Arbitrage limits heighten dollar shortages abroad during volatile times

U.S. dollars are hard to find in foreign markets during times of heightened risk, as evidenced by two interesting and related features in the post-2007 international financial landscape.

The first feature, persistent and positive deviations in covered interest parity (CIP), involves episodes of persistent differences between the cost of borrowing dollars in the U.S. market and the cost of borrowing abroad.

The second feature is dollar appreciation in times of heightened risk or risk aversion. In a recent theoretical paper, we show how the two features relate closely and signal a dollar shortage abroad as risk increases.

Positive covered interest parity deviations since 2007

A borrower requiring dollars for a short term can borrow them in the onshore or offshore markets. For those with access to the U.S. onshore market, the cost to borrow dollars is the U.S. interbank interest rate (the rate at which banks lend among themselves). Those lacking U.S. market access can, instead, obtain dollars in the offshore market through synthetic dollar borrowing.

For a synthetic dollar transaction, one borrows a foreign currency, such as euros, and uses the swaps market to convert those euros into dollars. Taking the process step by step, the holder of the borrowed euros converts them into dollars on the spot market at the spot exchange rate and simultaneously enters into a forward contract to convert the dollars back into euros at a specified future date at the forward exchange rate. Those proceeds of the swap repay the original euro debt.

The cost of this synthetic dollar borrowing is the euro interbank interest rate plus the forward premium, the difference between the forward and spot exchange rates. The forward rate is known when the contract is entered into, so there is no uncertainty. And if counterparty risk is negligible—that is, the risk of dealing with the party on the other side of the swap—borrowing dollars directly or borrowing dollars synthetically are both risk-free transactions.

In a world of effective international arbitrage, these two methods of obtaining dollars should cost the same. If there was a positive spread between the synthetic dollar borrowing rate and the U.S. onshore rate, banks with access to the onshore dollar market would borrow dollars onshore and lend them synthetically via a swap transaction, reducing the spread.

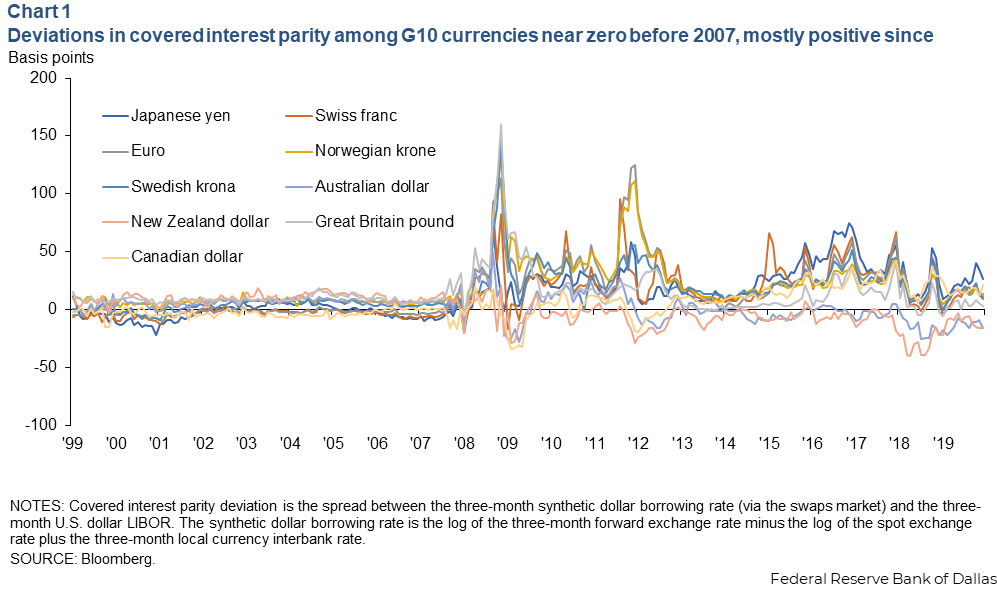

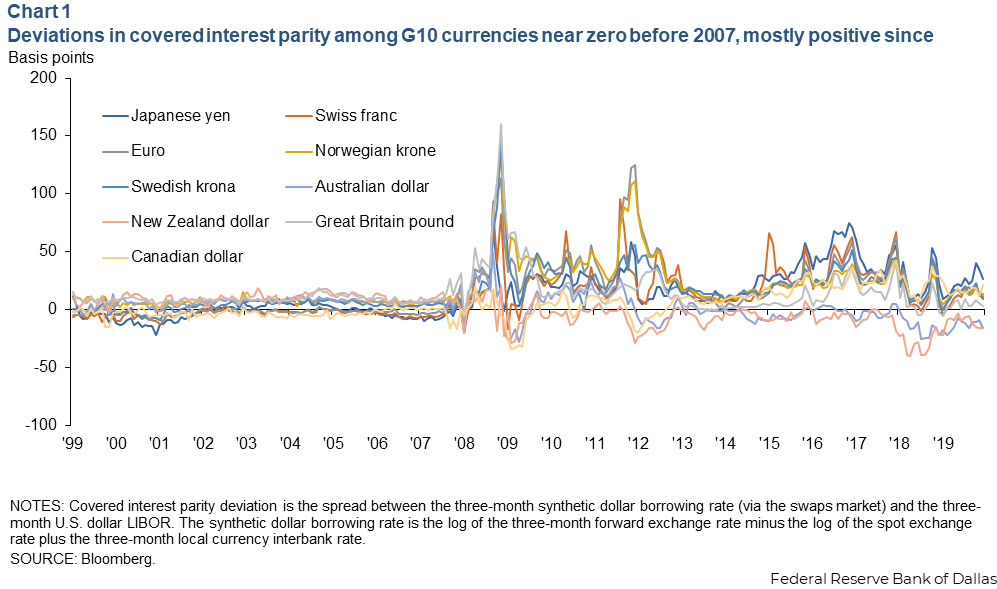

If these banks were unconstrained, then CIP arbitrage would be perfect and any potential arbitrage profits would be reduced to zero, as was the case before 2007 (Chart 1).

Among the Group of 10 industrialized nations (G10), the nearly zero deviations before 2007 indicate a borrower would pay the same rate for borrowing dollars directly in the U.S. market as for borrowing synthetic dollars in a foreign market. For the past 15 years, CIP deviations have been generally positive and variable. Moreover, these spreads are positively correlated with a measure of risk, the VIX (the Chicago Board Options Exchange’s volatility index), meaning these spreads increase when risk increases.

Dollar appreciation during risk-off episodes

The second interesting development in international markets since the Global Financial Crisis (2007–08) has been the safe haven role of the U.S. dollar. Post-2007, the dollar appreciates against most currencies during a time of heightened risk or risk aversion, what is known as a “risk-off” episode in the markets.

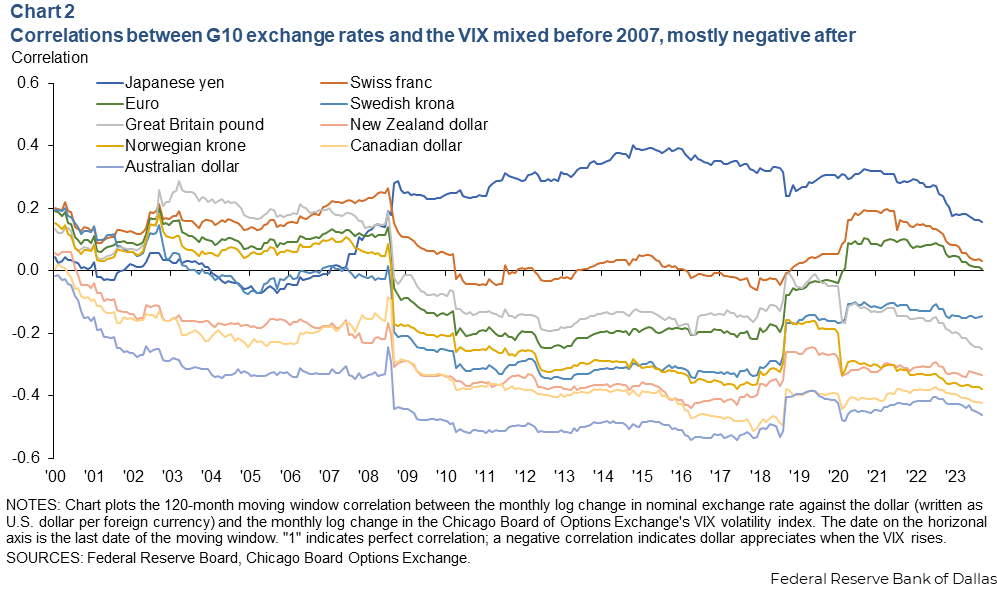

Chart 2 plots the 10-year moving window correlation between the monthly percent change in the nominal exchange rate against the dollar and the monthly percent change in the VIX for each of the G10 currencies. The exchange rates are written as U.S. dollars per foreign currency unit, so a negative correlation means the dollar appreciates when the VIX rises.

Before 2007, these correlations were mixed; the correlation was positive for about half of the G10 currencies and negative for half. This changed in 2008, when there was an abrupt negative shift in the correlations for each of these currencies except for the Japanese yen.

Since then, nearly all of these correlations have been negative, with the exceptions of the yen and occasionally the Swiss franc. Interestingly, the correlation between the euro and the VIX has turned positive over the past few years.

How are these developments related?

What explains these changes, and why did they occur so suddenly after 2007? In our recent paper, we set out to answer this question. The answer in two words: market segmentation.

Before the Global Financial Crisis, the U.S. dollar funding market was globally integrated, driven by effective international arbitrage. However, in the aftermath of the crisis, a significant transformation occurred, leading to a segmentation between onshore and offshore dollar markets.

To show this, we developed a two-country general equilibrium model in which both the spot exchange rate and the CIP deviation are determined endogenously. Markets are segmented in the sense that there is an onshore and an offshore dollar market, and there may be imperfect arbitrage between the two.

We then consider how an increased demand for liquidity—a global "dash for cash"—would affect the dollar exchange rate and equilibrium CIP deviations. For U.S. borrowers, Federal Reserve liquidity facilities, whereby the central bank ensures dollar availability to key U.S. market participants during periods of market duress, can easily provide dollar liquidity. But these Fed liquidity facilities are unavailable to foreign borrowers, and while a foreign central bank can provide liquidity in its domestic currency, it cannot provide dollar liquidity.

This feature means an excess demand for dollar liquidity can develop abroad. This would lead to a positive spread between the cost of borrowing dollars abroad and in the U.S.

If global banks were unconstrained, this potential arbitrage opportunity would be driven to zero. While the Fed’s liquidity facilities may only be available to borrowers’ onshore dollar market, global CIP arbitrage will satisfy any excess demand for dollar liquidity abroad by borrowing dollars from the U.S. market and lending them abroad.

But if global banks face leverage constraints, which the economics literature suggests have arisen in part due to new financial regulations since the 2008 crisis, their ability to exploit this arbitrage is limited. In such instances, equilibrium CIP deviations can occur. These deviations widen when liquidity demands increase.

A higher interest rate for borrowing dollars abroad, in turn, leads to a dollar appreciation. Borrowers outside the U.S. may demand more U.S. dollars, possibly to hold more dollar cash balances or to repay dollar debt from a previous period.

When widening equilibrium CIP deviations raise the cost of borrowing dollars, borrowers will move to instead buy dollars on the spot market. This spot market demand leads to dollar appreciation. In equilibrium, the spot exchange rate will increase to the point that borrowers are indifferent to borrowing dollars when the CIP deviation is high or buying dollars when the currency is expensive.

Central bank swap lines lessen this segmentation

Key to market segmentation in the model is the restriction that the Fed’s liquidity facilities are inaccessible to offshore market borrowers. However, the Fed can enter into arrangements with other central banks. Central bank dollar liquidity swaps allow the Fed and a foreign central bank to swap a certain amount of currency for a short period. This allows the foreign central bank to provide dollar liquidity to its domestic borrowers.

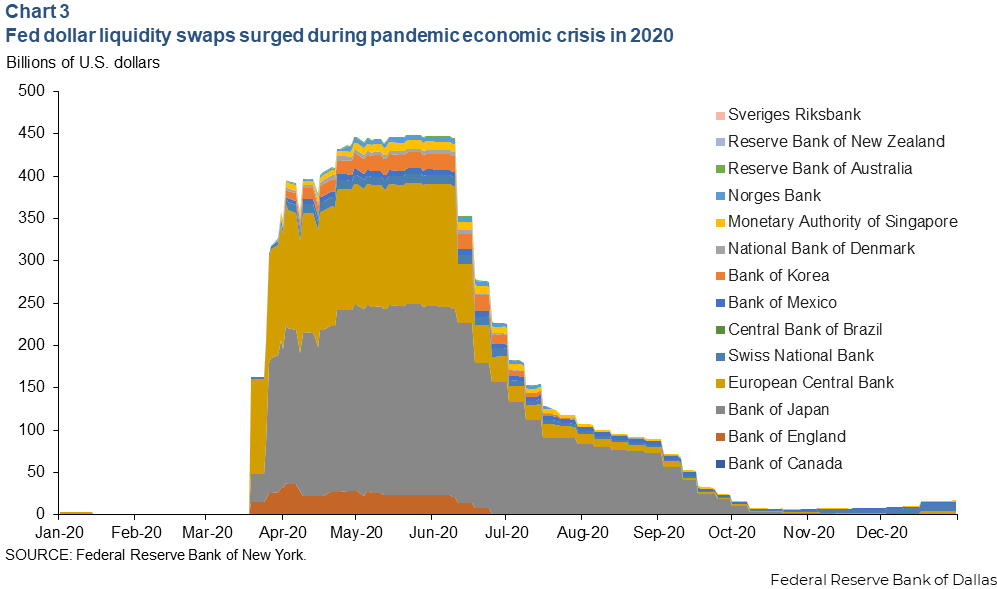

Chart 3 plots the value of dollar liquidity swaps outstanding with foreign central banks through 2020. The Fed and foreign central banks began introducing swap lines on a temporary and limited basis in the 2007–08 crisis, and since 2013, the Fed has had permanent dollar liquidity lines with five foreign central banks: the Bank of Canada, the Bank of England, the Bank of Japan, the European Central Bank and the Swiss National Bank. In late March 2020, at the height of the pandemic, the Fed opened temporary dollar swap lines with nine additional central banks.

The pandemic crisis sparked a global dash for cash, and an excess demand for dollars developed abroad. In response, central banks utilized dollar liquidity swap lines with the Fed, and the outstanding amount of dollar liquidity swaps between them surged in March 2020, before dissipating and returning to near zero by the end of 2020.

Such excess demand for dollars may have been supplied by the private sector through CIP arbitrage in prior years. Constraints on CIP arbitrage have led to positive and persistent equilibrium CIP deviations; this has opened a new role for the Fed to provide dollar liquidity to the rest of the world through central bank dollar liquidity swaps.

About the authors

The views expressed are those of the authors and should not be attributed to the Federal Reserve Bank of Dallas or the Federal Reserve System.

{kind=link}