Implications of the Iran war for U.S. inflation

The outbreak of the Iran war in late February 2026 disrupted oil and refined product exports from the Middle East. This has been reflected in a global surge in crude oil and retail gasoline prices, with no end in sight.

A question of immediate interest to policymakers and consumers is how rising gasoline prices driven by this conflict will affect U.S. headline and core inflation. There is also concern that these gasoline price increases may raise household inflation expectations, amplifying the direct impact of higher gasoline prices.

A major challenge in answering these questions in real time is that the evolution of the price of oil, and hence the price of gasoline, remains highly uncertain. It is unknown how long the Strait of Hormuz will remain closed and how much oil will be exported from the Persian Gulf if the war continues.

Recent research at the Federal Reserve Bank of Dallas quantifies the impact of the 2026 Iran war on U.S. inflation and household inflation expectations under a range of scenarios. Whereas that study started with the largest possible oil supply shortfall and examined the sensitivity of the implied impact on inflation under a range of scenarios, the focus of this article is to examine a scenario that reflects the current shortfall in global oil supplies.

Under this current scenario, 2026 fourth-quarter-over-fourth quarter headline PCE inflation increases by 0.6 percentage points, while core PCE inflation increases by 0.2 percentage points. We discuss how sensitive this result is to changes in expectations and the resumption of military action.

How we go about quantifying the inflationary impact

Our analysis builds on an earlier Federal Reserve Bank of Dallas study that shows how the global price of oil responds to geopolitically driven oil production shortfalls, accounting for the fact that such events are rare and occur with a time-varying probability.

The model from that study is used to construct paths for the quarterly price of oil under a range of scenarios about the nature of the oil supply shortfall. We then translate a given oil price path into the corresponding path for retail gasoline prices, taking into account the actual evolution of oil and gasoline prices in March 2026 and the cost share of oil in the retail gasoline price.

We incorporate this gasoline price path into recently developed empirical models of the impact of monthly gasoline price shocks on U.S. inflation and household inflation expectations. This provides insights into the magnitude and persistence of the potential impact of higher oil prices during 2026 and 2027, building on the historical relationship between gasoline prices, inflation and inflation expectations.

A complete cessation of oil exports from the Persian Gulf, including a closure of the Strait of Hormuz, would correspond to a disruption of 20 percent of global oil supplies. Here we focus on a scenario that involves a 15 percent shortfall. This takes into account the diversion of some oil exports to ports outside the Persian Gulf.

We assume that the closure of the Strait of Hormuz lasts for one quarter, after which there is uncertainty about when oil supplies will return to normal. This is equivalent to expecting the shortfall of oil supplies to gradually decline over time following the one-quarter closure. We discuss alternative scenarios further below.

Empirical findings

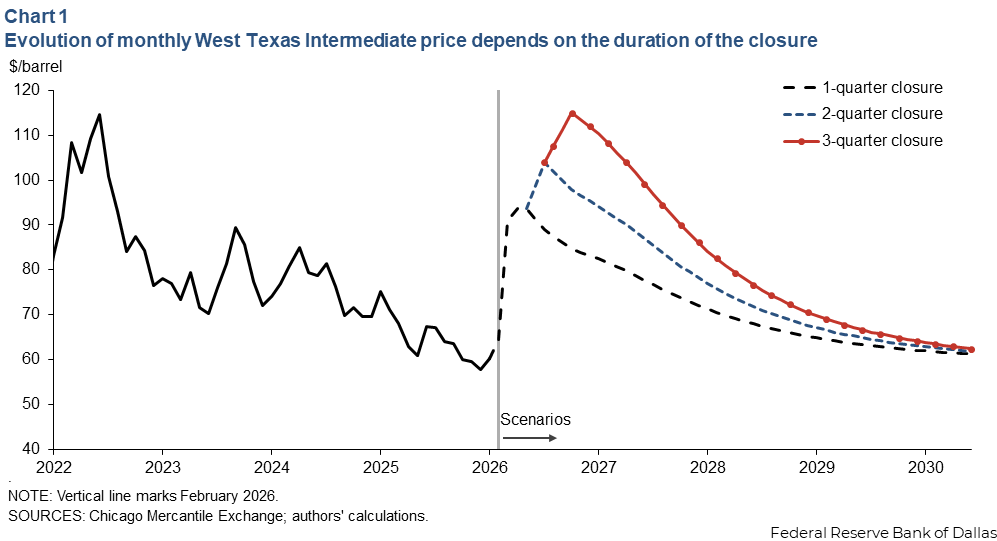

Our model predicts that in this case, the monthly average price of West Texas Intermediate (WTI) crude oil would peak at $94 per barrel in April and May 2026 and remain above $80 per barrel throughout 2026 (Chart 1, black-dashed line).

The sharp increase in the WTI price causes headline inflation to rise by 1.7 percentage points at an annualized rate in first quarter 2026 (Table 1). Headline inflation remains elevated through third quarter 2026. This lifts fourth-quarter-over-fourth-quarter headline inflation by 0.6 percentage points in 2026.

| 2026 | Headline inflation | Core inflation | 1-year inflation expectations |

| Q1 | 1.7 | 0.1 | 0.1 |

| Q2 | 0.5 | 0.4 | 0.4 |

| Q3 | 0.3 | 0.2 | 0.3 |

| Q4 | 0.0 | 0.2 | 0.2 |

| Q4/Q4 | 0.6 | 0.2 | - |

| NOTES: Quarterly inflation rates are annualized. SOURCE: Authors’ calculations. |

|||

There are also meaningful effects on inflation excluding food and energy (commonly referred to as core inflation). While the impact on core inflation is muted in first quarter 2026, it increases by 0.4 percentage points in the second quarter, followed by smaller increases later in the year. This translates to a 0.2 percentage point increase in fourth-quarter-over-fourth-quarter core inflation in 2026.

These impacts are not associated with large shifts in household inflation expectations. The effect on one-year inflation expectations peaks at 0.4 percentage points in the second quarter. The effects on long-run inflation expectations are negligible throughout the year.

Empirical findings under alternative scenarios

Our framework facilitates the evaluation of the inflationary impact under alternative scenarios. Under a given scenario, we generate the path of the U.S. retail gasoline price implied by the model of the global economy. We then use that path.

While we have chosen to focus on the case in which the Strait reopens and global oil supplies start returning to normal after only one quarter, the inflationary effects are larger when the Strait remains closed for two or three quarters.

If the Strait remains closed for two quarters, the WTI price peaks at $104 per barrel in July (Chart 1, blue-dashed line). If the Strait remains closed for three quarters, the price peaks at $115 per barrel in October (Chart 1, red-dotted line).

The higher oil price path in turn implies larger effects on inflation and inflation expectations. If the Strait remains closed for three quarters, for example, the impact on fourth-quarter-over-fourth-quarter headline inflation in 2026 increases to 1.1 percentage points, while the impact on core inflation increases to 0.3 percentage points (Table 2). One-year inflation expectations are also pushed up by as much as 0.5 percentage points in third quarter 2026, but the effects on long-term inflation expectations remain muted.

| 2026 | Headline inflation | Core inflation | 1-Year inflation expectations |

| Q1 | 1.7 | 0.1 | 0.1 |

| Q2 | 0.8 | 0.4 | 0.4 |

| Q3 | 1.3 | 0.4 | 0.5 |

| Q4 | 0.6 | 0.4 | 0.4 |

| Q4/Q4 | 1.1 | 0.3 | - |

| NOTES: Quarterly inflation rates are annualized. SOURCE: Authors’ calculations. |

|||

One could also consider a scenario in which market participants expect the outage to last much longer than in the scenarios discussed so far, for example, because Iran continues to restrict oil traffic through the Strait. This would substantially increase the initial oil price path while the Strait is assumed to be closed, causing larger increases in headline and core inflation and inflation expectations than in our earlier scenarios. This further highlights that the impact of the Iran war crucially depends on expectations.

All scenarios we discussed so far postulate a 15 percent shortfall in global supplies. An alternative, less-optimistic scenario would involve a somewhat larger oil supply shortfall, which could occur if peace talks fail and the war causes further damage to oil infrastructure in the Middle East.

As expected, a larger shortfall systematically raises the path of the WTI price as well as the impact on inflation and inflation expectations without changing the overall pattern of these effects. A smaller shortfall, perhaps due to a breakthrough in peace talks, would have the opposite effect

Beyond the Iran war

Our analysis covers a broad range of plausible outcomes. The differences in inflation outcomes can be traced to differences in assumptions about the nature of the oil supply disruption, mirroring differences in public perceptions. How relevant each of these scenarios is may change as the geopolitical situation in the Middle East evolves.

While our focus has been on the impact of the 2026 Iran war, our approach provides a blueprint for analyzing similar crises in the future. This is particularly important given that geopolitical oil supply disruptions have been a recurrent phenomenon since the 1970s.

About the authors

Lutz Kilian is a vice president in the Research Department and director of the Center for Energy and the Economy at the Federal Reserve Bank of Dallas.

Michael Plante is an assistant vice president in the Research Department at the Federal Reserve Bank of Dallas.

Alexander W. Richter is a vice president in the Research Department at the Federal Reserve Bank of Dallas.

Xiaoqing Zhou is an assistant vice president in the Research Department at the Federal Reserve Bank of Dallas.