Nominal GDP outlook suggests it’s time to end monetary accommodation

Although U.S. output and employment remain below their pre-COVID-19 trends, inflation is sharply higher. Even inflation gauges that exclude extreme individual price movements often attributed to special factors are exceeding the Federal Open Market Committee’s (FOMC’s) long-run target of 2 percent.

This combination suggests that a supply shortfall is constraining the recoveries of output and employment. Supply shortfalls depress real activity while boosting inflation. Demand shortfalls, in contrast, lower both real activity and inflation. We see evidence of a supply shortfall in tight labor markets and stressed supply chains, which make it harder for businesses to keep pace with shifts in the composition of demand.

We discuss how monetary policy should respond to shortfalls in demand and supply and how a broad measure of liquidity—nominal gross domestic product (NGDP)—can help guide monetary policy. We argue that the policy response to COVID-19 has been broadly on track to date but that continued monetary accommodation (low interest rates and an expanding Fed balance sheet) risks fueling excessive inflation.

Responding to demand shortfalls

There is wide agreement that the Federal Reserve should respond to demand shortfalls by providing accommodation. Easy monetary policy works to counteract declining demand, helping to maintain full employment and price stability.

The only real disagreements are on implementation: How aggressive should the policy response be, and how rapidly should accommodation be withdrawn? The Federal Reserve’s new monetary policy strategy, announced in August 2020, is designed to guard against a premature withdrawal of accommodation.

Responding to supply shortfalls

The appropriate policy response to a supply shortfall is not so clear-cut. Efforts to stabilize real activity will add to already-elevated inflation pressures, while efforts to stabilize inflation will further depress activity. The FOMC has promised to weigh “inflation pressures” against “employment shortfalls” in such a scenario, but it has offered no explicit guidance on how it will weigh them.

Targeting nominal income

The Federal Reserve Act calls on the FOMC to maintain long-run growth in dollar liquidity “commensurate with the economy’s long-run potential to increase production, so as to promote the goals of maximum employment, stable prices and moderate long-term interest rates.”

One very broad measure of liquidity is the dollar value of the goods and services produced in the U.S. economy—nominal gross domestic product. NGDP also measures the dollar incomes generated by U.S. economic activity. Consistent with the Federal Reserve Act, the FOMC could prespecify a target NGDP path it believes sufficient to support full employment and price stability over time and then adjust its policy tools to keep NGDP near that target.

Sensibly, NGDP targeting requires that the FOMC try to cancel out negative demand shocks, which put downward pressure on both real activity and inflation and threaten to push NGDP below its target path.

Negative supply shocks lower output relative to trend, raise prices relative to trend or both. An NGDP-targeting central bank will aim for an inflation overshoot proportional to the output shortfall, allowing variation in inflation that helps stabilize nominal incomes.

Stable nominal incomes enhance financial stability in an economy where households, businesses and state and local governments have fixed nominal obligations, such as mortgage, auto loan, lease and employee pension payments.

A credible NGDP target would also anchor inflation expectations at the horizon over which output is expected to converge to potential.

Because it focuses on a single indicator, NGDP targeting would enhance the Fed’s accountability and transparency. It would also reduce policy uncertainty, especially in the face of supply shocks.

To demonstrate how NGDP targeting might be used to guide and evaluate monetary policy, we consider two historical episodes: the global financial crisis (GFC) and the ongoing COVID-19 pandemic.

Nominal GDP after the global financial crisis

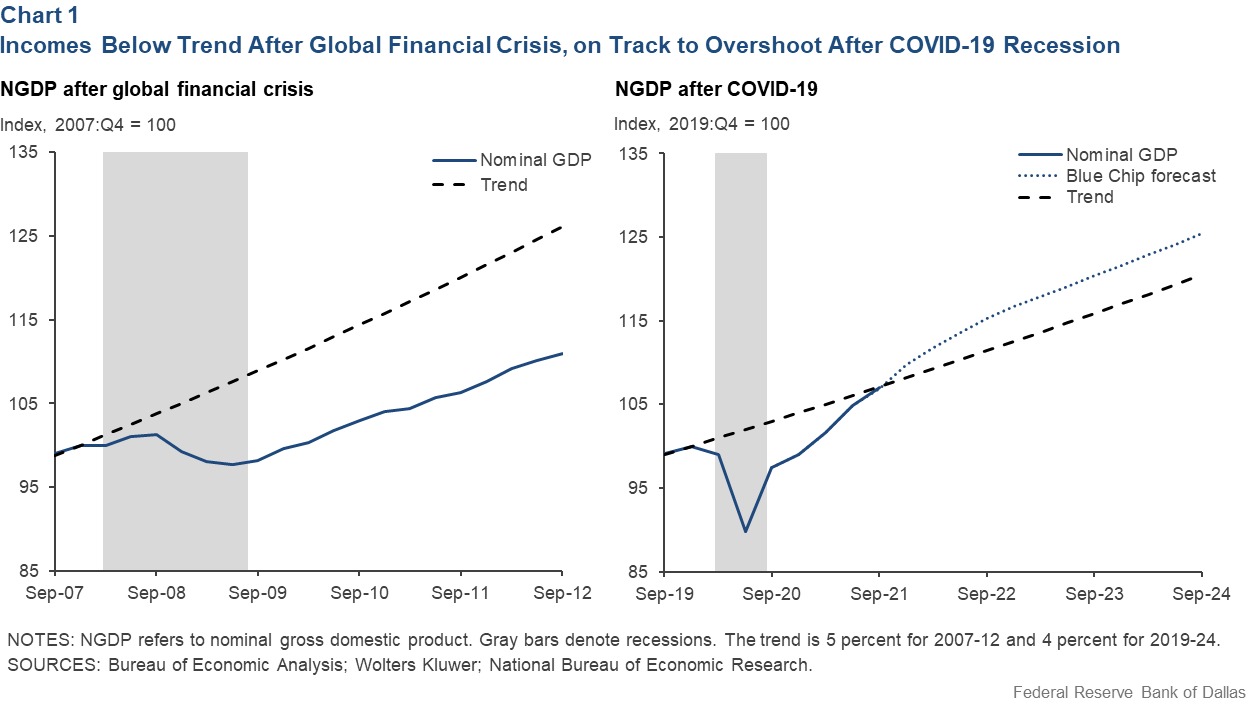

Just before the 2008–09 GFC, Blue Chip forecasters estimated the U.S. economy’s long-run real (inflation-adjusted) GDP growth at 2.9 percent and believed that the Federal Reserve would be content for inflation to average 2.1 percent.

The economy was thought to be at full employment. So, a 2.9 percent + 2.1 percent = 5.0 percent NGDP growth target would have supported the Federal Reserve’s dual mandate. Indeed, analysts forecasted 5.0 percent NGDP growth over the coming years, and economic decision-makers presumably made financial commitments accordingly.

Over the five years from fourth quarter 2007 through fourth quarter 2012, annual NGDP growth averaged just 2.2 percent, causing NGDP to fall well below the 5.0 percent growth path analysts expected (Chart 1, left panel).

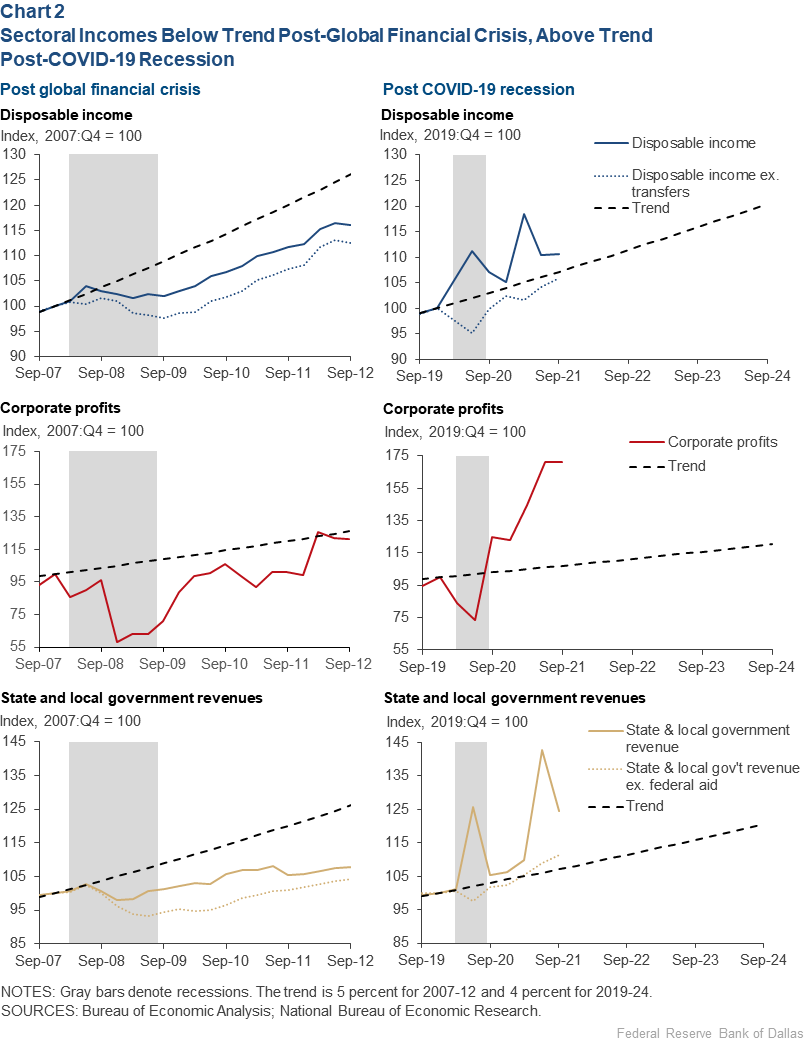

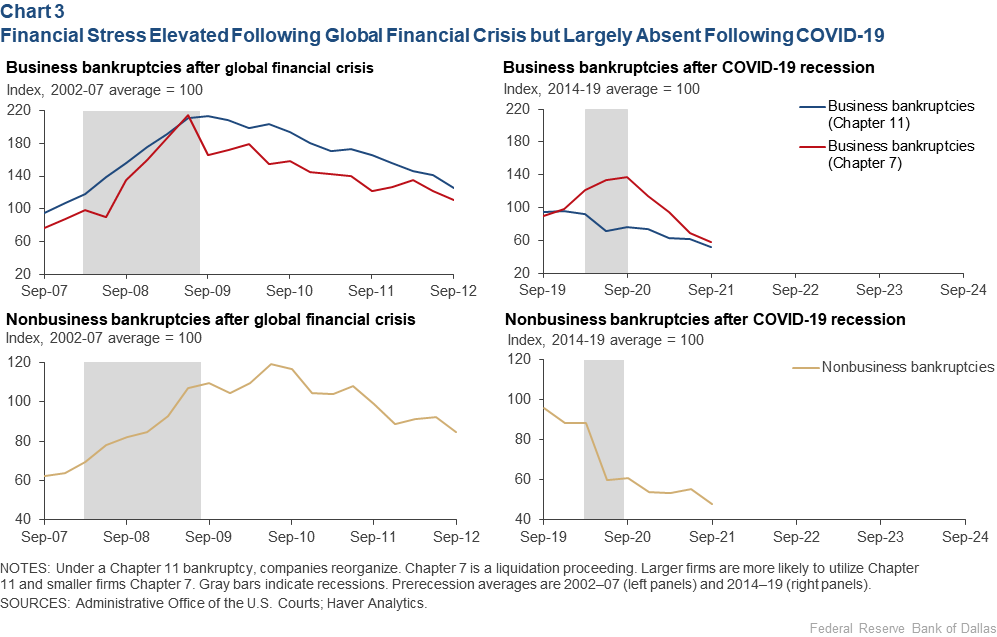

The NGDP shortfall was reflected in below-trend growth in household and corporate incomes and in state and local government revenues (Chart 2, left panels). The resultant financial stress—illustrated in the left-side panels of Chart 3—likely contributed to a slow recovery in output and employment.

Nominal GDP after COVID-19

In 2019, forecasters estimated the U.S. economy’s real growth potential at 2.0 percent, and the Federal Reserve reaffirmed a 2.0 percent inflation objective. The economy was likely near full employment. Thus, an appropriate target rate of NGDP growth would have been 4.0 percent (2.0 percent real potential growth + 2.0 percent target inflation). Private analysts were, in fact, expecting NGDP growth to average just under 4.0 percent over 2020–24.

COVID-19 initially caused a steep decline in both real activity and inflation. Over the first two quarters of 2020, real GDP fell 10.1 percent, and prices were unchanged. Policymakers responded with unprecedented fiscal and monetary support, and over the next five quarters—ending in third quarter 2021—real GDP increased by a stunning 12.9 percent, and prices rose 5.6 percent. This surge put NGDP just below the 4.0 percent growth path expected prior to the pandemic, as the right-hand panel of Chart 1 shows.

Household incomes, state and local-government revenues and corporate profits have exceeded prepandemic expectations, driven in part by large federal transfers and aggressive fiscal stimulus as noted in the right-hand panels of Chart 2. As a result, households and businesses experienced fewer financial strains during the pandemic period than in prior years (Chart 3, right panels).

Real GDP remains about 2 percent below what was expected prepandemic, reflecting lingering supply problems. That real shortfall has been almost exactly offset by a price level that is 1.9 percent above prepandemic expectations.

A central bank focused solely on containing inflation would likely have been less accommodative, while a central bank focused solely on real activity would have applied more stimulus. The middle course that the Federal Reserve has followed so far, with below-trend output offset by above-trend inflation, is consistent with a 4 percent NGDP growth target.

Where do we go from here?

The policy response to COVID-19 has successfully protected the income and revenue streams of households, businesses, and state and local governments, limiting financial strains and promoting a strong labor market recovery. Aggregate income, as measured by NGDP, is back on its prepandemic path.

But will NGDP stay on that path? Professional forecasters think not. Blue Chip forecasters see NGDP growth exceeding 4.0 percent from now through 2025. Thereafter, growth stabilizes, leaving the level of NGDP 4.2 percent above trend, as depicted in the right panel of Chart 1.

If the pandemic has no lasting effect on real output, that upward shift in NGDP would imply a price path 4.2 percent higher than before the pandemic. If the pandemic leaves a lasting negative mark on output, the upward shift in the price path will be even larger. The expectations of Fed policymakers, as documented in the latest Summary of Economic Projections, are broadly consistent with this outlook.

An NGDP-targeting strategy would prescribe removing policy accommodation more rapidly than currently expected in order to keep incomes nearer their prepandemic trends and reduce the long-run price-level impact of the pandemic.

About the Authors

Tyler Atkinson

Atkinson is a business economist in the Research Department at the Federal Reserve Bank of Dallas.

Evan Koenig

Koenig was a senior vice president in the Research Department at the Federal Reserve Bank of Dallas.

Ezra Max

Max is a research analyst in the Research Department at the Federal Reserve Bank of Dallas.

The views expressed are those of the authors and should not be attributed to the Federal Reserve Bank of Dallas or the Federal Reserve System.