Fed’s 1994 rate aggressiveness led to emerging-market turmoil; is this time different?

As the Federal Reserve embarks on a monetary tightening cycle, only a few spots of vulnerability have appeared among emerging markets. Unlike in 1994, when U.S. policymakers’ aggressiveness roiled these markets—especially Mexico’s—the markets appear in a relatively safer place now.

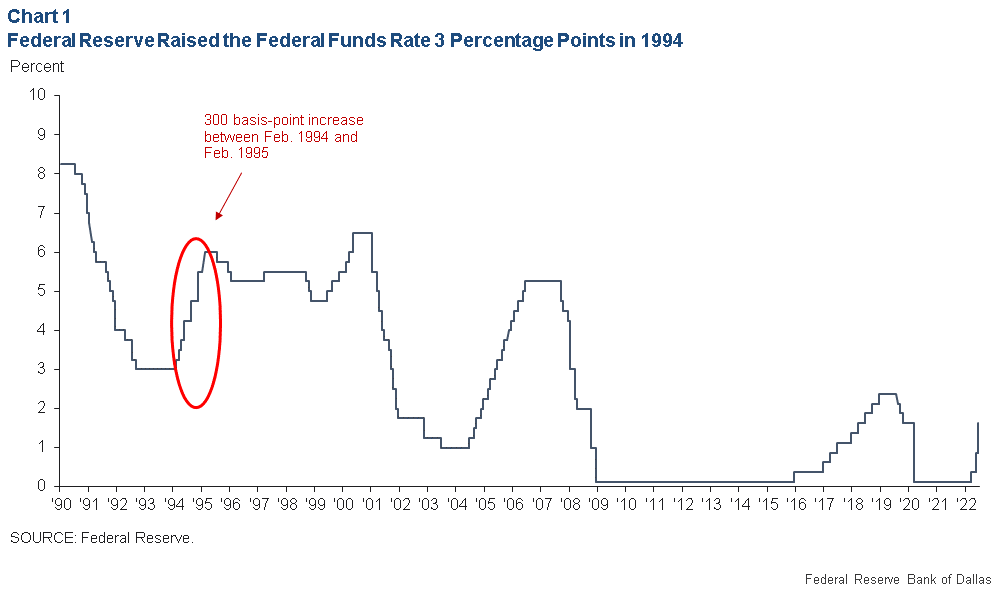

Current Fed monetary tightening is the most forceful in almost three decades. The federal funds target rate has increased by 1.5 percentage points over the past three meetings and is expected to rise a total 3.25 percentage points in 2022, according to the median projection from the Summary of Economic Projections released after the June Federal Open Market Committee meeting.

This would be a quarter percentage point greater than the 3 percentage points of tightening between February 1994 and February 1995 (Chart 1).

Mexico’s tequila crisis and rising U.S. rates

During the 1994 tightening cycle, the penultimate increase was a 75-basis-point (0.75 percentage points) move in November 1994, the Fed’s last 75-basis-point boost until June 15, 2022. The tightening cycle sparked the Mexican currency crisis in December 1994—nicknamed the “Tequila Crisis.”

While domestic factors, including excessive debt build-up, political instability and an unsustainable exchange rate peg, made the economy especially vulnerable to external shocks, Fed interest rate increases provided the final jolt.

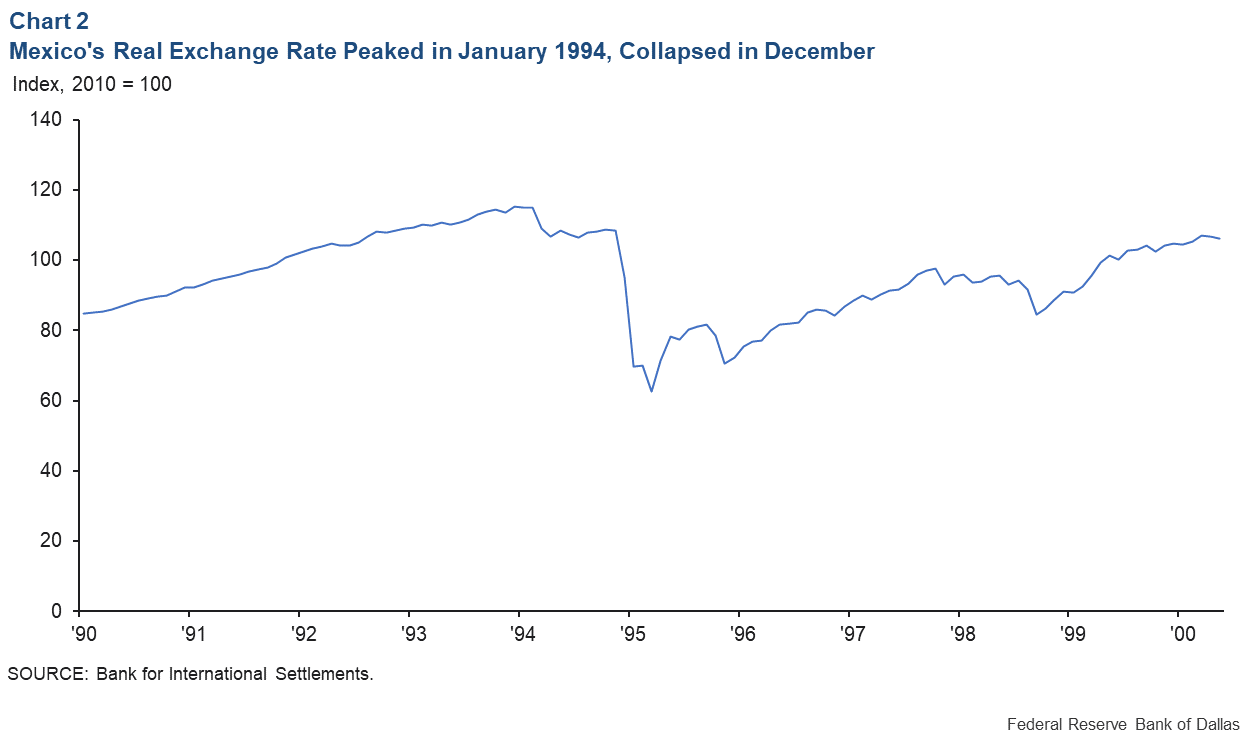

The Mexican real exchange rate (the value of the Mexican peso in terms of dollars, adjusted for the purchasing powers of the two currencies) peaked in January 1994 and gradually depreciated during 1994, losing about 8 percent of its value. The real exchange rate collapsed in December that year, dropping more than 40 percent of its value between November and March 1995 (Chart 2).

The interest rate on the three-month Mexican treasury bill rose from around 10 percent in February 1994 to 14 percent in November. It skyrocketed to more than 70 percent by March 1995.

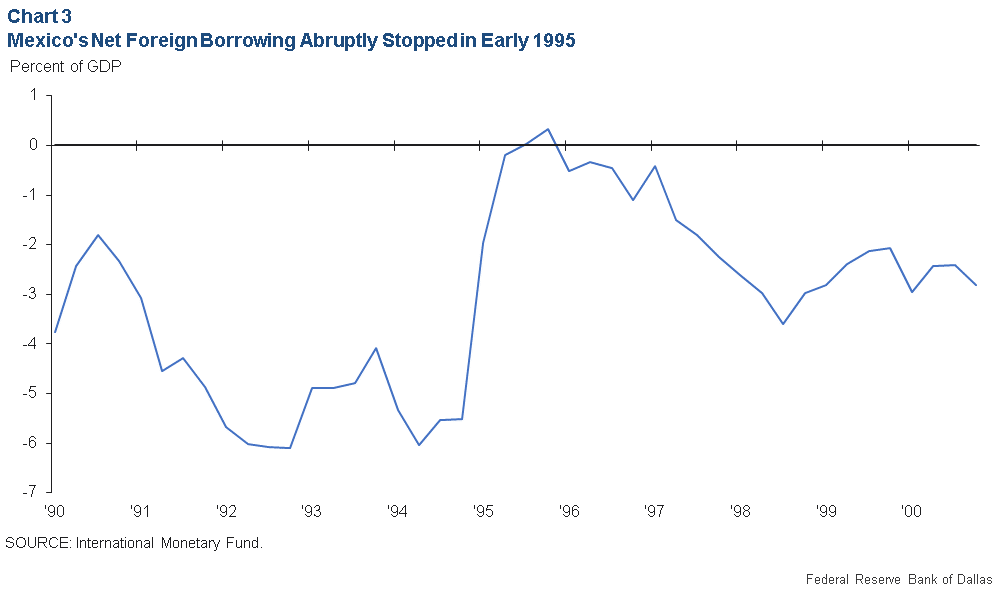

This real-exchange-rate collapse and spiking local interest rates were tied to a collapse in foreign borrowing. The Mexican current account deficit—a measure of net capital inflows—had grown during the early 1990s, reaching nearly 6 percent of GDP by 1994. By the second quarter of 1995, Mexico was running a current account surplus, indicating that those foreign capital inflows had come to a halt (Chart 3).

Why foreign borrowing suddenly stopped

What explains this sudden collapse of the Mexican exchange rate and foreign borrowing in late 1994 in response to a Fed tightening cycle? And while the 1994 Fed began tightening in February, why did it only lead to a gradual exchange rate depreciation and a gradual interest rate increase through November, before the December collapse?

In a recent article, we model a collapse in foreign borrowing in a small open economy in response to an increase in the foreign interest rate, and we describe policies that a central bank can implement to prevent it.

For this, we rely on the model of an underborrowing equilibrium (from Stephanie Schmitt-Grohé and Martín Uribe 2021). In this underborrowing equilibrium model, a small open economy faces a borrowing constraint—its ability to borrow from abroad depends on the value of collateral. The economy faces a currency mismatch where borrowing is denominated in the foreign currency but at least some collateral is denominated in the domestic currency.

Under a range of possible conditions, two equilibria can occur in a country with high external debt. This results from a circularity—high foreign borrowing leads to a strong exchange rate that supports high foreign borrowing (and conversely, a weakening exchange rate produces inadequate backing for such borrowing).

In one equilibrium, foreign borrowing is high, leading to strong domestic consumption and a strong exchange rate, raising the value of collateral, loosening borrowing constraints and allowing still more foreign borrowing. In another equilibrium, foreign borrowing is low, leading to low domestic consumption and a weak exchange rate, reducing the value of domestic collateral, tightening borrowing constraints and reducing foreign borrowing.

Ripple effects of high U.S. policy rate

In this framework, even a modest increase in the U.S. interest rate can trigger a collapse in foreign borrowing in an emerging-market economy such as Mexico. As the U.S. interest rate increases, there will be a gradual reduction in Mexican capital inflows and the real exchange rate as investors find U.S. assets more attractive. This resembles the 8 percent depreciation in the Mexican real exchange rate between February and November 1994.

There comes a point where the value of the exchange rate no longer supports the high borrowing/high consumption equilibrium. At that point, there is a collapse in foreign borrowing, or a “sudden stop,” as borrowing constraints bind. The economy must revert to the only equilibrium remaining, with low foreign borrowing, low consumption and a weak exchange rate.

Of course, the Fed tightening cycle in 1994 didn’t trigger a sudden stop in all emerging-market economies. Two key factors explain why a collapse happened in Mexico and not elsewhere.

The first factor is the economy’s level of external debt. Key to the existence of an underborrowing equilibrium is a high level of external debt. When an emerging-market economy’s level of external debt is high, continued foreign borrowing is only supported by a strong exchange rate that raises the value of domestic collateral.

In this case, even a small increase in U.S. interest rates could upset that fragile equilibrium. Mexico had run high current account deficits of nearly 6 percent of GDP throughout the early 1990s, so by 1994, the economy had accumulated a sufficient stock of external debt.

The second factor is central bank reserves. Central bank reserves are liquid foreign currency assets that a central bank can sell in a time of crisis to support the value of the currency and prevent a collapse. In 1994, Mexico’s central bank reserves were insufficient.

If the rise in the U.S. interest rate leads to a fall in foreign inflows and exchange rate depreciation, the central bank can sell foreign assets and use the proceeds to buy domestic assets, offsetting the decline in foreign capital inflows. A sufficient amount of selling by the central bank will support the value of the exchange rate when U.S. interest rates are rising, ensuring that the exchange rate can still support the high borrowing/high consumption equilibrium.

However, to sell foreign assets during a crisis, the central bank must own a stock of such assets before the crisis. Emerging markets must decide what reserve level is adequate to protect their currency against swings in foreign monetary policy.

Pablo Guidotti, a former deputy finance minister in Argentina, came to a conclusion that was later popularized by former Federal Reserve Chairman Alan Greenspan. In a 1999 speech, Greenspan summarized the rule stating “that countries should manage their external assets and liabilities in such a way that they are always able to live without new foreign borrowing for up to one year.”

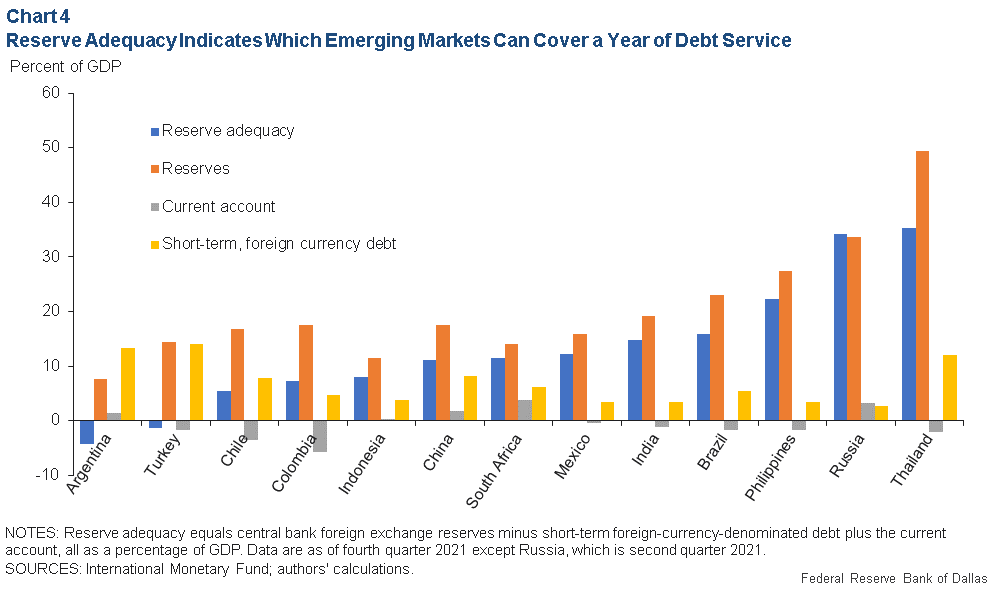

The Guidotti–Greenspan rule leads to a simple measure of a central bank’s reserve adequacy: foreign exchange reserves minus the sum of short-term foreign-currency-denominated external debt and the current account deficit.

Banco de México entered 1994 with foreign exchange reserves of about 5 percent of GDP. At the time, the Mexican current account deficit was nearly 6 percent of GDP, meaning that the central bank did not have enough reserves to cover a year’s worth of new borrowing, much less service existing debts.

Is this time different?

Chart 4 presents reserve adequacy as well as its three components for the major emerging-market economies at the end of 2021.

Reserve adequacy is negative only in Turkey and Argentina, with their low stock of reserves and high amounts of short-term foreign currency debt. Colombia and Chile have relatively high current account deficits but, at least for the time being, have a high stock of reserves and a relatively low stock of short-term foreign currency debt.

Mexico is in a much different place than it was in 1994. It boasts a relatively high stock of reserves, a small current account deficit and a stock of short-term foreign currency debt that is among the lowest in the major emerging markets.

This suggests that as the Fed tightens monetary policy and raises interest rates, many major emerging-market economies—notably including Mexico—are in a much safer place than they were in 1994, the last time the Fed was so aggressive.

About the Authors

Scott Davis

Davis is an economic policy advisor and senior economist at the Federal Reserve Bank of Dallas.

Michael B. Devereux

Devereux is a professor of economics at the University of British Columbia.

Changhua Yu

Yu is an associate professor of economics at Peking University.

The views expressed are those of the authors and should not be attributed to the Federal Reserve Bank of Dallas or the Federal Reserve System.