U.S. battery industry cuts losses, shifts to new ventures amid EV bust

The future of the U.S. battery industry looked extremely promising several years ago. Consumer interest in electric vehicles (EVs) was rising, and the Inflation Reduction Act, passed in 2022, provided incentives for the domestic production of lithium-ion batteries that would power those vehicles.

Automakers responded with bold pledges to increase sales of EVs, pledges that were mirrored by major investment in gigafactories (enormous factories for producing lithium-ion batteries). More than 20 gigafactories were announced in the U.S. from 2021 through 2022, representing more than $50 billion in potential investment and thousands of new jobs. More announcements followed in 2023 and 2024.

Over the past year, though, it has become clear these ambitions will not be realized, and automakers and battery companies are reassessing the future. Many companies have made painful cutbacks. At the same time, those battery manufacturers in the right position are shifting toward new opportunities, some that do not rely on the EV market for success.

Expectations for U.S. EV demand reset

Until recently, almost all announced gigafactories in the U.S. were intended to produce batteries for EVs, tying their economic fortunes to automakers' ability to sell a sufficiently large number of those vehicles.

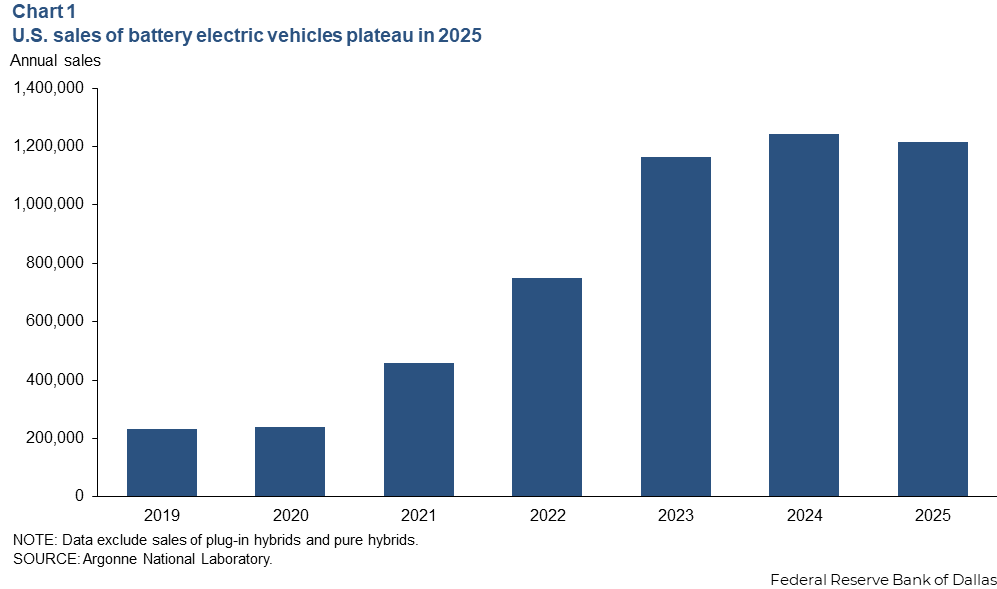

U.S. sales of EVs rose rapidly from 2021 through 2023 and exceeded 1 million vehicles by 2023, making up 7.5 percent of total auto sales (Chart 1). Many new EVs carried lower price tags and traveled at greater range than their predecessors, increasing their attractiveness to consumers. Government subsidies helped support demand.

However, the pace of growth slowed substantially in 2024 and essentially plateaued in 2025. Despite efforts to introduce EVs of sufficient quality and low enough price to convince U.S. consumers to switch en masse from gasoline-powered cars, automakers couldn’t get more buyers to do so.

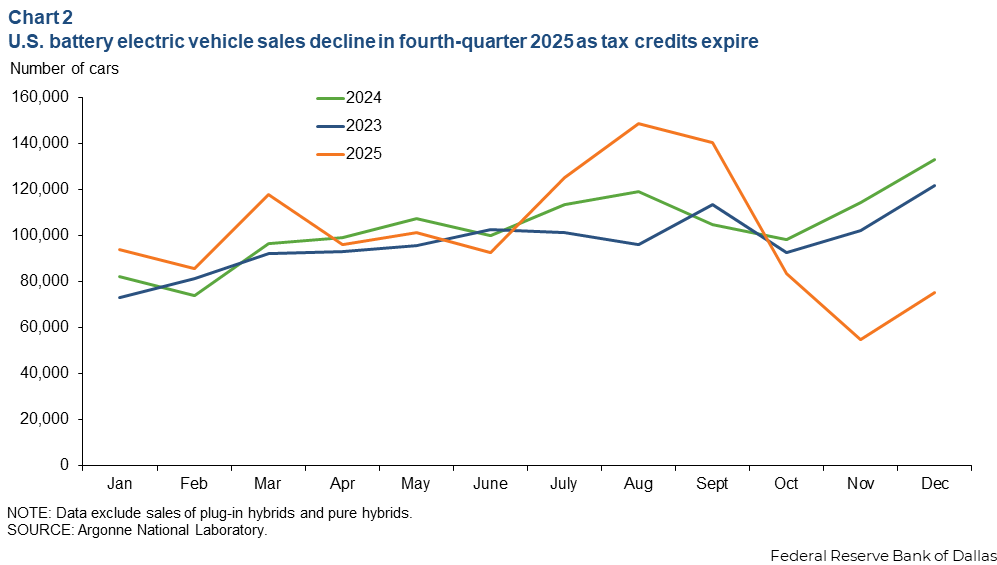

Recent federal policy changes have also affected sales. Consumer subsidies for purchasing EVs, originally scheduled to expire in 2032, were instead eliminated at the end of September 2025. Sales were unusually high preceding the expiration deadline and then dropped precipitously (Chart 2).

Current sales of EVs are insufficient to justify the investments made in gigafactories, and the outlook does not suggest significant improvement anytime soon. Many third-party forecasters have markedly cut their demand projections for EVs in the U.S. Automakers have also acknowledged these difficulties, both by reframing their EV sales goals and by making the difficult decision to write off billions of dollars of capital investments tied to EVs and batteries.

Companies have also sought to reduce EV prices by switching to a different type of lithium-ion battery. Historically, U.S. automakers have emphasized nickel-manganese-cobalt or nickel-cobalt-aluminum batteries, which store more energy per unit of mass than most other types of lithium-ion batteries. This translates to EVs that can travel greater distances between charges, answering a key concern for many U.S. consumers. But it also boosts vehicle prices because those batteries are relatively expensive.

One alternative, commonly used in Chinese EVs, is lithium-iron-phosphate. This alternative is often cheaper than nickel-manganese-cobalt or nickel-cobalt-aluminum batteries, and Ford, GM and Tesla, among others, are actively considering these batteries to reduce vehicle costs. One drawback, at least for the time being, is the investment required to bring to market a different kind of lithium-ion battery, one that the U.S. has significantly less experience producing and whose supply chain China dominates.

Batteries for the grid become a bright spot

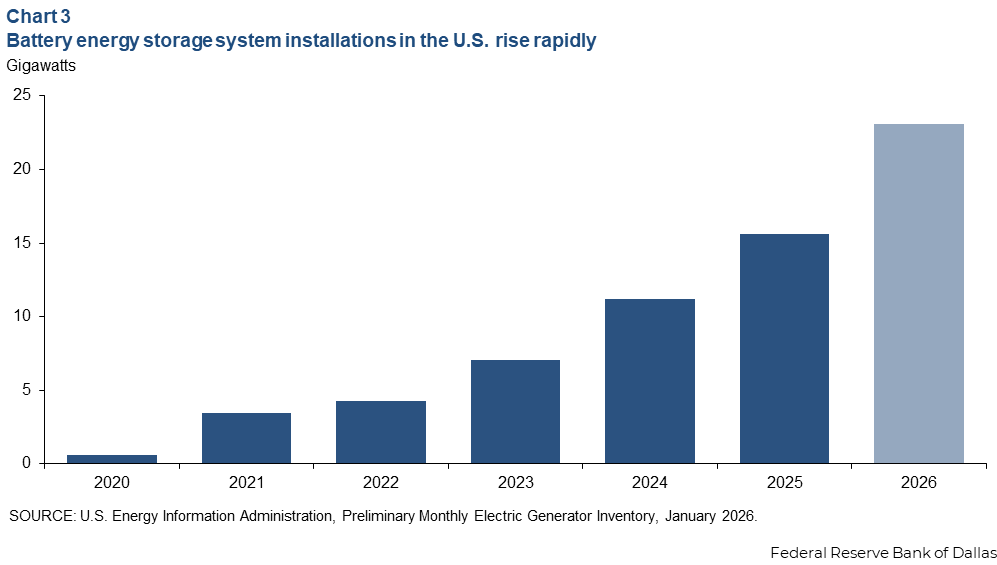

While EV sales have failed to meet expectations, the use of lithium-ion batteries in battery energy storage systems has grown rapidly, with demand expected to remain strong in 2026 (Chart 3). The systems can play a critical role in integrating intermittent renewables (solar and wind) into the grid, smoothing fluctuations in wholesale electricity prices and aiding short-term grid stability.

The number of battery installations for power storage systems has risen rapidly for at least two reasons. First, prices of lithium-ion batteries have declined dramatically in recent years, improving their economics. Second, a significant amount of utility-scale solar has been installed as well. Batteries are often viewed as especially complementary to solar power, as batteries can charge up during the early part of the day and then discharge in the evening when solar ramps down and wholesale electricity prices can spike.

There is also a growing realization that data centers will be important new users of battery energy storage systems, particularly for backup power. The electricity requirements of some proposed facilities are extremely large, requiring widespread use of batteries. For example, the proposed Stargate 1 project in Abilene, Texas, may install batteries with a total capacity of 1 gigawatt, roughly equivalent to 6 percent of all batteries installed on the grid in the U.S. in 2025.

Thus, the increasing prominence of battery storage presents a potential opportunity for U.S. battery makers, though the transition is not entirely costless. Battery storage systems commonly use a particular type of lithium-ion battery known as lithium-iron-phosphate. Because most U.S. automakers have focused their attention on other types of lithium-ion batteries, making the lithium-iron-phosphate batteries will require more investment.

Companies will also need to navigate an evolving policy landscape when thinking about these decisions. The One Big Beautiful Bill Act of 2025 maintains both a tax credit for the installation of battery energy storage systems and a tax credit that subsidizes the domestic production of batteries. In theory, these credits should be boons for domestic battery producers. However, the law also introduces restrictions on the involvement of certain foreign entities and ties access to the credits on meeting content requirements. The access rules aim to boost the use of domestically sourced inputs. The rules may prove challenging in the near term given the substantial involvement of China and Chinese companies in many parts of the battery supply chain.

Industry responds by canceling projects, changing battery types

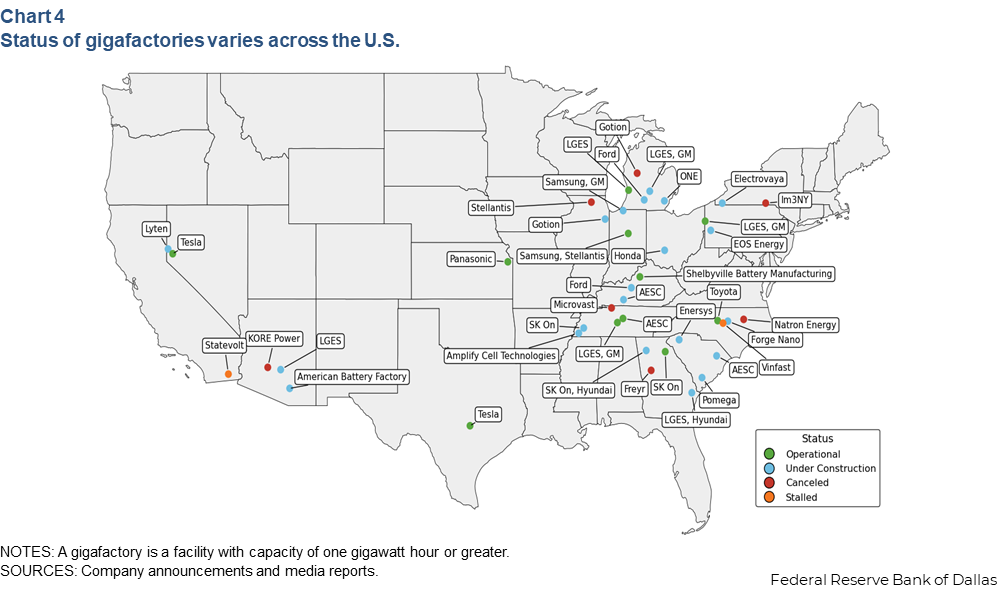

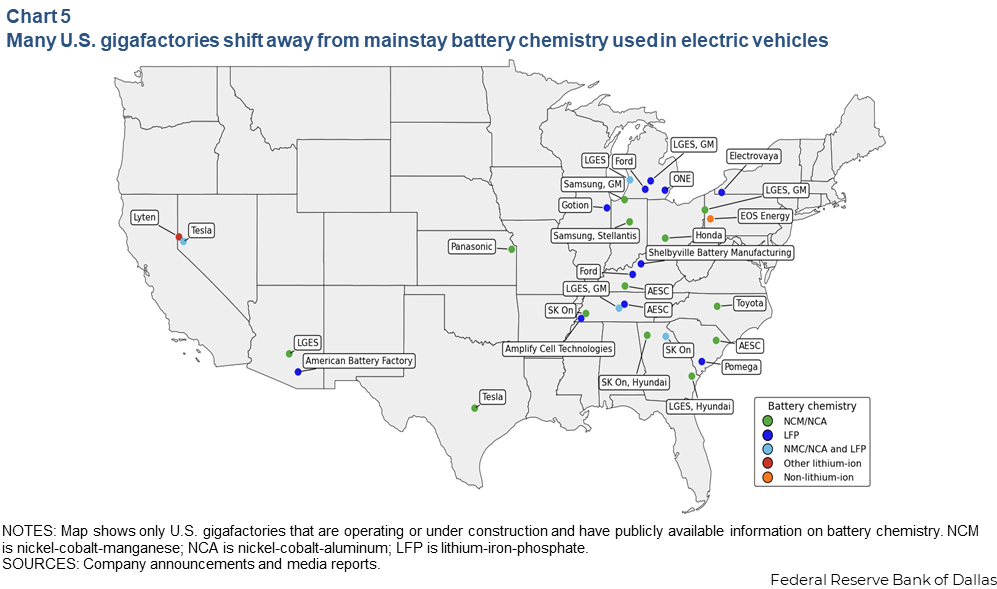

Several dozen new gigafactories in the U.S. have been announced in the past five years, leading to eventual emergence of a battery manufacturing base in the country. There are 12 plants operating and another 23 are at various stages of construction (Chart 4, green and blue dots).

Many of these plants produce the usual nickel-cobalt-manganese or nickel-cobalt-aluminum batteries used in EVs. But gigafactories associated with companies such as Tesla, LG Energy and Ford, among others, have revised their scope to include lithium-iron-phosphate production, either alongside or in place of traditional EV battery lines, to align with faster-growing battery storage system demand and the evolving EV market (Chart 5).

While some projects have made it across the finish line, many have faced setbacks reflecting new realities. Approximately 10 projects have been officially canceled or their progress has stalled, representing more than $10 billion in potential investment. The planned start dates of many plants under construction have been pushed out.

The projects under construction reflect a significant amount of potential capacity, especially when considering those focused on EVs. The fate of these plants hangs in the balance, whether they will be canceled or postponed indefinitely in 2026 due to the changing dynamics of the U.S. battery market.

About the authors

Michael Plante is an assistant vice president in the Research Department at the Federal Reserve Bank of Dallas.

Kunal Patel is a senior business economist in the Research Department at the Federal Reserve Bank of Dallas.

Isabelle Tseng is a former intern in the Research Department at the Federal Reserve Bank of Dallas.

Adefemi Abimbola is a research analyst in the Research Department at the Federal Reserve Bank of Dallas.