Effects of realized tariff changes on PCE prices peaked in first quarter 2026

We estimate the effect of 2025 realized tariff rate changes on relative prices. Tariff collections lagged behind announced policy changes, and our results imply a delayed impact of tariff changes on consumer prices relative to estimates based on tariff policy announcements.

Realized tariff rates are the ratio of calculated duties to the customs value of imports. Our analysis is based on realized tariff rates as of December 2025. We compare how price growth evolved in 2025 in core personal consumption expenditures (PCE) categories facing realized tariff rate changes. We use these findings to estimate the effect on relative prices.

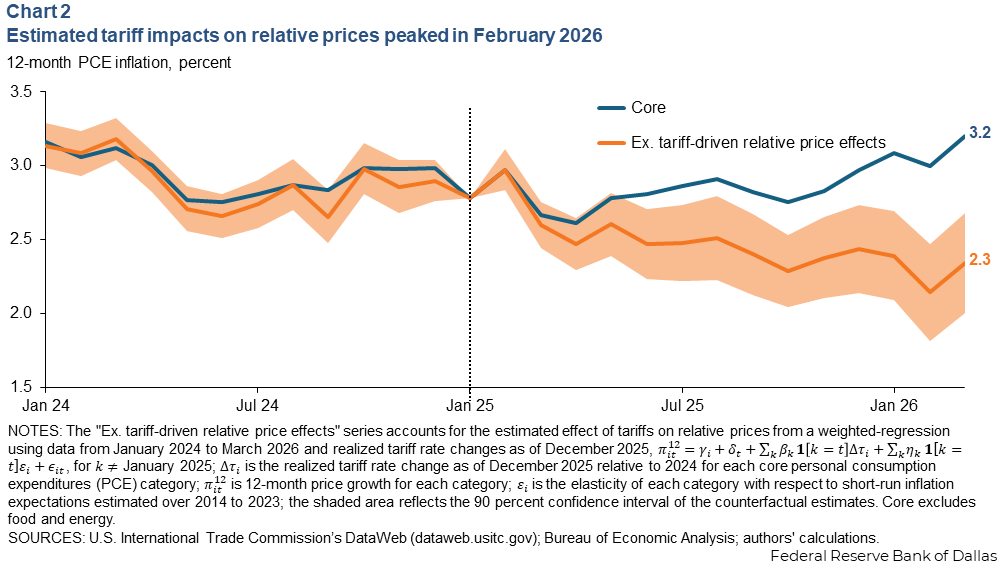

We estimate that tariff collections increased March 2026, 12-month core PCE inflation by about 0.80 percentage points and that core inflation absent tariff effects on relative prices would be 2.3 percent.

Additional tariff developments in 2026, including the Supreme Court’s International Emergency Economic Powers Act decision overturning continued imposition of many of the tariffs, and subsequent introduction of a planned alternative tariff structure, will likely influence goods prices moving forward.

Why use realized tariff rates?

Two factors motivate our choice to focus on the relative price effects of realized tariff rate changes rather than implied rates from announced tariff policy changes. First, there were many relatively large tariff policy changes in 2025. Second, there was general uncertainty about where policy changes would settle while negotiations with key trading partners continued throughout the year.

Given these observations, it is unclear whether we should expect firms to have passed through implied cost increases ahead of those realized. Instead, our estimates assume that firms are more likely to pass-through incurred cost increases from higher tariff collections on imported goods.

Notably, analysis based on realized rates requires taking as a given some adjustments to tariffs. Examples include if firms substitute away from high-tariffed countries to alternative foreign suppliers or toward domestic suppliers, changes in exchange rates and any additional adjustments due to tariff policy changes outside of the U.S.

We also assume that firms across the distribution of realized tariff changes would have responded similarly to a tariff increase of the same size. Our estimates can then be interpreted as the pass-through to consumer prices of higher costs incurred at the border due to realized tariff rate changes.

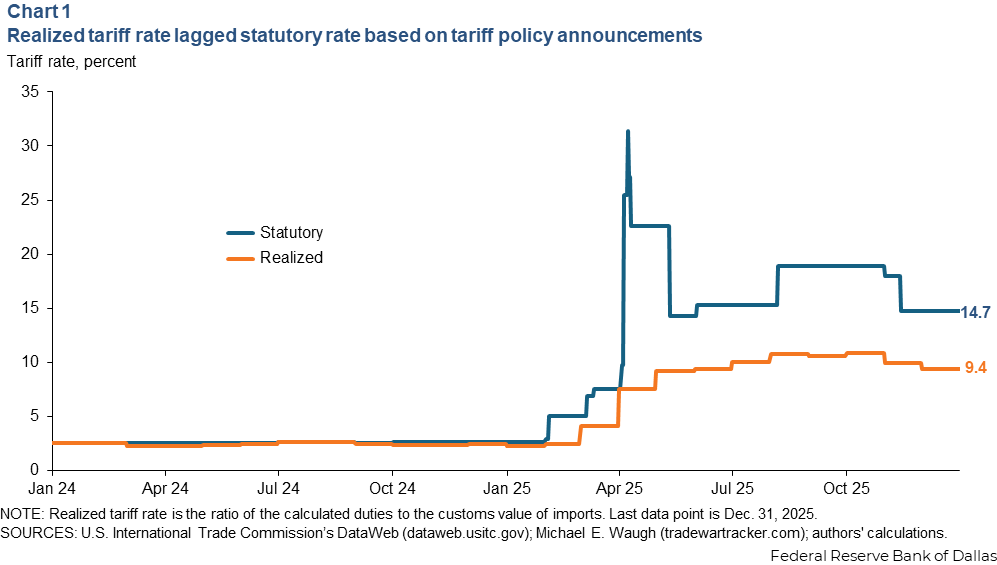

Tariff collections data imply that realized tariff rates differed from statutory tariff rates calculated based on tariff policy announcements during 2025 (Chart 1).

The realized tariff rate rose from 2.3 percent in 2024 to 10.9 percent by October 2025 and ended 2025 at 9.4 percent. Collected tariffs lagged behind announced policy changes, and a gap arose between the statutory and realized tariff rates that persisted over the year.

Tariff impacts strongest in February 2026

How did cost increases incurred from realized tariff rate changes in 2025 impact consumer prices? To determine the effect, we first calculate the predicted impact of realized tariff rate changes as of December 2025 relative to the average rate in 2024 across PCE categories excluding food and energy, or core PCE categories. We account for both the direct and indirect exposure of categories to imported commodities that faced realized tariff changes.

We then estimate the monthly relationship between excess increases in 12-month price growth across PCE categories and predicted increases in price levels attributable to end-of-year realized tariff rates. For each category, excess PCE inflation is measured relative to 12-month price growth rates from January 2025.

With this approach, we treat the 2025 tariff changes as a single, drawn-out event and do not impose the timing of when firms passed on incurred cost increases. We weight observations by the relative importance of each category for 12-month core PCE inflation, meaning our pass-through estimate places more weight on categories that account for a larger share of consumption expenditures.

In addition to tariffs, we account for category-specific effects or factors that impact a particular PCE category at all times during our sample period as well as time-specific effects. These are factors that impact all PCE categories in a similar way but vary over time—for example, macroeconomic conditions.

We recognize that underlying macroeconomic conditions can also differentially affect prices across core PCE categories. For this reason, we also account for varying price sensitivity among core PCE categories to inflation expectations. We estimate the sensitivity of each core PCE category to three-year-ahead inflation expectations as measured by the Federal Reserve Bank of New York Survey of Consumer Expectations median point prediction from 2014 to 2023. Including this elasticity in our estimation allows some of the time-specific effects that impact all categories to be attributable to inflation expectations, and accounts for the varying sensitivity of core PCE categories to inflation expectations.

Chart 2 shows counterfactual 12-month core PCE inflation estimates that account for the relative price impacts of tariffs from our estimation procedure.

The inflation estimates from this procedure prior to the tariff shock align with observed inflation. Estimated tariff impacts on 12-month core PCE inflation peaked in February 2026 at a level consistent with full pass-through of tariff collection-driven cost increases to consumer prices. Analysis of relative price effects due to monthly changes in statutory rates following tariff policy announcements imply a lower counterfactual core PCE inflation path in third and fourth quarter 2025.

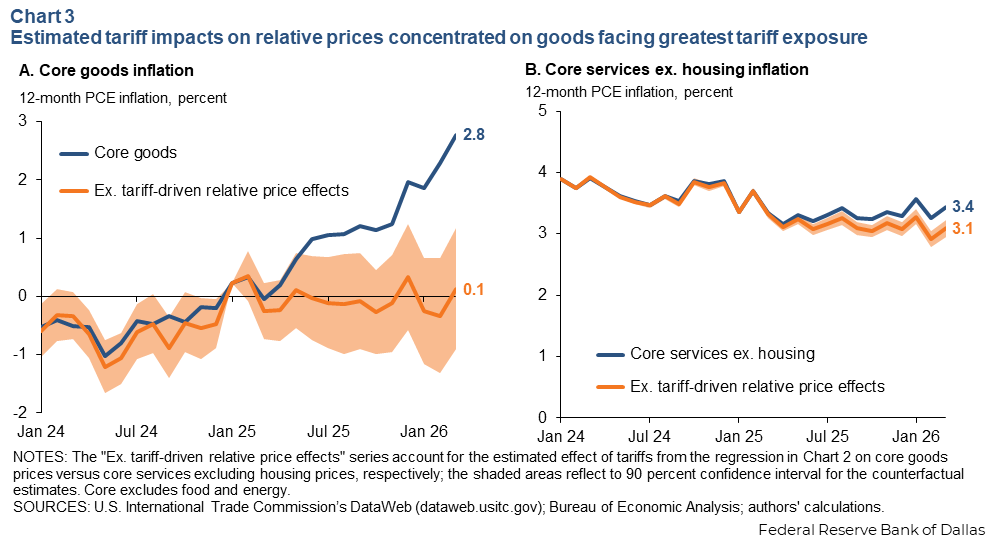

Chart 3 shows the corresponding counterfactual 12-month core goods and core services, excluding housing, PCE inflation rates. The main impact of tariffs on inflation was through goods prices. Notably, the counterfactual core goods inflation rate is also elevated compared with prepandemic. Twelve-month core goods inflation, accounting for tariff impacts, averaged near zero from February 2025 to March 2026.

Summary and comparison to other estimates

We find evidence that impacts of realized tariff rate changes on relative price changes across PCE categories peaked in first quarter 2026, and that these impacts are roughly consistent with the cumulative impact we would expect given the changes in realized tariff rates in 2025.

Our results suggest that additional strengthening of 12-month core goods inflation rates would likely be inconsistent with direct impacts of 2025 tariff rate changes alone but rather reflect tariff-driven spillovers or other factors keeping core goods inflation elevated

These results are consistent with those of a recent Federal Reserve Board staff FEDS Note based on announced tariff policy changes. The FEDS Note suggests that the peak impact of relative price changes due to tariff policy announcements on 12-month core PCE inflation occurred in January 2026. The two findings differ in the amount of 12-month core PCE inflation in the second half of 2025 attributable to relative price changes due to tariffs.

About the authors

Ron Mau is a senior business economist at the Federal Reserve Bank of Dallas.

Tucker Smith is a research economist in the Research Department of the Federal Reserve Bank of Dallas.