Texas economy shows resilience amid geopolitical uncertainty

The Texas labor market showed signs of increasing momentum in early 2026, with employment growing 1.7 percent during the first quarter after a sluggish 2025.

However, the war in Iran is a source of caution. The conflict has negatively affected nearly half of surveyed Texas businesses through higher fuel costs and heightened uncertainty. Even so, headline business activity indicators remain positive, pointing to an economy that is resilient but vulnerable to sustained geopolitical pressures. Manufacturing activity, in particular, has surged this year, driven by pent-up demand, onshoring production and artificial intelligence (AI) infrastructure investments.

Job growth picks up in Texas

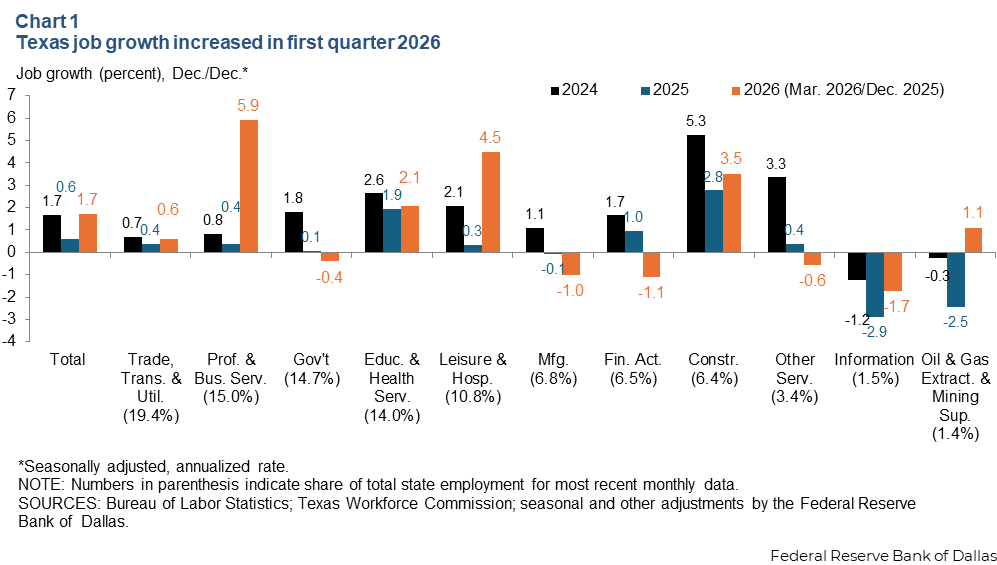

After experiencing unusually weak job gains in 2025 due to heightened policy uncertainty, higher tariffs and sharply lower immigration, Texas employment has begun to pick up. Jobs in the state increased 1.7 percent in the first quarter (Chart 1). While this rate of growth appears promising, it has been limited to a handful of sectors, with professional and business services accounting for a sizeable share.

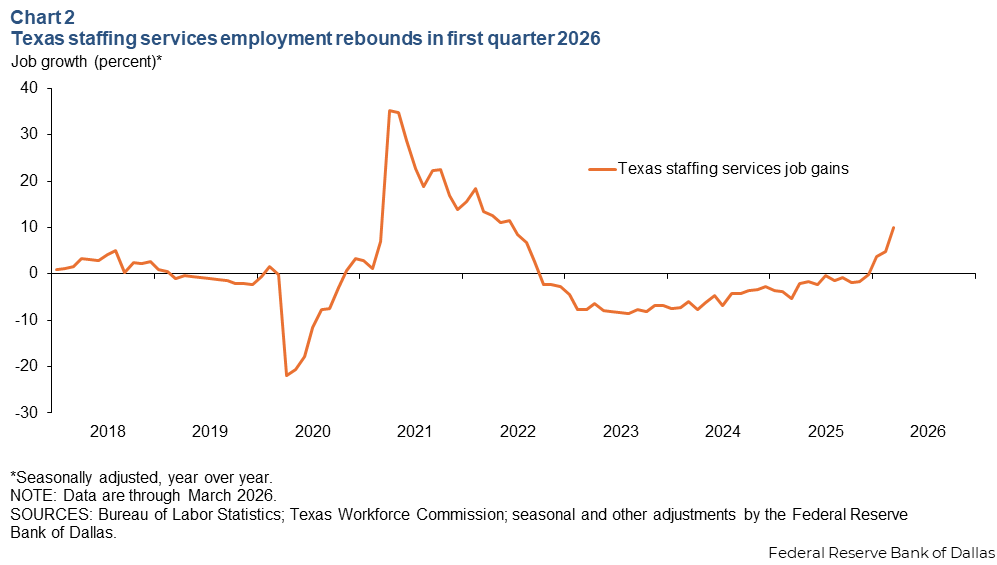

Most notably, staffing services employment (a subsector of professional and business services) rebounded in the first quarter, accounting for one-third of all job gains in the state (Chart 2). This rebound follows several years of contraction, which partially reflected a readjustment from pandemic-era highs that included a broader shift in employer preferences toward permanent hires during a tight labor market.

The recent resumption of growth in the sector bears watching. Employment services firms are often considered a leading indicator of labor market turning points because they can rapidly adjust headcounts in response to cyclical shifts. However, the outsized share could indicate that businesses prefer the flexibility of adding temporary workers over permanent staff amid heightened economic uncertainty. Nevertheless, the increased demand for temporary workers still signals an uptick in overall labor demand.

The unemployment rate in Texas has remained low and in line with the U.S. rate of 4.3 percent. Broader measures of unemployment, such as the U6 rate, which includes discouraged workers and part-time workers seeking full-time employment, declined from 8.5 percent to 7.9 percent during the first quarter, suggesting improvements in the labor market beyond the headline-unemployment rate.

However, Texas’ labor force participation rate ticked down further in March to 64.4 percent, a trend since September 2025, when the labor force participation rate was 64.9 percent. A declining participation rate could mask underlying weakness in the labor market if the drop is triggered by discouraged workers exiting the labor force entirely rather than actively seeking employment. Alternatively, it could also reflect an aging workforce and retiring workers or a drop in response rates among immigrants, whose participation rate tends to exceed that of U.S. workers. While this half-percentage point decline over six months isn't yet cause for alarm, it bears close monitoring. If this downward trajectory persists, it could signal deeper concerns about labor-market health.

Texas businesses report negative Iran war impacts

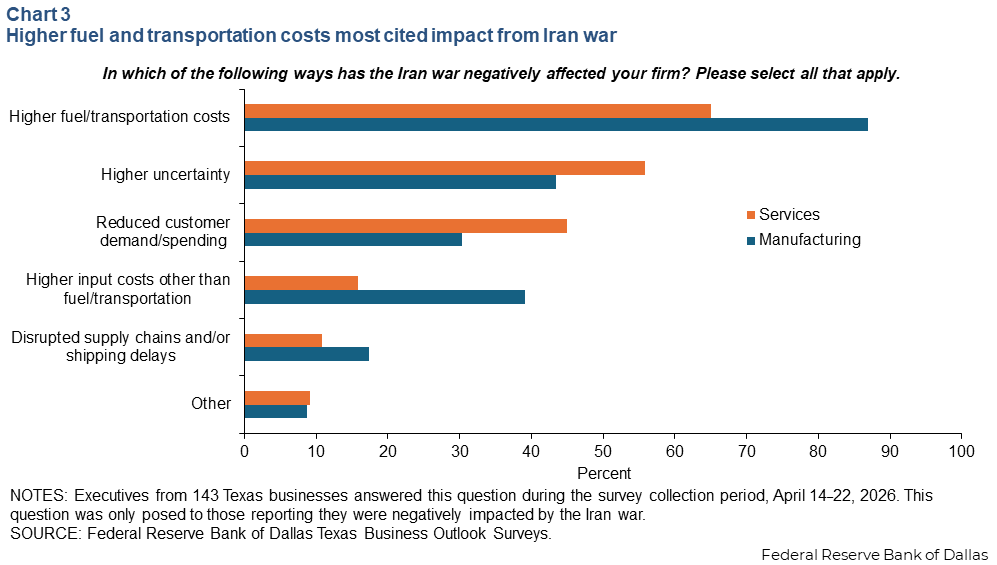

While the labor market shows improvement, geopolitical factors are creating headwinds. The Iran war has negatively affected many Texas businesses, though impacts are distributed unevenly across sectors. Nearly half of special question respondents to the Texas Business Outlook Surveys (TBOS) in April reported a net negative impact. The burden fell more heavily on service sector firms (51 percent citing negative impacts) versus manufacturers (35 percent).

Though a smaller share of manufacturers reported negative impacts overall, those affected faced more widespread cost pressures. Across both sectors, the most cited factors were higher fuel and transportation costs, particularly among manufacturers (Chart 3). Among manufacturers reporting negative impacts, 87 percent cited elevated fuel and transportation costs as a primary drag, followed by increased uncertainty (44 percent) and higher non-fuel input costs (39 percent).

One primary metals manufacturer noted, “Aluminum prices have risen substantially due to approximately 10 percent of the world’s primary aluminum supply coming from the Middle East, traveling via ship through the Strait of Hormuz. Also, two primary reduction smelters of aluminum were bombed by Iran, curtailing a significant portion of the production for that region. Prices should drop when the strait is fully back open, but the lost production will more than likely keep prices up somewhat.”

These inflationary pressures were also evident in firms' expectations for future price movements. Special survey questions from the March TBOS survey conducted at the outset of the Iran war revealed that expectations for both input cost increases and selling price increases ticked up compared with December.

Service sector firms faced a broader set of challenges, particularly on the demand side. While 65 percent of affected service firms cited higher fuel costs, 56 percent also pointed to heightened uncertainty and 45 percent to reduced customer demand, a notably higher share than among manufacturing firms.

One food services firm stated, “Customers are trading down on menu items. Increased inflation will put pressure on customers’ buying. I expect some restaurants may close their doors because of the inflation cost.”

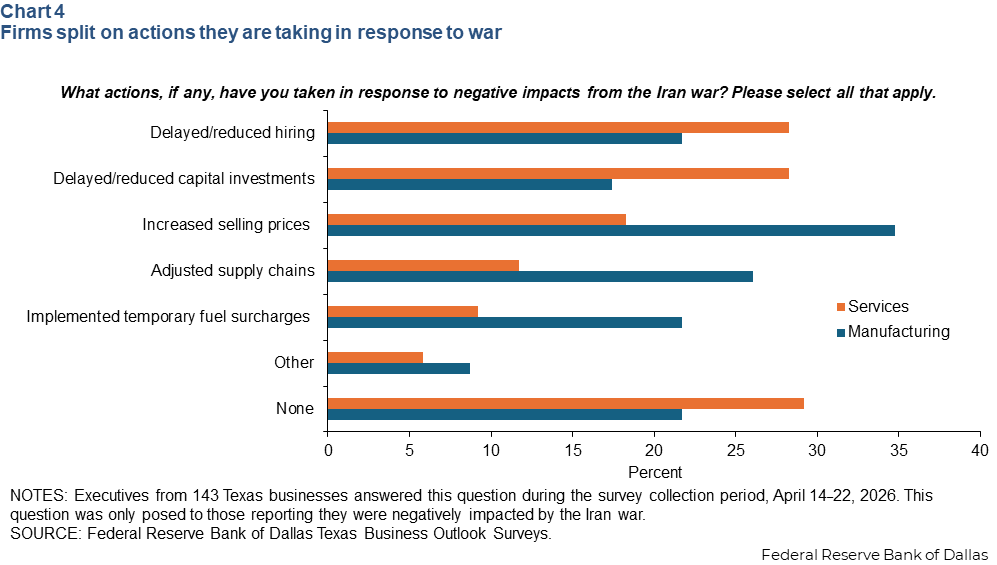

Responses to the war also differed by sector. Facing more cost increases, manufacturers gravitated towards raising selling prices (35 percent), while service sector firms leaned more toward delaying or reducing activities such as capital investment (28 percent) and hiring (28 percent) (Chart 4).

Still, among the firms already negatively impacted by the war, a meaningful share has yet to act. Some of this hesitation may be due to uncertainty surrounding the permanence of disruptions.

Not all Texas businesses are suffering, however. A small share of firms (6 percent) reported a net positive impact from the war, partly driven by increased activity in the oil and gas sector. Several chemical manufacturers also noted positive impacts from higher prices and greater demand for domestic production amid global supply constraints.

While higher oil prices typically benefit Texas given the state's role as an energy producer, there is reason to believe that the positive impacts will be less pronounced this time. The state's economy is more diversified than during past oil shocks, and oil and gas production is now more efficient, requiring fewer employees.

More importantly, significant uncertainty remains about how long elevated oil prices will persist. The lengthy lag time—typically 6–8 months—required for new production to reach major pipeline networks means that producers are often hesitant to ramp up output in response to what may be transitory price shocks.

Business activity resilient despite impacts from war

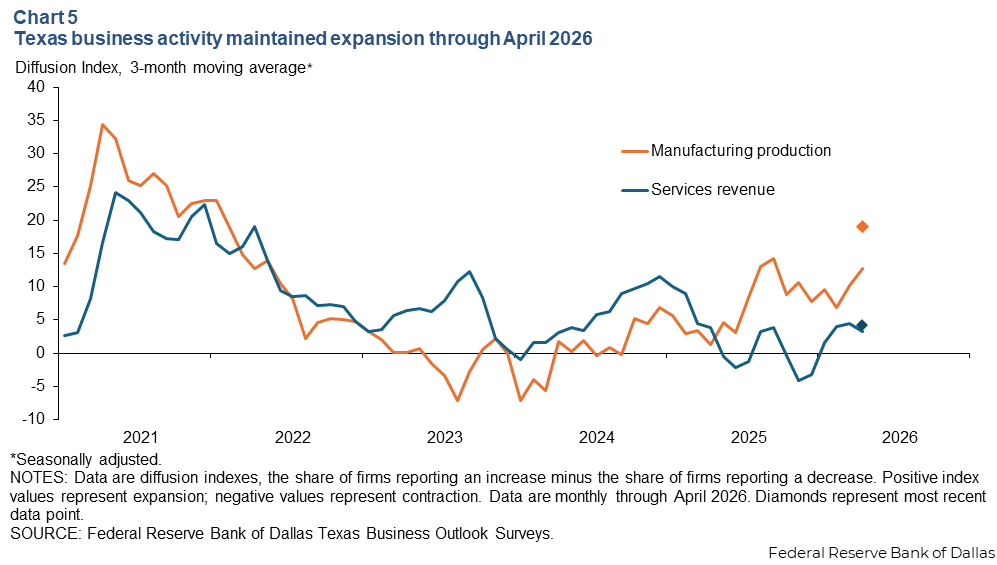

Despite Iran war-related disruption, headline indicators from the April TBOS point to economic resilience (Chart 5). On the manufacturing side, the headline production index jumped to 19.0 in April from 6.8 in March, well above the series average of 9.6. The new orders index was also positive for a fourth consecutive month and above its historical average.

This sustained improvement in new orders is notable as it points to likely future increases in production activity. The rise in manufacturing activity this year is likely due to the release of pent-up demand from delayed projects, onshoring production and AI-related infrastructure build-out.

The service sector tells a similar, though less pronounced, story. The headline revenue index edged up three points to 4.3 in April, suggesting revenue increased slightly.

The road ahead: resilience under pressure

Early evidence from 2026 suggests that the Texas economy entered the year on firmer footing than in 2025. Employment growth has picked up, and the jobless rate remains low and stable. The TBOS headline indexes show that business activity continues to expand despite negative impacts from the Iran war.

However, several factors warrant careful monitoring in the months ahead. The war's most visible effects, including higher fuel costs and heightened uncertainty, could erode some of the state's positive economic momentum. Key indicators to watch for include whether staffing services growth translates into permanent hiring, and whether labor force participation stabilizes or declines further.

While Texas businesses have demonstrated notable resilience thus far, the durability of this activity will depend largely on how quickly geopolitical tensions ease and whether cost pressures moderate.

About the authors

Isabel Brizuela is a business economist in the Research Department of the Federal Reserve Bank of Dallas.

Ethan Dixon is a research analyst in the Research Department at the Federal Reserve Bank of Dallas.