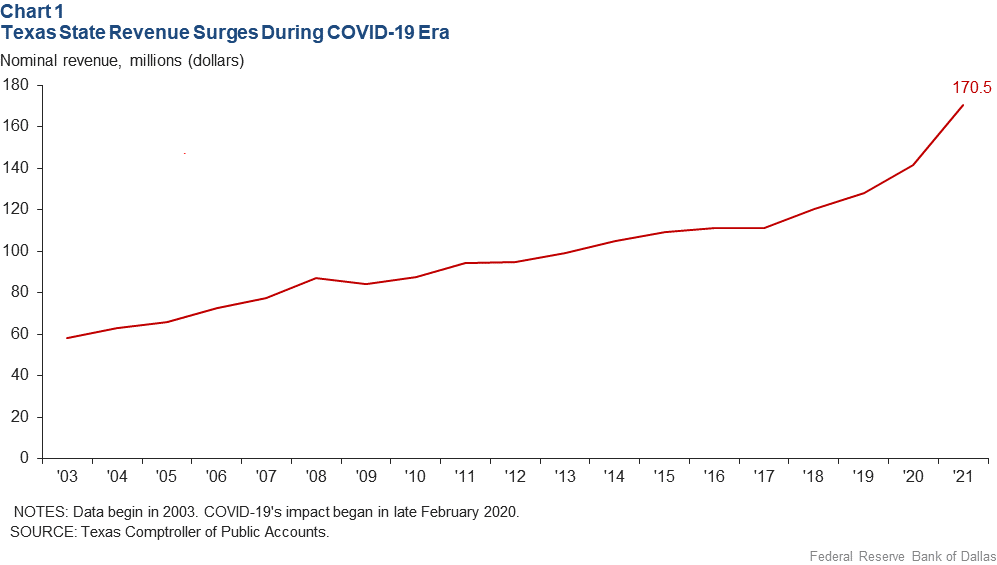

Rising Texas Revenue

Typically, state government revenues fall during recessions. In the pandemic recession, however, Texas revenue rose. State revenue growth actually accelerated from 6.5 percent in 2019 to 10.6 percent in 2020, despite COVID-19 dramatically contracting economic activity. Revenue grew by an even larger 20.4 percent in fiscal 2021, covering the 12 months ended Aug. 31, 2021 (Chart 1).

The 2020–21 nominal revenue growth of $42.5 billion almost equaled the $43.7 billion by which revenue grew in the preceding 10 years, even though those earlier years were COVID-free, and the Texas economy was routinely described as “robust” during that time.

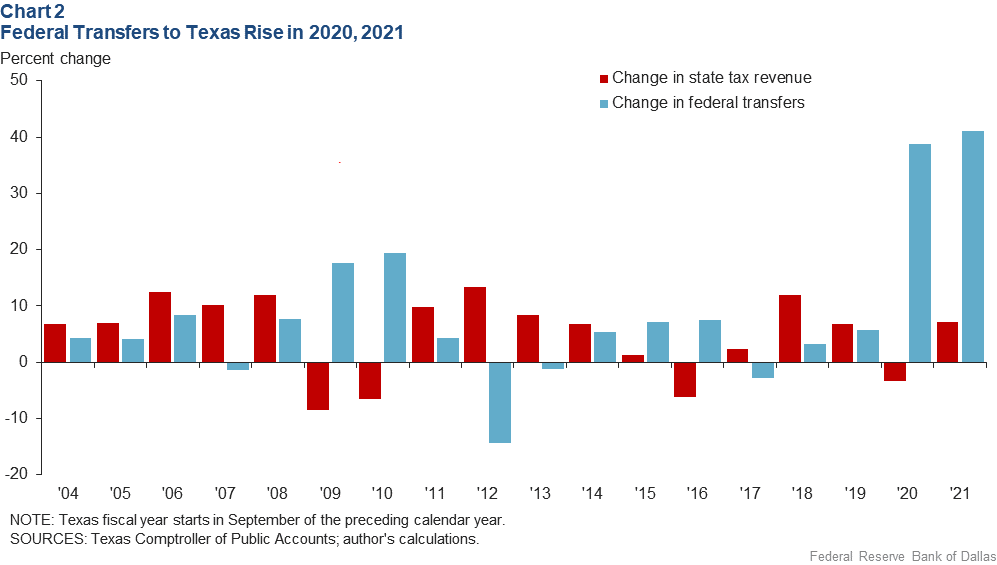

Federal transfers propelled the Texas revenue rise. While state tax revenue actually fell 3 percent ($2.0 billion) from fiscal 2019 to fiscal 2020, the federal contribution to Texas revenue rose by an unprecedented 38.6 percent ($16.2 billion) to more than make up the difference (Chart 2).[1] Then in fiscal 2021, federal transfers jumped an additional 40.9 percent ($23.8 billion), while state tax revenue increased by a more modest 7.1 percent ($4.1 billion).

In each of those two fiscal years, federal transfers supplanted state taxes to become the primary funding source for Texas.

To understand how unusual this is, it’s instructive to look at federal transfers as a share of Texas revenue over time. Historically, just less than half of Texas revenue comes from taxes (such as the sales tax), while one-third comes from federal transfers, much of which is earmarked for efforts such as the Medicaid low-income health coverage program that is administered at the state level but funded jointly by states and the federal government.

But as the severity of COVID-19 became clear, the federal government launched an unprecedented array of stimulus measures designed in part to bolster the fiscal capacity of state and local governments. These programs are largely responsible for the federal transfer surge.

Home-Price Impact

Real estate valuations provided additional support to Texas government efforts to weather the pandemic-era fiscal storm. In contrast to the state government, which is constitutionally prohibited from assessing a statewide property tax on Texas residents, local jurisdictions’ assessment and collection of property tax fund their operations.

School districts are perhaps the most prominent, spending this revenue on public schools and educating students. But numerous other public entities also receive and spend property tax revenue—including hospital districts, community college districts, emergency-response districts and water districts—without which, local residents would potentially lose access to vital public services.

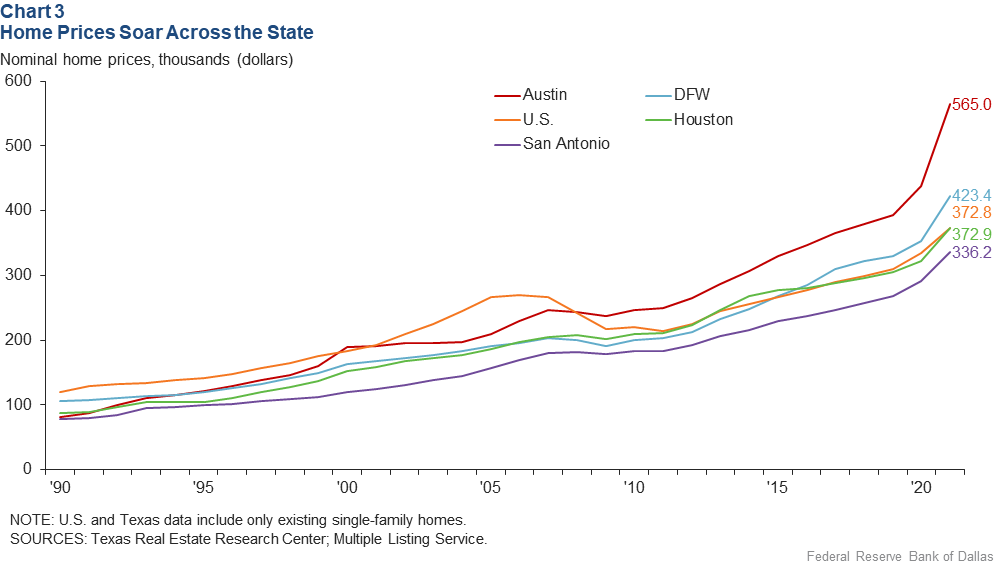

During the national 2002–07 housing boom, Texas home prices remained relatively flat as national prices soared and then retrenched.[2] Historically, Texas home values have escaped most—though not all—boom-and-bust cycles, limiting the extent to which city and county government coffers are subject to property tax volatility.

But in a break from prior patterns, Texas home prices fully participated in the 2012–21 national boom. And because Texas levies are set as a percentage of home valuations, local jurisdictions have shared the gains in the form of higher property tax revenue. Exact figures are unavailable, but data from the state comptroller’s office indicate local property tax revenue rose roughly 20 percent between 2017 and 2021.[3]

While home prices didn’t rise at the same pace in every jurisdiction, a look at the state’s largest metro areas illustrates just how rapidly they accelerated in recent years (Chart 3).[4]

Between 2000 and 2011, the average price of single-family homes rose at an annual rate of 2 percent in Dallas–Fort Worth, 3 percent in Houston, 4 percent in San Antonio and 2.6 percent in Austin. Over the next eight years, those rates roughly doubled to 6.3 percent in DFW, 4.7 percent in Houston, 4.8 percent in San Antonio and 5.8 percent in Austin.

Single-family home prices spiked in 2020–21, rising at annual rates of 13.3 percent in DFW, 10.6 percent in Houston, 12.0 percent in San Antonio and 19.9 percent in Austin.

How and why home prices appreciate is complicated. Many economic factors contribute, making it difficult to compare one period with another and draw inferences about what is likely to happen today. And there are many factors, from a strong business climate to plentiful domestic and international migration, that likely prop up home demand in Texas more than in the U.S. as a whole.

However, the economic literature on housing markets is very clear that, barring a dramatic increase in supply, home-price appreciation slows when interest rates rise.[5] And we are in such an environment today, with the Fed raising rates five times through September 2022 and Chairman Jerome Powell pledging at the Jackson Hole meeting in August to apply monetary policy as “forcefully” as is needed to lower inflation even if doing so “bring[s] some pain to households and businesses.”

Revenue Outlook

If historically anomalous home-price appreciation is unlikely to continue, what about historically anomalous federal transfers to states and localities? The fiscal stimulus programs designed to combat the economic impact of COVID-19 were always designed to be targeted, timely and temporary, just as similar but smaller programs during the Great Recession had been.[6]

Most pandemic relief measures that elevated federal transfers to Texas in 2020 and 2021 have ended. It’s unlikely they will be resurrected in subsequent years—at least not without a substantial reassessment of how large government should be during normal economic times.

The funding of those federal transfers also poses future challenges. Orthodox public finance suggests accumulating government surpluses during expansions, which can then be used to fund above-normal levels of government services during recessions without accumulating debt. But during the eight-year expansion leading up to COVID-19, the federal government did not run a surplus in any of those years and actually accumulated real debt at a historically rapid peacetime pace.

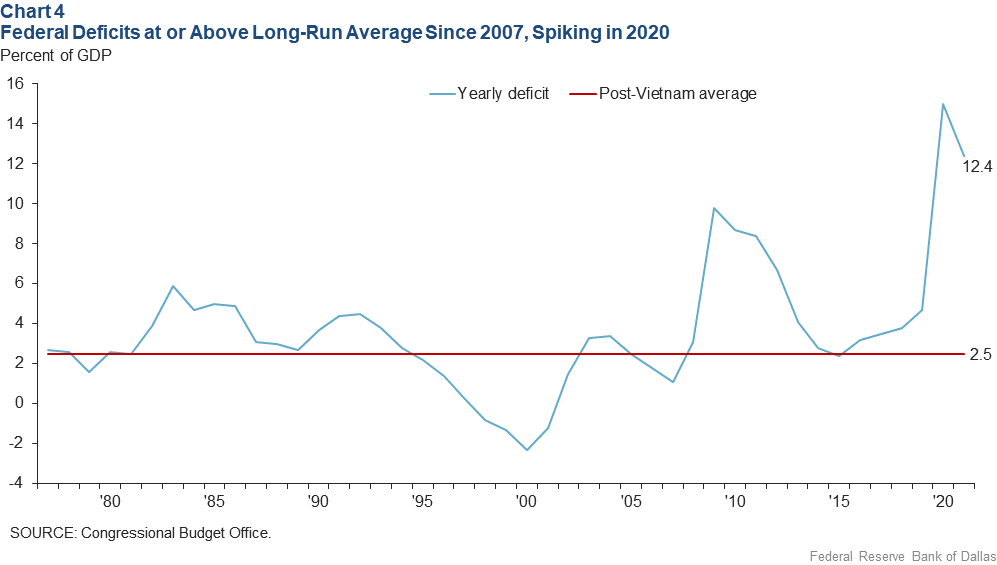

From the end of the Vietnam War in the mid-1970s to the Great Recession (December 2007–June 2009), the federal government incurred average deficits equal to 2.5 percent of GDP (Chart 4).

It is not surprising that deficits during the Great Recession and its immediate aftermath would exceed this level, and they did, at an average of 8.4 percent of GDP from 2009 to 2012. But during the expansion years of 2013–19, they remained somewhat above the long-run average rather than falling below it. Deficits again soared during the COVID-19-era to breach the peacetime record previously set during the Great Recession.

To understand the future path of fiscal policy, it’s important to remember that the nation’s annual deficits must be serviced by interest payments. While debt incurred since the Great Recession was financed at historically low interest rates, current and future deficits likely won’t be.

The Congressional Budget Office (CBO) expects the average interest rate for federal debt to rise from 1.8 percent today to 3.1 percent in 2032 and 5.2 percent in 2052. Coupled with an expectation that future federal deficits will remain above their historic average of 2.5 percent of GDP in perpetuity, the CBO projects that federal interest payments as a share of GDP will more than quadruple over the next three decades, rising from 1.6 percent today to 7.2 percent in 2052.[7]

Economic research indicates that government’s “fiscal space”—the capacity to respond to recession through fiscal stimulus as occurred during the COVID-19 outbreak—is lower when a substantial portion of tax revenue is committed to servicing previously accumulated debt.[8] Even without the recent run-up in federal debt, historically large fiscal stimulus from the federal government to states and localities was destined to decline going forward.

Economic theory also suggests the reduction in fiscal space caused by the nation’s large and growing federal debt could at the margin reduce the magnitude of stimulus during future recessions. That, in turn, could mean resources will be harder to come by when recessions occur for both state and local governments and the underserved individuals who will most need assistance.

Over the last few years, the fiscal capacity of state and local governments in Texas has been bolstered by federal transfers, whose impact on the federal budget was lessened by historically low interest rates that also supported rapid home-price appreciation.

As those unusual circumstances run their course, Texas would be expected to return to a more traditional fiscal setup in which state tax revenues are again the primary driver of state spending and where local governments no longer experience double-digit yearly increases in their property tax bases.

Throttling Down Spending

Though there are reasons to believe above-normal spending growth at the state and local level won’t persist over the longer term, it’s worth noting that Texas job growth consistently exceeded the national average by about a percentage point before the onset of COVID-19.

The fundamental factors that supported Texas’ relatively rapid growth—a favorable business climate, readily available housing, and higher-than-average domestic and international migration—haven’t changed.[9]Yet longer-term challenges remain in the areas of education, health and infrastructure that will help determine how quickly the state economy grows in the future and the extent to which all Texans can fully participate in the prosperity that growth brings.[10], [11], [12] More broadly, the state’s ability to navigate these challenges may well determine how nimbly Texas can emerge from the next economic downturn.

Notes

- “COVID-19’s Fiscal Ills: Busted Texas Budgets, Critical Local Choices,” by Jason Saving, Federal Reserve Bank of Dallas Southwest Economy, Third Quarter, 2020.

- “Texas Property Taxes Soar as Homeowners Confront Rising Values,” by Jason Saving, Federal Reserve Bank of Dallas Southwest Economy, Third Quarter, 2018.

- “As Texas Home Values Skyrocket, State Officials Wrestle with How to Slow Property Tax Increases,” by Joshua Fechter, Texas Tribune, April 22, 2022, accessed Sept. 2, 2022.

- “Around the Region: Texas Home Prices Rose at Record Pace in 2021,” by Luis Torres, Federal Reserve Bank of Dallas Southwest Economy, Second Quarter, 2022.

- For more on how housing market turbulence can be monitored, see “Real-Time Market Monitoring Finds Signs of U.S. Housing Bubble,” by Jarod Coulter, Valerie Grossman, Enrique Martinez-Garcia, Peter C.B. Phillips and Shuping Shi, Federal Reserve Bank of Dallas Dallas Fed Economics, March 29, 2022.

- “Can the Nation Stimulate Its Way to Prosperity?” by Jason Saving, Federal Reserve Bank of Dallas Economic Letter, vol. 5, no. 8, August 2010, accessed Sept. 2, 2022.

- This is the assumption made by the Congressional Budget Office in creating its long-run forecasts. Were fiscal policymakers to opt for lower deficits, the long-run fiscal outlook would become more favorable.

- “U.S. Budget Deficits Shrink but Longer-Run Issues Remain,” by Jason Saving, Federal Reserve Bank of Dallas Economic Letter, vol. 9, no. 3, March 2014, accessed Sept. 2, 2022.

- “Keys to Economic Growth: What Drives Texas?” by Jason Saving, Federal Reserve Bank of Dallas Southwest Economy, First Quarter 2009.

- “Texas K-12 Education Spending Set to Rise, but Who Will Pay?” by Jason Saving, Federal Reserve Bank of Dallas Southwest Economy, Third Quarter 2019.

- “Texas Health Coverage Lags as Medicaid Expands in U.S.,” by Jason Saving and Sarah Greer, Federal Reserve Bank of Dallas Southwest Economy, Fourth Quarter, 2015.

- “Budget Balancing Act: Health and Education Stretch Texas Resources,” by Jason Saving, Federal Reserve Bank of Dallas Southwest Economy, Third Quarter, 2014.

About the Author

Jason Saving

Saving is a senior business economist at the Federal Reserve Bank of Dallas.

Southwest Economy is published quarterly by the Federal Reserve Bank of Dallas. The views expressed are those of the authors and should not be attributed to the Federal Reserve Bank of Dallas or the Federal Reserve System.

Articles may be reprinted on the condition that the source is credited to the Federal Reserve Bank of Dallas.

Full publication is available online: www.dallasfed.org/research/swe/2022/swe2203.