Disparate supply-side forces gave U.S. economy an edge

The U.S. economy boasts robust growth and slowing inflation despite the highest interest rates in two decades. Such performance isn’t common globally, especially among other advanced economies, revealing crucial differences in the fundamental factors driving inflation and growth.

The Federal Open Market Committee increased the Federal Reserve’s policy rate, known as the federal funds rate, by 525 basis points (5.25 percentage points) over 11 meetings from March 2022 to July 2023. These moves were quickly followed by similar actions worldwide to rein in high inflation and return it to target levels.

We find that disinflation in the U.S. and other economies has been underway since at least June 2022. However, the impact of monetary policy on aggregate demand has varied. Furthermore, the unwinding of pandemic-era supply-chain dislocations has boosted aggregate supply in the U.S. more than in other economies, mitigating the impact of tighter financial conditions.

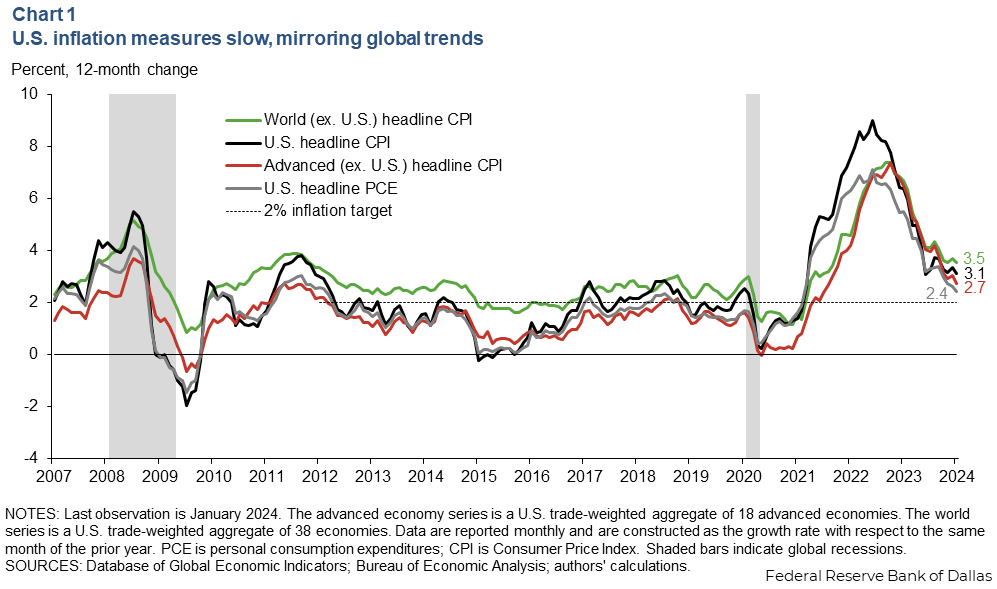

Tracking the U.S., global disinflation

The Federal Reserve Bank of Dallas’ Database of Global Economic Indicators (DGEI) derives aggregates of economic indicators for advanced economies and the world using U.S. trade weights. Each country’s influence on a given aggregate is based on how much it trades with the U.S. Removing the U.S. from these aggregates enables the identification of global trends the U.S. doesn’t directly drive, but ones global shocks or U.S. spillovers indirectly influence.

Different inflation measures are often considered. The Federal Reserve prefers personal consumption expenditures (PCE) inflation over Consumer Price Index (CPI) inflation, unlike most other central banks. PCE inflation covers a broader range of expenditures and employs chained-weighted indexes—reflecting the relative quantities of goods purchased—to depict consumer substitution patterns more accurately. Headline inflation is often contrasted with core inflation, excluding food and energy prices that are largely determined in international commodity markets.

All U.S. inflation measures have fallen sharply, with the declines beginning in mid-2022 leading other advanced economies and the rest of the world, according to DGEI data (Chart 1).

Although headline and core measures of U.S. PCE inflation are lower than CPI inflation (0.7 percentage points for headline, 1.1 percentage points for core in January 2024), prices remain above the Fed’s 2 percent inflation target.

U.S. CPI disinflation, measured from the mid-2002 peak, has exceeded that of representative U.S. trading partners.Diverging patterns of global growth point to disparate supply-side forces

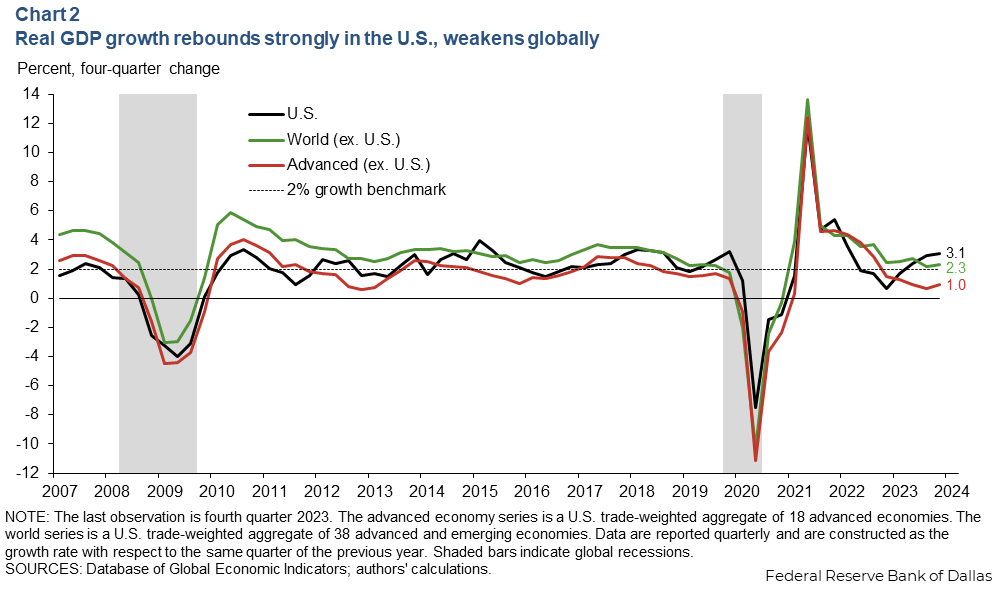

Tighter financial conditions tend to contribute to sluggish growth. However, the U.S. bucked this trend in 2023, experiencing a stronger-than-expected upswing (Chart 2).

By comparison, global growth softened in 2023, with just 1.0 percent four-quarter growth for other advanced economies and 2.3 percent for the rest of the world in the fourth quarter, the latest date for which global data are available. Both measures considerably trailed the U.S. 3.1 percent growth rate.

The U.S. growth advantage over the rest of the world in the second half of 2023 rarely occurs in the 16 years of data plotted in Chart 2 because the world aggregate includes major emerging economies that generally grow faster as they catch up to advanced countries’ standard of living. This divergence became especially apparent in recent quarters, leading some economists to argue that the U.S. might have tightened monetary policy less than many observers thought. (This could occur if the U.S. natural rate of interest (r-star)—the rate at which the policy rate is neither restrictive nor accommodative—increased as well.)Alternatively, the U.S. data could indicate that monetary policy is either working with variable lags or the pass-through of interest rates to economic activity has been weaker than in the past or than in other countries. There are also potentially nonmonetary-policy-related factors that may have driven a number of price changes—factors, for example, felt most directly in Europe and tied to Ukraine–Russia war-related disruptions.

Supply and demand help explain output, price shifts

Looking at how real (inflation-adjusted) GDP growth and inflation have behaved across countries indicates significant differences from prepandemic trends.

While monetary policy is assumed to primarily operate through shifts in aggregate demand, the international data suggest a different combination of factors has affected the U.S. and global economies following the pandemic, highlighting the significance of supply-side forces.

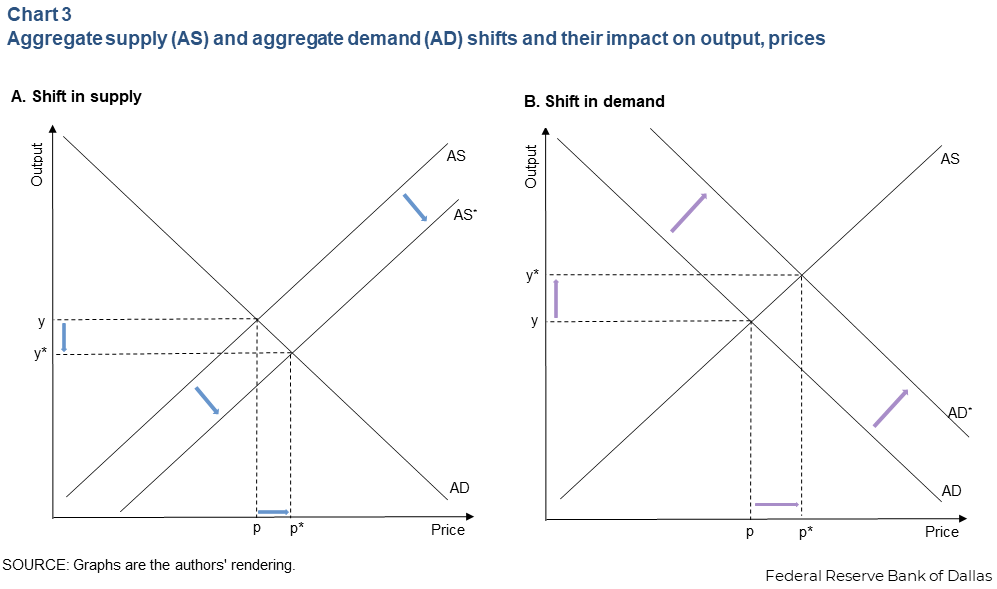

To examine this point more closely, we draw upon a graphical tool from standard macroeconomic theory (and from richer models with a capital accumulation mechanism). Chart 3 displays two intersecting lines, the aggregate demand (AD) curve and the aggregate supply (AS) curve. The horizontal axis represents the overall price level, while the vertical axis depicts the level of output or real GDP.

The AD curve slopes downward from left to right, indicating that as price decreases, the quantity of goods and services demanded by consumers increases. The AS curve typically slopes upward, indicating that as price increases, producers are willing to supply more output.

In the long run, the AS curve tends to become vertical, as long-run GDP is determined by factors such as technology or the labor force that do not respond to prices. The equilibrium, where the AD and AS curves intersect, represents a balanced point in the economy where there are stable price and output levels.

Shifts in either the aggregate supply (depicted in panel A) or the aggregate demand curves (panel B) cause changes in the price level and output—that is, inflation and growth fluctuations. When supply shifts dominate, inflation and output growth tend to move in opposite directions; when demand shifts, they move in the same direction. This intuition helps us interpret the correlation between growth and inflation when considering whether supply or demand factors dominate in the data.Aggregate supply shifts explain the U.S. rebound

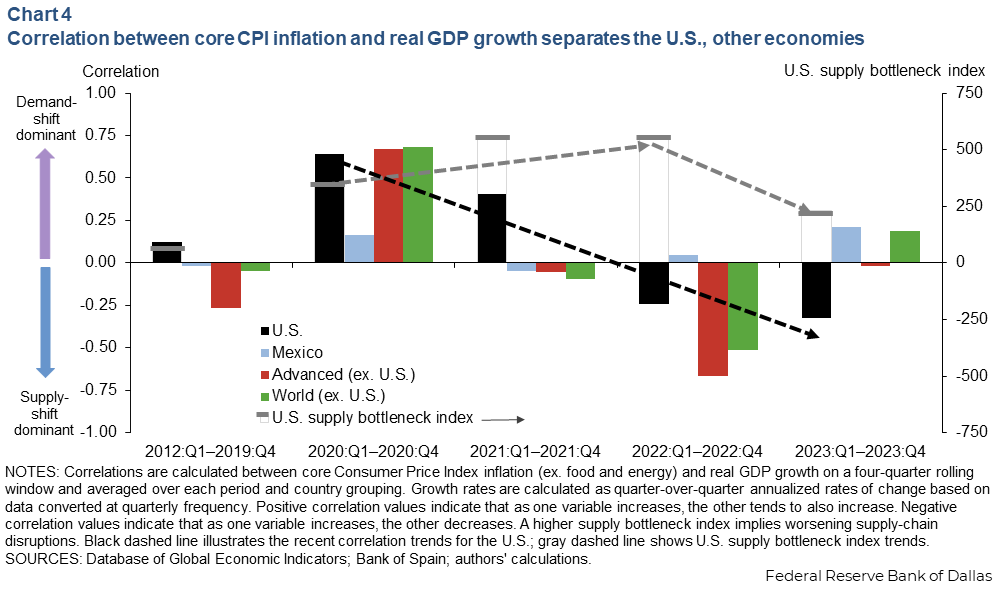

We calculate the correlations between real GDP growth and core inflation—isolated from international commodity prices—separately for each of the advanced (ex. U.S.) and the world (ex. U.S.) aggregates and the U.S. over rolling four-quarter periods and covering the prepandemic years (Chart 4).

At the onset of the pandemic in early 2020, GDP growth and core inflation were strongly positively correlated and declining, largely reflecting demand constraints due to lockdowns and other COVID-19-related policies that depressed aggregate demand more than supply.

As restrictions eased and fiscal and monetary stimulus boosted demand, growth and inflation rebounded. From late 2020 to 2021, global supply-chain disruptions and supply-side input cost pressures became major drivers of the economy. Those forces damped the impact of fiscal and monetary policies installed to support aggregate demand, helping weaken the correlation between growth and core inflation in the U.S. and especially globally.

New supply-chain challenges arose in 2022, including the Ukraine–Russia war and related oil/commodity price pressures. Other supply-side issues became more prominent, notably China’s strict zero-tolerance COVID-19 policy, causing closure of swaths of the Chinese economy and prompting supply disruptions to dominate demand even in the U.S.

Heading into 2023, global inflation started to quickly decline as central banks pursued tighter monetary policy and some pandemic-related stimulus waned. Concurrently, GDP growth weakened in most advanced economies, while it strengthened in the U.S. possibly due to rapidly easing U.S. supply bottlenecks and above-trend immigration boosting the U.S. labor force. Moreover, the pause in policy rate increases that began in July 2023 further aids economic growth.

The evidence suggests growing importance of demand shifts outside of the U.S., with limited spillovers from the U.S. In fact, U.S. advances have not resulted in greater concordance of the U.S. economic cycle with that of Mexico, the largest U.S. trading partner. Notably, Mexico’s experience appears more like the rest of the world.

Supply recovery cushioned tightening financial conditions

The trajectory of U.S. real GDP growth and inflation suggests a soft landing remains plausible, despite lingering uncertainty and consumer angst. The Fed’s more-restrictive monetary policy stance since early 2022 has contributed to abating inflationary pressures, while easing supply-chain disruptions have spurred growth.

From this perspective, recent U.S. economic strength has less to do with oil/commodity prices or with monetary policy transmission and more with favorable supply-side conditions than those of other nations more directly exposed to various global crises. As global supply conditions normalize and the U.S. nears prepandemic conditions, future inflation reduction becomes harder without further softening aggregate demand.

Supply challenges impacting GDP growth and inflation could also reemerge. For example, they might be driven by factors such as geopolitical instability in the Middle East affecting trade through the Suez Canal and/or climate-related challenges such as drought constraining shipping through the Panama Canal.

About the authors

Enrique Martínez García is an economic policy advisor in the Research Department at the Federal Reserve Bank of Dallas.

Braden Strackman is a research analyst in the Research Department at the Federal Reserve Bank of Dallas.

The views expressed are those of the author and should not be attributed to the Federal Reserve Bank of Dallas or the Federal Reserve System.