Data center boom expected to raise electricity component of PCE inflation

With the emergence of artificial intelligence, data center construction has surged with plans for more to become operational in the coming years. The growth of data centers poses challenges to the electric grid with important implications for retail electricity prices and inflation.

While there are many challenges to a rapid expansion of data centers, including concerns about the supply chains for turbines, batteries, transformers and chips, and the need for a much larger skilled workforce, this development has attracted much attention among market observers. For example, BloombergNEF projects that power demand from data centers is set to double from 40 gigawatts today to 80 gigawatts by 2031.

Recent analysis conducted at the Federal Reserve Bank of Dallas forecasts the rise in wholesale and retail electricity prices attributable to the data center boom under a range of hypothetical scenarios. Of particular interest from a policy point of view are the implications of these scenarios for personal consumption expenditures (PCE) inflation, the Federal Reserve’s preferred inflation measure.

Even a modest data center boom could substantially raise retail electricity prices and hence annual inflation. For example, under plausible assumptions about the data center build-out and utilization, annual PCE inflation in 2030 would increase by between 0.04 and 0.13 percentage points. Slower-than-expected growth of renewable energy sources—wind and solar—could nearly double the inflationary effect.

This analysis, while tentative, is the first attempt to quantify these inflationary effects using a model of electricity markets grounded in detailed data about all existing and planned data centers and all power plants in the U.S., including planned additions, retirements and upgrades. The model also draws on fuel price and power demand forecasts generated by the Energy Information Administration and proprietary data on the power use of data centers.

Why data centers matter for electricity prices

New residents or companies moving into a community routinely request a connection to the electric grid. These expansions in service tend to be modest, gradual and predictable, allowing utility companies to finance them through retail price adjustments borne by existing customers. This practice no longer works well when a data center consuming the power equivalent of a small city requests new service. Such rapid load growth inevitably involves costly grid upgrades and additional infrastructure.

Regulators have instituted a queue for “large load” requests, typically involving fees for new connections. These fees tend to be modest, leaving existing customers on the hook for the expansion of the electric grid. The potential for significant increases in electricity bills has led government leaders in some states to consider legislation shielding ratepayers from the additional grid costs or even limiting data center construction completely. Companies such as Microsoft and Anthropic, in response, have pledged to pay the cost of connecting their data centers to the grid. However, how these commitments will materialize remains to be seen.

Existing customers, besides facing some of the costs of expanding the grid, also confront the rising costs of generating electricity. As data centers raise the demand for power and more expensive power providers are called upon, the wholesale price of electricity rises in the short run. In the longer run, higher prices incentivize new power generation with customers indirectly paying for the costs of building new power plants, expanding renewables and adding battery storage.

A central question is how much we expect the wholesale and retail price of electricity to increase in the coming years. Answering this question requires a model based on detailed data about projected electricity demand and supply because past electricity price data offer little guidance about future prices in a market that is fundamentally changing and will continue to evolve in the coming years.

Modeling the evolution of wholesale electricity prices, 2026–30

We construct such a model based on analysis of the data for all current and planned power plants and data centers in the U.S. The model aggregates hourly forecasts of the wholesale electricity price for 22 electricity grid regions in the U.S. under various scenarios. These price forecasts are generated by solving the cost minimization problem of regional system operators, hour by hour, given the supply curve of the available power generators and a forecast of the base load on the grid from conventional power users as well as the added power demand expected from data centers.

The implied wholesale prices are then aggregated over time and across regions to generate predictions of the monthly increases in U.S. wholesale electricity prices for each year between 2026 and 2030 as a result of the data center boom.

One important challenge in modeling is that the maximum potential use of electricity is known for only 62 percent of existing data centers. That share drops to 50 percent for planned data centers. The actual utilization of that capacity is even less certain.

Another challenge is that planned data centers are best thought of as options. Firms put in multiple applications for data centers in different locations, hoping for a good deal, with no intention of actually constructing all of these projects. Thus, standard measures of the load required by planned data centers must be taken with a grain of salt.

We consider a range of scenarios to deal with these challenges. For example, because not all proposed data centers will be constructed and some will generate their own power “behind-the-meter,” we reduce the proposed capacity by 40 percent in line with industry expectations. Power usage also varies by data center type. To account for uncertainty about the hourly utilization of data centers, we consider two utilization patterns.

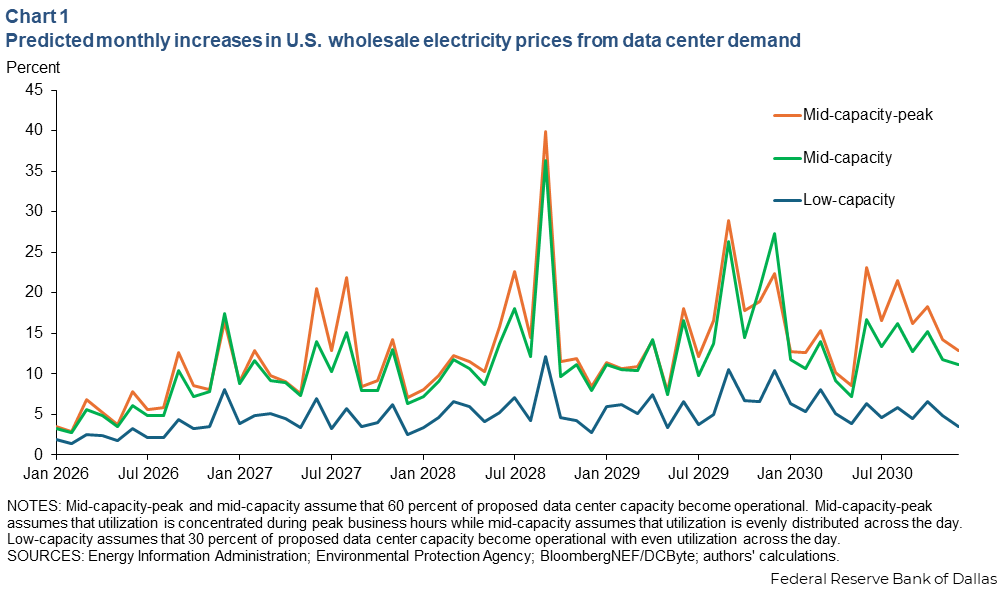

In one scenario (mid-capacity-peak), power demand is concentrated in the peak business hours of the day. In the other scenario (mid-capacity), demand is evenly spread throughout the day. Both scenarios are grounded in reported utilization rates and market share data by data center type from Bloomberg NEF and DCByte. We also consider a third scenario (low-capacity) that assumes only 30 percent of proposed data center capacity connects to the grid with power usage evenly spread throughout the day.

The choice of the scenario greatly matters for the implied monthly increases in average U.S. wholesale electricity prices (Chart 1). At one extreme, these increases may exceed 40 percent in selected months, while at the other extreme they may be bounded by 12 percent.

As in the historical data, there is large seasonal variability in wholesale electricity price forecasts. Our ultimate interest, of course, is not the predicted evolution of wholesale electricity prices but how these price increases affect the retail prices consumers pay. These are subject to state regulation and, thus, are much less volatile.

From wholesale electricity prices to inflation

In practice, local electricity suppliers faced with higher wholesale electricity prices will request state regulators adjust future retail prices to ensure suppliers can recoup their rising costs. Rather than modeling this regulatory process, we assume that all of the average wholesale price increase will pass through to retail prices within the same year. This simplifying assumption may affect the timing of increases from one year to the next but has little effect on the overall trend in retail prices.

We further incorporate the fact that wholesale purchases of electricity typically account for about 50 percent of the retail price of electricity. This implies percentage increases in retail prices are only half as large as the corresponding percentage increases in wholesale prices.

Finally, we take account of the fact that the weight of electricity purchases in the construction of the PCE depends on the evolution of the retail electricity price. We therefore update this expenditure share based on the predicted retail price in line with our model-based price forecasts, starting from the current expenditure share of 1.27 percent, assuming that all other prices remain unchanged.

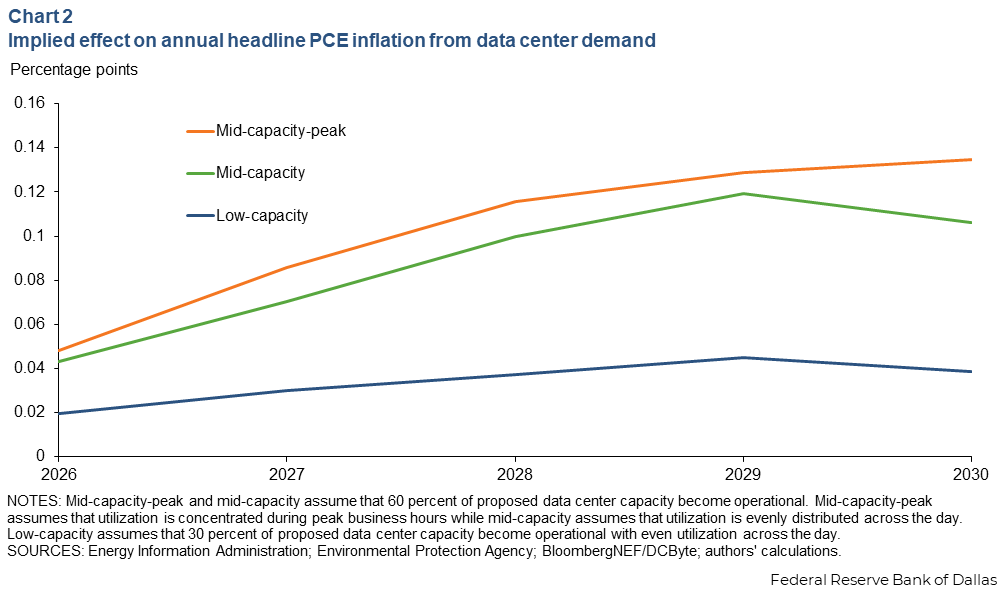

Not surprisingly, the inflationary impact also greatly depends on the assumptions made about the build-out of the data centers and their utilization. In all scenarios, the impact of the data center boom grows substantially over time (Chart 2).

In our two mid-capacity scenarios, the impacts on inflation are similar. When utilization is concentrated in peak hours, data centers alone increase headline PCE inflation by 0.05 percentage points in 2026 and by 0.13 percentage points in 2030 through their effect on retail electricity prices. When utilization is spread throughout the day, the effects are slightly lower. In the low-capacity scenario by contrast, the inflationary impact shrinks to between 0.02 percentage points in 2026 and 0.04 percentage points in 2029.

As a point of comparison, if all proposed data centers were to connect to the grid and operated at maximum capacity all the time, annual PCE inflation would rise 1.02 percentage points in 2030. This evidence indicates substantial uncertainty about the inflationary impact of the data center boom.

While this maximum capacity scenario is highly implausible, it highlights the upside risk to inflation from data centers. Given the emerging public and political resistance to rising electricity prices and the growing willingness of data center operators to pay for the expansion of the grid and added power generation, we believe that outcomes between the low- and mid-capacity scenarios are most likely.

Sensitivity of the inflationary impact to projections of solar power growth

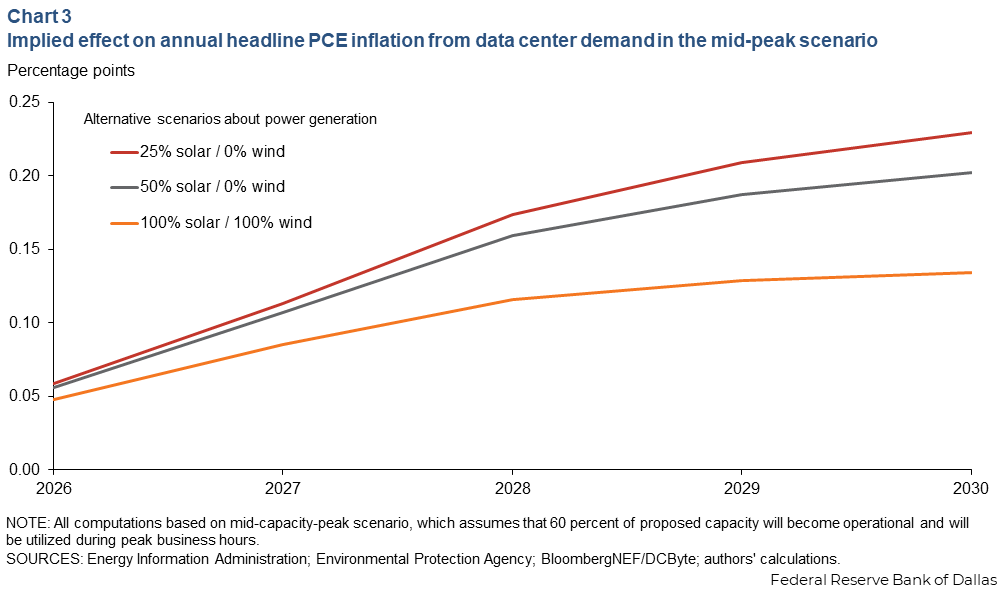

These estimates implicitly assume that a combination of delaying the retirement of existing power plants and the continued build-out of onshore wind power and, more importantly, of solar power will occur in line with Energy Information Administration data on proposed projects. Thus, the inflationary impacts in Chart 2 hinge on the growing reliance of the electricity market on renewables.

Next, we examine the additional inflationary impact in the mid-capacity-peak scenario, assuming only 50 percent of the proposed solar power growth and none of the proposed onshore wind power growth become available. We also consider a more extreme scenario that further reduces solar growth to only 25 percent of what has been proposed (Chart 3).

The model implies that by 2030 the additional increase in annual PCE inflation could be as high as 0.10 percentage points in the case where additional solar is only 25 percent of proposed projects, nearly doubling the inflationary impact from data centers.

While these effects will be somewhat smaller under the alternative scenarios, our analysis highlights the sensitivity of the inflation projections to assumptions about power generation even at short horizons. When extending the forecast horizon beyond 2030, the inflationary effects of data centers would be expected to increase sharply in the absence of substantial investments in new natural gas and/or nuclear power generation.

Implications for inflation

Undoubtedly, this analysis may be refined in many ways. For example, one could take account of interregional electricity transmission along with the costs of transmission and distribution. Or one could model the pass-through from wholesale to retail electricity prices.

Nevertheless, our analysis highlights three key points:

- A large-scale build-out of data center infrastructure, as discussed by many market observers, would raise annual PCE inflation at ever-increasing rates between 2026 and 2030. The impact on annual inflation would rise to 1.02 percentage points in 2030 if all proposed data centers were connected to the grid and fully utilized.

- Such estimates are unrealistically large, but even a much more modest data center boom could substantially raise retail electricity prices and, hence, annual inflation. For example, under more plausible assumptions about the data center build-out and utilization, annual PCE inflation in 2030 would still increase by between 0.04 and 0.13 percentage points.

- Slower-than-expected renewables growth could nearly double the inflationary effect.

About the authors

Owen Kay is a former research economist at the Federal Reserve Bank of Dallas and an external research affiliate of the Center for Energy Economics.

Lutz Kilian is a vice president in the Research Department and director of the Center for Energy and the Economy at the Federal Reserve Bank of Dallas.

Reid Taylor is a research economist in the Research Department at the Federal Reserve Bank of Dallas.