Capital flowed from emerging markets as pandemic, economic cycle took hold

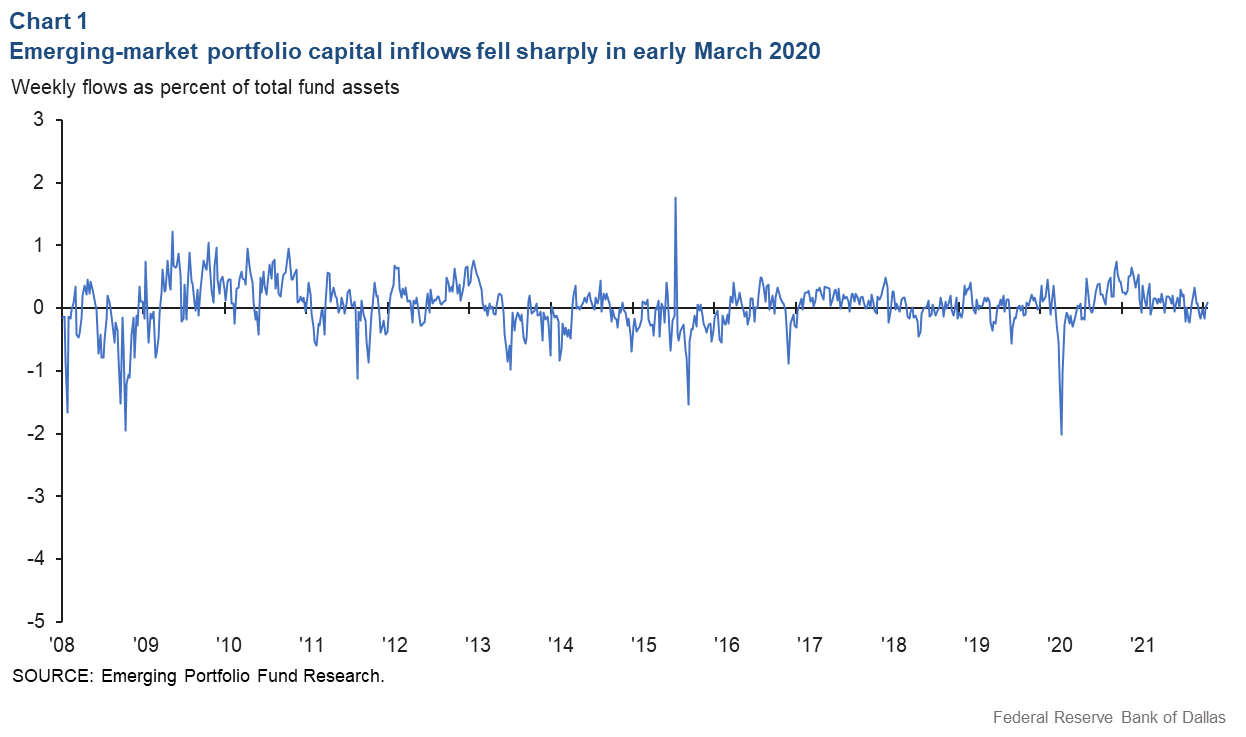

Weekly portfolio capital inflows to emerging-market economies fell sharply as the COVID-19 pandemic shook the global economy in March 2020.

The drop was comparable to that during the depths of the Global Financial Crisis in 2008, based on data for a sample of 24 emerging-market economies compiled by Emerging Portfolio Fund Research and used here as a proxy for capital flows (Chart 1). The data show movement into emerging-market bond and equity mutual funds and exchange-traded funds (ETFs). In the third week of March 2020 and in the second week of October 2008, weekly portfolio outflows from emerging-market funds totaled nearly 2 percent of the funds’ total assets under management.

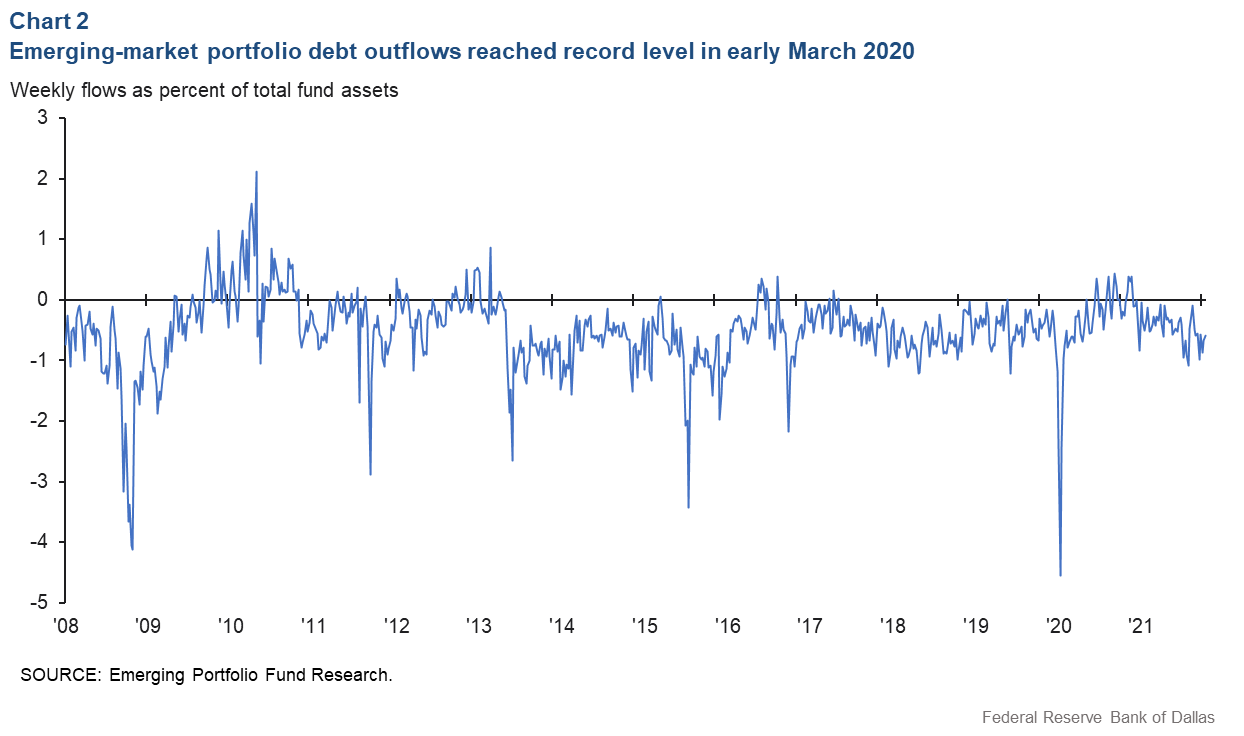

This pace of capital outflows is even more dramatic when focusing on portfolio debt flows—that is, outflows from emerging-market bond funds. The weekly pace of bond fund outflows in March 2020 was more than 4.5 percent of total assets (Chart 2). That exceeded the pace from previous crisis episodes of the past 15 years—the Global Financial Crisis, the 2011 euro-area crisis, the 2013 “taper tantrum” and the 2015 Chinese renminbi devaluation.

Cycles in international capital flows tend to track the cycles in world risky-asset prices, commonly referred to as the global financial cycle. In a recent Dallas Fed working paper, we find that fluctuations in the global financial cycle, reflecting impacts from the COVID crisis, account for roughly one-third of the movement in emerging-market inflows during 2020–23.

We arrive at this conclusion by examining global risky-asset prices and capital flows around the COVID crisis and asking three questions:

- How did the global financial cycle behave during the COVID crisis?

- What features of an economy made it vulnerable to a sharp drop in capital inflows during the COVID crisis?

- How well do fluctuations in the global financial cycle explain capital flows during the COVID crisis?

Global financial cycle accompanied COVID crisis

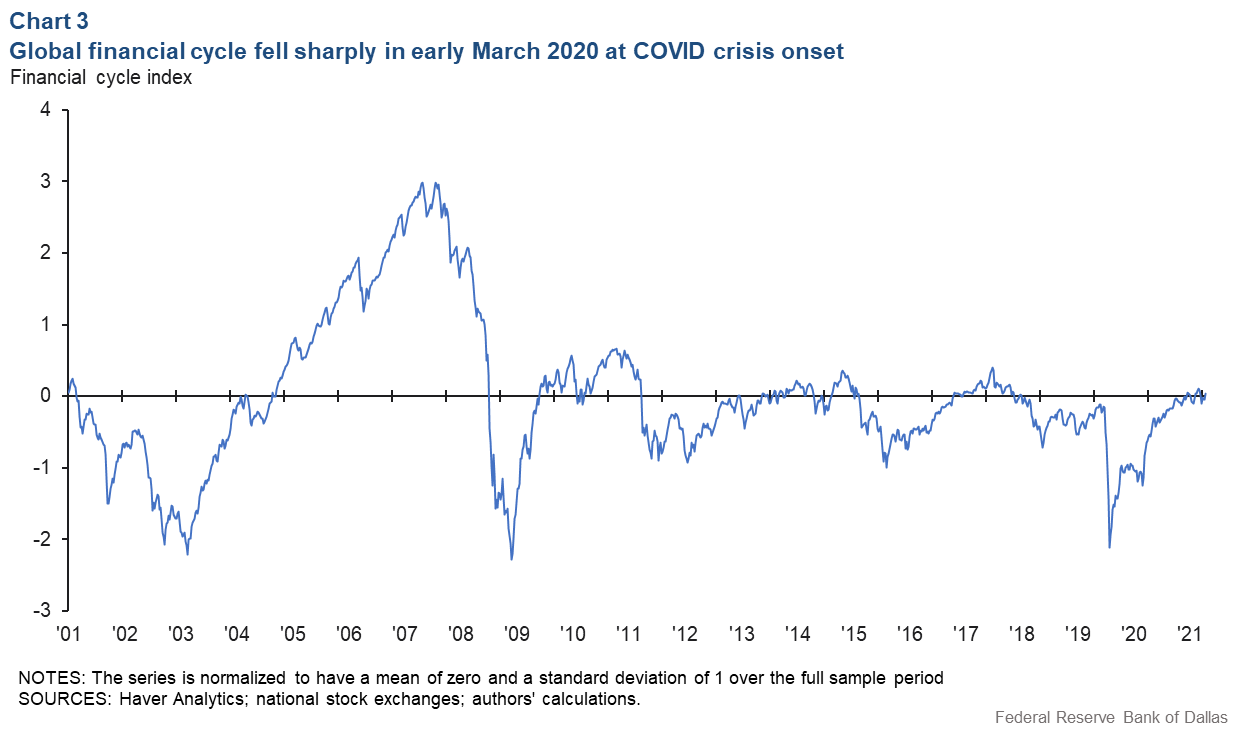

Silvia Miranda-Agrippino and Hèléne Rey (“U.S. monetary policy and the global financial cycle”) measure the global financial cycle as the common trend in a panel of world risky-asset prices. These authors view this common component at a monthly frequency, which for most research questions is more than adequate. However, to measure the global financial cycle around the COVID crisis, we extract a common trend from a panel of stock market indexes in 52 countries at a weekly frequency.

Chart 3 presents this weekly global financial-cycle index, which is normalized to have a mean of zero and a standard deviation of one (meaning the area where roughly two-thirds of readings fall). We observe a two-standard-deviation fall (encompassing roughly 95 percent of results) in this common component of global risky-asset prices over a four-week period from mid-February to mid-March 2020.

During our overall sample period, which begins in 2001, the only comparable global risky-asset price decline in magnitude and speed was a two-standard-deviation index decline over an eight-week period in September and October 2008 (the midst of the Global Financial Crisis).

Looking at risky-asset price data less frequently would mix the crash in the global financial-cycle index in early March 2020 with a partial recovery that started later that same month. When using the same risky-asset price data aggregated at a monthly frequency, we observe only a 1.5 standard-deviation fall in the global financial cycle over February and March 2020.

A country’s vulnerability to a capital inflows decline

We are particularly interested to learn how much a country’s portfolio capital inflows fall after global risky-asset prices decline. To discover this, we regress the weekly change in a country’s portfolio capital inflows on the weekly change in the global financial-cycle index to estimate the elasticity, or sensitivity, of a country’s capital flows with respect to fluctuations in the global financial cycle.

We find that, on average, weekly outflows from emerging-market debt or equity funds were about 2 percent of total assets in response to a one-standard-deviation fall in the global financial-cycle index. This figure was about 2.5 percent when focusing on outflows from debt funds. These estimates are consistent with the statistics presented earlier detailing the sizable fall in emerging-market portfolio flows and debt flows in response to the two-standard-deviation fall in the global financial-cycle index at the onset of the COVID crisis.Our regression analysis also highlights important cross-country differences in the sensitivity of a country’s capital inflows to fluctuations in the global financial cycle. We find, in line with other studies, that macroeconomic factors such as a country’s current account balance (total of bought and sold goods, services and financial transactions) or a country’s net foreign-asset position largely affected how a country’s capital inflows responded to a downturn in global risky-asset prices.

All else equal, an increase in the ratio of the current account to GDP of 1 percentage point lowers the elasticity of a country’s total portfolio inflows by about 0.04 percentage points of total assets. (A positive current account means a country makes more than it expends; a negative one means the country expends more than it takes in.)

In other words, comparing a country with a current account deficit of 5 percent of GDP and one with a current account surplus of 5 percent of GDP, the portfolio capital inflows would be about 0.4 percentage points lower in the deficit country in response to a one-standard-deviation fall in the global financial cycle.

Moreover, this response would be 0.8 percentage points greater following the two-standard-deviation fall in the global financial-cycle index at the onset of the COVID crisis. In the context of average portfolio outflows of 2 percent at the start of the COVID crisis shown in Chart 1, our estimates suggest that cross-country differences in the current account balance explain a substantial portion of the differences in capital flow responses.

The heterogeneity in capital flow responses appears even more substantial when focusing on portfolio debt flows. All else equal, an increase in the current-account-to-GDP ratio of 1 percentage point lowers the elasticity of a country’s portfolio debt inflows by about 0.09 percentage points of total assets. Comparing a country with a current account deficit of 5 percent of GDP and one with a current account surplus of 5 percent of GDP, portfolio debt outflows would be about 1.8 percentage points higher in the current-account-deficit country at the onset of the COVID crisis.

While the effect of macroeconomic fundamentals such as current account balances on a country’s capital outflows has been well-documented, we also ask if measures capturing the intensity of the COVID pandemic—like the weekly changes in new COVID cases normalized by population—affect the response of a country’s portfolio capital inflows to a decline in the global financial-cycle index.

We estimate that, all else equal, a doubling of the weekly new COVID cases—common at the beginning of new infection waves—raises the elasticity of a country’s total portfolio inflows by 0.5 percentage points of total assets. In other words, all else equal, at the global onset of the COVID crisis in March 2020, a country whose infection counts were doubling every week would see a 1 percentage-point greater fall in capital inflows than a country where COVID case counts remained stable.

Given that the global financial-cycle index fell by two standard deviations at the onset of the COVID crisis, rapid increases in COVID cases appear to have had a similar effect as a large current account deficit on capital inflows to a given emerging-market economy.

Financial-cycle fluctuations’ impact on portfolio capital inflows

Finally, we can ask how well fluctuations in the global financial cycle explain the portfolio capital inflows to emerging markets, and if this relationship changed during the COVID crisis.

We calculate the goodness-of-fit from our regression model. When regressing the weekly change in portfolio inflows on its own lags and country-fixed effects—but without the global financial-cycle factor over our entire 2001–21 sample period—the goodness-of-fit is about 0.20. In other words, lags and fixed effects alone can explain about 20 percent of the fluctuations in the weekly change in emerging-market portfolio capital inflows.

But when the global financial-cycle factor is added to this regression, the goodness-of-fit jumps to 0.45. Therefore, the global financial cycle explains roughly a fourth of the fluctuations in emerging-market portfolio capital inflows over our full sample.

The quantitative importance of the global financial cycle in explaining fluctuations in portfolio capital inflows is even greater over the last two years of our sample period, 2020–21. When adding the global financial-cycle factor as an explanatory variable, the goodness-of-fit of the model increases from 0.17 to 0.50. Therefore, the global financial cycle explains roughly one-third of fluctuations in emerging-market portfolio capital inflows during last two years in our sample that encompasses the COVID crisis.

About the Authors

The views expressed are those of the authors and should not be attributed to the Federal Reserve Bank of Dallas or the Federal Reserve System.